Chapter 6: Interest Rates

Comprehensive/Spreadsheet Problem

133

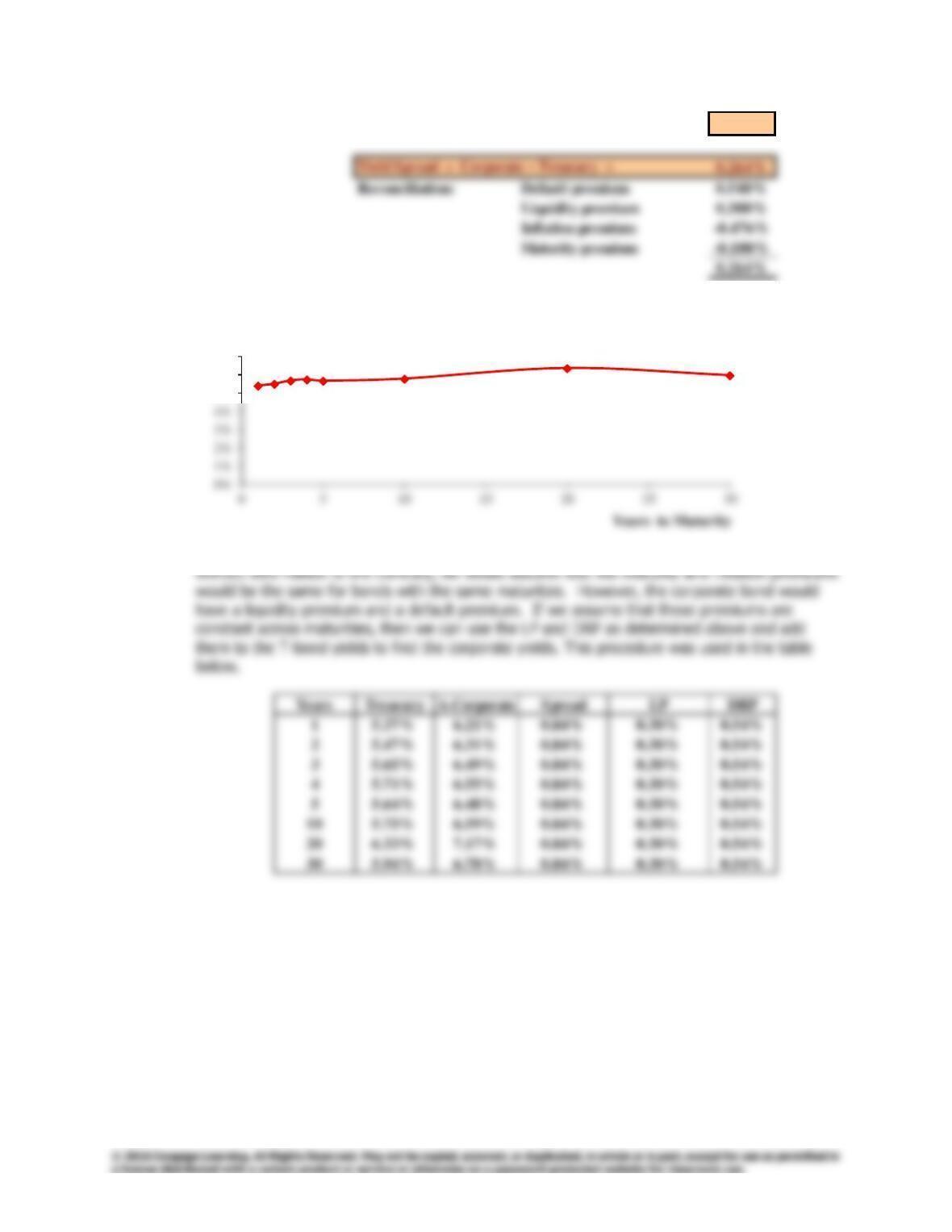

c.

d. The real risk-free rate would be the same for the corporate and treasury bonds. Similarly,

7–year Corporate yield = r* + IP7 + MRP7 + LP + DRP = 7.817%

5%

6%

7%

Interest Rate

Yield Curve

134

Comprehensive/Spreadsheet Problem

Chapter 6: Interest Rates

Now we can graph the data in the first 3 columns of the above table to get the Treasury and A-

rated Corporate yield curves:

8%

Interest Rate

Treasury and A-Rated Corporate Yield Curves

Note that if we constructed yield curves for corporate bonds with other ratings, the higher the

f.

(1) The 1-year rate, 1 year from now

(2) The 5-year rate, 5 years from now

(4) The 10-year rate, 20 years from now

Chapter 6: Interest Rates

Integrated Case

135

Integrated Case

6-21

Morton Handley & Company

Interest Rate Determination

Maria Juarez is a professional tennis player, and your firm manages her

money. She has asked you to give her information about what determines

the level of various interest rates. Your boss has prepared some questions

for you to consider.

A. What are the four most fundamental factors that affect the cost of

money, or the general level of interest rates, in the economy?

Answer: [Show S6-1 and S6-2 here.] The four most fundamental factors

affecting the cost of money are (1) production opportunities, (2)

136

Integrated Case

Chapter 6: Interest Rates

B. What is the real risk-free rate of interest (r*) and the nominal risk-

free rate (rRF)? How are these two rates measured?

Answer: [Show S6-3 and S6-4 here.] Keep these equations in mind as we

discuss interest rates. We will define the terms as we go along:

Chapter 6: Interest Rates

Integrated Case

137

C. Define the terms

inflation premium (IP), default risk premium

(DRP), liquidity premium (LP), and maturity risk premium (MRP)

.

Which of these premiums is included in determining the interest

rate on (1) short-term U.S. Treasury securities, (2) long-term U.S.

Treasury securities, (3) short-term corporate securities, and (4)

long-term corporate securities? Explain how the premiums would

vary over time and among the different securities listed.

Answer: [Show S6-5 here.] The inflation premium (IP) is a premium added

to the real risk-free rate of interest to compensate for expected

inflation.

138

Integrated Case

Chapter 6: Interest Rates

3. The rate on short-term corporate securities is equal to the real

4. The rate for long-term corporate securities also includes a

D. What is the term structure of interest rates? What is a yield

curve?

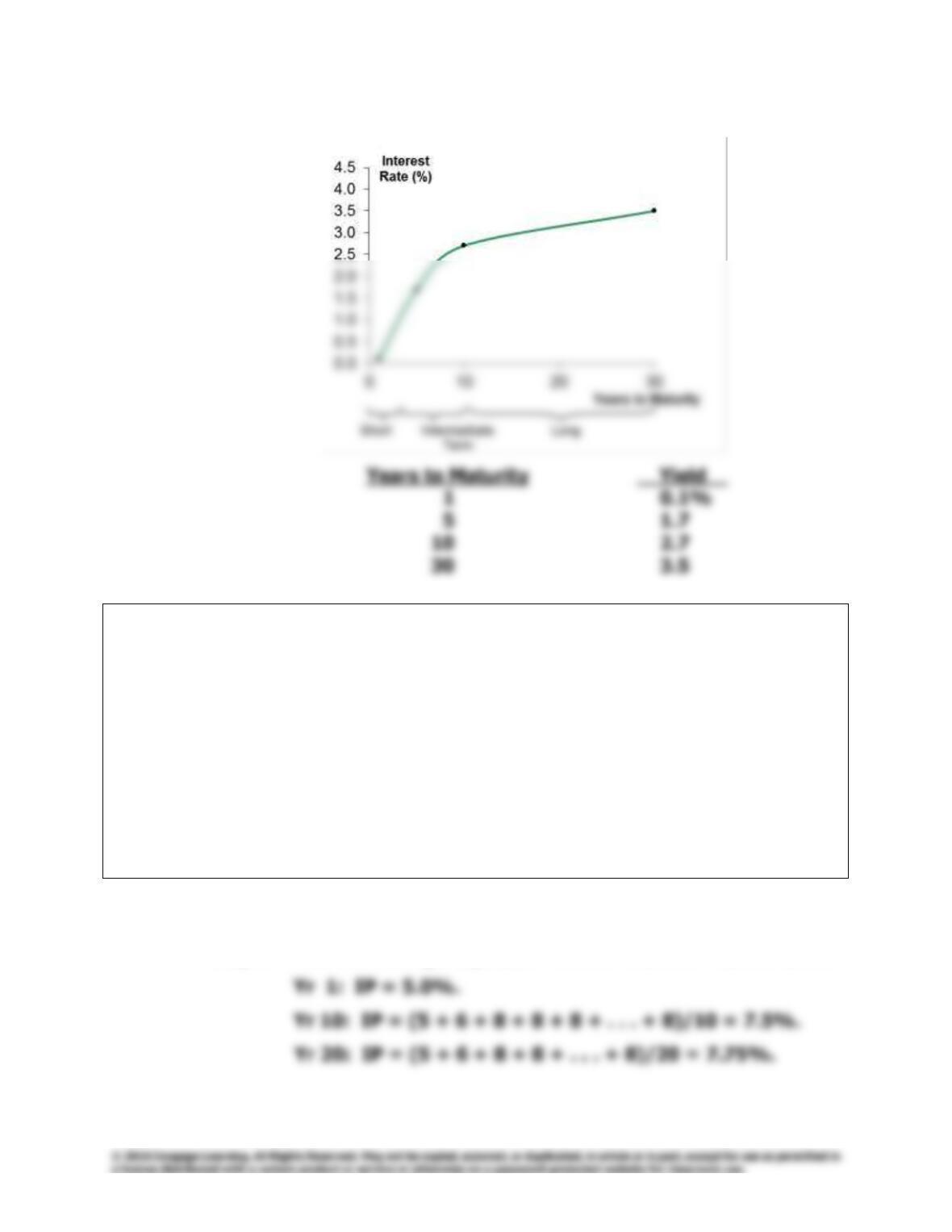

Answer: [Show S6-6 here. S6-6 shows a recent (April 2014) Treasury yield

Chapter 6: Interest Rates

Integrated Case

139

Yield Curve for April 2014

E. Suppose most investors expect the inflation rate to be 5% next

year, 6% the following year, and 8% thereafter. The real risk-free

rate is 3%. The maturity risk premium is zero for bonds that

mature in 1 year or less and 0.1% for 2-year bonds; then the MRP

increases by 0.1% per year thereafter for 20 years, after which it

is stable. What is the interest rate on 1-, 10-, and 20-year

Treasury bonds? Draw a yield curve with these data. What factors

can explain why this constructed yield curve is upward-sloping?

Answer: [Show S6-7 through S6-12 here.]

