250 Chapter 9

unskilled labor. Each home involves framing (F), roofing (R), and finish carpentry

(FC). During recent months, A crews have demonstrated a capability of framing one

home, roofing two, and doing finish carpentry for no more than four homes per

A. Formulate the linear programming problem that DCH would use to minimize

its total labor costs per month, showing both the inequality and equality forms

of the constraint conditions.

B. Solve the linear programming problem and interpret your solution values.

C. Assuming that DCH can both buy and sell subcontracting services at prevailing

P9.4 SOLUTION

A. The problem requires minimization of total labor costs subject to constraints on home

Linear Programming 251

B. By graphing the constraints and the lowest possible isocost line, we find at the

optimal Point, X, that LR = LFC = 0.

From (3),

From (1),

And, from the objective function:

Solution values can be interpreted as follows:

252 Chapter 9

D. In general, the isocost relation for this problem is:

Where C0/CA is the intercept and –(CB/CA) is the slope coefficient.

The slope of the isocost line will fall (become less negative) as CA increases, holding

Linear Programming 253

Delmar Custom Homes

7

8

9

10

“A” Crews

FEASIBLE SPACE

Framing Constraint (1)

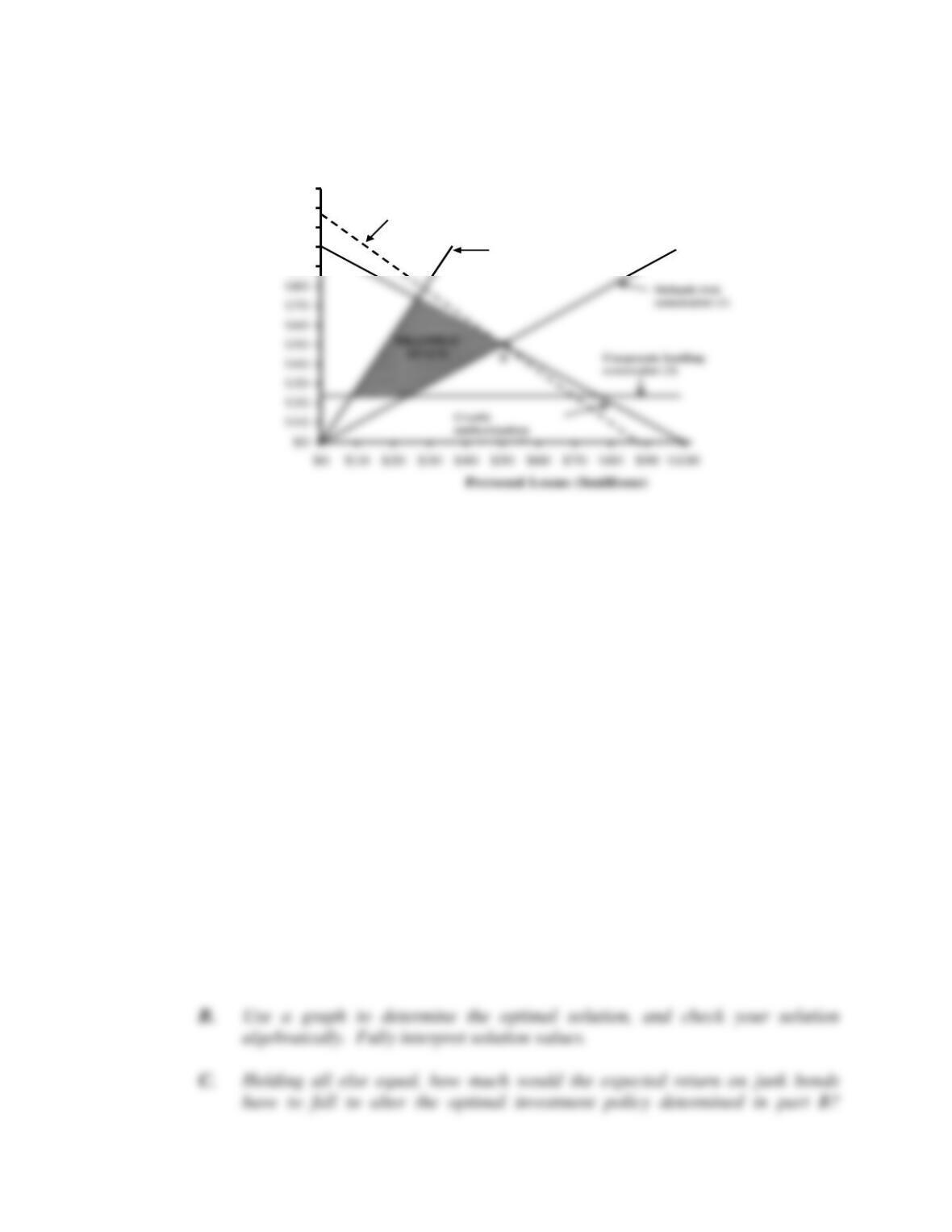

P9.5 Optimal Credit Policy. Kate Warner, a senior loan officer with Citybank in

Cleveland, Ohio, has both corporate and personal lending customers. On average,

the profit contribution margin or interest rate spread is 1.5 percent on corporate

loans and 2 percent on personal loans. This return difference reflects the fact that

personal loans tend to be riskier than corporate loans. Warner seeks to maximize the

total dollar profit contribution earned, subject to a variety of restrictions on her

A. Using the inequality form of the constraint conditions, set up and interpret the linear

programming problem that Warner would use to determine the optimal dollar

amount of credit to extend to corporate (C) and personal (P) lending customers.

Also formulate the LP problem using the equality form of the constraint conditions.

B. Use a graph to determine the optimal solution, and check your solution

algebraically. Fully interpret solution values.

254 Chapter 9

P9.5 SOLUTION

A. Warner’s goal is to maximize the profit contribution earned on loans to corporate (C)

plus personal (P) lending customers, subject to a variety of restrictions on her

In equality form, the constraint conditions are:

