09 Case model 12/9/2018

PART C

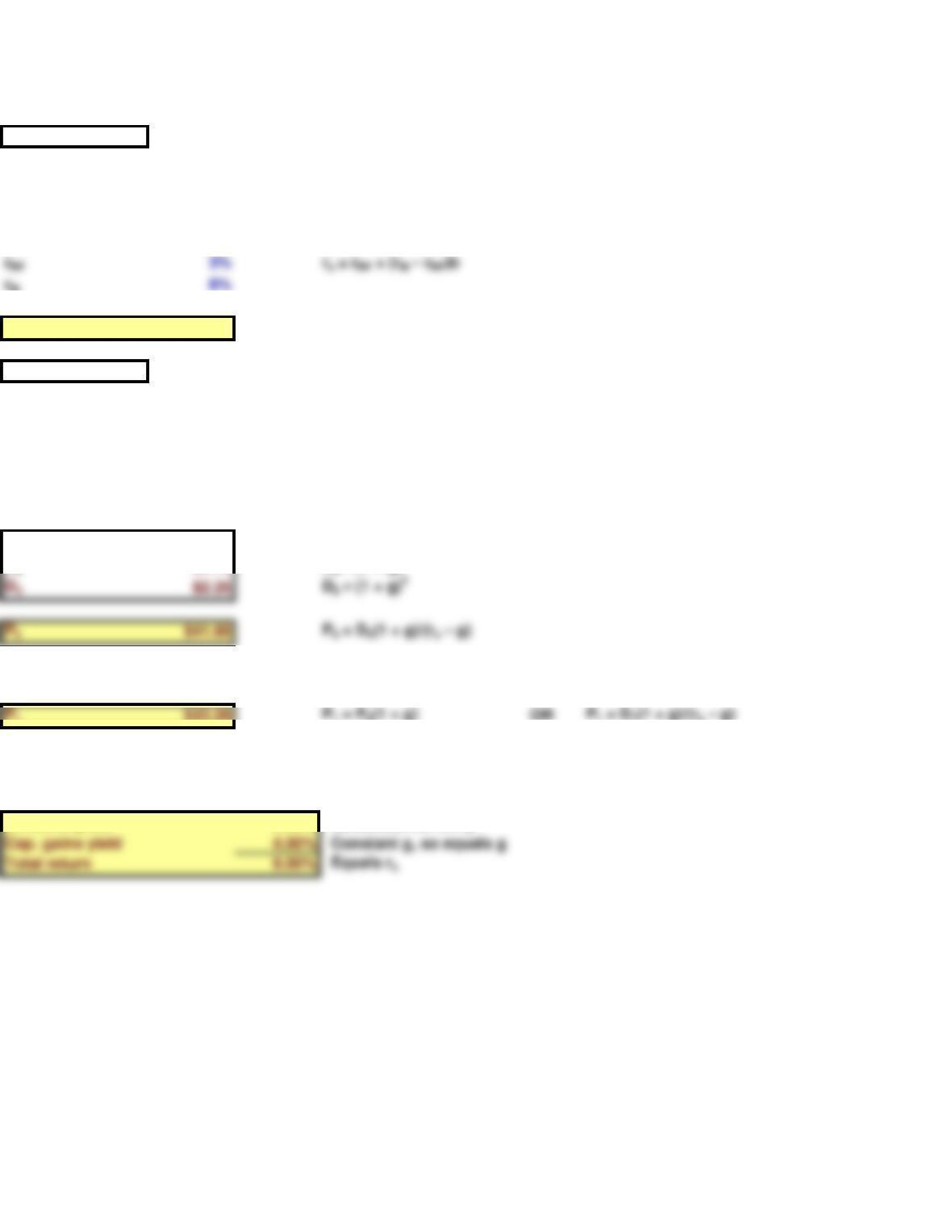

Beta 1.2 Use the CAPM:

rs = 9.0%

PART D

D0$2.00

g4%

D1$2.08 D0 × (1 + g)

D2$2.16 D0 × (1 + g)2

P0$41.60 P0 = D0(1 + g)/(rs – g)

(3) What is the stock’s expected value one year from now?

P1$43.26 P1 = P0(1 + g) OR P1 = D1(1 + g)/(rs – g)

Dividend yield 5.00%

Calculated as D1/P0

9/12/2022 17:18

Chapter 9. Stocks and Their Valuation

This spreadsheet model is designed to be used in conjunction with the chapter’s integrated case and the related

PowerPoint slide presentation.

Assume that Bon Temps has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 3%, and that

the required rate of return on the market is 8%. What is Bon Temps’s required rate of return?

Assume that Bon Temps is a constant growth company whose last dividend (D0, which was paid yesterday) was

$2.00 and whose dividend is expected to grow indefinitely at a 4% rate.

(1) What is the firm’s expected dividend stream over the next 3 years?

(2) What is its current stock price?

(4) What are the expected dividend yield, capital gains yield, and total return during the first year?

PART E

P0$40.00

PART F

g0%

P0 = D0(1 + g)/(rs – g)

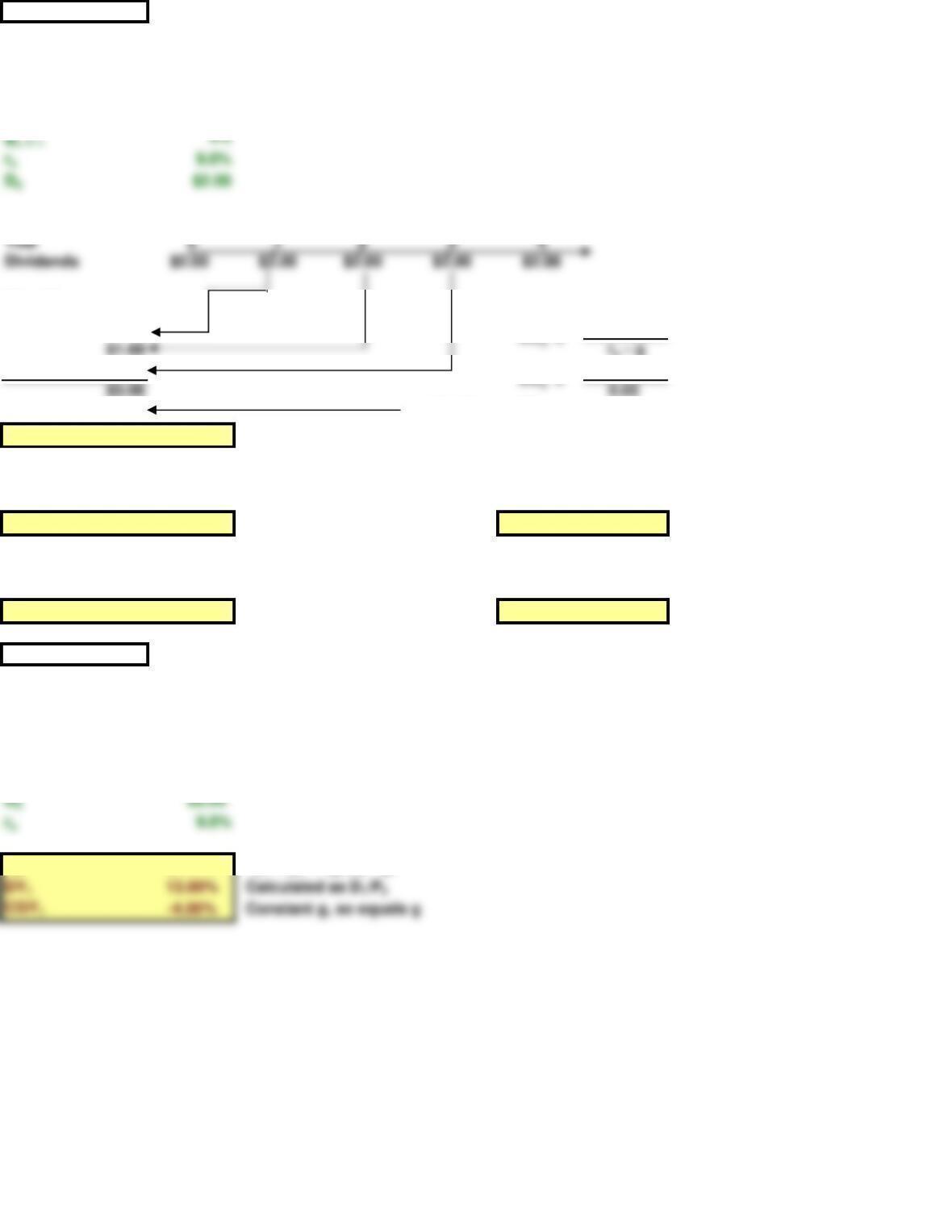

PART G

gS, 1 30%

gS, 2 20%

gS, 3 10%

gL, 4 -> 4%

rs9.0%

D0$2.00

4%———————->

Year 0 1 2 3 4

PV of Dn

$2.39

D4

$2.65 $3.57

$55.12 $71.39

$62.78

= P0

DY1 = D1/ P0

DY1 = $2.60 /$62.78

DY4 = D4/ P3

Now assume that Bon Temps’s dividend is expected to grow 30% the first year, 20% the second year, 10% the

third year, and return to its long-run constant growth rate of 4%. What is the stock’s value under these

conditions? What are its expected dividend and capital gains yields in Year 1? In Year 4?

<———–30%———–20%———–10%—>

What would the stock price be if its dividends were expected to have zero growth?

Now assume that the stock is currently selling at $40.00. What is its expected rate of return?

D1$2.08

PART H

gS, 1-3 0%

4%———————->

PV of Dn

$1.83

D4

$1.54 $2.08

$32.12 $41.60

= HV3

$37.19

= P0

DY1 = D1/ P0

DY1 = $2.00 /$37.19

DY1 = 5.38% CGY1 = 3.62%

DY4 = D4/ P3

DY4 = $2.08 /$41.60

DY4 = 5.00% CGY4 = 4.00%

PART I

g -4%

P0$14.77 P0 = D0(1 + g)/(rs – g)

Suppose Bon Temps is expected to experience zero growth during the first 3 years and then resume its steady-

state growth of 4% in the fourth year. What would be its value then? What would be its expected dividend and

capital gains yields in Year 1? In Year 4?

Finally, assume that Bon Temps’s earnings and dividends are expected to decline at a constant rate of 4% per

year, that is, g = -4%. Why would anyone be willing to buy such a stock, and at what price should it sell? What

would be its dividend and capital gains yields in each year?