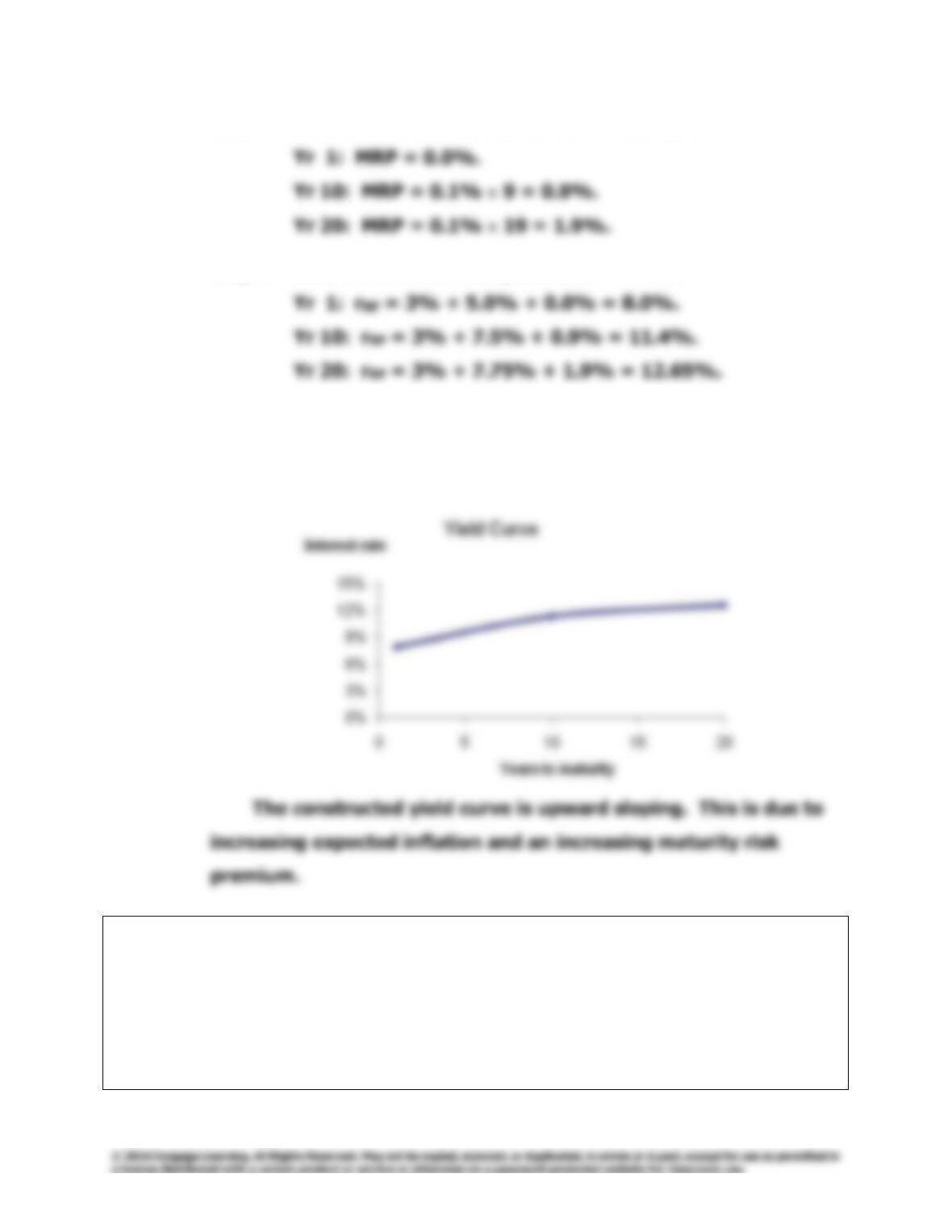

Step 1: Find the average expected inflation rate over Years 1 to 20:

140

Integrated Case

Chapter 6: Interest Rates

Step 2: Find the maturity risk premium in each year:

Step 3: Sum the IPs and MRPs, and add r* = 3%:

The shape of the yield curve depends primarily on two factors: (1)

expectations about future inflation and (2) the relative riskiness of

securities with different maturities.

F. At any given time, how would the yield curve facing a AAA-rated

company compare with the yield curve for U.S. Treasury

securities? At any given time, how would the yield curve facing a

BB-rated company compare with the yield curve for U.S. Treasury

securities? Draw a graph to illustrate your answer.

Chapter 6: Interest Rates

Integrated Case

141

Answer: [Show S6-13 and S6-14 here.] (Curves for AAA-rated and BB–

rated securities have been added to an illustrative yield curve to

Illustrative Corporate and Treasury Yield Curves

142

Integrated Case

Chapter 6: Interest Rates

G. What is the pure expectations theory? What does the pure

expectations theory imply about the term structure of interest

rates?

Answer: [Show S6-15 and S6-16 here.] The pure expectations theory

assumes that investors establish bond prices and interest rates

H. Suppose you observe the following term structure for Treasury

securities:

Maturity Yield

1 year 6.0%

2 years 6.2

3 years 6.4

4 years 6.5

5 years 6.5

Assume that the pure expectations theory of the term structure is

correct. (This implies that you can use the yield curve provided to

“back out” the market’s expectations about future interest rates.)

What does the market expect will be the interest rate on 1-year

securities 1 year from now? What does the market expect will be

the interest rate on 3-year securities 2 years from now? Calculate

these yields using geometric averages.

Chapter 6: Interest Rates

Integrated Case

143

Answer: [Show S6-17 through S6-20 here.] Calculation for r on 1-year

securities one year from now:

I. Describe how macroeconomic factors affect the level of interest

rates. How do these factors explain why interest rates have been

lower in recent years?

Answer: [Show S6-21 here.] Expected inflation, default risk, maturity risk,

144

Integrated Case

Chapter 6: Interest Rates