B. From the graph, it is obvious that the default risk (1) and credit authorization (4)

constraints are binding and, therefore, that SD = SA = 0 at point X. At this point, our

Linear Programming 255

From (1),

From (2),

From (3),

And finally, from the objective function:

Solution values can be interpreted as follows:

256 Chapter 9

SC = $25,000,000 At optimum, Warneris lending corporate customers $25

P9.6 Optimal Portfolio Decisions. The James Bond Fund is a mutual fund (open-end

investment company) with an objective of maximizing income from a widely

diversified corporate bond portfolio. The fund has a policy of remaining invested

largely in a diversified portfolio of investment-grade bonds. Investment-grade bonds

have high investment quality and receive a rating of Baa or better by Moody’s, a

bond rating service. The fund’s investment policy states that investment-grade bonds

are to be emphasized, representing at least three times the amount of junk bond

holdings. Junk bonds pay high nominal returns but have low investment quality, and

they receive a rating of less than Baa from Moody’s. To maintain the potential for

high investor income, at least 20 percent of the fund’s total portfolio must be invested

in junk bonds. Like many funds, the James Bond Fund cannot use leverage (or

borrowing) to enhance investor returns. As a result, total bond investments cannot

total more than 100 percent of the portfolio. Finally, the current expected return for

investment-grade (I) bonds is 9 percent, and it is 12 percent for junk (J) bonds.

A. Using the inequality form of the constraint conditions, set up and interpret the

linear programming problem that the James Bond Fund would use to

determine the optimal portfolio percentage holdings of investment-grade (I)

and junk (J) bonds. Also formulate the problem using the equality form of the

constraint conditions. (Assume that the fund managers have decided to remain

fully invested and therefore hold no cash at this time.)

Citybank

$90

$100

$110

$120

$130

Corporate Loans

($millions)

Business cycle

risk constraint (2)

$1.75 million

Isoreturn curve

258 Chapter 9

D. In anticipation of a rapid increase in interest rates and a subsequent economic

downturn, the investment committee has decided to minimize the fund’s

exposure to bond price fluctuations. In adopting a defensive position, what is

the maximum share of the portfolio that can be held in cash given the

investment policies stated in the problem?

