Basic Econometrics, Gujarati and Porter

48

CHAPTER 6:

EXTENSIONS OF THE TWO-VARIABLE LINEAR REGRESSION

MODEL

6.1 True. Note that the usual OLS formula to estimate the intercept is

6.2

(

a

) & (

b

) In the first equation an intercept term is included.

(

c

) For each model, a one percentage point increase in the monthly

(

d

) As discussed in the chapter, this model represents the

(

f

) Since we have a reasonably large sample, we could use the

(

g

) As per Theil’s remark discussed in the chapter, if the intercept

6.3

(

a

) Since the model is linear in the parameters, it is a linear

Basic Econometrics, Gujarati and Porter

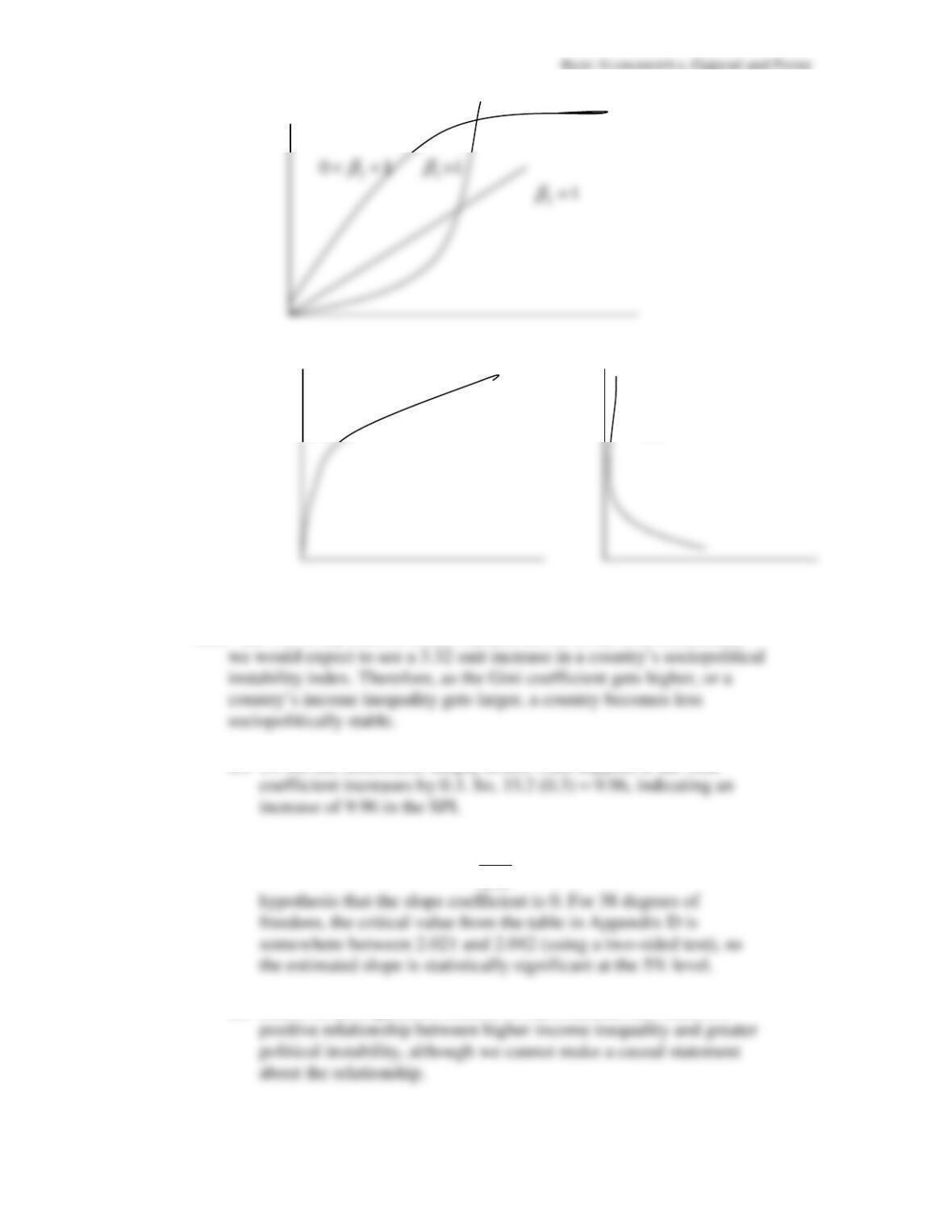

6.4

slope = 1 Slope >1

6.5

For Model I we know that

For Model II, following similar step, we obtain:

