Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

8

9

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

40

41

42

43

44

45

A B C D E F G H I J

12/9/2012

Situation

Features of Common Stock

Classified Stock

THE DISCOUNTED DIVIDEND APPROACH

D1D2DN

( 1 + rs ) ( 1 + rs ) 2 ( 1 + rs ) N

Sam Strother and Shawna Tibbs are senior vice presidents of Mutual of Seattle. They are co-directors of the company's

pension fund management division, with Strother having responsibility for fixed income securities (primarily bonds) and

+

+

. . . .

Chapter 7 Mini Case

b. (1.) Write out a formula that can be used to value any stock, regardless of its dividend pattern.

1. Common Stock represents ownership. 2. Ownership implies control. 3. Stockholders elect directors. 4. Directors hire

management who attempt to maximize stock price.

Here is the basic dividend valuation equation:

Classified Stock carries special provisions. For example, shares could be classified as founders' shares which come with

voting rights but dividend restrictions.

a. Describe briefly the legal rights and privileges of common stockholders.

𝐏𝟎=

58

59

60

61

62

69

70

71

72

73

74

75

76

A B C D E F G H I J

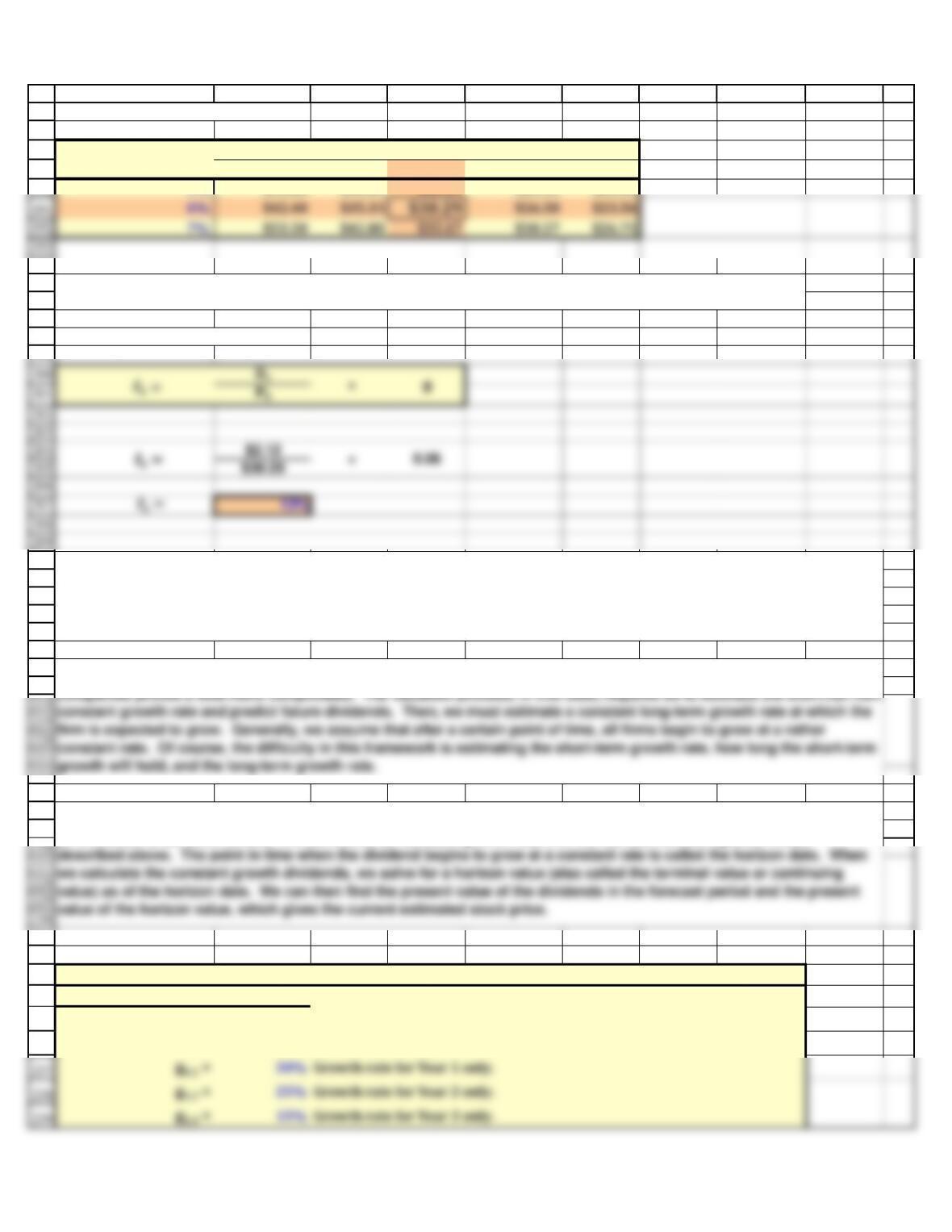

VALUING STOCKS WITH A CONSTANT GROWTH RATE

D1

( rs – g )

In this stock valuation model, we first assume that the dividend and stock will grow forever at a constant growth rate.

Naturally, assuming a constant growth rate for the rest of eternity is a rather bold statement. However, considering the

In this equation, the long-run growth rate (g) can be approximated by multiplying the firm's return on assets by the

retention ratio. Generally speaking, the long-run growth rate of a firm is likely to fall between 5% and 8% a year.

𝐏𝟎=

77

78

79

80

81

82

83

84

94

95

96

97

98

99

100

112

113

114

115

116

117

118

A B C D E F G H I J

Constant Growth Model:

INPUTS:

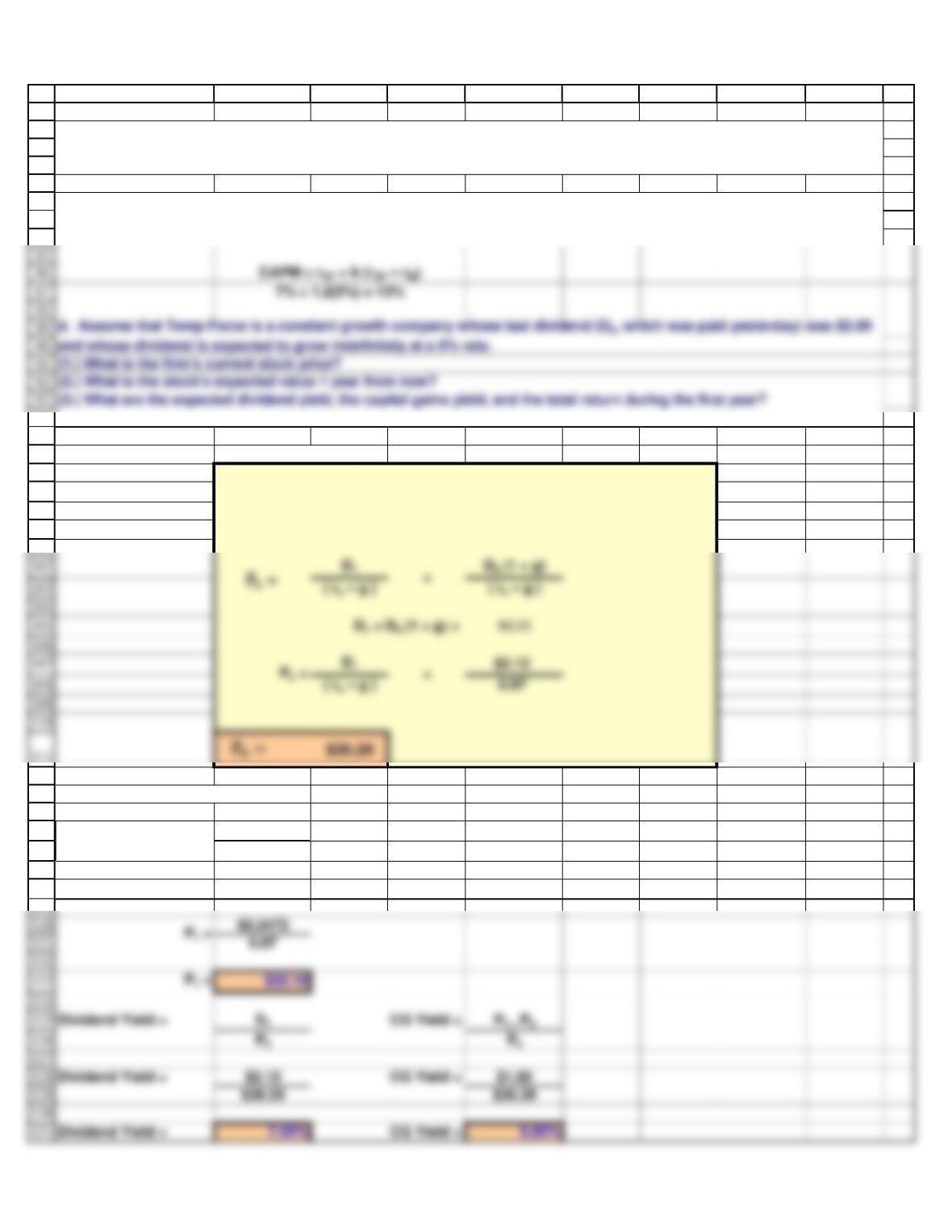

D0 = $2.00

g = 6%

rs =13.0%

Stock Price 1 year from now:

D2

( rs – g )

D2 = D1 (1+g) = $2.2472

(c.) What happens if a company has a constant g which exceeds rs? Will many stocks have expected g > rs in the short

run (i.e., for the next few years)? In the long run (i.e., forever)? Answer: See Chapter 7 PowerPoint file.

c. Assume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 7.0%, and that the

market risk premium is 5%. What is the required rate of return on the firm’s stock?

P1 =

132

133

134

135

147

148

149

150

151

152

153

154

155

156

157

167

168

169

170

171

172

A B C D E F G H I J

Total Yield =

Dividend

Yield

+

CG

Yield

INPUTS:

P0 = $30.29

D0 = $2.00

g = 6%

rs =13.0%

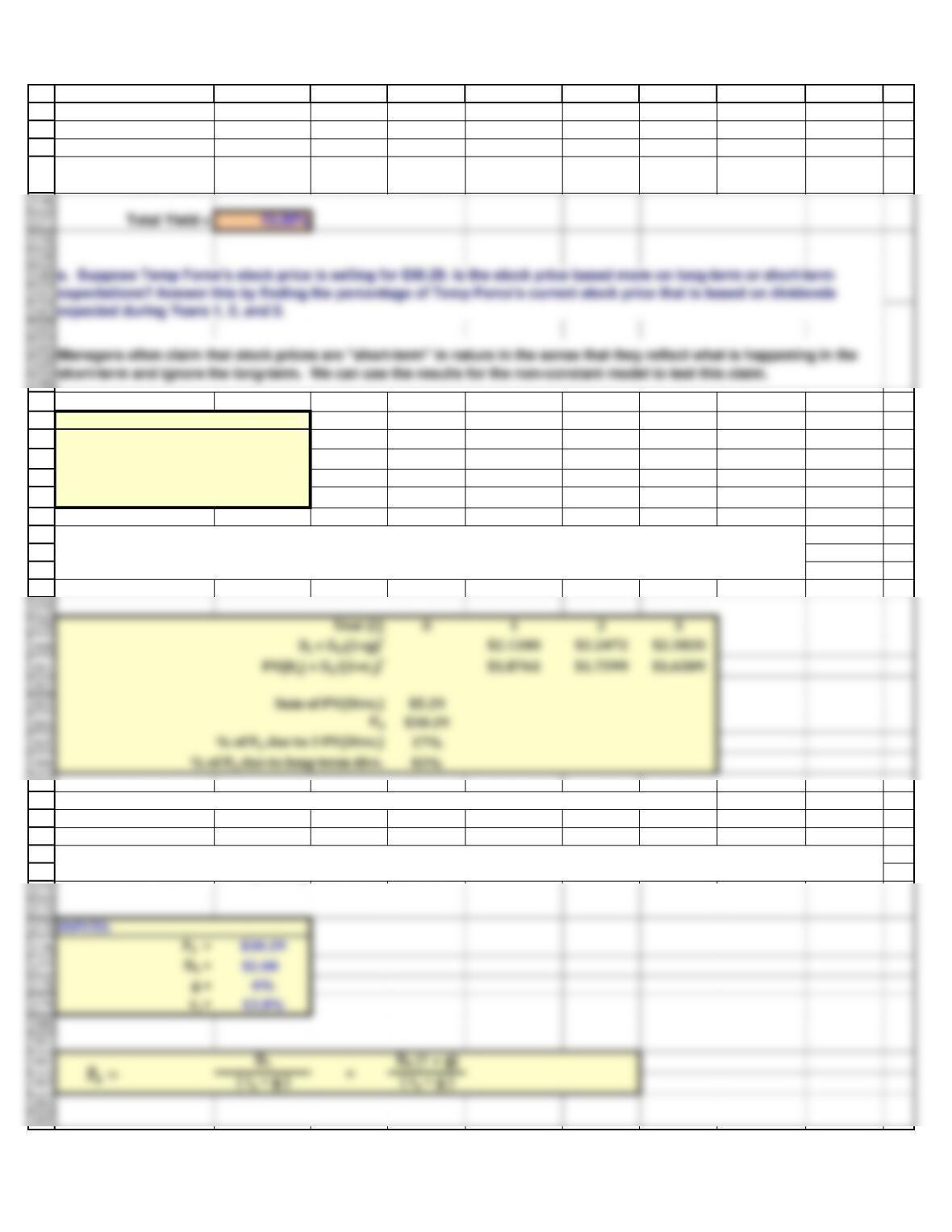

For most stocks, the percentage of the current price that is due to long-term cash flows is over 80%.

The first step is to forecast the dividends for the next 3 years. Then we find the present value of these dividends

and compare that PV with the current stock price, which reflects the PV of all future dividends.

f. Why are stock prices volatile? Using Temp Force as an example, what is the impact on the estimated stock price if g

falls to 5% or rises to 7%? If rs changes to 12% or to 14%?

186

187

188

189

190

194

195

196

197

198

210

211

212

213

214

215

216

217

222

223

224

225

231

232

233

234

235

236

A B C D E F G H I J

Estimated Price for Changes in Inputs

Growth Rate: g Required Return: rs

11.0% 12.0% 13.0% 14.0% 15.0%

5% $35.00 $30.00 $26.25 $23.33 $21.00

Rearrange to rate of return formula

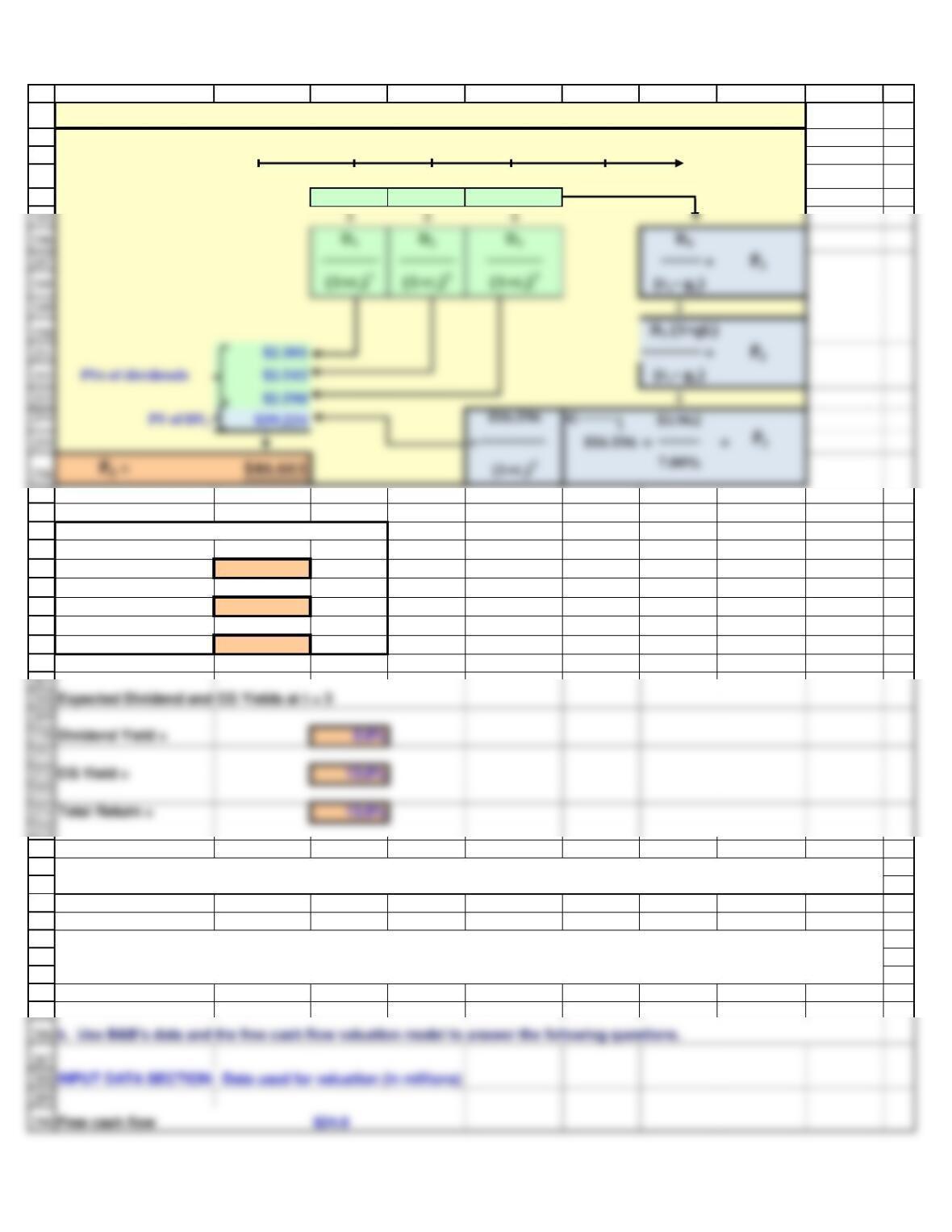

Process for Finding the Value of a Nonconstant Growth Stock

INPUTS:

D0 = $2.00 Last dividend the company paid.

rs = 13.0% Stockholders' required return.

For many companies, it is unreasonable to assume that it grows at a constant growth rate. Hence, valuation for these

Specifically, we will predict as many future dividends as we can and discount them back to the present. Then we will treat

all dividends to be received after the convention of constant growth rate with the Gordon constant growth model

h. Now assume that Temp Force’s dividend is expected to experience nonconstant growth of 30% from Year 0 to Year 1,

25% from Year 1 to Year 2, and 15% from Year 2 to Year 3. After Year 3, dividends will grow at a constant rate of 6%. What

is the stock’s intrinsic value under these conditions? What are the expected dividend yield and capital gains yield during

the first year? What are the expected dividend yield and capital gains yield during the fourth year (from Year 3 to Year 4)?

g. Now assume that the stock is currently selling at $30.29. What is its expected rate of return?

240

241

242

243

244

257

258

259

260

261

262

263

264

265

266

276

277

278

279

280

281

282

283

284

285

A B C D E F G H I J

gL = 6% Constant long-run growth rate for all years after Year 3.

Growth rate 30% 25% 15% 6% 6%

Year 0 1 2 3 4

Dividends $2.6000 $3.2500 $3.7375

Expected Dividend and CG Yields at t = 0

Dividend Yield = 5.6%

CG Yield = 7.4%

Total Return = 13.0%

i. What is free cash flow (FCF)? What is the weighted average cost of capital? What is the free cash flow valuation model?

Answer: See Chapter 7 Mini Case Show

j. Use a pie chart to illustrate the sources that comprise a hypothetical company’s total value. Using another pie chart,

show the claims on a company’s value. How is equity a residual claim? Answer: See Chapter 7 Mini Case Show

291

292

293

294

295

296

297

298

304

305

306

307

308

309

310

311

312

324

325

326

327

328

329

330

331

332

A B C D E F G H I J

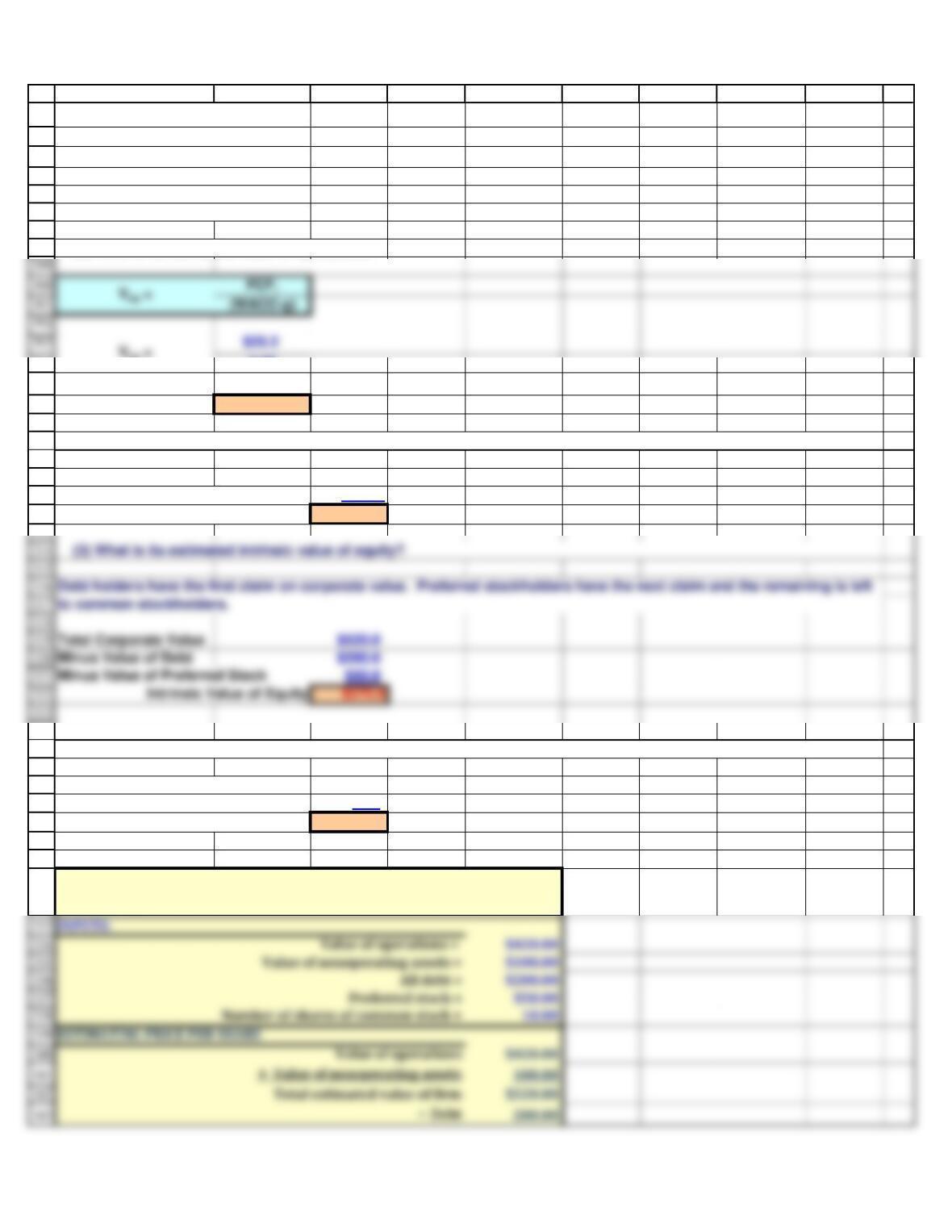

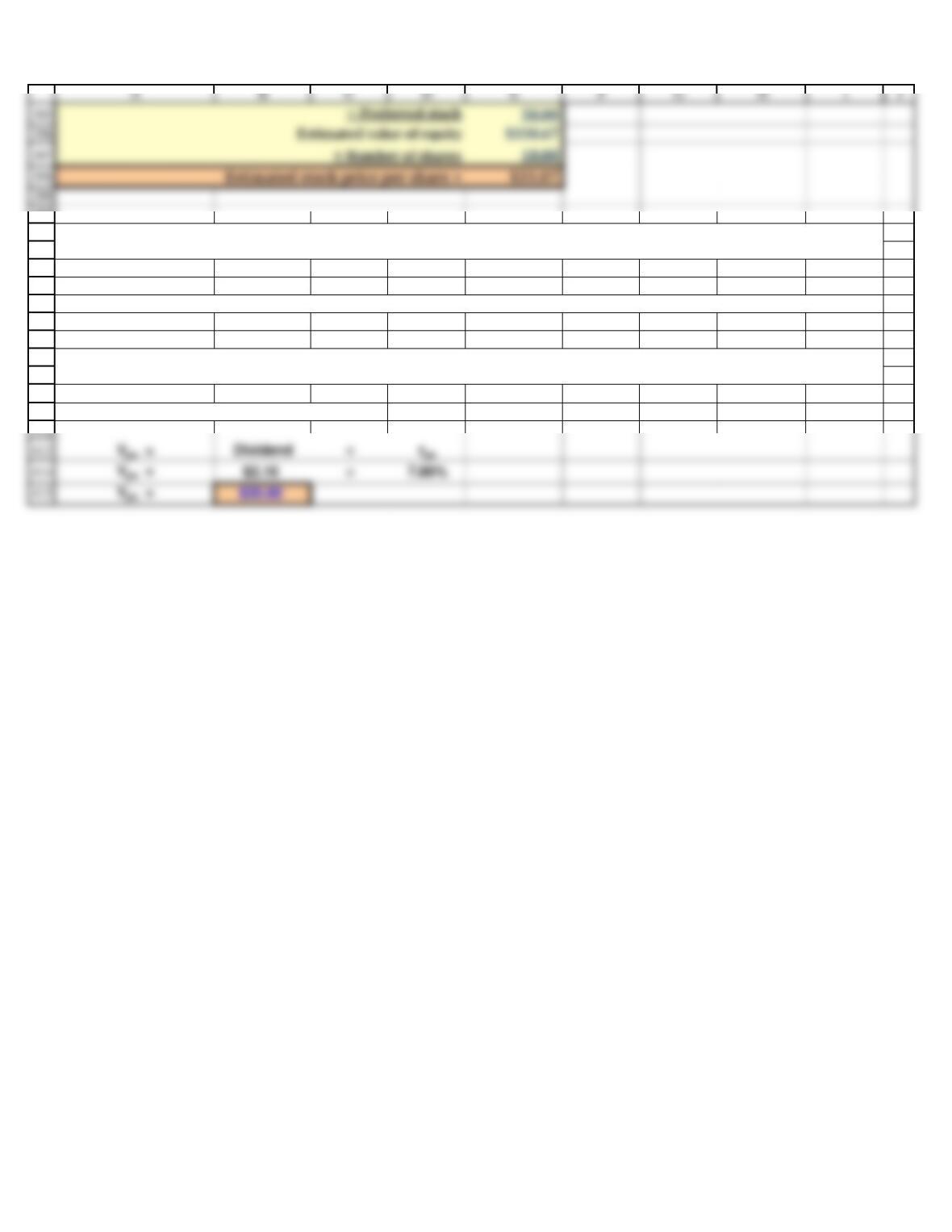

11%

5%

$100.0

$200.0

$50.0

Number of shares of stock 10.0

(1) What is its estimated value of operations?

0.06

Vop = $420.00

Value of Operation $420.0

Plus Value of Non-operating Assets $100.0

Total Corporate Value $520.0

Intrinsic Value of Equity $270.0

Divided by number of shares 10.0

Intrinsic price per share $27.00

(2) What is its estimated total corporate value?

(4) What is its estimated intrinsic stock price per share?

Marketable securities

Debt

Preferred stock

WACC

Growth

Estimating the Value of R&R’s Stock Price (Millions, Except for Per

Share Data)

344

345

346

347

348

349

350

351

352

353

354

355

356

357

358

359

360

361

362

363

364

365

366

378

379

380

381

382

383

384

A B C D E F G H I J

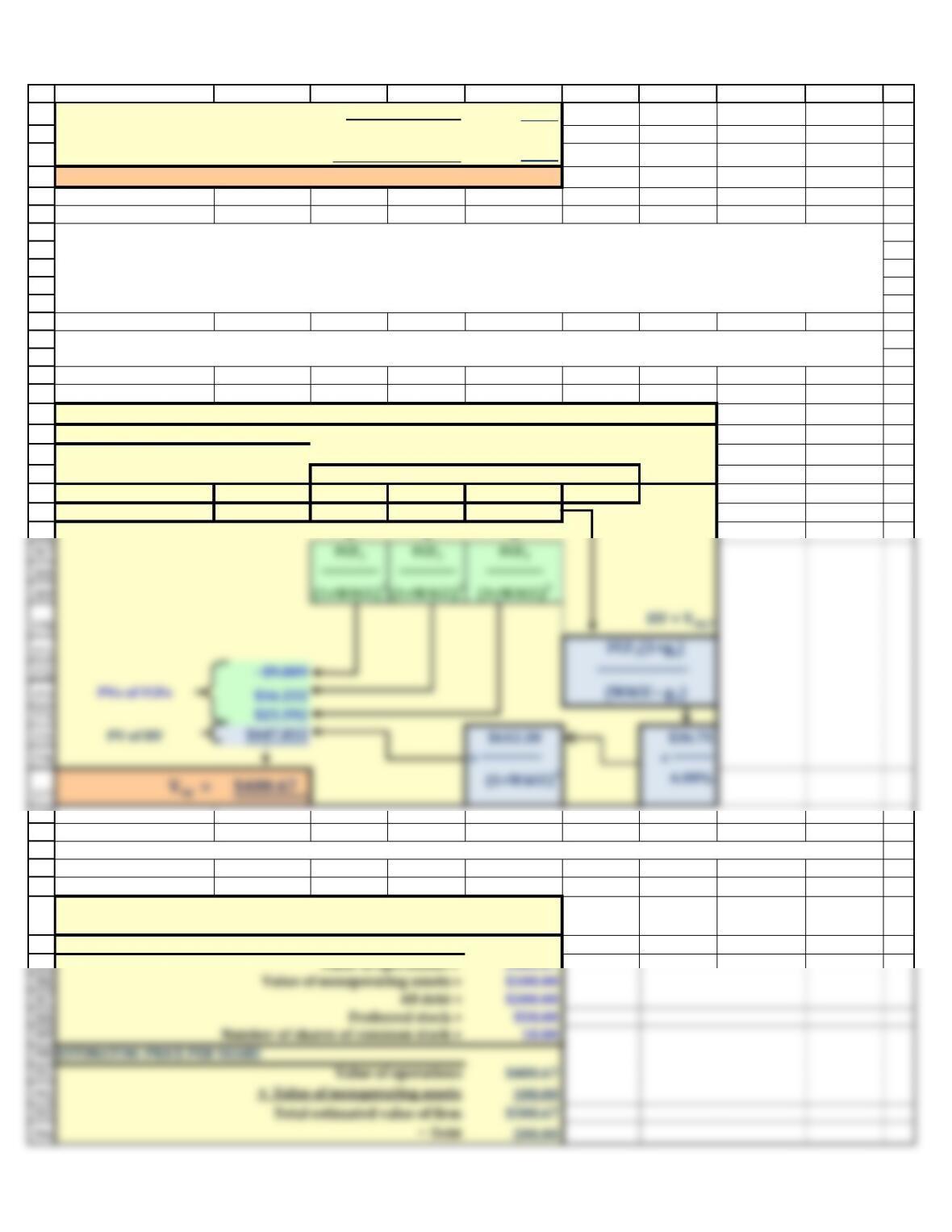

− Preferred stock 50.00

Estimated value of equity $270.00

÷ Number of shares 10.00

Estimated stock price per share = $27.00

B&B's Value of Operations (Millions of Dollars)

INPUTS:

gL = 5.00%

WACC = 11.00%

Year 0 1 2 3 4

FCF −$10.00 $20.00 $35.00

↓ ↓ ↓

INPUTS:

(1.) What is its horizon value (i.e., its value of operations at year three)? What is its current value of operations (i.e., at

time zero)?

Estimating the Value of R&R’s Stock Price (Millions, Except for Per

Share Data)

Projections

(2.) What is its value of equity on a price per share basis?

l. You have just learned that B&B has undertaken a major expansion that will change its expected free cash flows to −$10

million in 1 year, $20 million in 2 years, and $35 million in 3 years. After 3 years, free cash flow will grow at a rate of 5%. No

new debt or preferred stock were added, the investment was financed by equity from the owners. Assume the WACC is

unchanged at 11% and it that there are still has 10 million shares of stock outstanding.

400

401

402

403

404

405

406

407

408

409

410

411

The dividend stream would be a perpetuity.

o. What is preferred stock? Suppose a share of preferred stock pays a dividend of $2.10 and investors require a return of

7%. What is the estimated value of the preferred stock?

m. Compare and contrast the free cash flow valuation model and the dividend growth model. Answer: See Chapter 7

Mini Case Show

n. What is market multiple analysis? Answer: See Chapter 7 Mini Case Show