<——————–0%——————–>

gL, 4 -> 4%

PART J

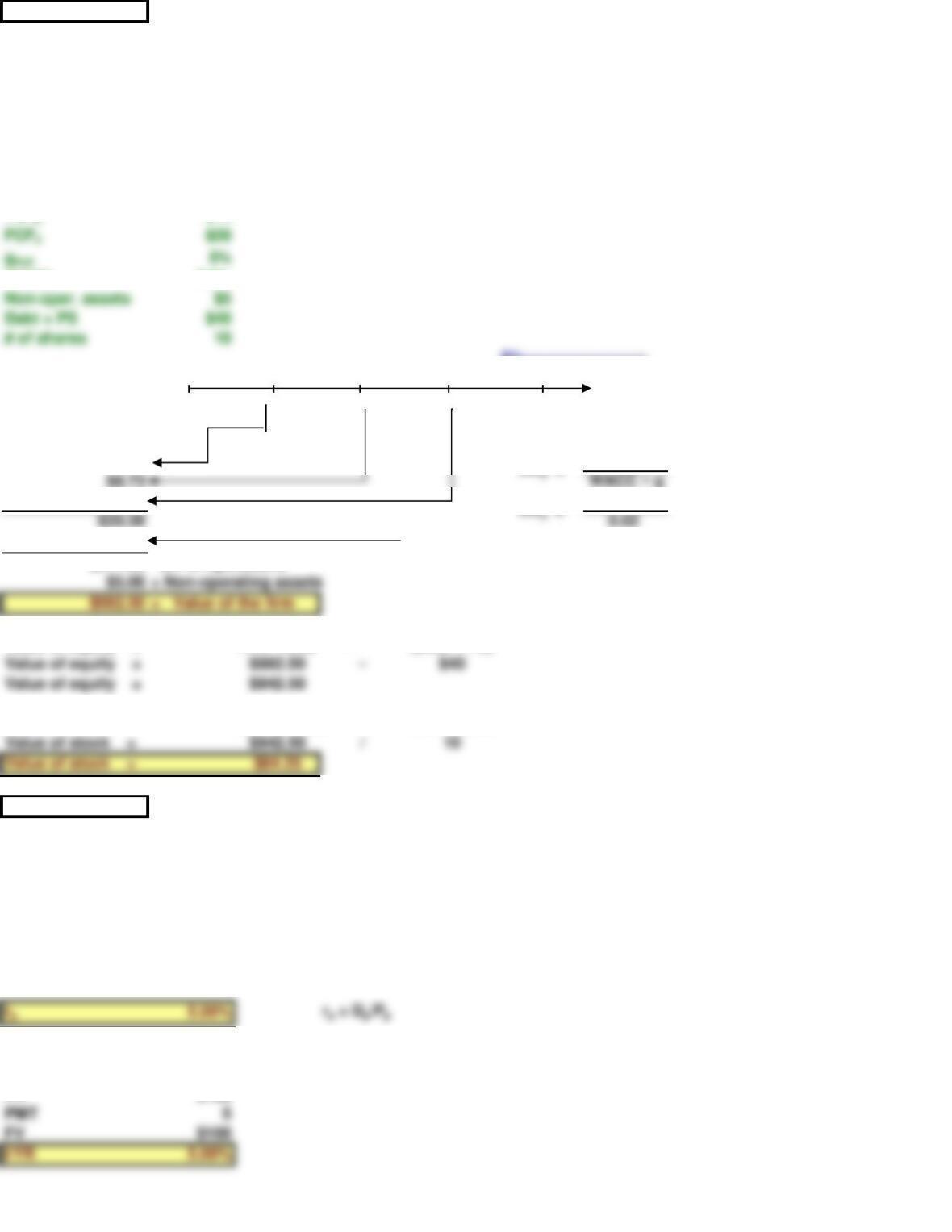

FCF1-$5

FCF2$10

WACC 7.0%

Year 0 1 2 3 4

FCF’s -$5.00 $10.00 $20.00 $21.00

PV of FCFn

-$4.67

FCF4

$16.33 $21.00

857.11 $1,050.00

= HV3

$877.50 MV of operations

Value of equity =

Firm Value –(Debt + PS)

Value of stock = Equity Value / # of shares

PART K

Perpetual:

Dp$5

Pp$100

20-year maturity:

N20

PV $100

Suppose Bon Temps decided to issue preferred stock that would pay an annual dividend of $5 and that the issue

price was $100 per share. What would be the stock’s expected return? Would the expected rate of return be the

same if the preferred was a perpetual issue or if it had a 20-year maturity?

Suppose Bon Temps embarked on an aggressive expansion that requires additional capital. Management

decided to finance the expansion by borrowing $40 million and by halting dividend payments to increase retained

earnings. Its WACC is now 7%, and the projected free cash flows for the next 3 years are -$5 million, $10 million,

and $20 million. After Year 3, free cash flow is projected to grow at a constant 5%. What is Bon Temps’s market

value of operations? If it has 10 million shares of stock, $40 million of debt and preferred stock combined, and $5

million of non-operating assets, what is the price per share?

HV3 =

FCF3$20