09 Chapter model 12/12/2018

THE DISCOUNTED DIVIDEND MODEL (Section 9-4)

CONSTANT GROWTH STOCKS (Section 9-5)

The long-run growth rate (g) is especially difficult to measure, but one approximates this rate by

multiplying the firm’s return on equity by the fraction of earnings retained, ROE x

(1 – Payout ratio). Generally speaking, the long-run growth rate is likely to fall between 5% and

Chapter 9. Stocks and Their Valuation

The basic dividend valuation equation is:

This model is similar to the bond valuation models developed in Chapter 7 in that we employ

discounted cash flow analysis to find the value of a firm’s stock.

The value of any financial asset is equal to the present value of future cash flows provided by the

asset. Stocks can be evaluated in two ways: (1) by finding the present value of the expected

future dividends, or (2) by finding the present value of the firm’s expected future free cash flows,

subtracting the market value of the debt and preferred stock to find the total value of the common

equity, and then dividing that total value by the number of shares outstanding to find the value per

share. Both approaches are examined in this spreadsheet.

In the constant growth model, we assume that the dividend will grow forever at a constant growth

rate. This is a very strong assumption, but for stable, mature firms, it can be reasonable to

assume that the firm will experience some ups and downs throughout its life but those ups and

downs balance each other out and result in a long-term constant rate. In addition, we assume that

the required return for the stock is a constant. With these assumptions, the price equation for a

common stock simplifies to the following expression:

EXAMPLE

g4.0%

rs9.0%

STOCK PRICE SENSITIVITY

Resulting

% Change Last Price

-30% $0.70 $14.56

-15% $0.85 $17.68

% Change

rs$20.80

-30% 6.30% $45.22

-15% 7.65% $28.49

% Change g $20.80

-30% 2.80% $16.58

-15% 3.40% $18.46

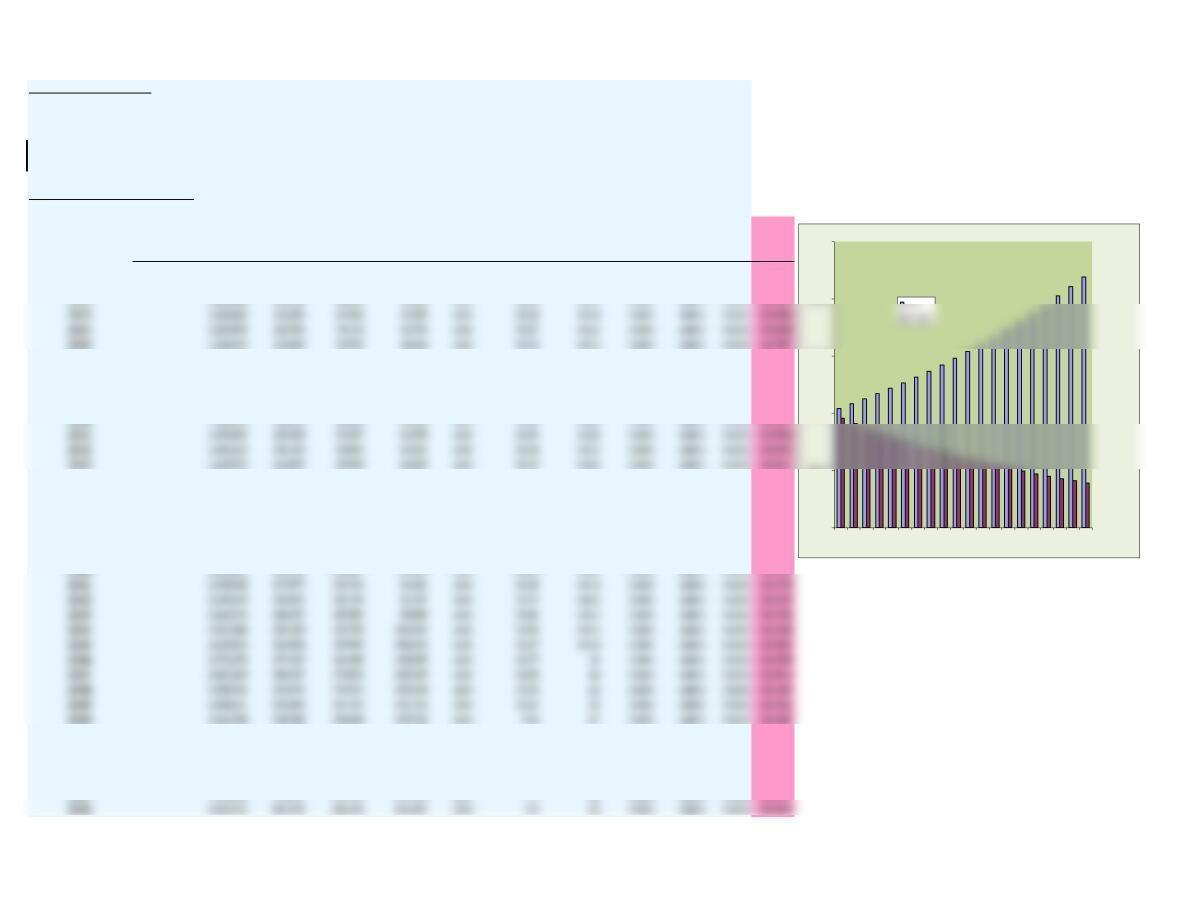

One of the keys to understanding stock valuation is knowing how various factors affect the stock

price. We construct below a series of data tables and a graph to show how the stock price is

affected by changes in the dividend, the growth rate, and rs.

From the chart we see that the stock price increases with increases in the dividend and the growth

rate but decreases with increases in the required return. The dividend relationship is linear, while

price is a nonlinear function of the growth rate and the required return. Changes in rs and g have

especially strong effects on the stock price. This occurs because as rs declines or g increases,

Keller Medical Products just paid a dividend of $1.00, and the dividend is expected to grow at a

constant rate of 4%. What stock price is consistent with these numbers, assuming a 9% required

return?

$30

$40

$50

$60

$70

$90

-30% -20% -10% 0% 10% 20% 30%

% Change in Input

g

EXPECTED RATE OF RETURN ON A CONSTANT GROWTH STOCK

D1

P0

EXAMPLE

P0 $20.80

D1$1.040

EXTENSION

What is the expected price of this stock in 5 years?

N = 5

You buy a stock for $20.80, and you expect the next annual dividend to be $1.04. Furthermore,

you expect the dividend to grow at a constant rate of 4%. What is the expected rate of return and

dividend yield on the stock?

Using the constant growth equation, we transpose the equation to solve for rs. In doing so, we are

now solving for an expected return. Here is the resulting equation:

rs =

+

g

VALUING NONCONSTANT GROWTH STOCKS (Section 9-6)

EXAMPLE

D0$1.00

PV of dividends

1.0092$

1.0184

3.0554$ 27.6848 = Terminal value =

21.3777 0.050

= rs − gL

24.4331$

= P0

PREFERRED STOCK (Section 9-8)

EXAMPLE

For many companies, it is unreasonable to assume constant growth. Here valuation procedures

become a little more complicated, because we must estimate a short-run nonconstant growth rate,

then assume that after a certain point of time the firms will grow at a constant rate, and estimate

A special case of the constant growth model is a stock with a zero growth rate. Such a stock is a

A perpetual preferred stock pays a $10 annual dividend and has a required return of 10.3%. What

is its value?

A company just paid a $1.00 dividend, and it is expected to grow at 10% for the next 3 years. After

3 years the dividend is expected to grow at the rate of 4% indefinitely. If the required return is 9%,

what is the stock’s value today?

The point in time when the dividend begins to grow at a constant rate is called the “horizon date,”

EXAMPLE

N50

N50

I6%

Had this been a perpetual preferred with a required return of 6%, what would be the stock price?:

Consider another preferred stock that has a finite life of 50 years (a sinking fund preferred issue),

a $100 par value, and a $10 annual dividend. The required return is 8%. If the par value is repaid at

maturity in 50 years, what is the price of the stock?

What would its value be if the required return declined to 6%?

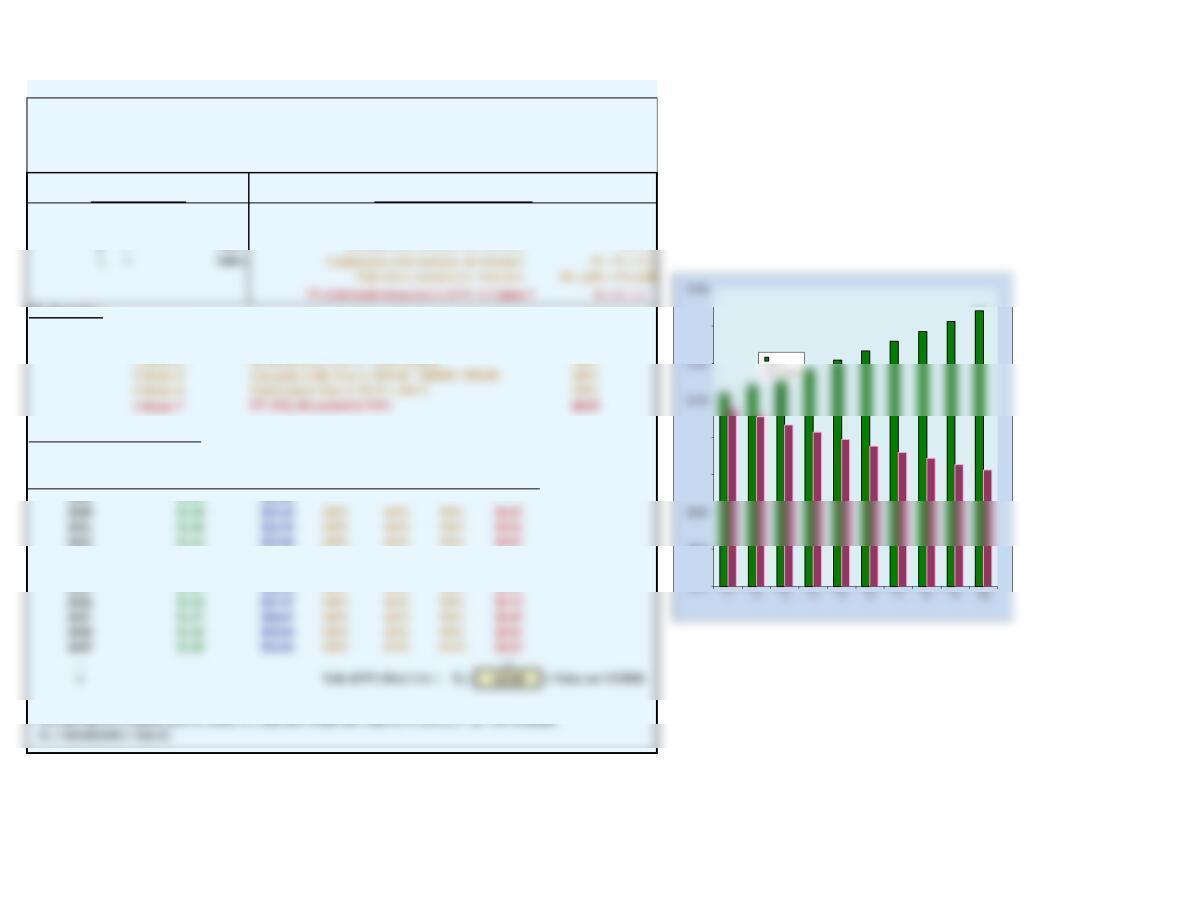

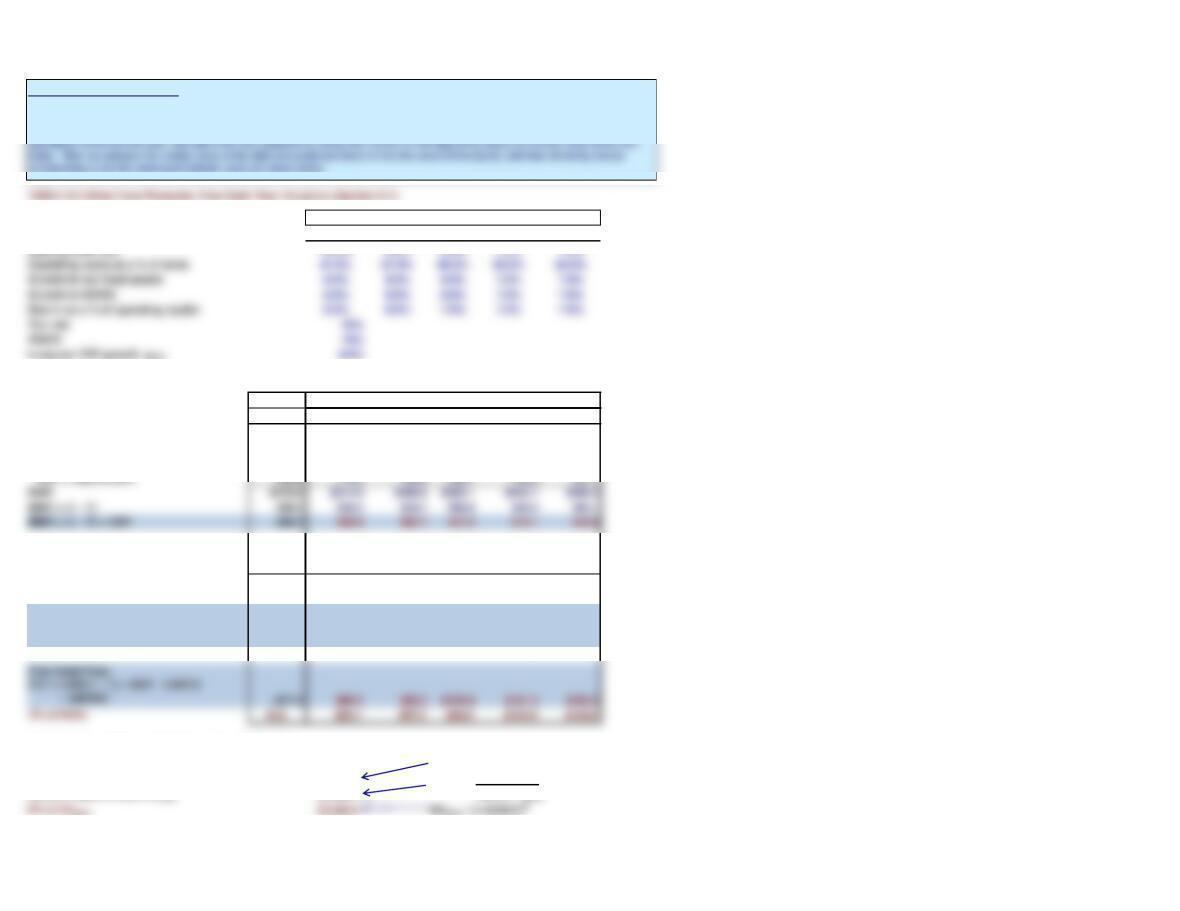

Table 9.1 Analysis of a Constant Growth Stock

12/12/2018

D0 = $1.00 Dividend in Year t , Dt , in Column 2 Dt-1(1 + g)

P0 = $20.80 Intrinsic value (and price) in Year t, Pt , in Column 3 Dt+1 / (rs − g)

g = 4.00% Dividend yield (constant) in Column 4

Dt / Pt-1

III. Examples:

Column 2

D1 = $1.00(1.04) $1.04

Column 3

P0 = $1.04 / (0.09 − 0.04) $20.80

IV. Forecasted Results over Time: PV of

At end Dividend Capital Total dividend

of year: Dividend Price * yield gains yield return at 9.0%

(1) (2) (3) (4) (5) (6) (7)

2023 $1.17 $24.33 5.0% 4.0% 9.0% $0.83

2024 $1.22 $25.31 5.0% 4.0% 9.0% $0.79

2025 $1.27 $26.32 5.0% 4.0% 9.0% $0.75

I. Basic Information:

II. Formulas Used in the Analysis:

In Section I we show the basic inputs, the formulas are in Section II, and in Section III we give examples of how cells in Columns 2

through 7 are calculated. The dividends and stock prices grow at a constant rate of 4%; the capital gains yield is equal to the growth

rate; the dividend yield is a constant 5.0%; and the total annual return is a constant 9.0%. We plot the first 10 years of dividends and their

PVs in the chart to the right of the table.

* Because this is a constant growth stock, we could have found the value for Pt as Pt-1(1 + g). For example,

$0.00

$0.20

$0.60

$0.80

$1.40

DPS

Table 9.1a Analysis of a Constant Growth Stock: Beginning with Earnings

III. Explanation of the Columns

2.

3.

4.

5.

7.

The stock price is found by use of Equation 9.2, P0 = D1 / (rs – g), e.g., $1.04 / (0.09 – 0.04)

= $20.80 at the start of 2020.

8. The stock price grows at the constant rate, 4%.

10.

The capital gains yield is (Pt – Pt-1) / Pt = ($21.63 – $20.80) / $20.80 = 4.0%, and it is equal

to the constant growth rate.

The growth rate is equal to the fraction of earnings retained times ROE, or g = (1 – Payout) × ROE =

(1 – 0.6)(10%) = 0.4(10%) = 4% for 2020 and all subsequent years. Earnings, dividends, and the stock price all

grow at this constant rate.

2020.

ALTERNATIVE VERSION OF TABLE 9.1 (Not in text). We know that dividends must come from earnings, and earnings

must come from assets, which are bought with debt and equity capital. Therefore, we develop below Table 9.1a, which

starts with assets and ROA (or ROE), calculates net income, applies a payout ratio, and then gets DPS and other values.

Total dividends paid at the end of year, e.g., dividends in 2020 were (payout ratio)(net income) = 0.6($100,000) =

$60,000.

I. Data Used By Analyst Equity = Assets (no debt): $1,000,000

Rate of return on equity, ROE: 10%

Dividend payout: 60.0%

Shares outstanding: 60,000

Required rate of return, rs:9.00%

II. Forecasted Results Over Time

Assets Net Total Earnings Growth Price Dividend Capital Total PV DIV

Year and Equity Income Dividends Retained Rate DPS per Share Yield Gains yield Return at 9.0%

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (7)

2020 $1,000,000 $100,000 $60,000 $40,000 $20.8

2021 $1,040,000 $104,000 $62,400 $41,600 4.0% $1.04 $21.6 5.00% 4.00% 9.00% $0.9541

2026 1,265,319 126,532 75,919 50,613 4.0% $1.27 $26.3 5.00% 4.00% 9.00% $0.7545

2027 1,315,932 131,593 78,956 52,637 4.0% $1.32 $27.4 5.00% 4.00% 9.00% $0.7199

2028 1,368,569 136,857 82,114 54,743 4.0% $1.37 $28.5 5.00% 4.00% 9.00% $0.6868

2029 1,423,312 142,331 85,399 56,932 4.0% $1.42 $29.6 5.00% 4.00% 9.00% $0.6553

2034 1,731,676 173,168 103,901 69,267 4.0% $1.73 $36.0 5.00% 4.00% 9.00% $0.5182

2035 1,800,944 180,094 108,057 72,038 4.0% $1.80 $37.5 5.00% 4.00% 9.00% $0.4944

2036 1,872,981 187,298 112,379 74,919 4.0% $1.87 $39.0 5.00% 4.00% 9.00% $0.4717

2037 1,947,900 194,790 116,874 77,916 4.0% $1.95 $40.5 5.00% 4.00% 9.00% $0.4501

2038 2,025,817 202,582 121,549 81,033 4.0% $2.03 $42.1 5.00% 4.00% 9.00% $0.4295

2039 2,106,849 210,685 126,411 84,274 4.0% $2.11 $43.8 5.00% 4.00% 9.00% $0.4098

2051 3,373,133 337,313 202,388 134,925 4.0% 3.4 70 5.00% 4.00% 9.00% $0.2332

2052 3,508,059 350,806 210,484 140,322 4.0% 3.5 73 5.00% 4.00% 9.00% $0.2225

2053 3,648,381 364,838 218,903 145,935 4.0% 3.6 76 5.00% 4.00% 9.00% $0.2123

2054 3,794,316 379,432 227,659 151,773 4.0% 3.8 79 5.00% 4.00% 9.00% $0.2026

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

2066 6,074,823 607,482 364,489 242,993 4.0% 6.1 126 5.00% 4.00% 9.00% $0.1153

2067 6,317,816 631,782 379,069 252,713 4.0% 6.3 131 5.00% 4.00% 9.00% $0.1100

2068 6,570,528 657,053 394,232 262,821 4.0% 6.6 137 5.00% 4.00% 9.00% $0.1050

2069 6,833,349 683,335 410,001 273,334 4.0% 6.8 142 5.00% 4.00% 9.00% $0.1002

Part 1. Key Inputs

2020 2021 2022 2023 2024

Part 2. Forecast of Cash Flows During Period of Nonconstant Growth

Historical

2019 2020 2021 2022 2023 2024

Sales $3,000.0 $3,300.0 $3,597.0 $3,884.8 $4,156.7 $4,447.7

Operating costs 2,622.0 2,871.0 3,129.4 3,340.9 3,533.2 3,780.5

DEP = Depreciation 100.0 116.6 168.0 158.7 169.8 181.7

Net fixed assets $1,000.0 $1,080.0 $1,166.4 $1,259.7 $1,347.9 $1,442.2

Net oper. working capital (NOWC) 800.0 864.0 933.1 1,007.8 1,078.3 1,153.8

Total operating capital $1,800.0 $1,944.0 $2,099.5 $2,267.5 $2,426.2 $2,596.0

Net CAPEX = Change in net fixed assets 130.0 80.0 86.4 93.3 88.2 94.4

230.0 196.6 254.4 252.0 258.0 276.1

ΔNOWC 150.0 64.0 69.1 74.6 70.5 75.5

Part 3. Horizon Value and Intrinsic Value Estimation

Estimated Value at the Horizon, 2024

FCF2024 (1+gFCF)

Free Cash Flow (2025) $202.0

FCF2025

Horizon Value at 2024, HV2024 $3,366.7 WACC − gFCF

Forecasted Years

HV2024 =

CAPEX = Gross capital expenditures

= Net CAPEX + DEP

Forecasted Years

VALUING THE ENTIRE CORPORATION Part 1 of the following table sets forth the analyst’s assumptions for specific operating variables. These

values are then used, in Part 2, to project free cash flows from 2020 out to the “horizon year,” after which it is assumed that the 2024

FCF will grow at the constant rate gLR. The PV of the FCFs during the nonconstant growth period are then discounted at the WACC.

Finally, in Part 3, we find the sum of the nonconstant FCF PVs, then use the constant growth model to find the value of the firm‘s

Long-run FCF growth, gFCF 4.0%

Calculation of Firm’s Intrinsic Value

Sum of PVs of FCFs, 2020-2024 $474.7

PV of HV2024 2,090.5

MV of nonoperating assets 0.0

Total corporate value $2,565.2

SECTION 9-4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

P0$40.00

3. If D1 = $2.00, g = 6%, and P0 = $40, what is the stock’s expected dividend yield, capital gains

yield, and total expected return for the coming year?

SECTION 9-5 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

D1$1.00

D1$1.00

g0%

rs11%

Payout 25%

rs12%

3a. Firm A is expected to pay a dividend of $1 at the end of the year. The required rate of

return is rs = 11%. Other things held constant, what would the stock’s price be if the growth

rate was 5%?

4b. What would its expected growth rate be if it paid out 75% of its earnings as dividends?

g5%

rs11%