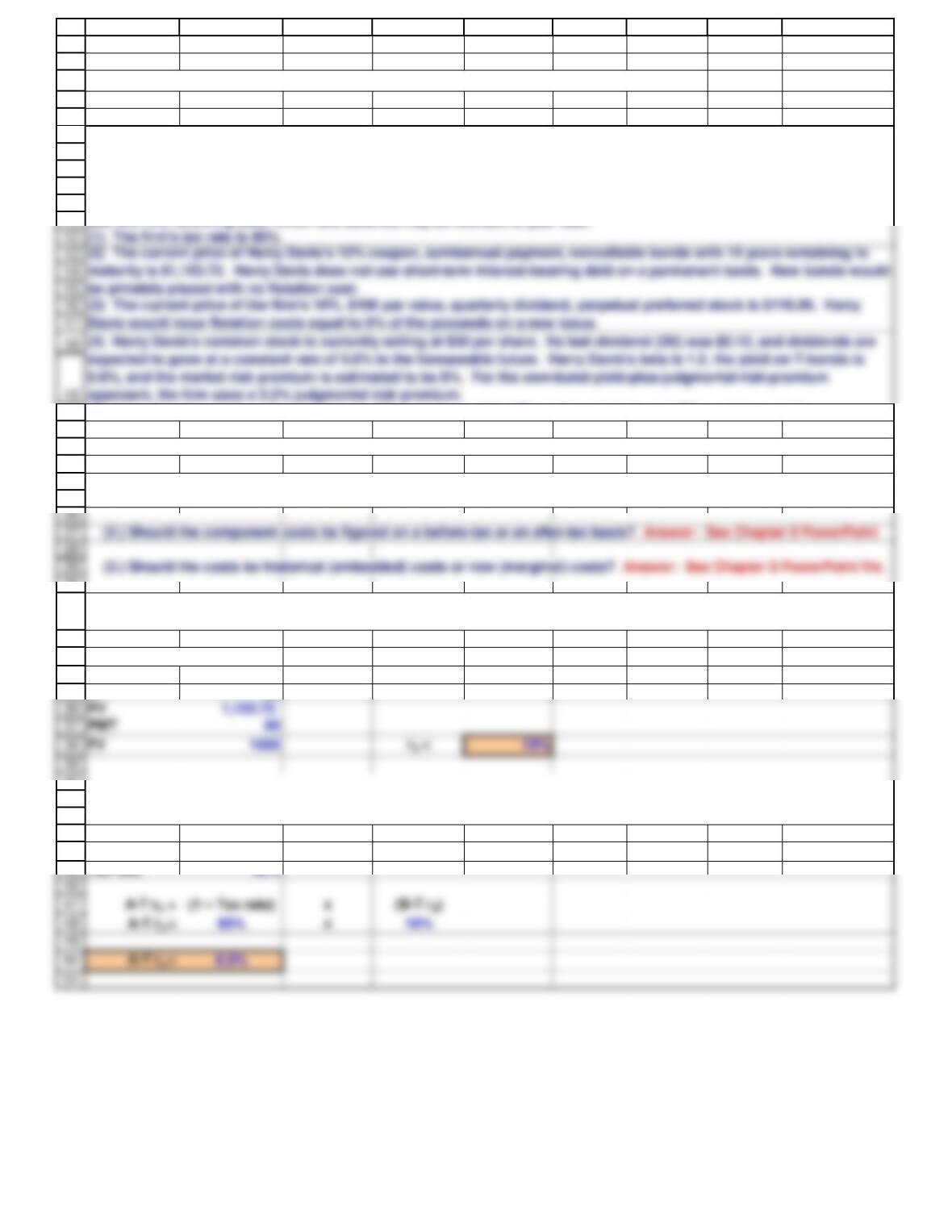

(2.) Should the component costs be figured on a before-tax or an after-tax basis? Answer: See Chapter 9 PowerPoint

1

2

3

4

5

6

7

8

9

10

11

20

21

22

23

24

25

30

31

32

33

34

35

40

41

42

43

44

45

A B C D E F G H I

12/10/2012

Situation

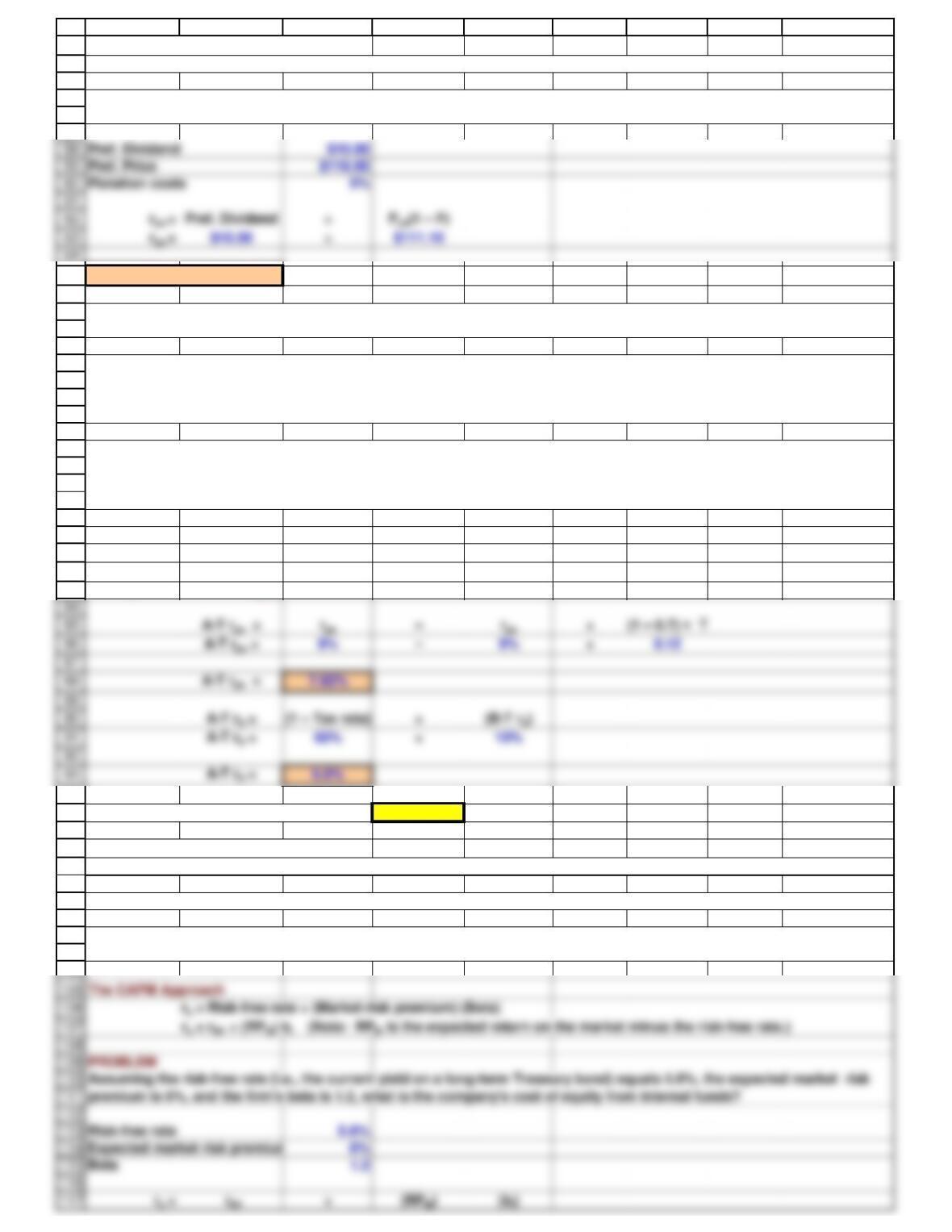

COST OF DEBT, rd

N30

B-T rd10%

Tax rate 40%

Chapter 9. Mini Case

The relevant cost of debt is the after-tax cost of new debt, taking account of the tax deductibility of interest. The after-tax

rate is calculated by multiplying the interest rate (or the before-tax cost of debt) times one minus the tax rate.

To help you structure the task, Leigh Jones has asked you to answer the following questions.

(5) Harry Davis’s target capital structure is 30% long-term debt, 10% preferred stock, and 60% common equity.

b. What is the market interest rate on Harry Davis’s debt and what is the component cost of this debt for WACC

purposes?

During the last few years, Harry Davis Industries has been too constrained by the high cost of capital to make many

capital investments. Recently, though, capital costs have been declining, and the company has decided to look seriously

at a major expansion program that has been proposed by the marketing department. Assume that you are an assistant to

Leigh Jones, the financial vice president. Your first task is to estimate Harry Davis’s cost of capital. Jones has provided

you with the following data, which she believes may be relevant to your task:

a. (1.) What sources of capital should be included when you estimate Harry Davis’s weighted average cost of capital

(WACC)? Answer: See Chapter 9 PowerPoint file.

(1) The firm’s tax rate is 40%.

(2) The current price of Harry Davis’s 12% coupon, semiannual payment, noncallable bonds with 15 years remaining to

maturity is $1,153.72. Harry Davis does not use short-term interest-bearing debt on a permanent basis. New bonds would

be privately placed with no flotation cost.

Davis would incur flotation costs equal to 5% of the proceeds on a new issue.

approach, the firm uses a 3.2% judgmental risk premium.

52

53

54

55

56

57

87

92

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

94

95

Assuming the risk-free rate (i.e., the current yield on a long-term Treasury bond) equals 5.6%, the expected market risk

premium is 6%, and the firm’s beta is 1.2, what is the company‘s cost of equity from internal funds?

96

97

98

99

100

101

102

103

104

A B C D E F G H I

COST OF PREFERRED STOCK, rps

rps =9.0%

Example:

rps 9%

rd10%

T40%

A-T Risk Premium on Preferred 1.92%

COST OF EQUITY (INTERNAL), rs

The cost of preferred stock is simply the preferred dividend divided by the price the company will receive if it issues new

preferred stock. No tax adjustment is necessary, as preferred dividends are not tax deductible.

Corporations own most preferred stock, because 70% of preferred dividends are non-taxable to corporations. Therefore,

preferred stock often has a lower before-tax yield than the before-tax yield on debt. But, the after-tax costs to the issuer

are higher on preferred stock than debt. This is consistent with the higher risks of preferred stock.

(2.) Harry Davis’s preferred stock is riskier to investors than its debt, yet the preferred’s yield to investors is lower than

the

Preferred stock carries a higher risk to investors than debt. Companies are not required to pay preferred dividends

although, firms typically want to pay preferred dividends. Otherwise, they cannot pay common dividends, so there will be

difficulty raising additional funds, and preferred stockholders may gain control of the firm.

d. (1.) What are the two primary ways companies raise common equity? Answer: See Chapter 9 PowerPoint file.

(2.) Why is there a cost associated with reinvested earnings? Answer: See Chapter 9 PowerPoint file.

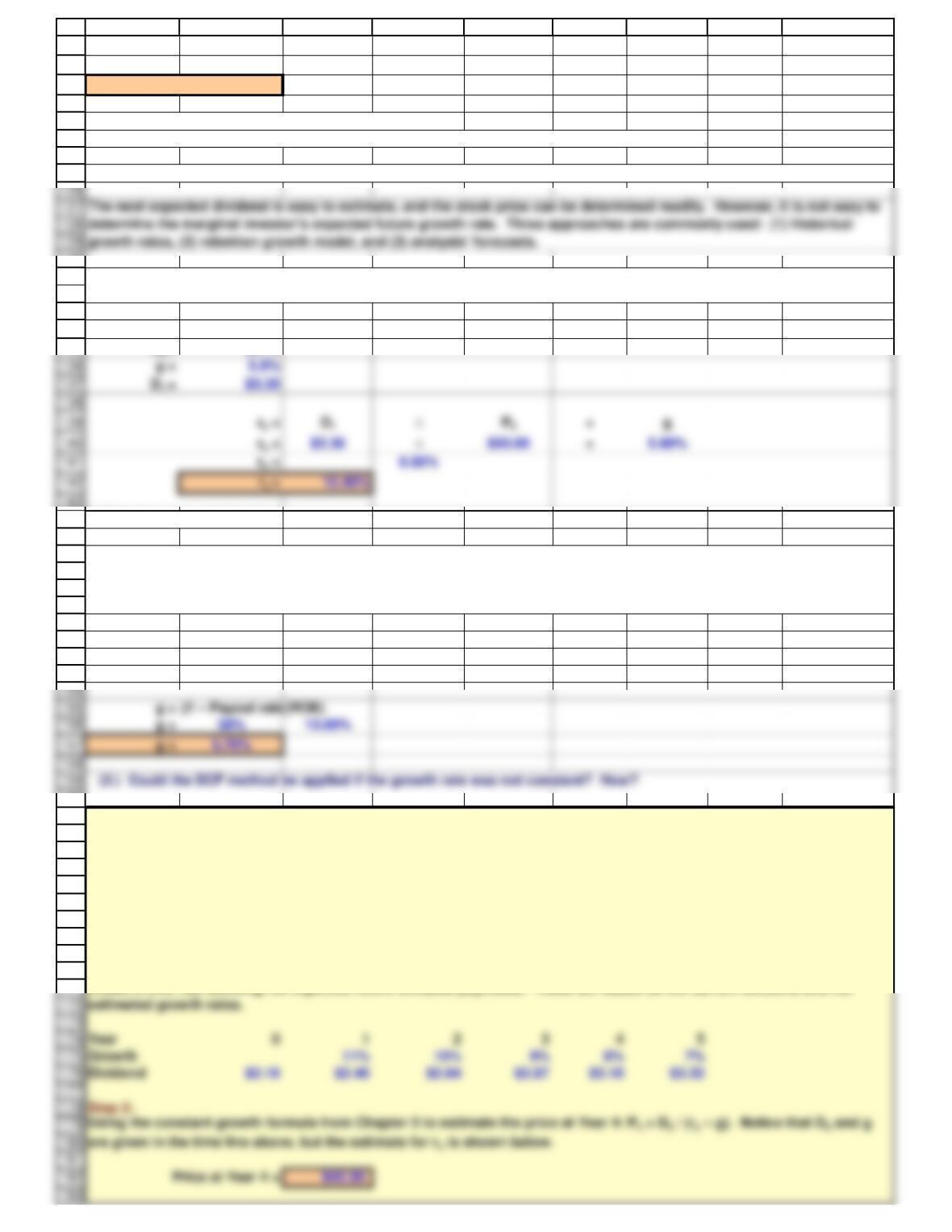

(3.) Harry Davis doesn’t plan to issue new shares of common stock. Using the CAPM approach, what is Harry Davis’s

estimated cost of equity?

c. (1.) What is the firm’s cost of preferred stock?

64

D1 =$3.30

156

(3.) Could the DCF method be applied if the growth rate was not constant? How?

118

119

120

121

122

123

124

125

130

131

132

133

134

135

144

145

146

147

148

149

150

151

152

153

160

181

182

Step 2:

estimated growth rates.

are given in the time line above, but the estimate for rs is shown below.

161

162

163

164

165

166

167

168

169

170

171

A B C D E F G H I

rs = 5.6% +6.0% 1.2

rs = 5.6% +7.2%

rs = 12.80%

THE DISCOUNTED CASH FLOW APPROACH

e. (1.) What is the estimated cost of equity using the discounted cash flow (DCF) approach?

P0 =$50.00

D0 =$3.12

2. Retention Growth Model

Find g:

Payout rate = 62%

ROE = 15%

BONUS: APPLICATION OF THE DISCOUNTED CASH FLOW APPROACH WHEN GROWTH IS NOT CONSTANT

Step 1:

Suppose a firm’s stock trades at $50 and its most recent dividend was $3.12. If the expected constant growth rate is 5.8%,

what is the firm‘s cost of equity?

Create a time line showing the expected future dividend payments. These are based on the current dividend and the

Suppose the current dividend is $2.16 per share and the current actual price that we observe is $32.00 per share.

Analysts forecast growth of 11% the first year, 10% the second year, 9% the third year, 8% the fourth year, and 7%

thereafter. Estimate the cost of equity.

e. (2.) Suppose the firm has historically earned 15% on equity (ROE) and retained 35% of earnings, and investors expect

this situation to continue in the future. How could you use this information to estimate the future dividend growth rate,

and what growth rate would you get? Is this consistent with the 5% growth rate given earlier?

As we noted earlier, analysts often provide non-constant estimates of future growth. We can use a modification of the

discounted cash flow valuation procedure for non-constant growth from Chapter 5 to estimate the cost of equity.

The simplest DCF model assumes that growth is expected to remain constant, and in this case: rs = D1/P0 + g.

determine the marginal investor’s expected future growth rate. Three approaches are commonly used: (1) historical

growth rates, (2) retention growth model, and (3) analysts’ forecasts.

184

185

186

187

188

189

203

204

205

206

A B C D E F G H I

Step 3:

Calculated Current Price = $32.00

THE BOND-YIELD-PLUS-JUDGMENTAL-RISK-PREMIUM APPROACH

Calculate the current price of the stock, based on the estimate of rs below. To do this, find the present value of the price

at Year 4, P4, and then find the present value of the dividends from Year 1 through Year 4. Use the cost of equity, rs,

shown below, as the discount rate.

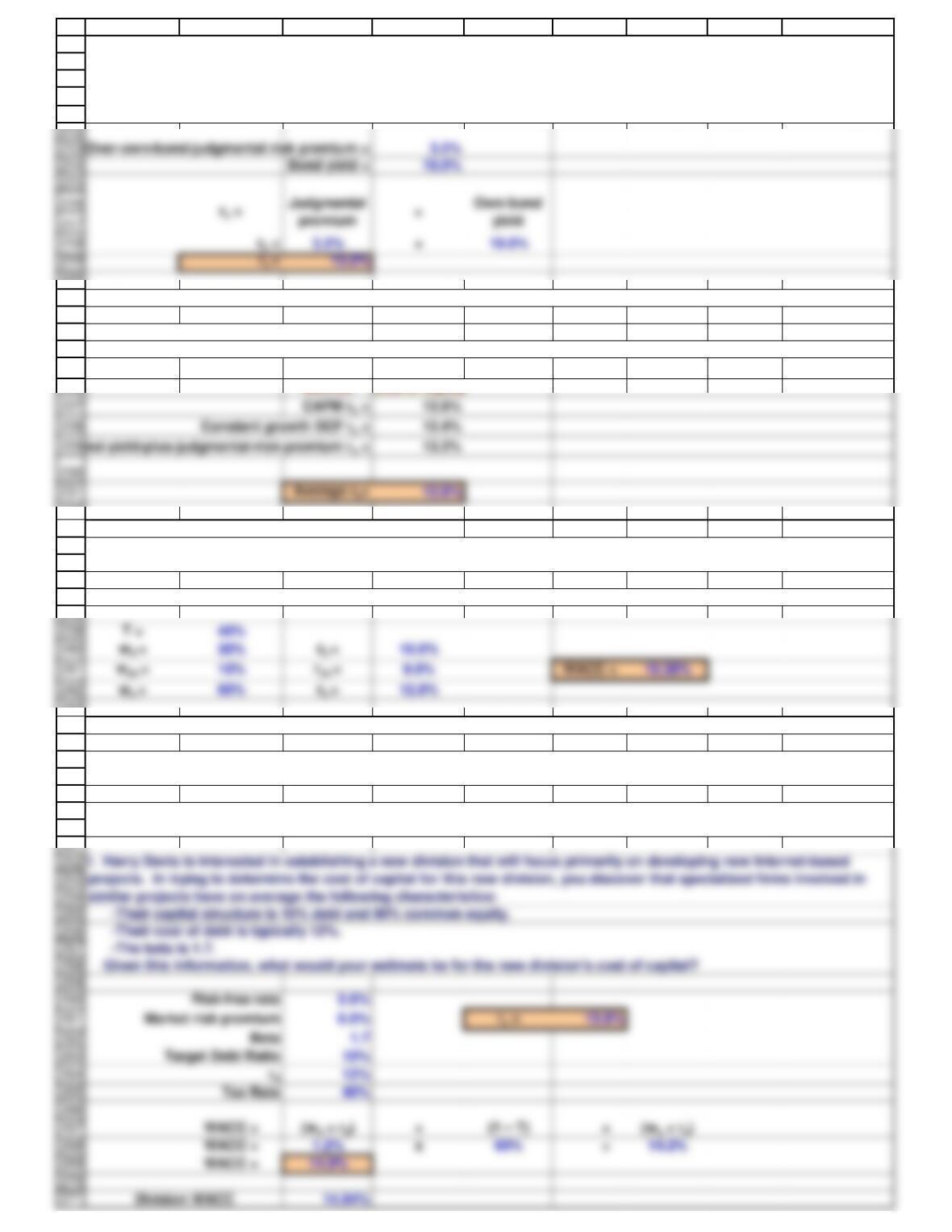

f. What is the cost of equity based on the over-own-bond-yield-plus-judgmental-risk-premium method?

196

202

Step 4:

equity, rs, in cell B194. Note: You must begin with a value in cell B194 that is greater than the long-term growth rate of

7%, or the constant growth formula will not be valid.

Note that if rs is not equal to 14.87%, then the Calculated Current Price will not be equal to the actual current price of $32.

In other words, 14.87% is the only correct value for rs, given the current stock price, the expected future dividends, and

the long-term constant growth rate of 7%.

207

208

209

210

211

220

221

projects. In trying to determine the cost of capital for this new division, you discover that specialized firms involved in

similar projects have on average the following characteristics:

222

223

224

225

226

232

233

234

235

236

237

243

244

245

246

247

248

249

250

A B C D E F G H I

THE COST OF EQUITY ESTIMATE

Method

Cost of Equity

THE WEIGHTED AVERAGE COST OF CAPITAL

The weighted average cost of capital (WACC) is calculated using the firm’s target capital structure together with its after-

tax cost of debt, cost of preferred stock, and cost of common equity.

It is common to use several methods to estimate the cost of equity, and then find the average of these methods.

h. What is Harry Davis’s weighted average cost of capital (WACC)?

i. What factors influence a company’s WACC? Answer: See Chapter 9 PowerPoint file.

j. Should the company use the overall, or composite, WACC as the hurdle rate for each of its division’s? Answer: See

Chapter 10 PowerPoint file.

k. What procedures are used to determine the risk-adjusted cost of capital for a particular division? What approaches are

used to measure a division’s beta? Answer: See Chapter 9 PowerPoint file.

g. What is your final estimate for the cost of equity, rs?

This approach consists of adding a judgmental risk premium to the yield on the firm’s own long-term debt. It is logical

that a firm with risky, low-rated debt would also have risky, high-cost equity. Historically, we have observed that the risk

premium for equity is in the range of 3 to 5 percentage points. This method provides a ballpark estimate, and it is

generally used as a check on the CAPM and DCF estimates. This method is used primarily in utility rate case hearings.

D0 =$3.12

D1 =$3.30

Flotation percentage cost (F) = 15%

272

273

274

275

276

277

285

286

287

288

289

290

291

303

304

305

Notice that this cost of stock is quite different than the cost of stock without flotation costs. To find the cost of perpetual

preferred stock, simply use the procedure above with g = 0. If the preferred stock has a fixed maturity, then use the same

procedure as for debt, except that the preferred dividend is not tax deductible.

306

307

308

309

332

333

First, calculate the after-tax coupon payments and the net proceeds after the flotation costs.

318

319

320

321

322

323

324

A B C D E F G H I

10.38%

ADJUSTING THE COST OF CAPITAL FOR FLOTATION COSTS

P0 =$50.00

Net proceeds after flotation costs =

(Stock Price) (1 – F)

Net proceeds after flotation costs =

$50.00 85%

Net proceeds after flotation costs = $42.50

Net proceeds after flotation costs = $42.50

D1 =$3.30

g = 5.8%

PROBLEM: Flotation Costs and the Cost of Debt

Tax rate =

40%

Flotation percentage cost (F) = 2%

m. What are three types of project risk? How is each type of risk used? Answer: See Chapter 9 PowerPoint file.

This indicates that the division’s market risk is greater than the firm’s average division. Typical projects within this new

division would be accepted if their returns are above the divisional WACC.

Company WACC

o. (2.) Suppose Harry Davis issues 30-year debt with a par value of $1,000 and a coupon rate of 10%, paid annually. If

flotation costs are 2%, what is the after-tax cost of debt for the new bond issue?

Flotation costs are the fees charged by investment bankers plus the accounting and legal expenses associated with the

issuance of new securities. A company cannot use the entire proceeds of a new security issuance, because it must use

some of the proceeds to pay the flotation costs.

raised internally as retained earnings. Answer: See Chapter 9 PowerPoint file.

flotation cost?

336

337

338

339

340

341

342

351

352

353

A B C D E F G H I

Net proceeds after flotation costs = $1,000 98%

Net proceeds after flotation costs = $980

Number of coupon payments = N = 30

Now find the rate that the company pays, based on its net proceeds after flotation costs and its after-tax payments.

p. What four common mistakes in estimating the WACC should Harry Davis avoid?

Answer: See Chapter 9 PowerPoint file.

346

347

ignored. Therefore, analysts often ignore the flotation costs of debt.