1

2

3

4

5

6

10

11

12

13

14

15

20

16

21

22

23

24

25

26

27

31

28

34

A B C D E F G H I J K L M N O P Q R

06 Chapter Model 12/12/2018

THE DETERMINANTS OF INTEREST RATES (Section 6-3)

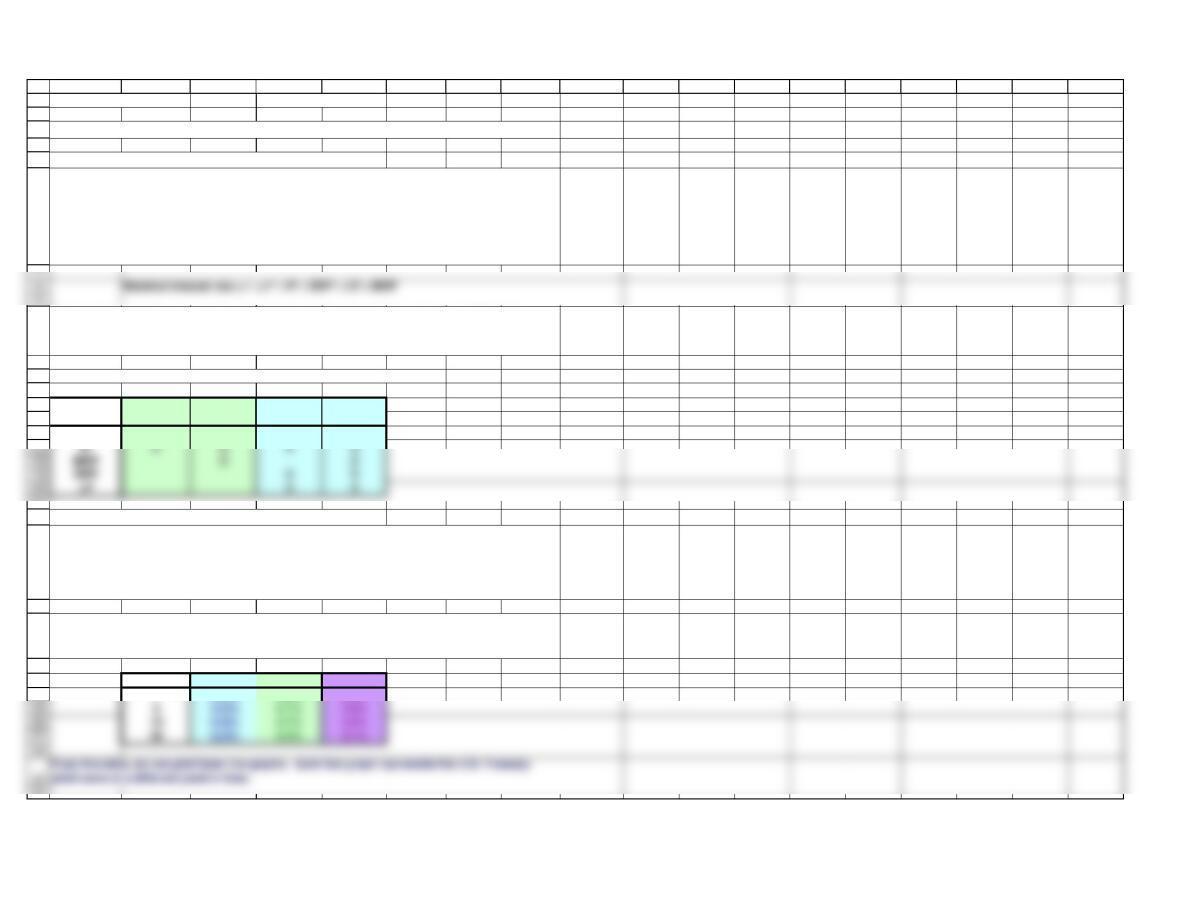

WHICH TYPES OF SECURITIES ARE EXPOSED TO WHAT KIND OF RISK?

Interest Rate Short-Term Long-Term Short-Term Long-Term

Parameter Treasuries Treasuries Corporates Corporates

r* X X X X

THE TERM STRUCTURE OF INTEREST RATES (Section 6-4)

Maturity (yrs) Mar-80 Feb-00 May-18

114.0% 6.2% 2.3%

Interest rates can easily be observed. All it requires is reading the newspaper, watching

television, or surfing the internet. However, it is not so easy to see the factors that determine

market interest rates, and the extent to which they shape interest rates. Naturally, the

determination of interest rates is a macroeconomic question that has numerous contributing

factors. However, in an effort to simplify the composition of interest rates, we will look at

nominal interest rates being composed of five driving forces, as outlined here:

Here r* represents the real risk-free rate of interest, IP is the inflation premium, DRP is the

default risk premium, LP is the liquidity premium, and MRP is the maturity risk premium.

