CHAPTER 8

PERFECT COMPETITION

In this chapter, you will find:

Learning Outcomes

Chapter Outline with PowerPoint Script

Chapter Summary

Teaching Points (as on Prep Card)

Solutions to Problems Appendix

Experiential Assignment

INTRODUCTION

This chapter introduces the benchmark market structure—perfect competition—and then looks at profit

maximization for the perfectly competitive firm in the short run and in the long run. Perfectly competitive

firms have no control over the market price so only quantity produced can be varied. The level of output

that maximizes firm profits, or minimizes firm losses, in the short and long run are discussed next.

According to the golden rule of profit maximization, firms produce output to the point where marginal cost

equals marginal revenue. The last third of the chapter examines long-run industry supply and the long-run

adjustment process.

LEARNING OUTCOMES

8-1 Describe the market structure of perfect competition.

Market structures describe important features of the economic environment in which firms operate. A

8-2 Determine the perfectly competitive firm’s profit-maximizing output in the short run.

All firms try to maximize economic profit, which is any profit above normal profit, by controlling

8-3 Outline the conditions under which a firm should decide to produce in the short run rather than

shut down, even though it incurs an economic loss.

Firms that have not identified a profitable level of output can either operate at a loss or shut down. In

8-4 Describe a perfectly competitive firm’s short-run supply curve.

If price exceeds average variable cost, the firm produces the quantity at which marginal revenue

equals marginal cost. A firm changes the rate of output if the market price changes. As long as the

Chapter 8 Perfect Competition 114

8-5 Explain why in perfect competition, there are no economic profits or losses in the long run.

In the long run, firms enter and leave the market, adjust the scale of operations, and experience no

8-6 Explain why, in some perfectly competitive industries, market supply curves slope upward in the

long run.

The firms in some industries encounter higher average costs as industry output expands in the long

8-7 Summarize how market equilibrium in perfect competition results in productive efficiency and

allocative efficiency.

Perfectly competitive markets exhibit both productive efficiency (because output is produced using

the most efficient combination of resources available) and allocative efficiency (because the goods

produced are those most valued by consumers). In equilibrium, a perfectly competitive market

allocates goods so that the marginal cost of the final unit produced equals the marginal value that con-

sumers attach to that final unit.

CHAPTER OUTLINE WITH POWERPOINT SCRIPT

USE POWERPOINT SLIDES 2-6 FOR THE FOLLOWING SECTION

An Introduction to Perfect Competition

Perfectly Competitive Market Structure: A perfectly competitive market:

Has many buyers and sellers.

USE POWERPOINT SLIDE 7 FOR THE FOLLOWING SECTION

Short-Run Profit Maximization

Total Revenue Minus Total Cost: The firm maximizes economic profit by finding the rate of output at

which total revenue exceeds total cost by the greatest amount.

Chapter 8 Perfect Competition 115

USE POWERPOINT SLIDE 8-11 FOR THE FOLLOWING SECTION

Marginal Revenue Equals Marginal Cost in Equilibrium

Marginal Revenue: The change in total revenue from selling another unit of output:

Market price = Marginal revenue = Average revenue

USE POWERPOINT SLIDES 12-14 FOR THE FOLLOWING SECTION

Minimizing Short-Run Losses

Short run: A period too short to allow existing firms to leave the industry.

Fixed Costs and Minimizing Losses: If a firm shuts down, it must still pay fixed costs. A firm produces

USE POWERPOINT SLIDES 15-19 FOR THE FOLLOWING SECTION

The Firm and Industry Short-Run Supply Curves

Short-Run Firm Supply Curve: That portion of a firm’s marginal cost curve that intersects and rises

USE POWERPOINT SLIDES 20-28 FOR THE FOLLOWING SECTION

Perfect Competition in the Long Run

Zero Economic Profit in the Long Run

Entry or exit of firms drives economic profit to zero so firms earn only a normal profit.

USE POWERPOINT SLIDES 29-31 FOR THE FOLLOWING SECTION

The Long-Run Industry Supply Curve: Shows the relationship between price and quantity

supplied once firms fully adjust to any short-term economic profit or loss resulting from a change in

USE POWERPOINT SLIDE 32 FOR THE FOLLOWING SECTION

Perfect Competition and Efficiency

Chapter 8 Perfect Competition 116

Productive Efficiency: Produce output at the minimum of the long-run average cost curve. Making stuff

right but maybe making the wrong stuff.

USE POWERPOINT SLIDES 33-35 FOR THE FOLLOWING SECTION

What’s So Perfect About Perfect Competition?

