Chapter 8

Financial Options and Applications in Corporate Finance

ANSWERS TO END-OF-CHAPTER QUESTIONS

8-1 a. An option is a contract which gives its holder the right to buy or sell an asset at some

predetermined price within a specified period of time. A call option allows the holder

to buy the asset, while a put option allows the holder to sell the asset.

b. A simple measure of an option’s value is its exercise value. The exercise value is

8-2 The market value of an option is typically higher than its exercise value due to the

speculative nature of the investment. Options allow investors to gain a high degree of

personal leverage when buying securities. The option allows the investor to limit his or

her loss but amplify his or her return. The exact amount this protection is worth is the

options time value, which is the difference between the option’s price and its exercise

value.

8-3 (1) An increase in stock price causes an increase in the value of a call option. (2) An

increase in strike price causes a decrease in the value of a call option. (3) An increase in

Answers and Solutions: 8 – 2

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

8-1 Exercise value = Current stock price – strike price

8-2 Option’s strike price = $15; Exercise value = $22; Time value = $5;

V = ? P0 = ?

8-3 P = $15; X = $15; t = 0.5; rRF = 0.06; 2 = 0.12; d1 = 0.24495;

d2 = 0.0000; N(d1) = 0.59675; N(d2) = 0.500000; V = ?

Using the Black-Scholes Option Pricing Model, you calculate the option’s value as:

Answers and Solutions: 8 – 3

8-5

.3319.0

33333.05.0

)333333.0)](2/25.0(05.0[)35/$30($ln

tσ

)]t2/

2

(σ

RF

[r(P/X)ln

1

d−=

++

=

++

=

d2 = d1 – (t)0.5 = -0.3319 – 0.5(0.33333)0.5 = -0.6206.

8-6 The stock’s range of payoffs in one year is $26 – $16 = $10. At expiration, the option

will be worth $26 – $21 = $5 if the stock price is $26, and zero if the stock price $16. The

range of payoffs for the stock option is $5 – 0 = $5.

Equalize the range to find the number of shares of stock: Option range / Stock range =

$5/$10 = 0.5.

8-7 The stock’s range of payoffs in six months is $18 – $13 = $5. At expiration, the option

will be worth $18 – $14 = $4 if the stock price is $18, and zero if the stock price $13. The

range of payoffs for the stock option is $4 – 0 = $5.

Answers and Solutions: 8 – 5

SOLUTION TO SPREADSHEET PROBLEMS

8-8 The detailed solution for the problem is available in the file Ch08 P08 Build a Model

Solution.xls at the textbook’s web site.

Mini Case: 8 – 6

MINI CASE

Assume that you have just been hired as a financial analyst by Triple Play Inc., a mid-sized

California company that specializes in creating high-fashion clothing. Since no one at

Triple Play is familiar with the basics of financial options, you have been asked to prepare

a brief report that the firm’s executives could use to gain at least a cursory understanding

of the topic.

To begin, you gathered some outside materials the subject and used these materials to

draft a list of pertinent questions that need to be answered. In fact, one possible approach

to the paper is to use a question-and-answer format. Now that the questions have been

drafted, you have to develop the answers.

a. What is a financial option? What is the single most important characteristic of

an option?

Answer: A financial option is a contract which gives its holder the right to buy (or sell) an

b. Options have a unique set of terminology. Define the following terms: (1) call

option; (2) put option; (3) strike price; (4) expiration date; (5) exercise value (6)

option price; (7) time value; (8) covered option; (9) naked option; (10) in-the-

money call; (11) out-of-the-money call; and (12) LEAPS.

Answer: 1. A call option is an option to buy a specified number of shares of a security

within some future period.

Mini Case: 8 – 7

Mini Case: 8 – 8

c. Consider Triple Play’s call option with a $25 strike price. The following table

contains historical values for this option at different stock prices:

Stock Price Call Option Price

$25 $ 3.00

30 7.50

35 12.00

40 16.50

45 21.00

50 25.50

1. Create a table which shows (a) stock price, (b) strike price, (c) exercise value, (d)

option price, and (e) the time value, which is the option’s price less its exercise

value.

Answer: Price Of Strike Exercise Value Market Price Time Value

Stock Price Of Option Of Option (D) – (C) =

c. 2. What happens to the option’s time value as the stock price rises? Why?

Answer: As the table shows, the option’s time value declines as the stock price increases. This