P9.6 SOLUTION

A. In this problem, the goal is to maximize the mutual fund investors’ expected income

In equality form the constraint conditions are:

Here I is the portfolio share in investment-grade bonds, J is the portfolio share in junk

Linear Programming 259

B. From the graph, we see that the investment-grade bond (I) and leverage (3)

Take (1) minus (3),

From (1),

I = 0.75

From (2),

And the investors’ expected Total Return is:

Solution values can be interpreted as follows:

260 Chapter 9

C. The isoreturn line I = (Total Return/RI) – (RJ/RI)J, and RI and RJ are returns on

D. The junk bond investment constraint requires that a minimum of 20 percent of the

overall portfolio be invested in junk bonds. From the investment-grade bond

Linear Programming 261

James Bond Fund

90%

100%

110%

120%

Investment-grade bond

constraint (1)

Junk Bond

investment constraint (2)

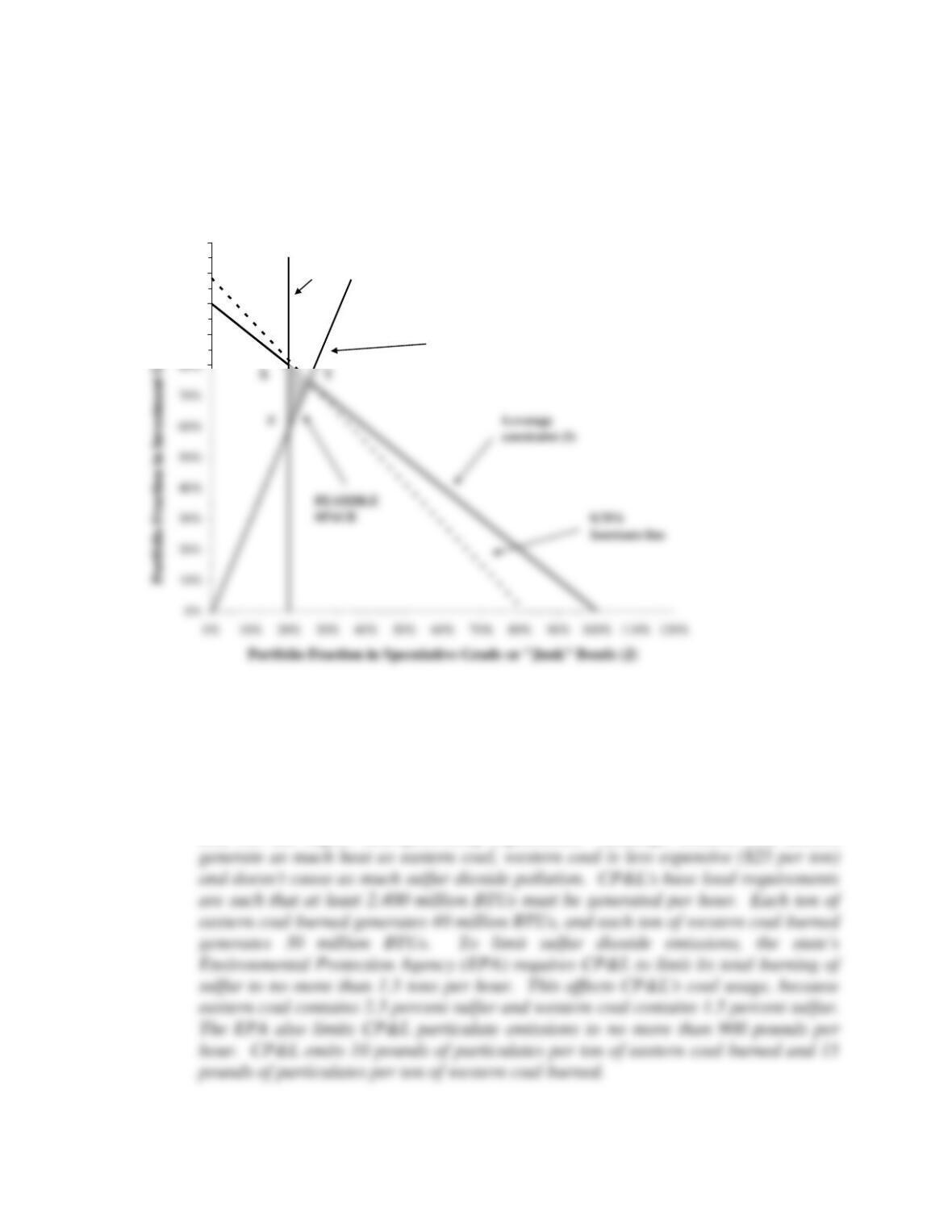

P9.7 Cost Minimization. Carolina Power and Light (CP&L) is a small electric utility

located in the Southeast. CP&L currently uses coal-fired capacity to satisfy its base

load electricity demand, which is the minimum level of electricity demanded 24 hours

per day, 365 days per year.

CP&L currently burns both high-sulfur eastern coal and low-sulfur western

coal. Each type of coal has its advantages. Eastern coal is more expensive ($50 per

ton) but has higher heat-generating capabilities. Although western coal doesn’t

262 Chapter 9

A. Set up and interpret the linear program that CP&L would use to minimize

hourly coal usage costs in light of its constraints.

B. Calculate and interpret all relevant solution values.

P9.7 SOLUTION

A. In this problem, the goal is to minimize CP&L’s hourly coal usage costs subject to

constraints on BTUs generated per hour, sulfur emissions per hour, and pounds of

particulate emissions per hour. The linear programming problem is:

In inequality form the constraint conditions are:

B. From the graph, we see the heat and particulate constraints are binding at the optimal

Linear Programming 263

Taking (1) minus 4 times (3),

From (1),

From (2),

Solutions values can be interpreted as follows:

264 Chapter 9