Gains from voluntary exchange through competitive markets:

CHAPTER SUMMARY

Market structures describe important features of the economic environment in which firms operate. These

features include the number of buyers and sellers in the market, the ease or difficulty of entering the

market, differences in the product across firms, and the forms of competition among firms.

A perfectly competitive market is characterized by (a) a large number of buyers and sellers, each too small

to influence market price; (b) firms in the market supply a commodity, which is a product undifferentiated

across producers; (c) buyers and sellers possess full information about the availability and prices of all

resources, goods, and technologies; and (d) firms and resources are freely mobile in the long run.

For a firm to produce in the short run, rather than shut down, the market price must at least cover the

firm’s average variable cost. If price is below average variable cost, the firm shuts down. That portion of

the marginal cost curve at or rising above the average variable cost curve becomes the perfectly

competitive firm’s short–run supply curve. The horizontal sum of each firm’s supply curve forms the

market supply curve. As long as price covers average variable cost, each perfectly competitive firm

maximizes profit or minimizes loss by producing where marginal revenue equals marginal cost.

Chapter 8 Perfect Competition 117

Perfectly competitive markets exhibit both productive efficiency (because output is produced using the

most efficient combination of resources available) and allocative efficiency (because the goods produced

TEACHING POINTS

1. A thorough understanding of the perfectly competitive market is essential to understanding the oth-

er market structures. Reiterate that in the perfectly competitive model no firm has control over the

market price. Students often find this assumption unrealistic because firms should have control over

2. The perfectly competitive model is often attacked because of its many supposedly unrealistic

assumptions. The purpose of the model is to illustrate competitive forces that are present in many

3. Students sometimes object to the idea that firms make output decisions based on marginal analysis.

The important point to stress is that although firms may not make marginal decisions explicitly, they

4. It is important to work through the firms’ decision process using numerical examples. For instance,

students often become confused as to why firms do not operate at the lowest point of average cost in

5. Students sometimes wonder why zero profits in the long run represent a stable, normal situation.

The key is to have them recall that this is zero economic profit. Zero economic profit means that

all resources are being paid exactly enough to keep them in the industry (i.e., their opportunity cost).

6. Aside from applying marginal analysis and understanding how firms make profit-maximizing

decisions in the perfectly competitive model, the importance of this chapter is in its implications for

economic efficiency. In Chapter 6, students were introduced to the notion of consumer surplus,

considering the demand curve to be a marginal benefit curve. Similarly, in this chapter, students

Chapter 8 Perfect Competition 118

will discover that for the competitive firm, the supply curve is the marginal cost curve. Just as

consumer surplus exists whenever the price is lower than the marginal benefits associated with

SOLUTIONS TO PROBLEMS APPENDIX

1. (Market Structure) Define market structure. What factors are considered in determining the

market structure of a particular industry?

Market structure refers to the important features that determine the level of competition in an

2. (Perfect Competition Characteristics) Describe the characteristics of perfect competition.

A perfectly competitive market is characterized by (1) many buyers and sellers—so many that

each buys or sells only a tiny fraction of the total amount in the market; (2) firms sell a com-

3. (Perfect Competition) What type of demand curve does a perfectly competitive firm face? Why?

The perfectly competitive firm faces a demand curve that is horizontal at the prevailing market

4. (Short-Run Profit Maximization) A perfectly competitive firm has the following fixed and

variable costs in the short run. The market price for the firm’s product is $150.

Output FC VC TC TR Profit/Loss

0 $100 $ 0 ___ ___ ___

1 100 100 ___ ___ ___

2 100 180 ___ ___ ___

Chapter 8 Perfect Competition 119

3 100 300 ___ ___ ___

4 100 440 ___ ___ ___

5 100 600 ___ ___ ___

6 100 780 ___ ___ ___

a. Complete the table.

b. At what output rate does the firm maximize profit or minimize loss?

c. What is the firm’s marginal revenue at each positive level of output? Its average revenue?

d. What can you say about the relationship between marginal revenue and marginal cost for

output rates below the profit-maximizing (or loss-minimizing) rate? For output rates above

the profit-maximizing (or loss-minimizing) rate?

a. Output FC VC TC TR Profit/Loss

0 $100 $ 0 $100 $ 0 $–100

5. (Minimizing Loss in the Short Run) Explain the different options a firm has to minimize losses

in the short run.

A firm in the short run is limited in its options, as the short run by definition is not enough time

6. (Short-Run Loss) Suppose a firm decides to shut down in the short run. What is the resulting loss?

If a firm shuts down in the short run its losses will equal its total fixed costs (because there

7. (The Short-Run Firm Supply Curve) Use the following data to answer the questions below:

Q VC MC AVC

1 $10 ___ ___

2 16 ___ ___

3 20 ___ ___

4 25 ___ ___

5 31 ___ ___

Chapter 8 Perfect Competition 120

6 38 ___ ___

7 46 ___ ___

8 55 ___ ___

9 65 ___ ___

a. Calculate the marginal cost and average variable cost for each level of production.

b. How much would the firm produce if it could sell its product for $5? For $7? For $10?

c. Explain your answers.

d. Assuming that its fixed cost is $3, calculate the firm’s profit at each of the production levels

determined in part (b).

For the answers to part a, see columns MC and AVC, respectively, in the following table:

Q VC MC AVC

1 $10 $10 $10.00

2 16 6 8.00

8. (The Short-Run Firm Supply Curve) Each of the following situations could exist for a perfectly

competitive firm in the short run. In each case, indicate whether the firm should produce in the

short run or shut down in the short run, or whether additional information is needed to determine

what it should do in the short run.

a. Total cost exceeds total revenue at all output levels.

b. Total variable cost exceeds total revenue at all output levels.

c. Total revenue exceeds total fixed cost at all output levels.

d. Marginal revenue exceeds marginal cost at the current output level.

e. Price exceeds average total cost at all output levels.

f. Average variable cost exceeds price at all output levels.

g. Average total cost exceeds price at all output levels.

a. Need additional information. Information regarding FC and/or VC is required. If a portion

Chapter 8 Perfect Competition 121

9. (Zero Economic Profits in Long Run) Why would firms choose to operate in a perfectly competi-

tive market even though they earn no economic profit in the long run?

Zero economic profit means total revenue is sufficient to cover all costs including the oppor-

10. (Zero Economic Profits in Long Run) Why is there no economic profit for perfectly competitive

firms in the long run? Why is there no economic loss?

11. (The Long-Run Industry Supply Curve) A normal good is being produced in a constant-cost,

perfectly competitive industry. Initially, each firm is in long-run equilibrium.

a. Graphically illustrate and explain the short-run adjustments for the market and the firm to a

decrease in consumer incomes. Be sure to discuss any changes in output levels, prices,

profits, and the number of firms.

b. Next, show on your graph and explain the long-run adjustment to the income change. Be

sure to discuss any changes in output levels, prices, profits, and the number of firms.

a. In the right panel of the following graph, the drop in consumer incomes decreases market

Chapter 8 Perfect Competition 122

b. In the long run, economic losses cause some firms to exit the industry, decreasing market

supply. Firms exit and supply decreases until losses are eliminated. In a constant-cost industry,

12. (Long-Run Industry Supply) Why does the long-run industry supply curve for an increasing-cost

industry slope upward? What causes the increasing costs in an increasing-cost industry?

The long-run supply curve in an increasing-cost industry is upward sloping because resource

prices rise as existing firms increase their scale of operation and as new firms enter. If market

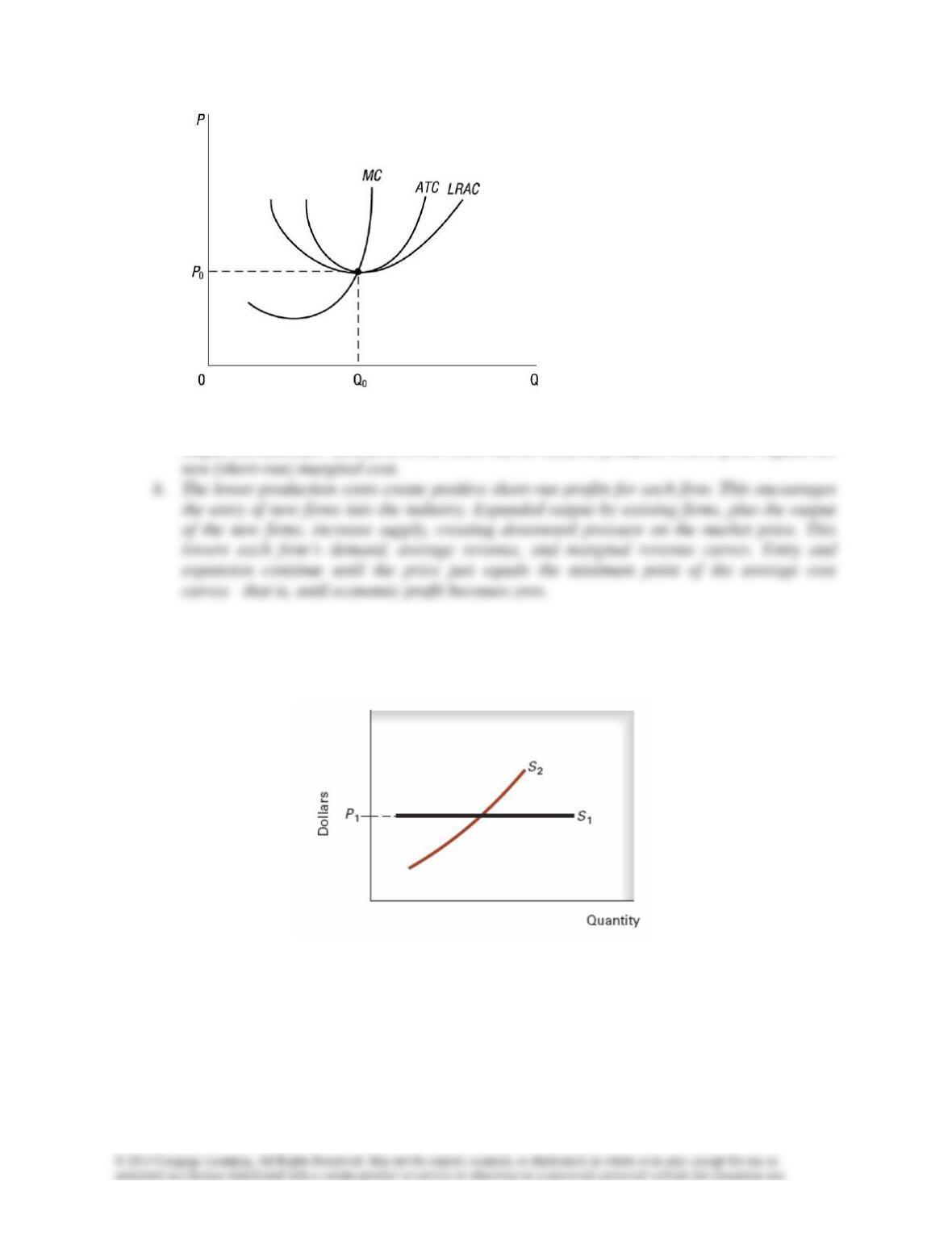

13. (Perfect Competition in the Long Run) Draw the short- and long-run cost curves for a

competitive firm in long-run equilibrium. Indicate the long-run equilibrium price and quantity.

a. Discuss the firm’s short-run response to a reduction in the price of a variable resource.

b. Assuming that this is a constant-cost industry, describe the process by which the industry

returns to long-run equilibrium following a change in market demand.

Chapter 8 Perfect Competition 123

a. A reduction in a resource price shifts all cost curves downward. Assuming a vertical shift,

output increases for each firm in the short run as the firm produces where price equals the

14. (The Long-Run Industry Supply Curve) The following graph shows possible long-run market

supply curves for a perfectly competitive industry. Determine which supply curve indicates a

constant-cost industry and which an increasing-cost industry.

a. Explain the difference between a constant-cost industry and an increasing-cost industry.

b. Distinguish between the long-run impact of an increase in market demand in a constant-cost

industry and the impact in an increasing-cost industry.

S1= constant cost; S2= increasing cost

Chapter 8 Perfect Competition 124

a. A constant-cost industry uses such a small portion of the resources available that increasing

output does not increase production costs. The average cost curve does not shift up or

15. (What’s So Perfect About Perfect Competition?) Use the following data to answer the questions.

Quantity Marginal Cost Marginal Benefit

0 — —

1 $2 $10

2 $3 9

3 $4 8

4 $5 7

5 $6 6

6 $8 5

7 $10 4

8 $12 3

a. For the product shown, assume that the minimum point of each firm’s average variable cost

curve is at $2. Construct a demand and supply diagram for the product and indicate the

equilibrium price and quantity.

b. On the graph, label the area of consumer surplus as f. Label the area of producer surplus as

g.

c. If the equilibrium price were $2, what would be the amount of producer surplus?

a & b.

Chapter 8 Perfect Competition 125

Experiential Assignment

1. Financial markets are quintessential examples of perfectly competitive markets. And, of course, the

Wall Street Journal features in-depth coverage of these markets. Have students go to the Money and