Mini Case: 8 – 9

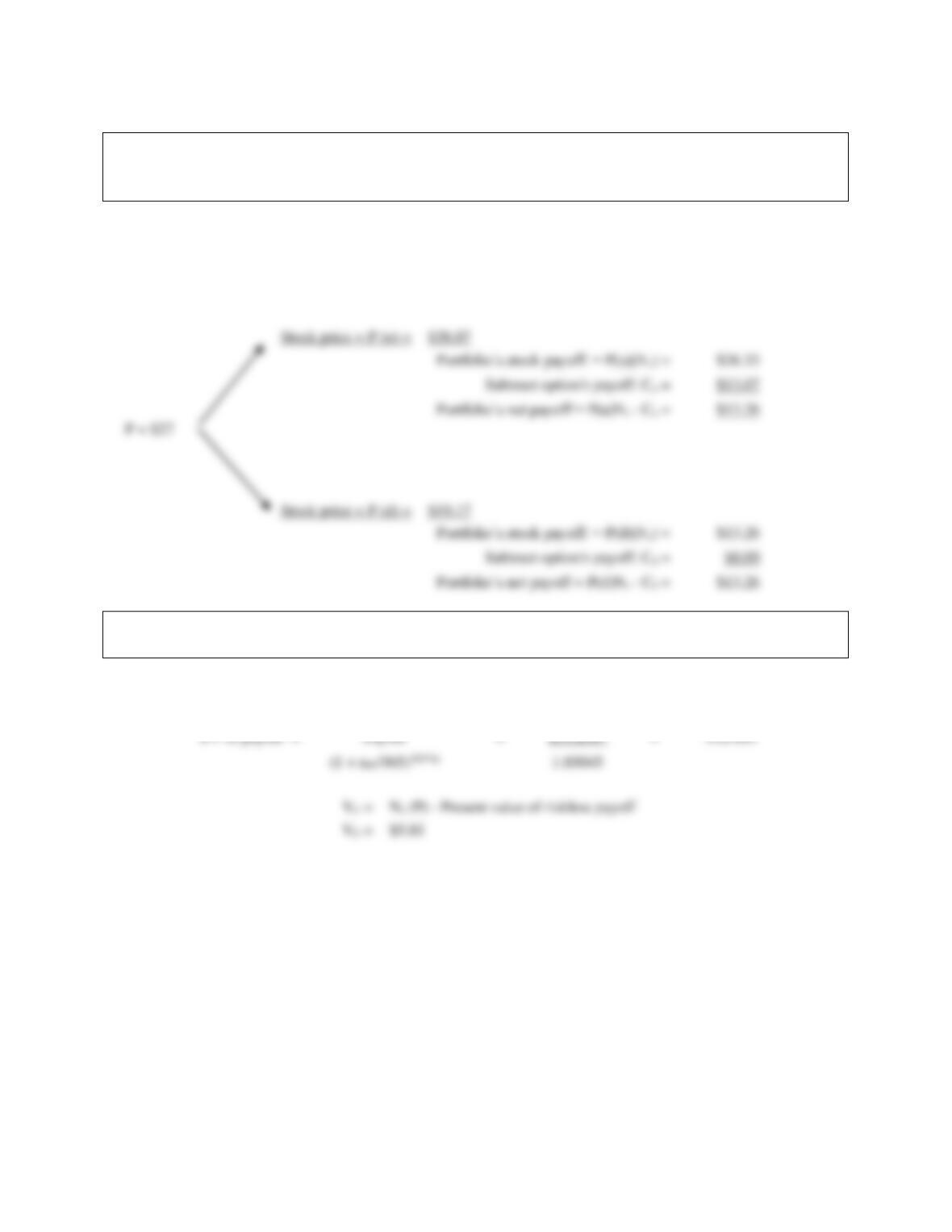

d. Consider a stock with a current price of P = $27. Suppose that over the next 6

months the stock price will either go up by a factor of 1.41 or down by a factor of

0.71. Consider a call option on the stock with a strike price of $25 which expires

in 6 months. The risk-free rate is 6%.

1. Using the binomial model, what are the ending values of the stock price? What

are the payoffs of the call option?

Answer: The assumptions which underlie the OPM are as follows:

Strike price: X =

$25.00

$27.00

$13.07

Mini Case: 8 – 10

d. 2. Suppose you write 1 call option and buy Ns shares of stock. How many shares

must you buy to create a portfolio with a riskless payoff (which is called a hedge

portfolio)? What is the payoff of the portfolio?

Answer:

Ns =

Cu – Cd

=

0.69153

P(u – d)

:

d. 3. What is the present value of the hedge portfolio’s riskless payoff? What is the

value of the call option?

Answer:

=

$12.865

1.03045

$5.81

$38.07

$26.33

$13.26

$19.17

$13.26

$13.26

Mini Case: 8 – 11

d. 4. What is a replicating portfolio? What is arbitrage?

Answer: If you borrow an amount equal to the present value of the hedge portfolio’s

riskless payoff and purchase Ns shares of stock, the portfolio’s payoff’s will

e. In 1973, Fischer Black and Myron Scholes developed the Black-Scholes Option

Pricing Model (OPM).

1. What assumptions underlie the OPM?

Answer: The assumptions which underlie the OPM are as follows:

• The stock underlying the call option provides no dividends during the life of the

option.

Mini Case: 8 – 12

e. 2. Write out the three equations that constitute the model.

Answer: The OPM consists of the following three equations:

V = P[N(d1) –

trRF

Xe−

[N(d2)].

Mini Case: 8 – 13

e. 3. What is the value of the following call option according to the OPM?

Stock Price = $27.00.

Strike Price = $25.00

Time To Expiration = 6 Months = 0.5 years.

Risk-Free Rate = 6.0%.

Stock Return Standard Deviation = 0.49.

Answer: The input variables are:

P = $27.00; X = $25.00; rRF = 6.0%; t = 6 months = 0.5 years; and = 0.49.

Mini Case: 8 – 14

f. What impact does each of the following call option parameters have on the value

of a call option?

1. Current Stock Price

2. Strike Price

3. Option’s Term To Maturity

4. Risk-Free Rate

5. Variability Of The Stock Price

Answer: 1. The value of a call option increases (decreases) as the current stock price

increases (decreases).

g. What is put-call parity?

Answer: Put-call parity specifies the relationship between puts, calls, and the underlying stock

price that must hold to prevent arbitrage: