08 Case model 9/12/2022 17:17 12/9/2018

Probability

Recession 0.1 3.0% -29.5% 24.5% 3.5% -19.5% -2.5%

Below avg. 0.2 3.0% -9.5% 10.5% -16.5% -5.5% 0.5%

Expected Return 3.0% 9.9% 1.2% 7.3% 8.0% 5.5%

Beta 0.00 1.31 -0.50 0.88 1.00 0.41

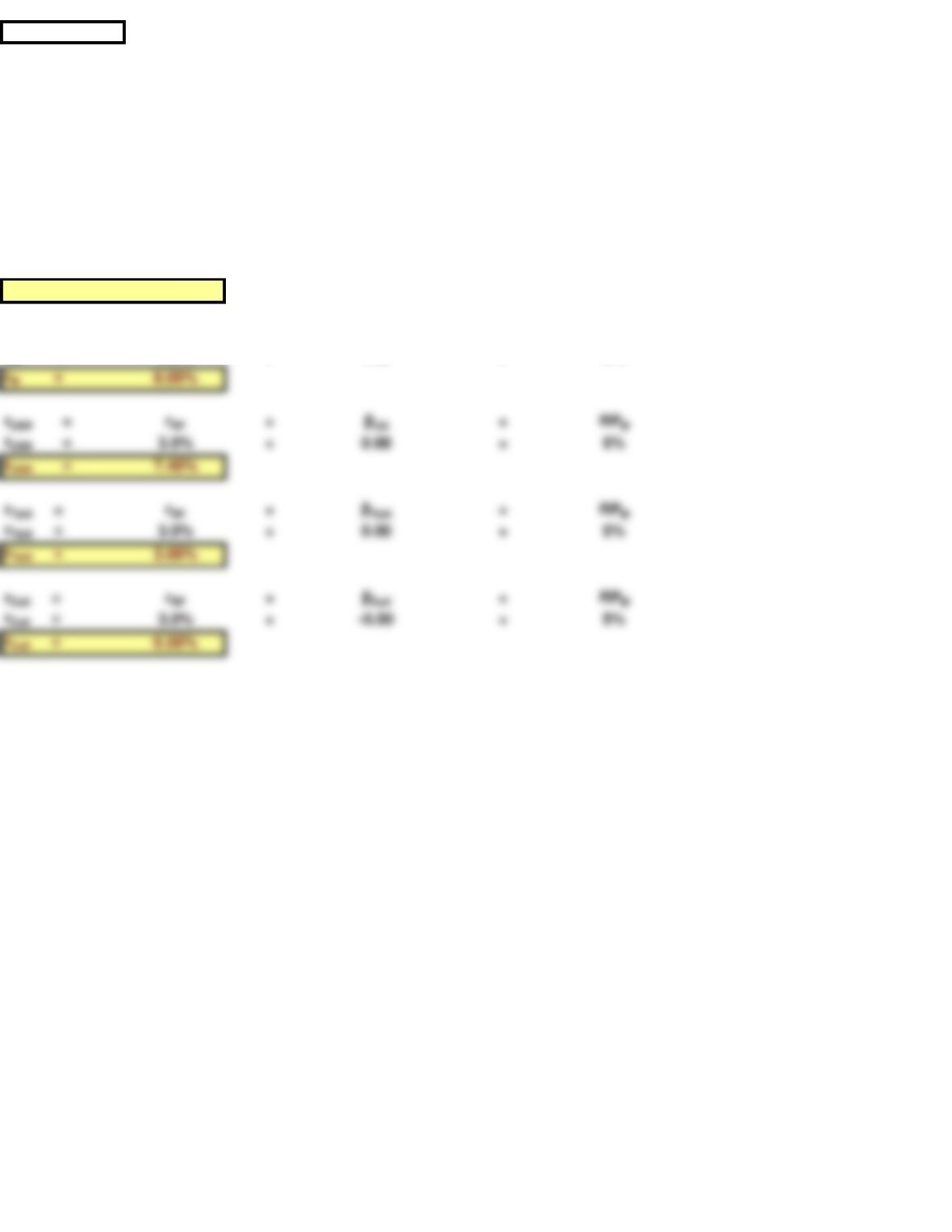

PART F

weight in High Tech 50%

weight in Collections 50%

State of the economy Port. return

Recession -2.5%

Below average 0.5%

Port. Sharpe ratio 0.55

Portfolio return 5.53%

Port. std dev 4.62%

Correlation = -0.9885

% in HT Exp. ret. Std. dev.

10% 2.0% 8.1%

40% 4.7% 1.7%

50% 5.5% 4.5%

80% 8.2% 13.8%

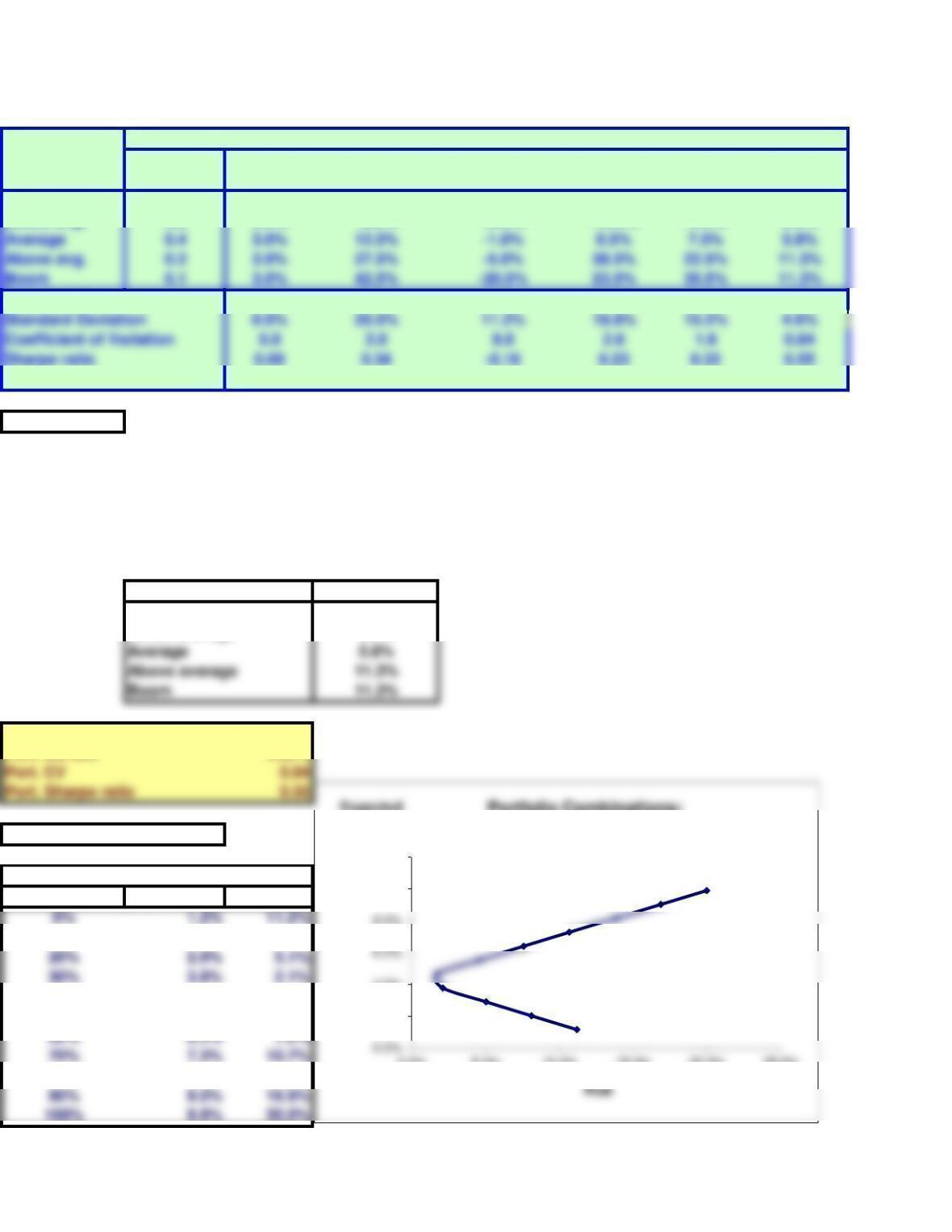

Chapter 8. Risk and Rates of Return

Returns on Alternative Investments

T-Bills

Market

portfolio

High Tech/Collections Portfolio

2-Stock

Portfolio

State of the

Economy

High Tech

Collections

U.S.

Rubber*

This spreadsheet model is designed to be used in conjunction with the chapter’s integrated case and the related

PowerPoint slide presentation.

Suppose you created a 2-stock portfolio by investing $50,000 in High Tech and $50,000 in Collections. (1)

Calculate the expected return, the standard deviation, the coefficient of variation, and the Sharpe ratio for this

portfolio, and fill in the appropriate blanks in the table.

2.0%

4.0%

8.0%

10.0%

12.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Expected

return

Portfolio Combinations:

HT and Collections

PART J

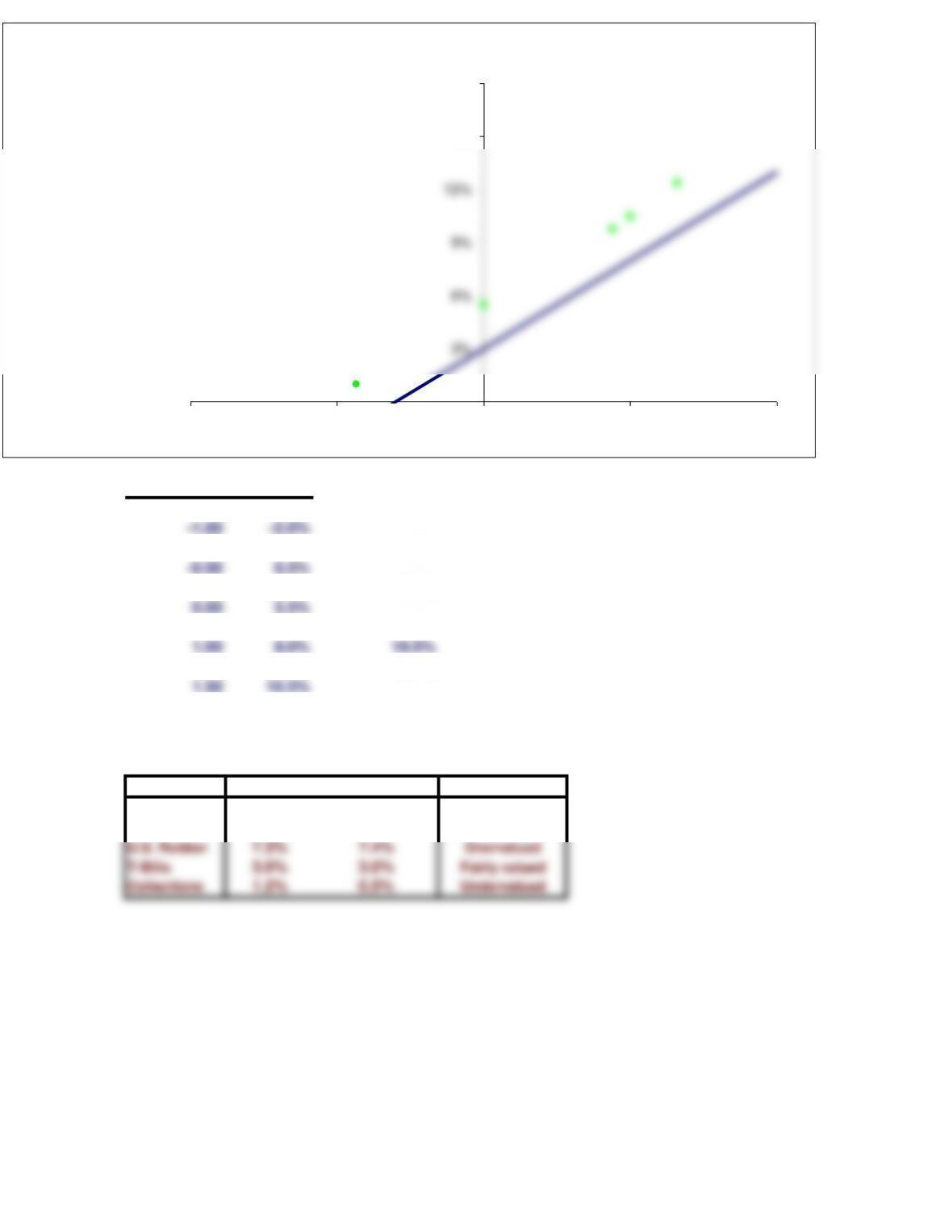

Risk-free rate 3.0% Risk-free rate 3.0%

RPM5.0% RPM5.0%

Beta 1CAPM 8.0%

rHT = rRF +βHT ×RPM

rHT = 3.0% +1.31 ×5%

rHT = 9.55%

rM = rRF +βM×RPM

rM = 3.0% +1.00 ×5%

The yield curve is currently flat; that is, long-term Treasury bonds also have a 3.0% yield. Consequently, Merrill

Finch assumes that the risk-free rate is 3.0%. (1) Write out

the SML equation, use it to calculate the required rate of return on each alternative, and graph the relationship

between the expected and required rates of return.

rM = 8.00%

rUSR = rRF +βUS ×RPM

rUSR = 3.0% +0.88 ×5%

rUSR = 7.40%

rTbill = rRF +βTbill ×RPM

rTbill = 3.0% +0.00 ×5%

rTbill = 3.00%

rColl = rRF +βColl ×RPM

rColl = 3.0% + -0.50 × 5%

Beta

rs

8.0%

-0.87 -1.4% 1.0%

0.00 3.0% 5.5%

0.88 7.4% 9.8%

1.32 9.6% 12.4%

2.00 13.0%

Security Exp. Ret. Req. Ret. Conclusion

High Tech 17.4% 1.30

9.9% 9.6% Undervalued

Market 8.0% 8.0% Fairly valued

(2) How do the expected rates of return compare with the required rates of return?

0%

15%

18%

-2.00 -1.00 0.00 1.00 2.00

Required and

Expected Returns

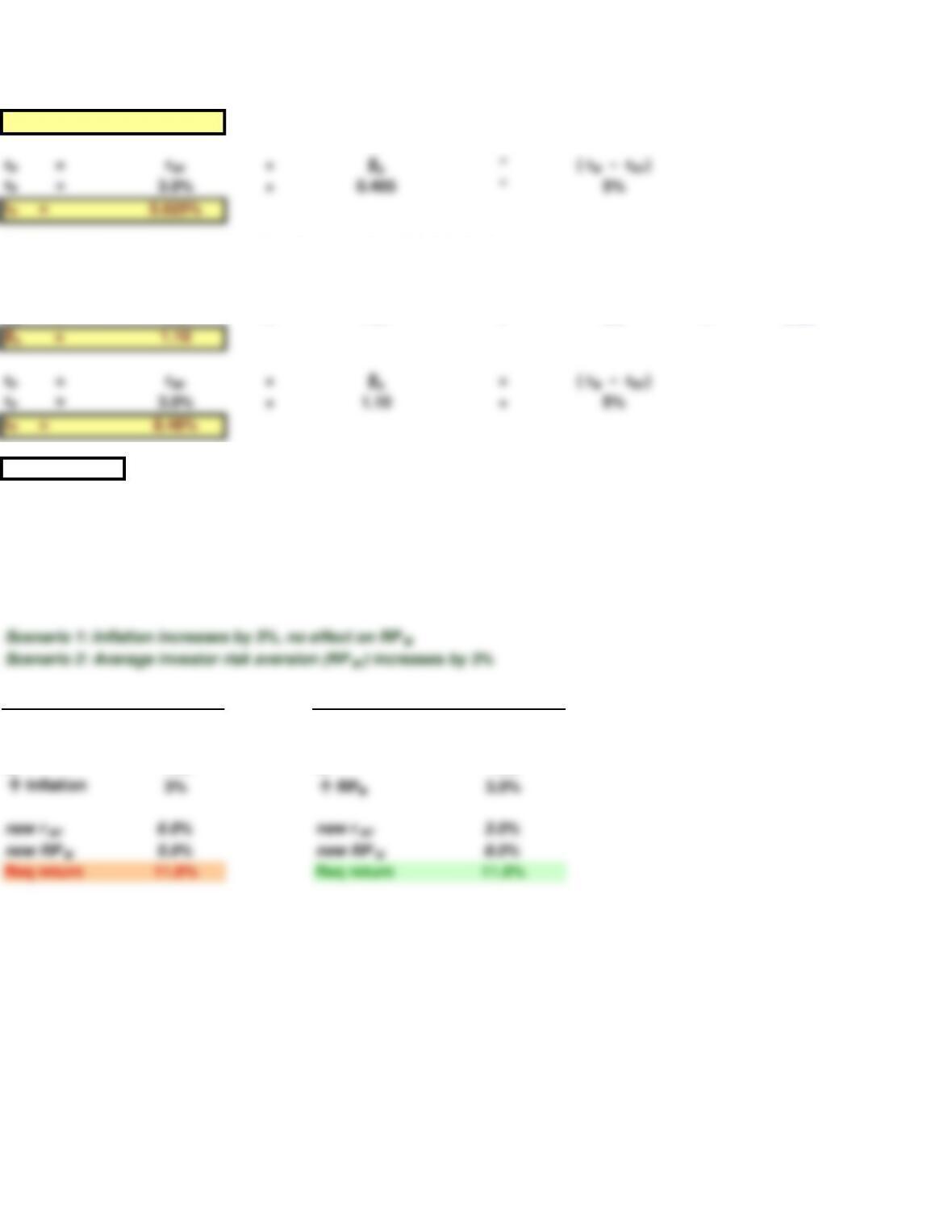

Beta

βp = wHT xβHT + wColl xβColl

βp = 0.5 x1.31 +0.5 x -0.50

βp = 0.405

βp = wHT xβHT + wUSR xβUSR

βp = 0.5 x1.31 +0.5 x0.88

PART K

old rRF 3.0% old rRF 3.0%

old RPM5.0% old RPM5.0%

bi1.00 bi1.00

Scenario 1

Scenario 2

(1) Suppose investors raised their inflation expectations by 3 percentage points over current estimates as

reflected in the 3.0% risk-free rate. What effect would higher inflation have on the SML and on the returns

required on high- and low-risk securities?

(2) Suppose instead that investors’ risk aversion increased enough to cause the market risk premium to increase

by 3 percentage points. (Inflation remains constant.) What effect would this have on the SML and on returns of

high- and low-risk securities?

(4) What would be the market risk and the required return of a 50-50 portfolio of High Tech and Collections?

For a portfolio consisting of 50% High Tech and 50% U.S. Rubber?

rP = rRF +βp* ( rM – rRF)

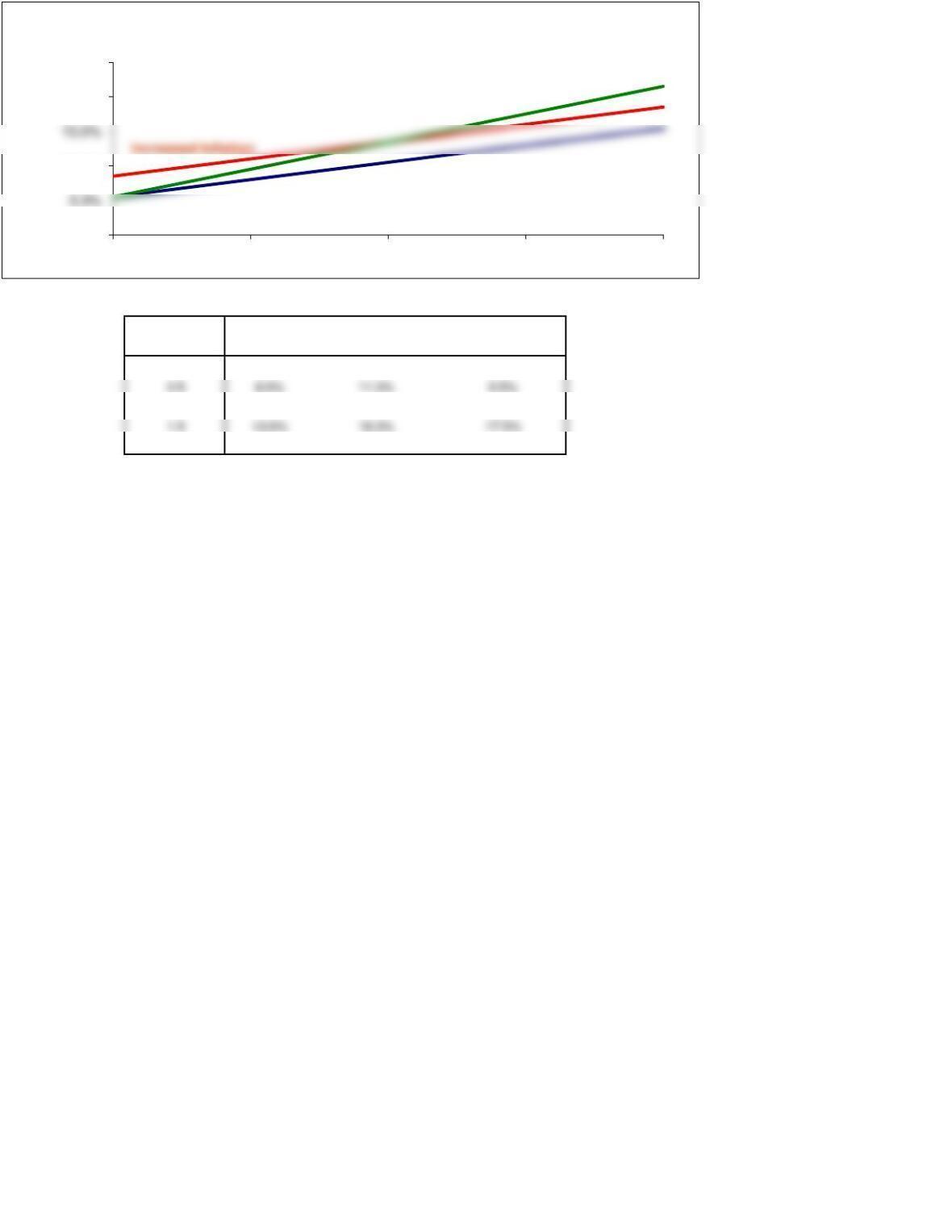

DATA TABLE USED TO MAKE SML GRAPH

Original Scenario 1 Scenario 2

Beta 8.0% 11.0% 11.00%

0 5.5% 8.5% 5.5%

1 10.5% 13.5% 13.5%

2 15.5% 18.5% 21.5%

0.0%

10.0%

20.0%

25.0%

0 0.5 1 1.5 2

Required return

Beta

Changes in the SML

Original Scenario

Increased Risk Aversion