6.6

We can write the first model as:

ln (w

1

Y

i

) =

*

1 2 2

ln( )

i i

w X u

α α

+ +

, that is,

50

6.7

Equation (6.6.8) is a growth model, whereas (6.6.10) is a linear

trend model. The former gives the relative change in the

6.8

The null hypothesis is that the true slope coefficient is 0.005.The

alternative hypothesis could be one or two-sided. Suppose we

use the two-sided alternative. The estimated slope value is 0.00705.

Using the

t

test, we obtain:

6.10

As discussed in Sec. 6.7 of the text, for most commodities the

6.11

As it stands, the model is not linear in the parameter. But consider

the following “trick.” First take the ratio of Y to (1-Y) and then take

51

6.12

(

a

)

(b)

2

β

>0

2

β

<0

6.13

(a) For every tenth of a unit increase (0.10) in the Gini coefficient,

(b)

To see this difference, simply assess what happens if the Gini

(c)

Using the standard

t

test,

t

=

33

.

2

1

1

.

8

=

2

.

8136 for testing the null

(d)

Based on the regression results, we can conclude that there is a

Basic Econometrics, Gujarati and Porter

Empirical Exercises

6.14

100

100

Y

=

−

2.0675 + 16.2662

1

X

6.15

(

a

)

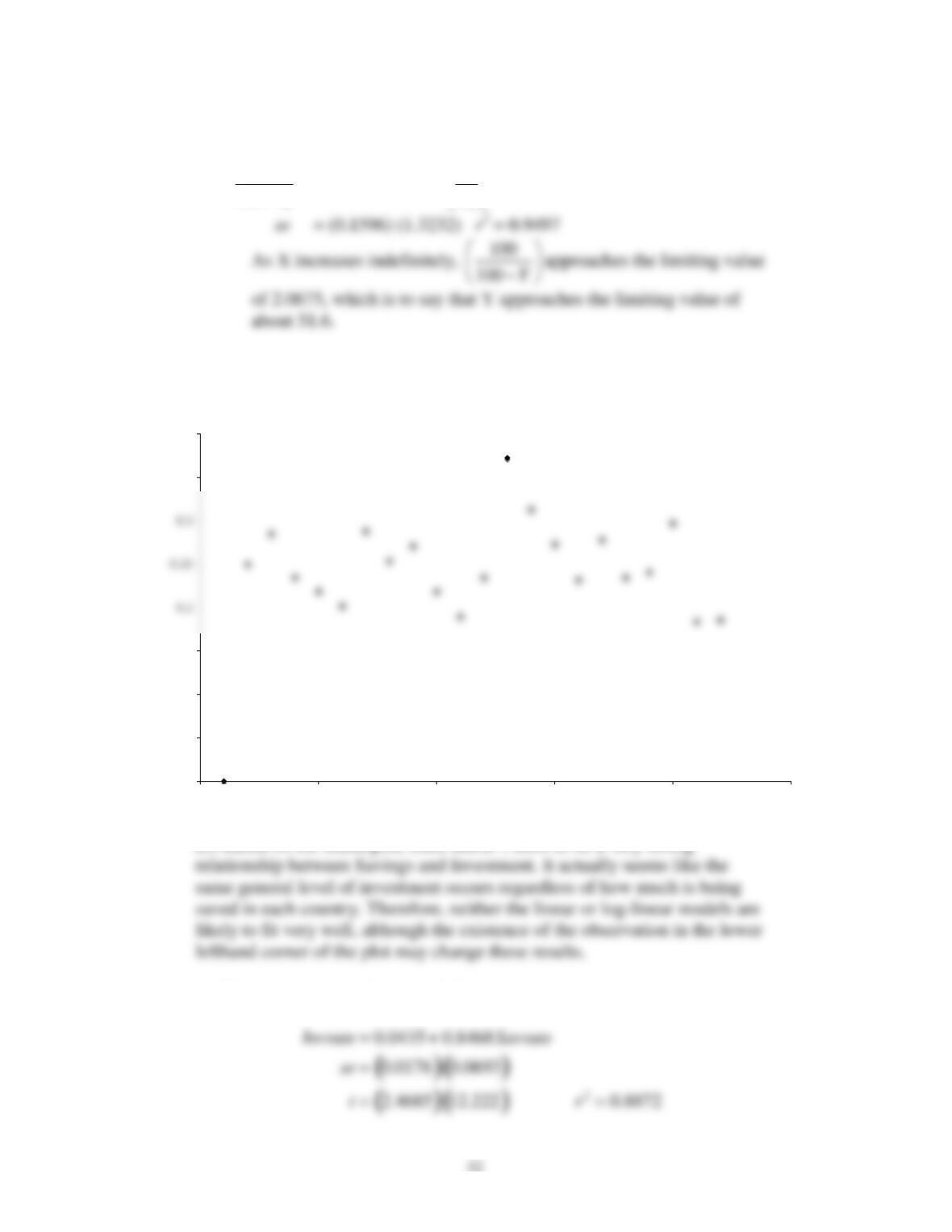

(

b

) Based on the scatterplot, there doesn’t seem to be a very strong

(

c

) The regression results are as follows:

Investment vs Savings

0

0.05

0.1

0.15

0.35

0.4

0 5 10 15 20 25

Savings Rate

Basic Econometrics, Gujarati and Porter

53

(d)

In the linear model, the slope coefficient can be interpreted as: If

the savings rate increases by 0.1 (relative to GDP), the increase in

(e)

The intercept in the linear model suggests that, when the savings

(g)

For the linear model, the elasticity is not apparent. The log-linear

model, however, already contains the results relative to the

elasticities of the variables. To create the elasticity, we need to

calculate the following:

54

6.16

(

a

)

Model Slope

estimate

se t r

2

Linear 0.173 0.0058 29.666 0.3671

(

b

) We cannot compare the

r

2

values directly, but it does seem that

the lin-log model has the best results. This would indicate that food

To obtain the growth rate of expenditure on durable goods, we can fit the log-

lin model, whose results are as follows:

As this regression shows, over the sample period, the (quarterly) rate of growth in

6.18

The corresponding results for the non-durable goods sector are:

ln Expnondur

= 7.6257 + 0.0098

t

55

6.19

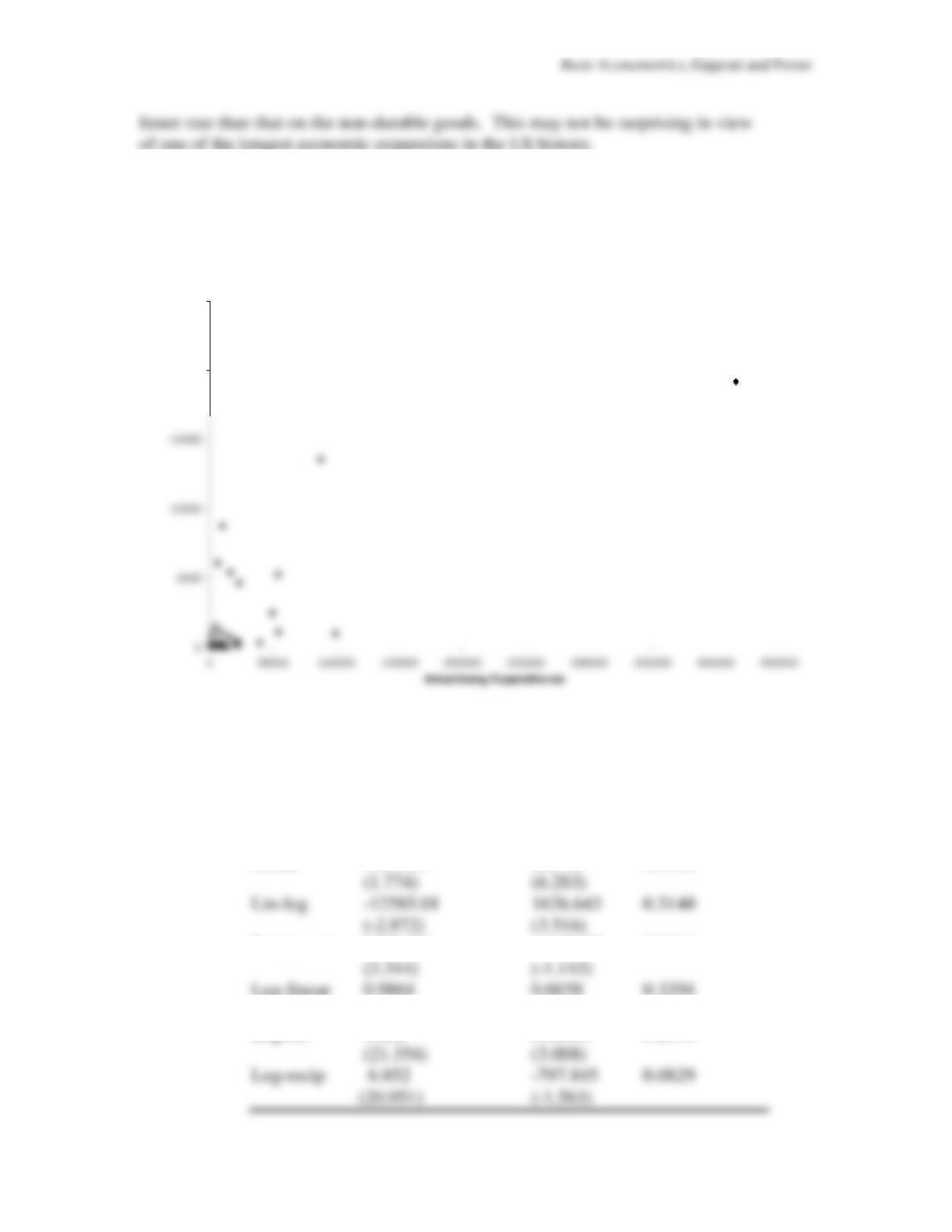

(a) The scattergram of total consumer expenditure and advertising

expenditure is as follows:

(b) Although the relationship between the two variables seems to be

positive, it is not clear which particular curve will fit the data. In the following

table we give regression results based on a few models.

Model Intercept Slope

r

2

_______________________________________________________

Linear 1057.361 0.0446 0.5938

Reciprocal 3077.256 -1642108 0.0461

(0.628) (3.642)

Log-lin 6.262 0.00001 0.2510

Consumer Expenditures vs Advertising Expenditures

20000

25000

Basic Econometrics, Gujarati and Porter

56

Note:

Figures in the parentheses are the estimated

t values.

(c) Assessing the ratio of the variables, it seems there are a few unusually high

