08 Chapter model 12/12/2018

STAND-ALONE RISK (Section 8-2)

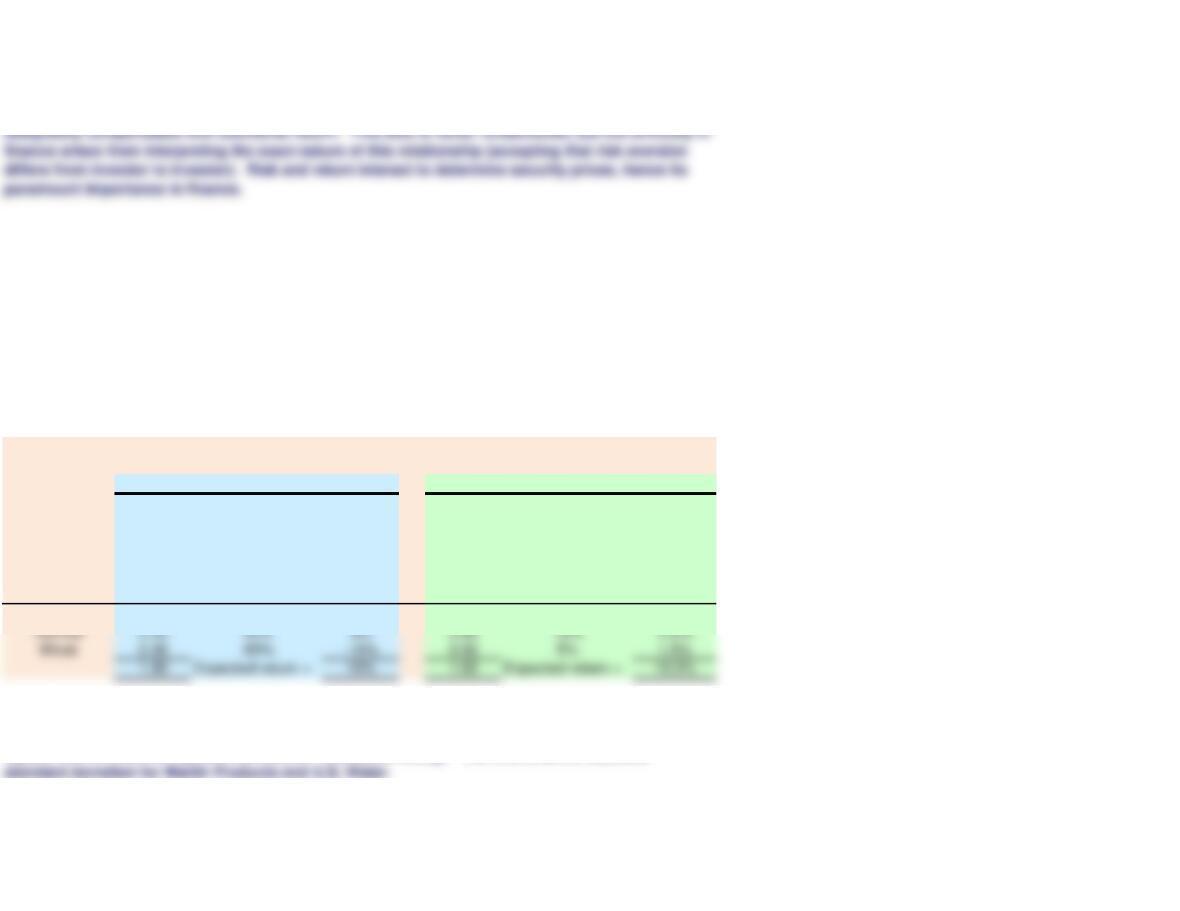

PROBABILITY DISTRIBUTIONS: CALCULATING EXPECTED RETURN

Table 8.1 Probability Distributions and Expected Returns

Rate of Rate of

Economy, Probability Return Probability Return

Which of This if This of This if This

Affects Demand Demand Product Demand Demand Product

Demand Occurring Occurs

(2) × (3) Occurring Occurs (5) × (6)

(1) (2) (3) (4) (5) (6) (7)

Strong 0.30 80% 24% 0.30 15% 4.5%

PROBABILITY DISTRIBUTIONS: CALCULATING STANDARD DEVIATION

U.S. Water

Standard deviation measures the variability of a set of observations and is calculated by finding the

square root of a sum of squared deviations. Sound confusing? The charts below calculate

9/12/2022 15:40

In explaining stand-alone risk, this model introduces probability distributions and the calculation of

expected returns, standard deviations, and coefficients of variation.

The relationship between risk and return is a fundamental axiom in finance. Generally speaking, it

is totally logical to assume that investors are only willing to assume additional risk if they are

Chapter 8. Risk and Rates of Return

The probability distribution is a listing of all possible outcomes and the corresponding probability.

The expected return is calculated by multiplying the possible returns by their corresponding

probabilities.