Together, these five factors determine the nominal interest rate, denoted by r.

The term structure describes the relationship between long-term and short-term interest rates.

Graphically, this relationship can be shown in what is known as the yield curve. In practice, the

yield curve is relatively easy to obtain. It is published daily in a variety of online and print news

sources. However, the “building block approach” to generating a yield curve is more

complicated. We will see that later when we build our own yield curve.

Before jumping into the creation of our own yield curve, let’s look at some historical interest

rate data and draw some historical yield curves. Here is some interest rate data from March

1980, February 2000, and May 2018.

Chapter 6. Interest Rates

35

36

37

38

39

40

41

42

43

44

55

56

57

58

59

60

61

64

65

66

A B C D E F G H I J K L M N O P Q R

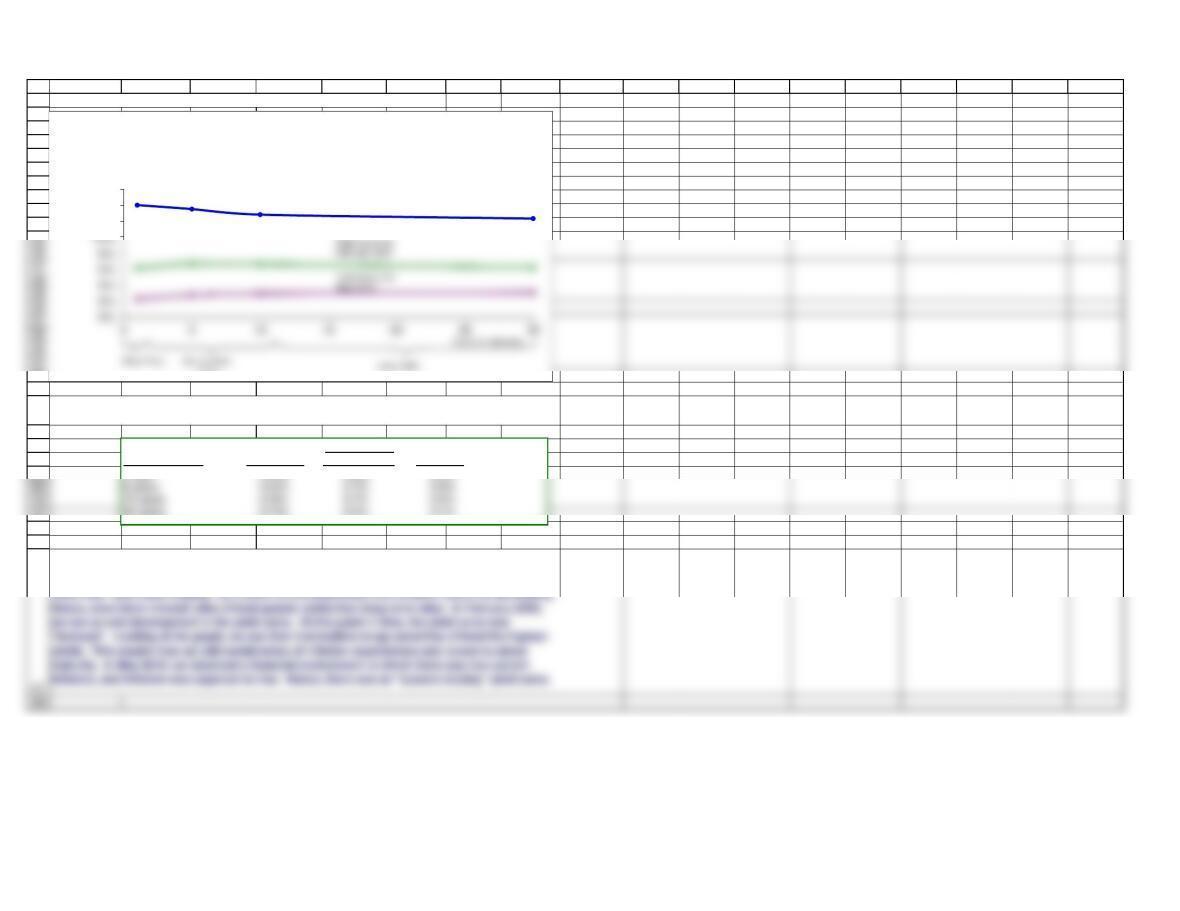

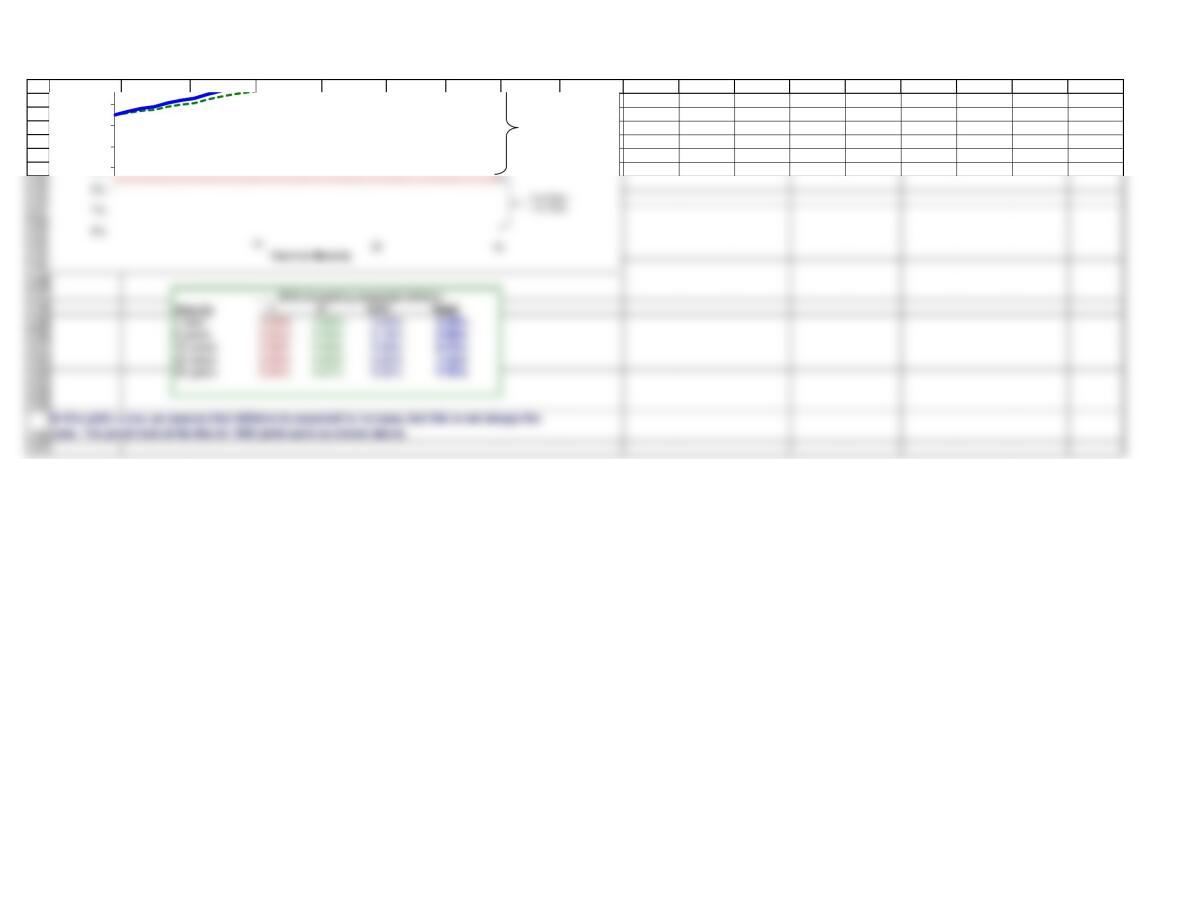

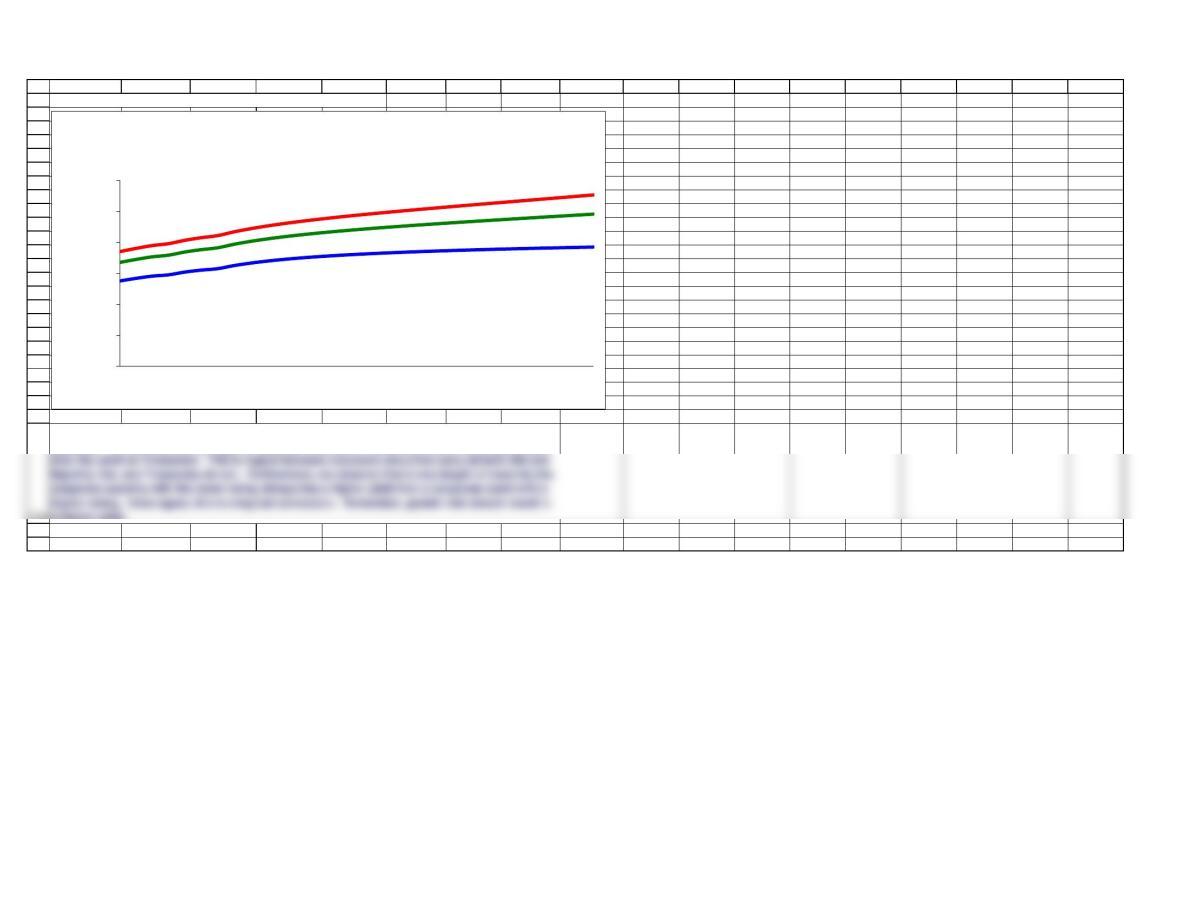

Figure 6.4 U.S. Treasury Bond Interest Rates on Different Dates

Then, we reproduce the data from the graph in this table, to make it look like it might have

appeared in the newspaper.

Looking at these three historical yield curves, we see that they paint very different landscapes of

the financial environment at those times. In the March 1980 yield curve, we see that the yield

12%

14%

16%

Interest Rate

(%)

Term

Yield Curve for

March 1980

Interest Rates

Term to Maturity March 1980 February 2000 May 2018

1 year 14.0% 6.2% 2.3%

30 years 12.3% 6.3% 3.1%

69

70

71

72

76

77

78

79

80

81

82

83

87

88

A B C D E F G H I J K L M N O P Q R

WHAT DETERMINES THE SHAPE OF THE YIELD CURVE? (Section 6-5)

Our Hypothetical Yield Curve

Setting up the yield curve

INPUT DATA

Real risk-free rate 2.50%

Expected inflation of 3% for the next 3years.

Now, we want to put all of these elements together. The second column shows the expected

real risk-free rate of interest (constant at 2.5%). The third column shows the inflation premium

(determined by the stated inflation expectations). The fourth column shows the maturity risk

premium (determined from the formula outlined above).

Now that we have experimented with historical interest rate data, we will move on and create our

own yield curve. This yield curve will be based upon whatever assumptions we feel like setting.

First, we will assume that the real risk-free rate of interest is 2.5%. Furthermore, we expect

inflation to be 3% for the next three years, 4% for the next four years, and 5% thereafter. That

89

90

91

100

101

102

103

104

105

117

118

122

123

124

125

126

127

A B C D E F G H I J K L M N O P Q R

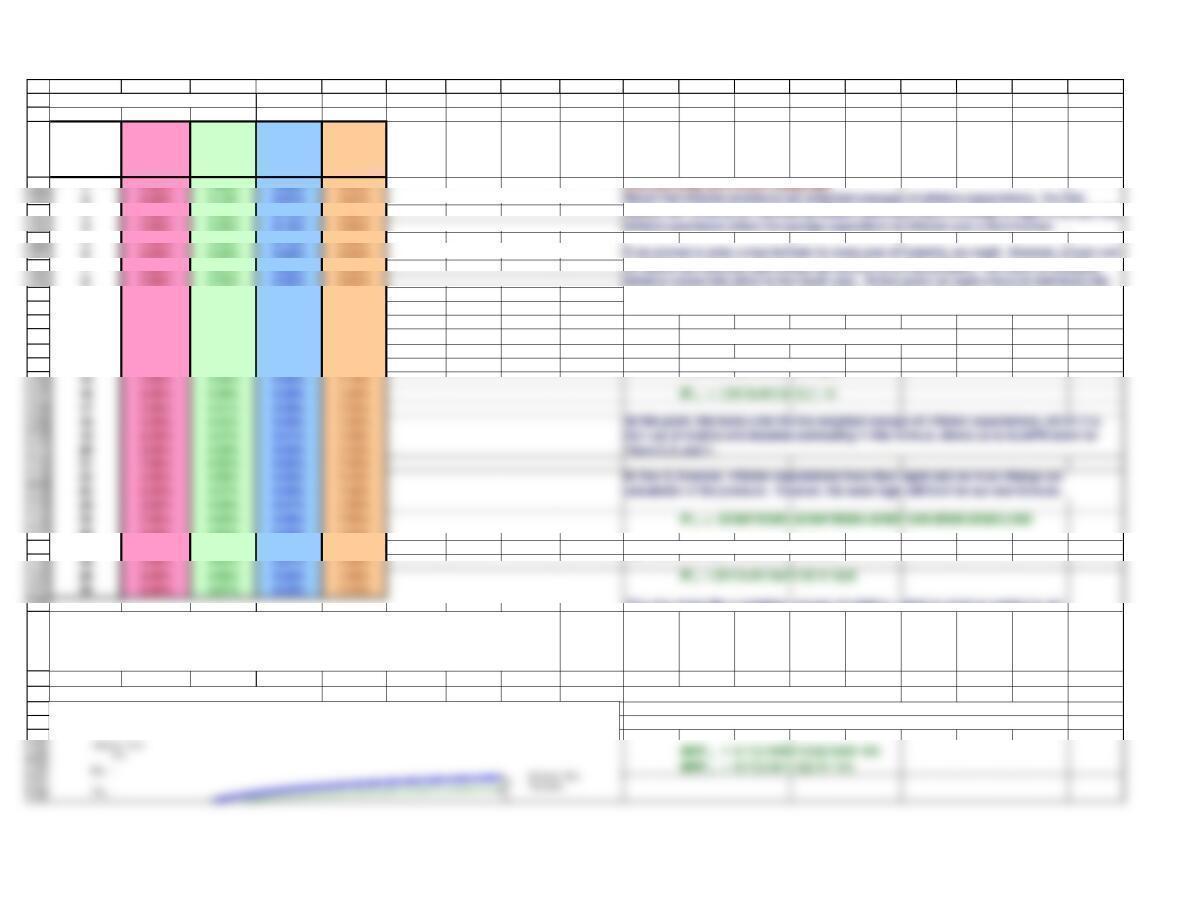

YIELD CURVE INFORMATION

Years to

Maturity

Real Risk-

Free Rate

(r*)

Inflation

Premium

(IP)

Maturity

Risk

Premium

(MRP)

Treasury

Yield

92.50% 3.89% 0.27% 6.66%

10 2.50% 4.00% 0.28% 6.78%

11 2.50% 4.09% 0.30% 6.89%

12 2.50% 4.17% 0.32% 6.98%

IP 4 = ($C$83*$E$83+$C$84*(A95-$E$83))/A95

13 2.50% 4.23% 0.33% 7.06%

14 2.50% 4.29% 0.35% 7.13% Substituting numbers, we get:

26 2.50% 4.62% 0.49% 7.61%

27 2.50% 4.63% 0.50% 7.63% Again substituting numbers, we find that:

This, too, looks like a weighted average of inflation, which is what we wanted to get.

Figure 6.5(a) Illustratvie Treasury Yield Curve CALCULATING MATURITY RISK PREMIUMS

This simply uses the formula previously stated and requires all relative addressing,

so that the formula can be input into the 1-year maturity bond, and AutoFill down.

account previous inflation expectations along with new expectations. Hence, the formula for

the fourth year’s inflation premium would be:

The table above gives us all of the components for our Treasury yield curve. Recall, we have

said that Treasury securities are subject to two kinds of risk premiums, the inflation premium

and the maturity risk premium. Just as we “built” Treasury yields in the table, we can “build” a

yield curve based upon these expectations.

When Inflation Is Expected To Increase

133

134

135

136

137

138

A B C D E F G H I J K L M N O P Q R

3%

4%

5%

6%

7%

Inflation

Premium

158

159

160

161

162

163

164

165

166

167

168

199

169

170

171

178

179

180

181

190

191

192

193

194

195

200

A B C D E F G H I J K L M N O P Q R

What If Inflation Is Expected To Decrease?

Real risk free rate 2.5%

Expected inflation of 5.0% for the next 3years.

Expected inflation of 4.0% for the next 4years.

Expected inflation of 3.0% thereafter.

Years to

Maturity

Real Risk-

Free Rate

(r*)

Inflation

Premium

(IP)

Maturity

Risk

Premium

(MRP)

Treasury

Yield

12.50% 5.00% 0.00% 7.50%

22.50% 4.95% 0.07% 7.52%

92.50% 4.11% 0.27% 6.88%

10 2.50% 4.00% 0.28% 6.78%

11 2.50% 3.91% 0.30% 6.71%

12 2.50% 3.83% 0.32% 6.65%

21 2.50% 3.48% 0.44% 6.41%

22 2.50% 3.45% 0.45% 6.40%

23 2.50% 3.43% 0.46% 6.39%

24 2.50% 3.42% 0.47% 6.39%

25 2.50% 3.40% 0.48% 6.38%

26 2.50% 3.38% 0.49% 6.37%

Our methodology for creating this yield curve‘s data will be exactly the same as above. In fact,

we will use all of the same formulas.

Now, we will construct a similar yield curve, except we will change inflation expectations.

Instead of increasing inflation, we will have decreasing inflation. We will assume that: inflation

is expected to be 5% for the next 3 years, 4% for the following 4 years, and 3% thereafter. All of

our other previous assumptions will be upheld.

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

230

231

233

234

235

236

238

A B C D E F G H I J K L M N O P Q R

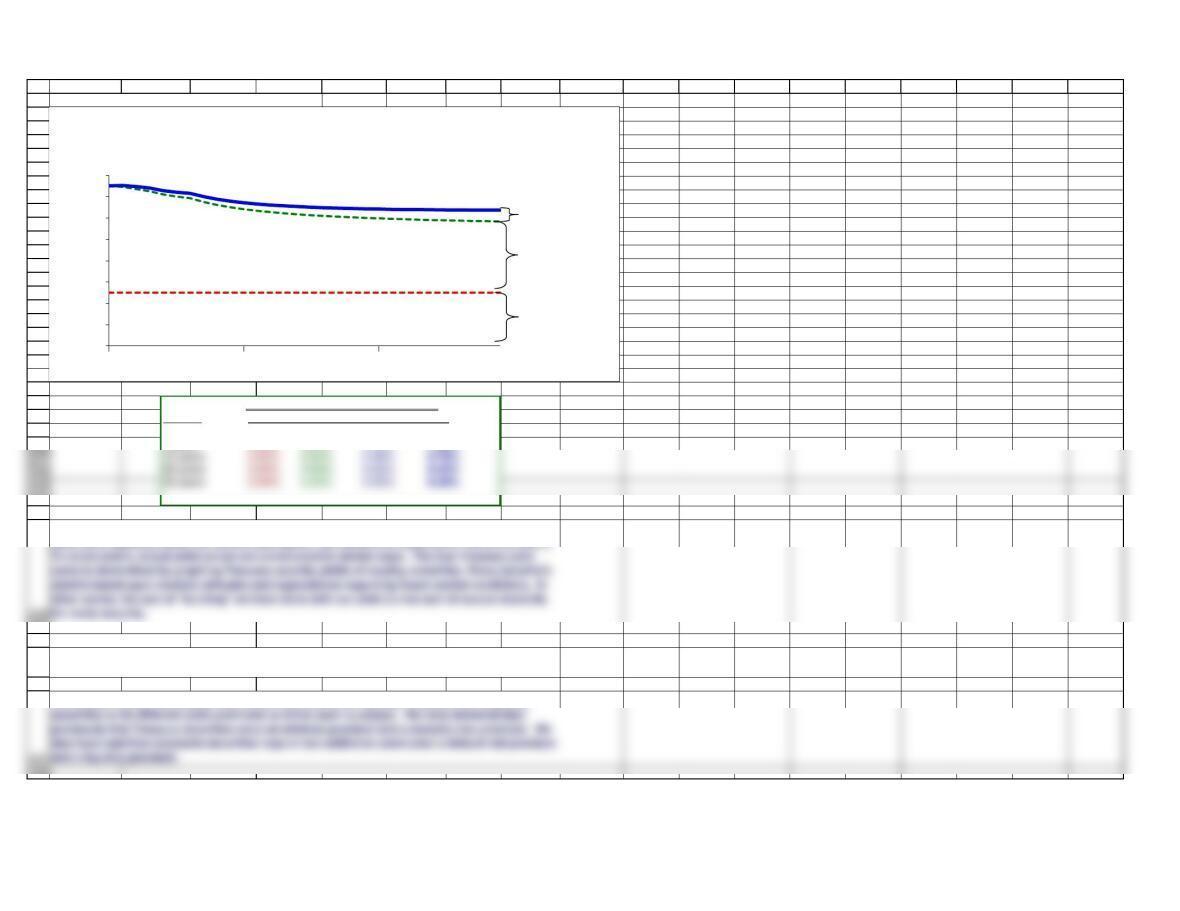

Figure 6.5(b) Illustratvie Treasury Yield Curve

CORPORATE BONDS

To this point, we have constructed two yield curves based upon hypothetical data. The first

yield curve operates under the simple assumption that inflation is expected to rise in the future.

The answer is yes. Remember, that the primary difference between Treasury and corporate

So far, we have addressed the yield curve construction for Treasury securities, but can

corporate bonds also be demonstrated in yield curve fashion?

0%

1%

2%

3%

4%

5%

6%

7%

8%

Interest Rate

(%)

Years to Maturity

When Inflation Is Expected To Decrease

Real Risk-

Free Rate

Inflation

Premium

Maturity Risk

Premium

20

30

10

With decreasing expected inflation

Maturity r* IP MRP Yield

1 year 2.50% 5.00% 0.00% 7.50%

5 years 2.50% 4.60% 0.18% 7.28%

239

240

241

242

243

244

245

246

261

247

249

250

251

252

253

254

255

256

A B C D E F G H I J K L M N O P Q R

Corporate Bond Yield Spread: DRP + LP

Bond

Rating

Corporate

Spread:

DRP + LP

AAA 1.05%

AA 1.20%

A 1.55%

BBB 1.90%

DRPt + LPt = Corporate spread * (1.02)(t−1)

Real risk-free rate 2.50%

Expected inflation of 3% for the next 3years.

This tells us the average spreads of corporate securities with various bond ratings. We will use

this data as the starting point for our corporate yield curves. Naturally, the first question that

The construction of corporate yields is a process of beginning with the appropriate Treasury

With all of that having been said, we can step forward and try to construct corporate yield

curves.

262

271

272

273

274

275

281

282

283

284

285

293

A B C D E F G H I J K L M N O P Q R

Years to

Maturity

Real Risk-

Free Rate

(r*)

Inflation

Premium

(IP)

Maturity

Risk

Premium

(MRP)

Treasury

Yield

AA-Rated

DRP + LP

AA-Rated

Bond

Yield

BBB-

Rated

DRP + LP

BBB-Rated

Bond Yield

92.50% 3.89% 0.27% 6.66% 1.41% 8.06% 2.23% 8.88%

10 2.50% 4.00% 0.28% 6.78% 1.43% 8.22% 2.27% 9.06%

11 2.50% 4.09% 0.30% 6.89% 1.46% 8.36% 2.32% 9.21%

12 2.50% 4.17% 0.32% 6.98% 1.49% 8.48% 2.36% 9.35%

13 2.50% 4.23% 0.33% 7.06% 1.52% 8.59% 2.41% 9.47%

19 2.50% 4.47% 0.41% 7.39% 1.71% 9.10% 2.71% 10.10%

20 2.50% 4.50% 0.42% 7.42% 1.75% 9.17% 2.77% 10.19%

21 2.50% 4.52% 0.44% 7.46% 1.78% 9.24% 2.82% 10.28%

22 2.50% 4.55% 0.45% 7.49% 1.82% 9.31% 2.88% 10.37%

23 2.50% 4.57% 0.46% 7.52% 1.86% 9.38% 2.94% 10.46%

294

295

296

297

298

299

300

301

302

303

304

305

306

307

308

309

310

311

312

313

314

315

316

317

318

319

320

A B C D E F G H I J K L M N O P Q R

Figure 6.6 Illustrative Corporate and Treasury Yield Curves

Looking at the yield curve we have constructed, we see a relationship that we should have

expected. We see that at any length of maturity, the yield on corporate bonds is always greater

a higher yield.

0%

2%

4%

6%

8%

10%

12%

Interest Rate

(%)

Years to Maturity

10

AA-Rated Bond

Treasury Bond

BBB-Rated Bond

20

30

321

323

324

325

327

328

329

330

331

4r1

5r5

332

333

334

340

341

342

343

A B C D E F G H I J K L M N O P Q R

USING THE YIELD CURVE TO ESTIMATE FUTURE INTEREST RATES (Section 6-6)

PROBLEM

Symbol:

Yield on 1-year bond 1 year from now =

1r1

Yield on 1-year bond 2 years from now =

2r1

Yield on 1-year bond 3 years from now =

3r1

Maturity Maturity Yield

1 year 1 5.02%

2 years 2 5.31%

Expected forward rates, in words:

Assuming that expectations theory holds, use the yield information below to back out the

following forward rates from the yield curve.

The shape of the yield curve depends primarily on two key factors: (1) expectations about future

inflation and (2) perceptions about the relative riskiness of securities of different maturities. The

first factor is the basis for the Pure Expectations Theory. If the relationship between

For instance, if the yield on a 1-year bond is 5% and that on a 2-year bond is 5.5%, the rate on a

1-year bond one year from now should be 6%, because (1.055)2 = (1.05)(1.06).

(1+ r5)5 = (1+ r4)4x (1 + 4r1)

4r1= 6.05%

(1+ r20)20 = (1+ r10)10 x (1 + 10r10)10

(1+ r30)30 = (1+ r20)20 x (1 + 20r10)10

351

352

353

354

358

359

360

361

366

367

368

369

378

A B C D E F G H I J K L M N O P Q R

(1+ r2)2 = (1 + r1) x (1 + 1r1)

1.1090 = 1.0502 x

(1 + 1r1)

1r1= 5.60%

(1+ r4)4 = (1+ r3)3x (1 + 3r1)

1.2459 = 1.1736 x

(1 + 3r1)

3r1= 6.16%

(1+ r10)10 = (1+ r5)5x (1 + 5r5)5

1.7375 = 1.3213 x

(1 + 5r5)5

5r5= 5.63%

The data used to construct the yield curve are readily available, and forward rates can be

calculated as shown above. Bond traders and corporate borrowers can use this information for

hedging in the futures market. For example, if a company plans to build a new plant two years

(1+ r3)3 = (1+ r2)2x (1 + 2r1)

2r1= 5.82%

1

2

3

4

5

6

A B C D E F G H

SECTION 6-2 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Inflation 2.0%

5a. If inflation during the last 12 months was 2% and the interest rate during that period was 5%,

what was the real rate of interest?

Inflation 4.0%

1

2

3

4

5

6

A B C D E F G H

SECTION 6-3 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

r* 2.0%

7a. Assume that the real risk-free rate is r* = 2% and the average expected inflation rate is 3%

for each future year. The DRP and LP for Bond X are each 1%, and the applicable MRP is 2%.

What is Bond X’s interest rate?

1

2

3

11

12

13

A B C D E F G H

SECTION 6-6 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

5a. Assume the interest rate on a 1-year T-bond is currently 7% and the rate on a 2-year bond

5b. What would the forecast be if the maturity risk premium on the 2-year bond was 0.5%

versus zero for the 1-year bond?