C. Holding all else equal, the only thing that changes when PW rises is that the isocost

line E = (C0/PE) –(PW/PE)W becomes steeper. Importantly, the feasible space

Because PW = $25 now,

Linear Programming 265

Carolina Power and Light

80

90

100

Eastern Coal

“E” (tons)

P9.8 Profit Maximization. Creative Accountants, Ltd., is a small San Francisco-based

accounting partnership specializing in the preparation of individual (I) and

corporate (C) income tax returns. Prevailing prices in the local market are $125 for

individual tax return preparation and $250 for corporate tax return preparation.

Five accountants run the firm and are assisted by four bookkeepers and four

secretaries, all of whom work a typical 40-hour workweek. The firm must decide

A. Set up the linear programming problem that the firm would use to determine

the profit-maximizing output levels for preparing individual and corporate

returns. Show both the inequality and equality forms of the constraint

conditions.

B. Completely solve and interpret the solution values for the linear programming

problem.

266 Chapter 9

C. Calculate maximum possible net profits per week for the firm, assuming that

the accountants earn $1,500 per week, bookkeepers earn $500 per week,

secretaries earn $10 per hour, and fixed overhead (including promotion and

other expenses) averages $5,000 per week.

F. Does the dual solution provide information useful for planning purposes?

Explain.

P9.8 SOLUTION

A. First, the profit contribution for preparing individual, I, and corporate, C, income tax

returns must be calculated. Profit contribution is price minus variable computer and

INPUT HOURS PER RETURN

OUTPUT

A

B

S

1

1

Linear Programming 267

In equality form the constraint conditions are:

B. By graphing the constraints and the highest possible isoprofit line, the optimal Point

X is identified where SA = SS = 0.

Thus,

From (1),

From (2),

268 Chapter 9

And the total profit contribution per week is

Solution values can be interpreted as follows:

C. The $18,000 maximum weekly profit contribution calculated in Part B is before fixed

D. Given 80 hours of excess bookkeeper capacity, if two bookkeepers are let go while