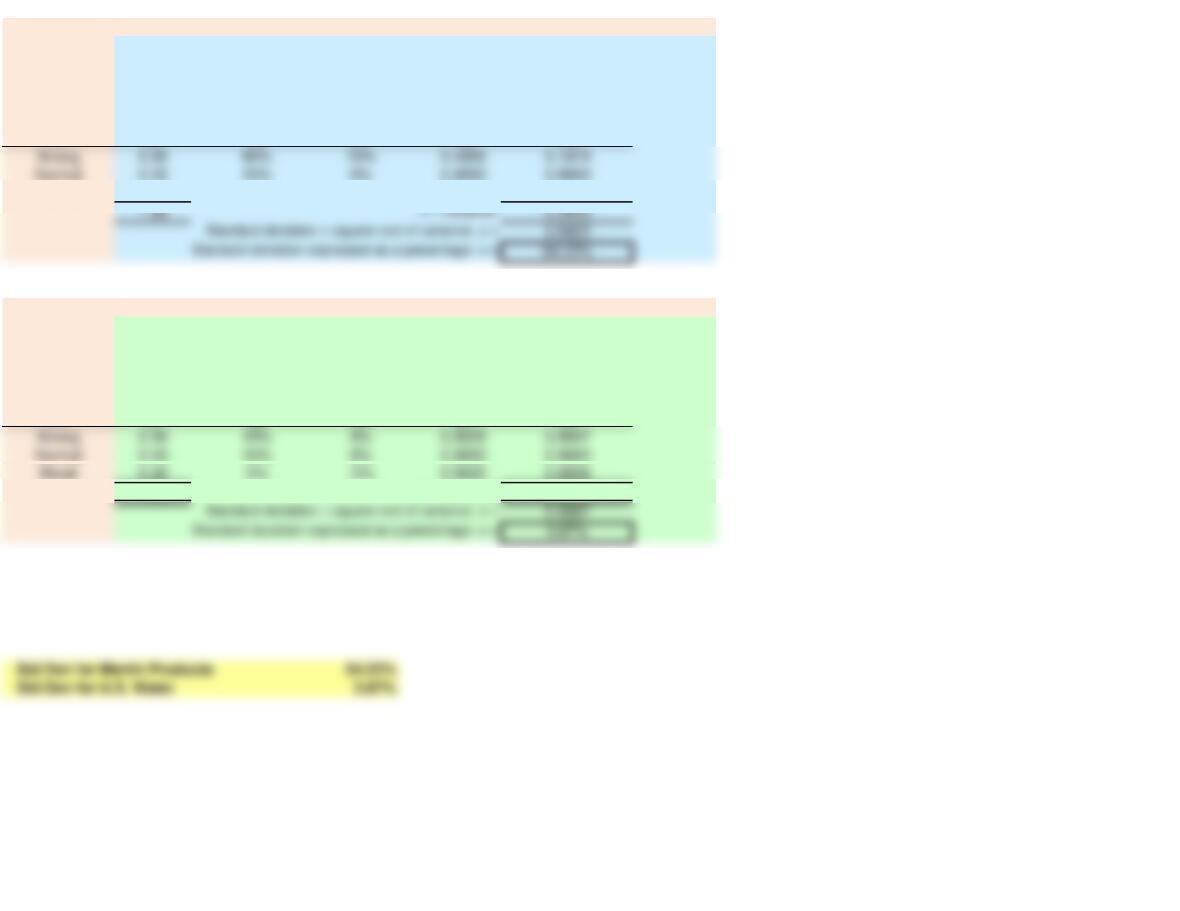

Martin Products

Table 8.2 Calculating Martin Products’ Standard Deviation

Rate of Deviation:

Economy, Probability Return

Actual –

Which of This if This 10% Squared

Affects Demand Demand Expected Deviation Deviation

Demand Occurring Occurs Return Squared

× Prob.

(1) (2) (3) (4) (5) (6)

Weak 0.30 -60% -70% 0.4900 0.1470

1.00 Σ = Variance: 0.2940

Calculating U.S. Water’s Standard Deviation

Rate of Deviation:

Economy, Probability Return

Actual –

Which of This if This 10% Squared

Affects Demand Demand Expected Deviation Deviation

Demand Occurring Occurs Return Squared

× Prob.

(1) (2) (3) (4) (5) (6)

1.00 Σ = Variance: 0.0015

When you calculate standard deviations from expected data in which all states of the world are

accounted for (where the sum of probabilities is 1), you are calculating a population standard

deviation (hence the use of Excel’s population standard deviation function, STDEVP).

Alternatively, you can use Excel’s STDEVP function by entering each return into the formula in the

same proportion as its probability. For instance, Strong demand occurs with a 30% probability, so

enter it three times. Notice this only works if the probabilities are nice, round numbers.

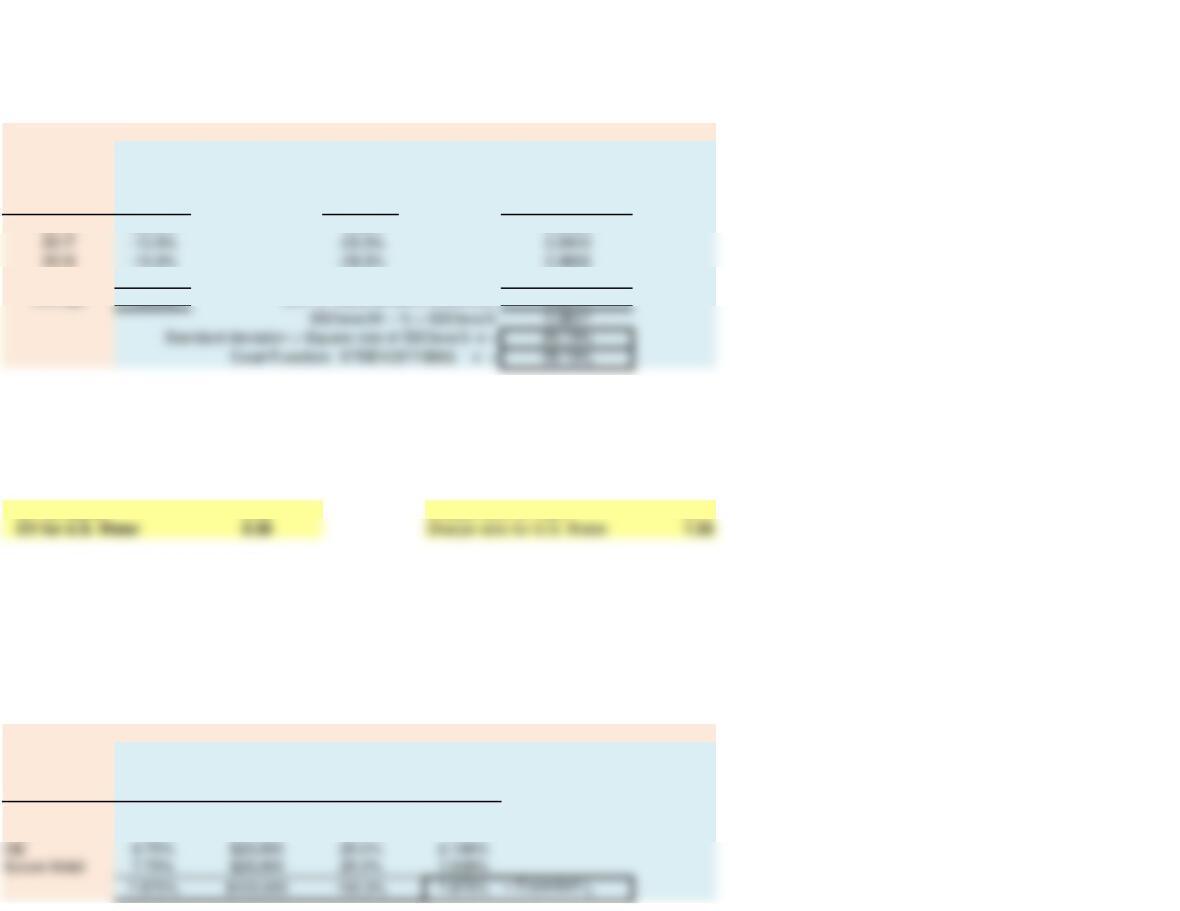

SAMPLE STANDARD DEVIATION CALCULATION

Table 8.3 Finding s Based on Historical Data

Deviation

from Squared

Year Return Average Deviation

(1) (2) (3) (4)

2016 30.0% 19.8% 0.0390

2019 40.0% 29.8% 0.0885

Average 10.3% 0.2541

COEFFICIENT OF VARIATION

Risk-free Rate 4.00%

CV for Martin 5.42 Sharpe ratio for Martin 0.11

CV for U.S. Water 0.39 Sharpe ratio for U.S. Water 1.55

RISK IN A PORTFOLIO CONTEXT (Section 8-3)

PORTFOLIO EXPECTED RETURN

Table 8.4 Expected Return on a Portfolio

Expected Dollars Percent of Product:

Stock Return Invested

Total (wi)(2) × (4)

(1) (2) (3) (4) (5)

Microsoft 7.75% $25,000 25.0% 1.938%

IBM 7.25% $25,000 25.0% 1.813%

More often in finance, you are dealing with a sample of historical data. In this case you need to

calculate a sample standard deviation. This process is outlined in the table below for a fictional

stock, and the Excel shortcut is also shown

Sum of Squared Devs (SSDevs):

Since stocks should be held in conjunction with well-diversified portfolios, it is important to analyze

them in terms of portfolio risk and return.

A problem sometimes arises when comparing standard deviations of different securities. If they

have different expected returns, you may not be able to compare them. The coefficient of variation

shows risk per unit of expected return.

A portfolio’s expected return is merely the weighted average of expected returns of the portfolio’s

components.

PORTFOLIO RISK

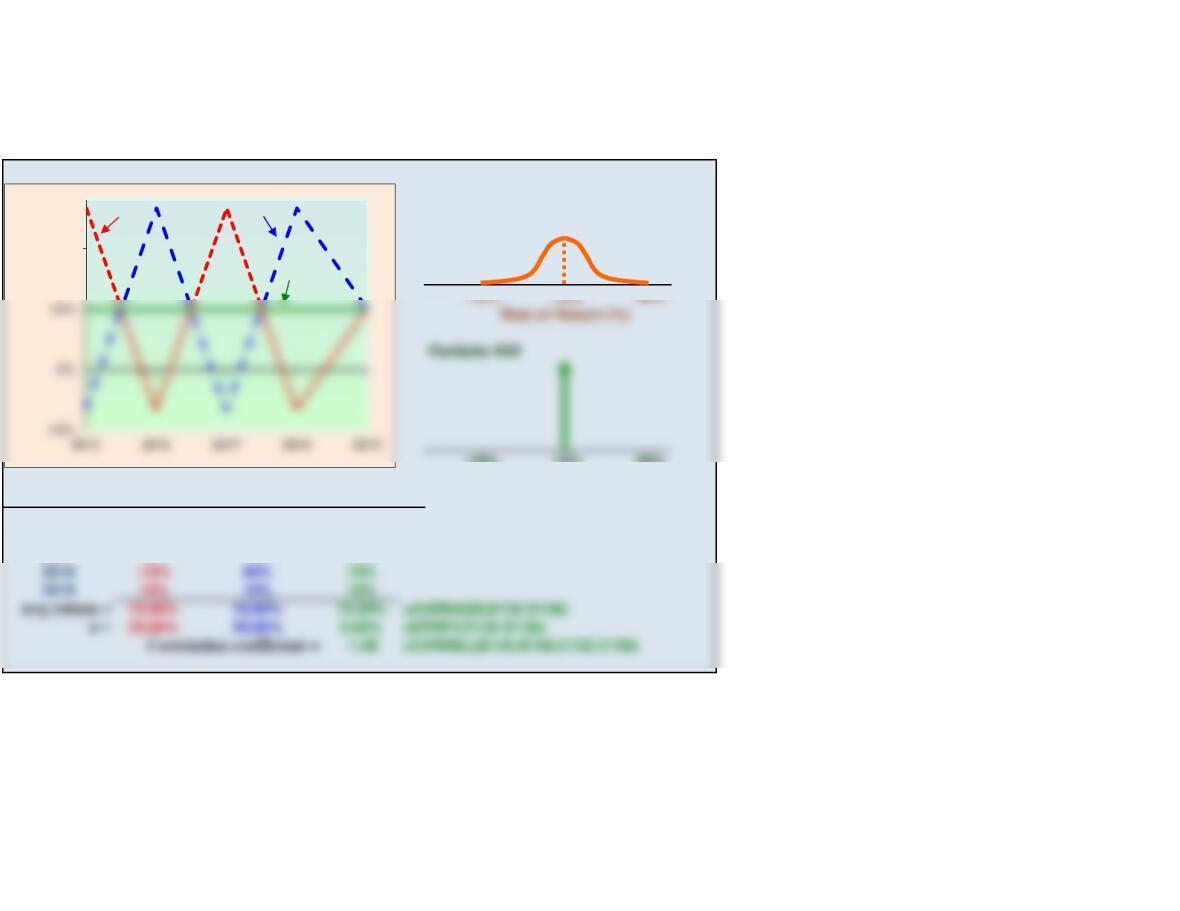

Stocks W and M, held separately

-10% 15% 40%

Rate of Return (%)

Year Stock W Stock M Portfolio WM

2015 40% -10% 15%

2016 -10% 40% 15%

2017 40% -10% 15%

2018 -10% 40% 15%

2019 15% 15% 15%

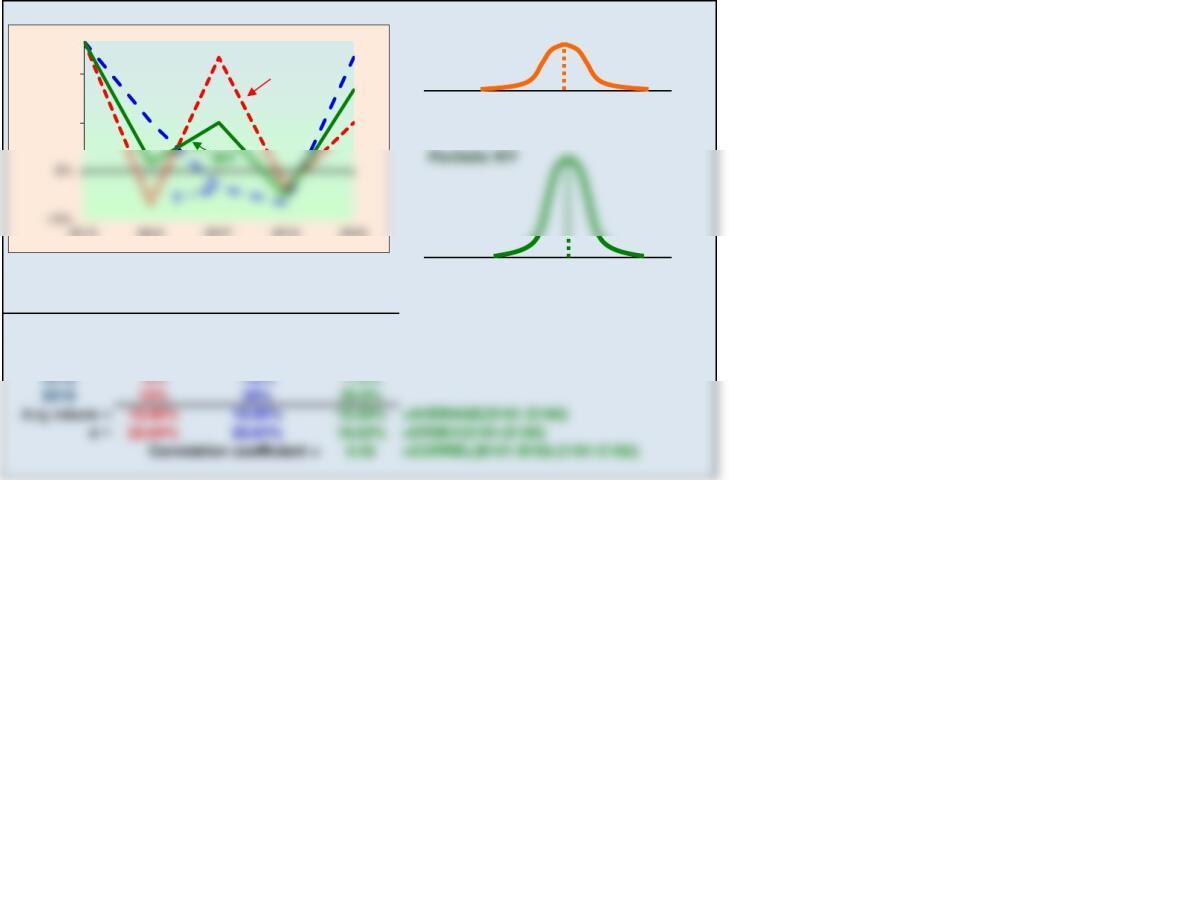

Figure 8.4 Returns with Perfect Negative Correlation, ρ = -1.0

CONCLUSION: When two stocks are perfectly negatively correlated, diversification is its strongest,

and in this case the portfolio return is a certain (no risk) 15%. Of course, this situation is very rare.

Portfolios of stocks are created to diversify investors from unnecessary risk. The diversifiable, or

idiosyncratic, risk is eliminated as more stocks are added. Diversification effects are strongest

when combining uncorrelated assets. The next few tables (and corresponding graphs) illustrate

how creating two-stock portfolios with different correlations between stocks affects the expected

return and risk of various fictional portfolios.

30%

Rate of

Return

W

M

WM

Figure 8.5 Returns with Partial Correlation, ρ = + 0.35

Stocks W and Y, held separately

-10% 15% 40%

Rate of Return (%)

-10% 15% 40%

Rate of Return (%)

Year Stock W Stock Y Portfolio WY

2015 40% 40% 40.0%

2016 -10% 15% 2.5%

2017 35% -5% 15.0%

2019 15% 35% 25.0%

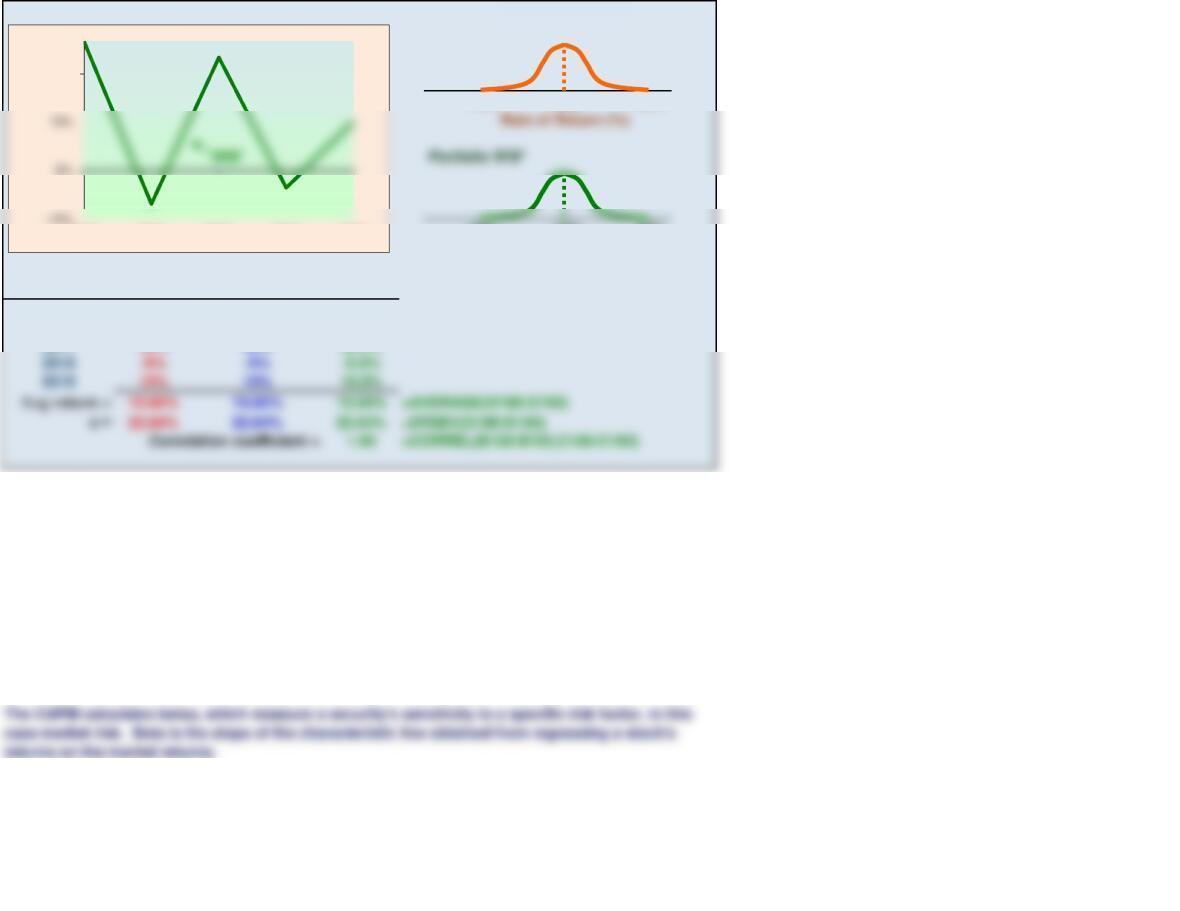

CONCLUSION: In the case where two stocks are somewhat correlated, diversification is effective in

lowering portfolio risk. Here, the portfolio return is an average of the stock returns and risk is

reduced from 22.64% per stock to 18.62% for the portfolio. If more similarly correlated stocks were

added, risk would continue to fall.

15%

30%

2015 2016 2017 2018 2019

Rate of

Return

W

Returns with Perfect Positive Correlation, ρ = + 1.0

Stocks W and W’, held separately

-10% 15% 40%

-10% 15% 40%

Rate of Return (%)

Year Stock W Stock W’ Portfolio WW’

2015 40% 40% 40.0%

2016 -10% -10% -10.0%

2017 35% 35% 35.0%

2019 15% 15% 15.0%

MARKET RISK AND BETA

Diversification can eliminate a lot of risk, but the risk that cannot be diversified away is called

market risk. This is the risk that should be priced in expected returns. An asset pricing model that

does focus on market risk is the Capital Asset Pricing Model (CAPM).

CONCLUSION: When two stocks are perfectly positively correlated, diversification has no effect and

the portfolio’s risk is a weighted average of its stock’s risk. Note, in this graph only the portfolio

returns are visible, but realize that the stock returns follow the same path. In other words, the line

shown is actually all three lines at once.

30%

2015 2016 2017 2018 2019

Rate of

Return

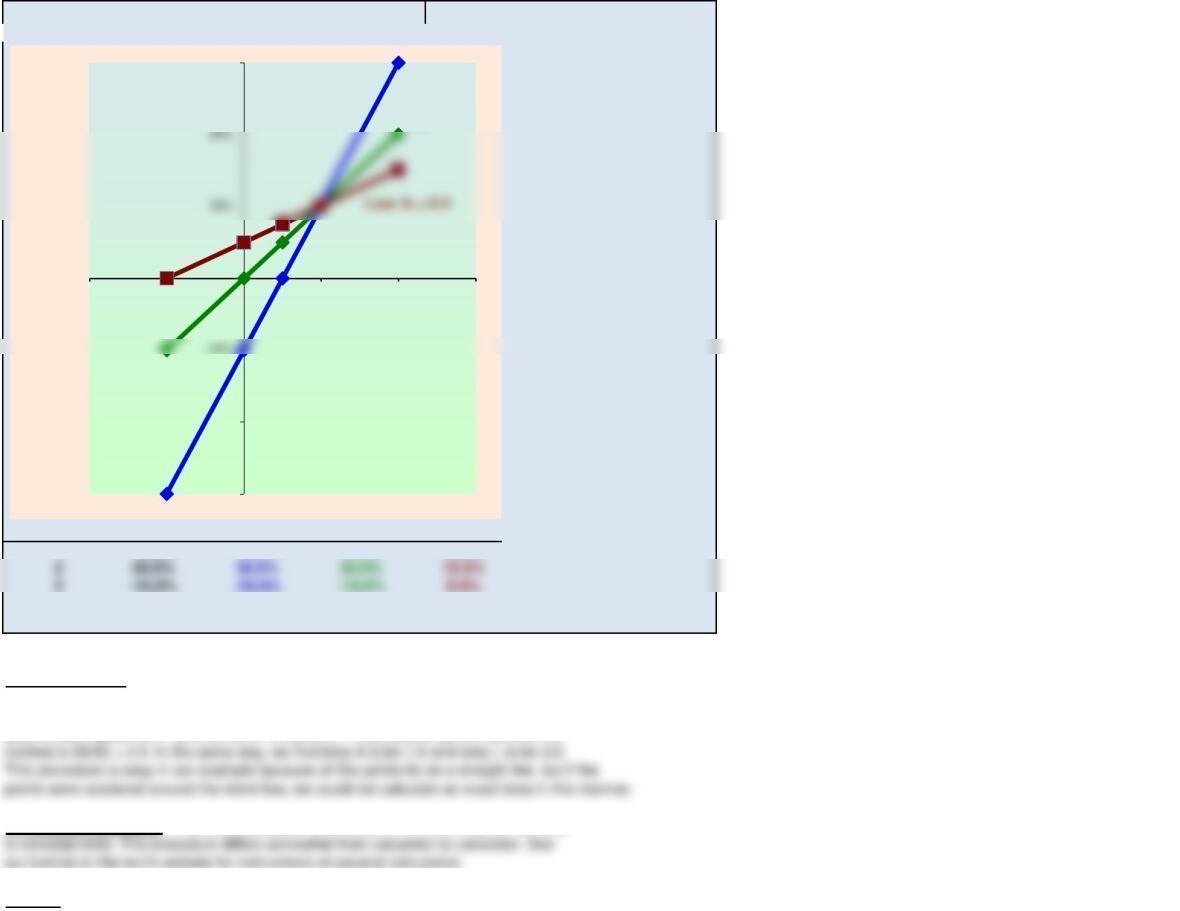

Figure 8.7 Betas: Relative Volatility of Stocks H, A, and L

Year

rMrHrArL

110.0% 10.0% 10.0% 10.0%

40.0% -10.0% 0.0% 5.0%

55.0% 0.0% 5.0% 7.5%

Calculating beta:

1. Rise-Over-Run. Divide the vertical axis change that results from a given change on

the horizontal axis, i.e., the change in the stock’s return divided by the change in the

market return. For Stock H, when the Market rises from -10% to +20%, or by 30%, the

stock’s return goes from -30% to +30%, or by 60%. Thus, beta H by the rise-over-run

2. Financial Calculator. Financial calculators have a built-in function that can be used

3. Excel. Excel’s Slope function can be used to calculate betas. Here are the functions

-30%

-20%

0%

30%

-20% -10% 0% 10% 20% 30%

Return on

Stocks

Return on Market

High: b = 2.0

Average: b = 1.0

220.0% 30.0% 20.0% 15.0%

for our three stocks:

BetaA1.0 =SLOPE(D235:D239,B235:B239)

THE RELATIONSHIP BETWEEN RISK AND RATES OF RETURN (Section 8-4)

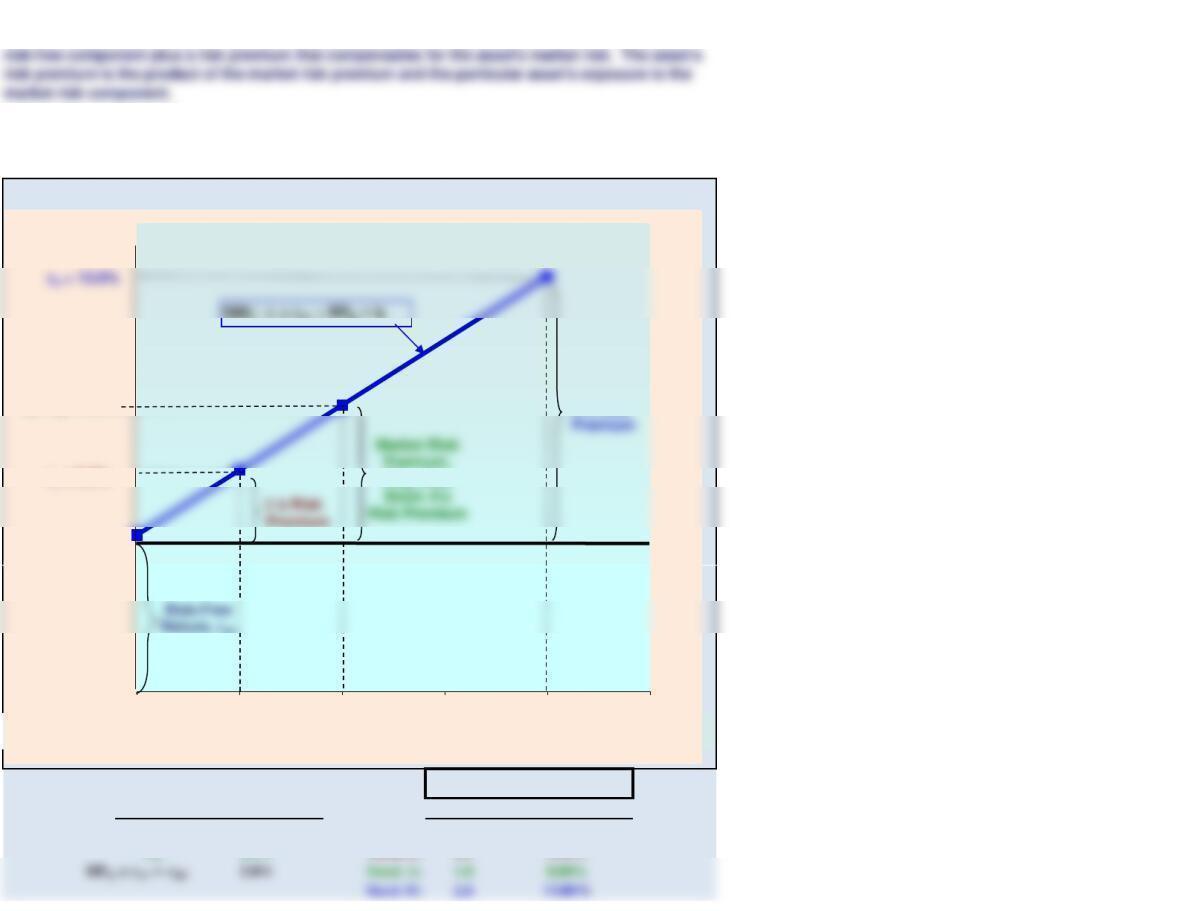

SECURITY MARKET LINE

Figure 8.8 The Security Market Line (SML)

The SML shows the relationship between the stock’s beta and its required return, as predicted by

the CAPM.

The CAPM posits that only market risk matters and an asset’s required return should consist of a

rRF = 3.0%

rL= 5.5%

r

A

= r

M

= 8.0%

Required Rate

of Return

RPM. Also

H’s Risk

SML: ri = rRF + (RPM)bi

Beta

ri

rRF 3.0% Riskless asset: 0.0 3.00%

rM8.0% Stock L: 0.5 5.50%

Key Inputs

0 0.5 1 1.5 2 2.5

Beta Coefficient

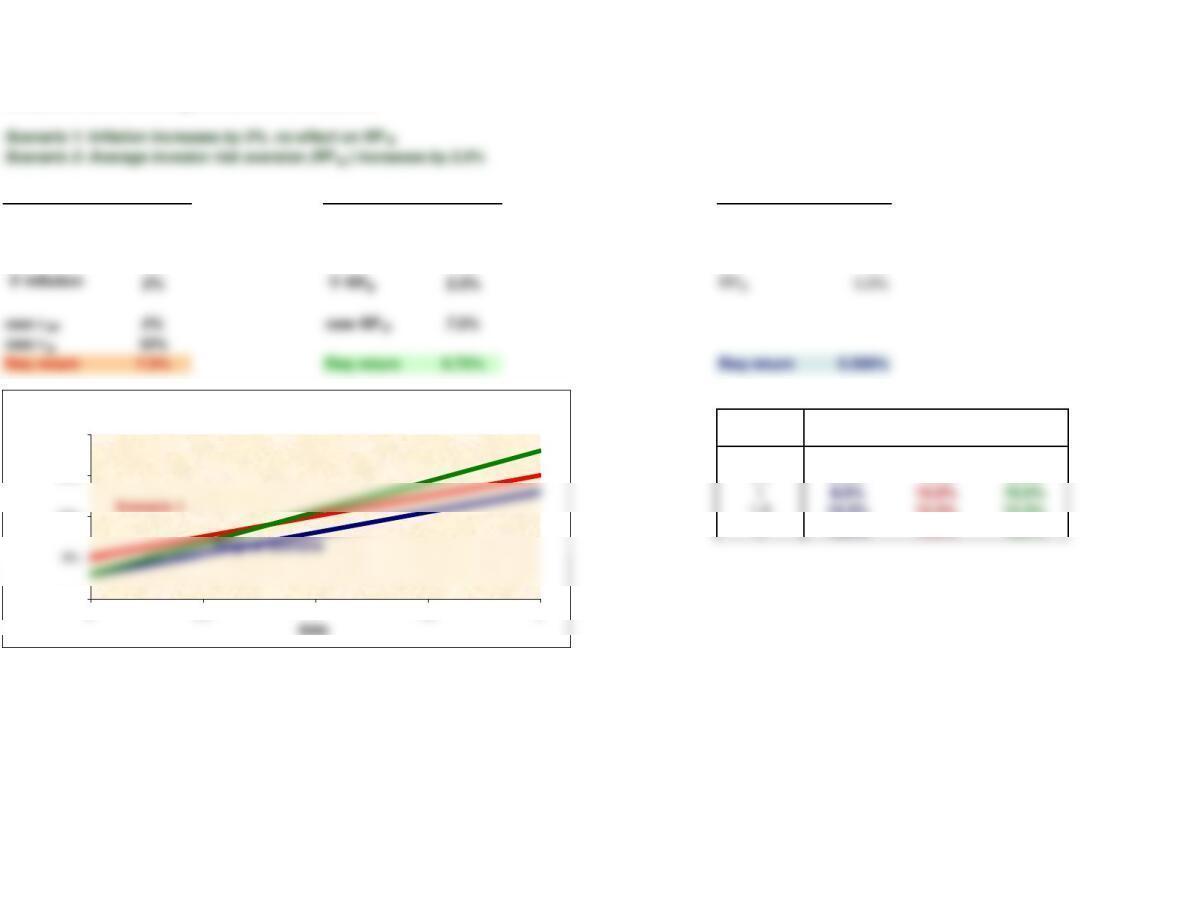

Changing market conditions

Scenario 1 Scenario 2 Original Scenario

old rRF 3% rRF 3% rRF 3.0%

old rM8% old rM8% rM8.0%

bi0.5 bi0.5 bi0.5

DATA TABLE USED TO MAKE SML GRAPH

Original Scenario 1 Scenario 2

Beta

5.5% 7.5% 6.75%

03.0% 5.0% 3.0%

0.5 5.5% 7.5% 6.8%

18.0% 10.0% 10.5%

1.5 10.5% 12.5% 14.3%

213.0% 15.0% 18.0%

Here, two market-affecting scenarios are considered.

The SML prices any asset in the market. So all assets lie somewhere on the SML (in terms of beta

and required return).

10%

15%

20%

Required Return Changes in the SML

Scenario 2

0%

0 0.5 1 1.5 2

SECTION 8-2 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Probability

Return Prob x Ret.

50% 20% 10.0%

6. An investment has a 50% chance of producing a 20% return, a 25% chance of producing an

8% return, and a 25% chance of producing a -12% return. What is its expected return?

SECTION 8-3 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Stock

Investment Beta

X$25,000 1.5

7. An investor has a 2-stock portfolio with $25,000 invested in Stock X and $50,000 invested in

Stock Y. X’s beta is 1.50 and Y’s beta is 0.60. What is the beta of the investor’s portfolio?

SECTION 8-4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Beta 1.2

Risk-free rate 4.5%

7. A stock has a beta of 1.2. Assume that the risk-free rate is 4.5% and the market risk

premium is 5%. What is the stock’s required rate of return?

Year

Market (rM) Stock (rJ)12/12/2018

36.60% 12.30%

530.60% 40.10%

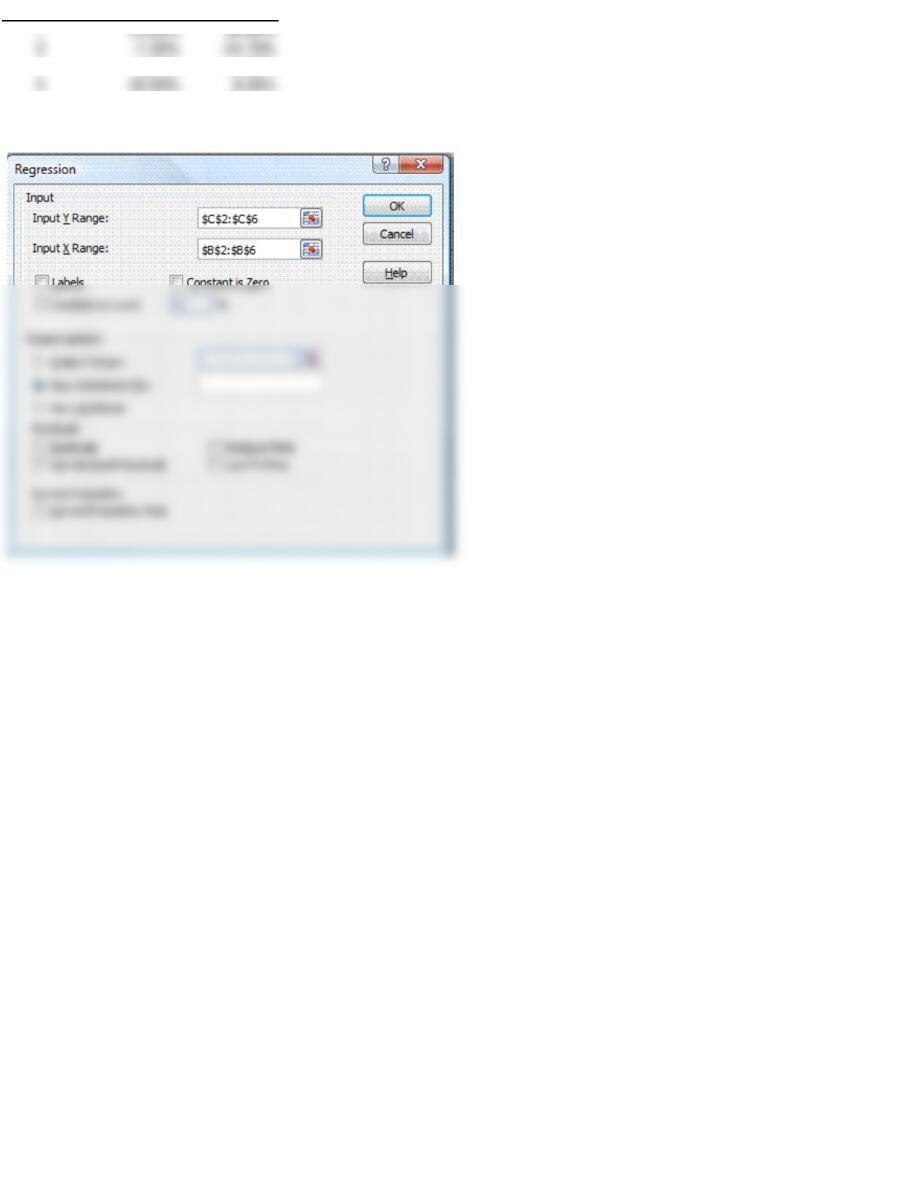

Dialog Box to Set Up Regression Analysis

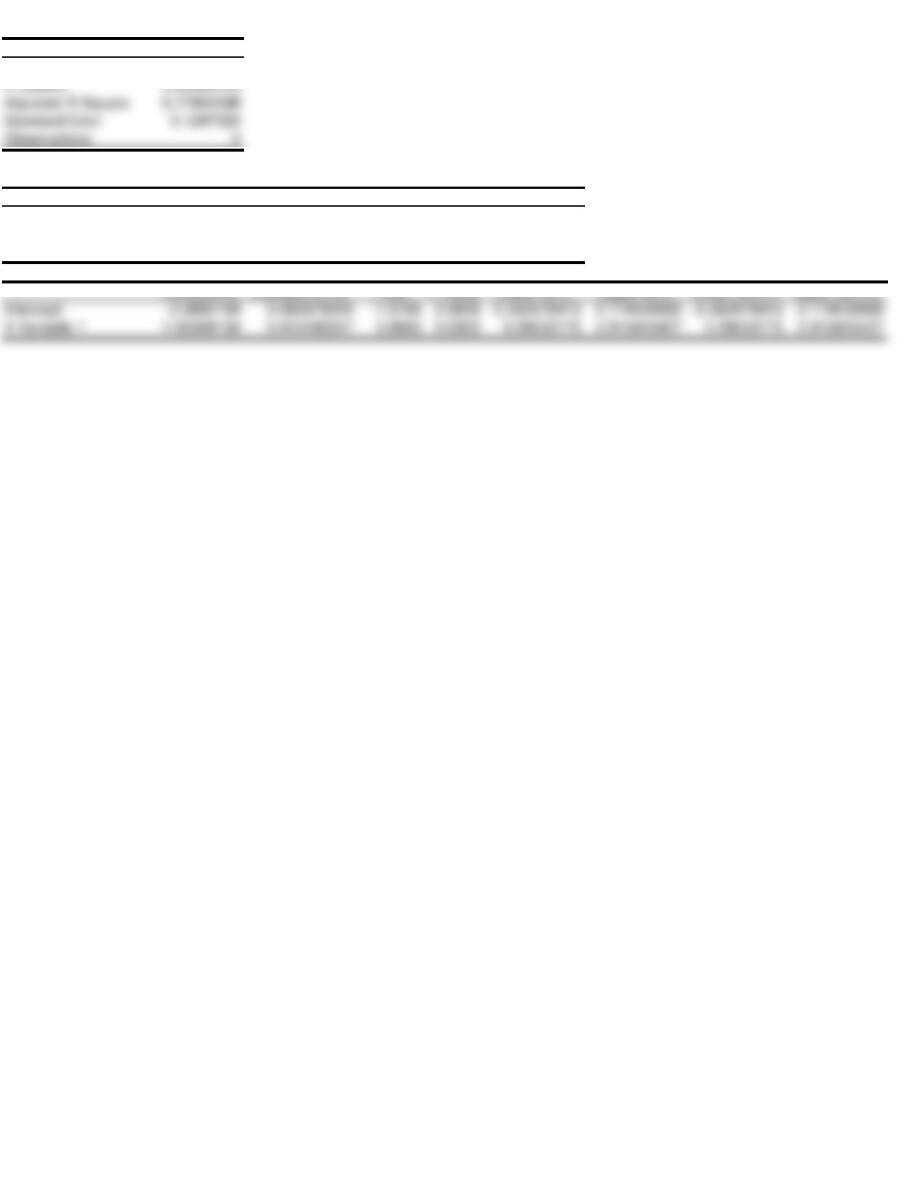

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.91339175

ANOVA

df SS MS F Significance F

Regression 1 0.234979562 0.23498 15.103 0.030195958

Residual 3 0.046674438 0.01556

Total 4 0.281654

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%