6.20

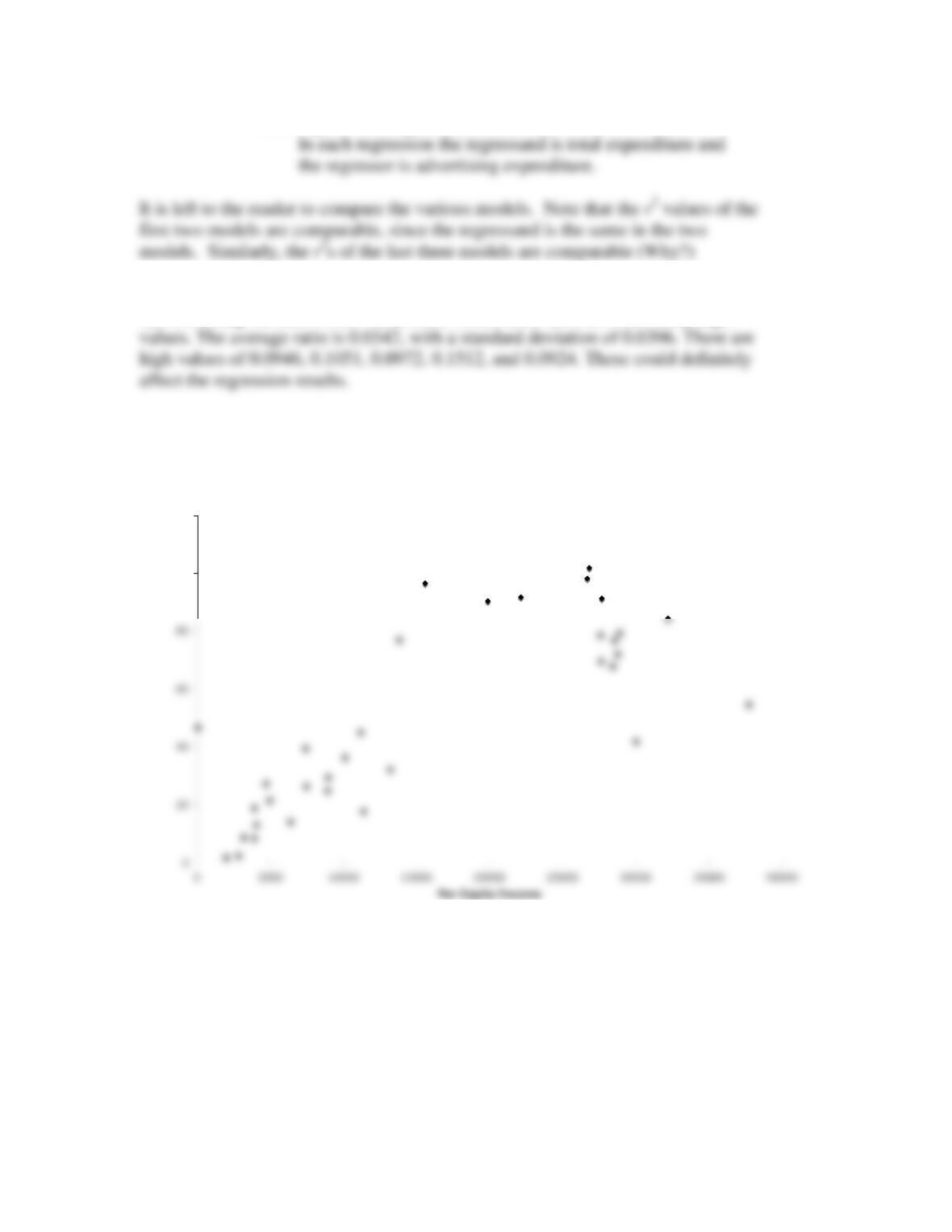

(a)

Cellphone Demand vs Per Capita Income

100

120

Basic Econometrics, Gujarati and Porter

57

(b)

(c) The first graph seems to exhibit non-constant variance, whereas the second

(e)

Double-log regression results are:

Log Cellphone Demand vs Log Income

0

0.5

2

4

5

4 5 6 7 8 9 10 11

Log Per Capita Income

Basic Econometrics, Gujarati and Porter

58

6.21 (a)

PC Demand vs Per Capita Income

60

70

80

Basic Econometrics, Gujarati and Porter

59

(b)

(c) The first graph seems to exhibit non-constant variance, whereas the second

(e) Double-log regression results are:

Log PC Demand vs Log Income

4

5

Basic Econometrics, Gujarati and Porter

60

6.22 (a) Linear regression results are: