Answers and Solutions: 6 – 1

Chapter 6

Risk and Return

ANSWERS TO END-OF-CHAPTER QUESTIONS

6-1 a. Stand-alone risk is only a part of total risk and pertains to the risk an investor takes by

holding only one asset. Risk is the chance that some unfavorable event will occur.

For instance, the risk of an asset is essentially the chance that the asset’s cash flows

will be unfavorable or less than expected. A probability distribution is a listing, chart

or graph of all possible outcomes, such as expected rates of return, with a probability

assigned to each outcome. When in graph form, the tighter the probability

distribution, the less uncertain the outcome.

d. The standard deviation (σ) is a statistical measure of the variability of a set of

observations. The variance (σ2) of the probability distribution is the sum of the

squared deviations about the expected value adjusted for deviation.

e. A risk averse investor dislikes risk and requires a higher rate of return as an

inducement to buy riskier securities. A realized return is the actual return an investor

receives on their investment. It can be quite different than their expected return.

Answers and Solutions: 6 – 2

coefficient (ρ) of +1.0 means that the two variables move up and down in perfect

synchronization, while a coefficient of -1.0 means the variables always move in

opposite directions. A correlation coefficient of zero suggests that the two variables

are not related to one another; that is, they are independent.

k. The beta coefficient is a measure of a stock’s market risk, A stock with a beta greater

than 1 has stock returns that tend to be higher than the market when the market is up

but tend to be below the market when the market is down. The opposite is true for a

stock with a beta less than 1..

n. Equilibrium is the condition under which the expected return on a security is just

equal to its required return,

r

= r, and the market price is equal to the intrinsic value.

The Efficient Markets Hypothesis (EMH) states (1) that stocks are always in

equilibrium and (2) that it is impossible for an investor to consistently “beat the

market.” In essence, the theory holds that the price of a stock will adjust almost

o. The Fama-French 3-factor model has one factor for the excess market return (the

market return minus the risk free rate), a second factor for size (defined as the return

on a portfolio of small firms minus the return on a portfolio of big firms), and a third

factor for the book–to-market effect (defined as the return on a portfolio of firms with

a high book-to-market ratio minus the return on a portfolio of firms with a low book–

to-market ratio).

p. Most people don’t behave rationally in all aspects of their personal lives, and

behavioral finance assumes that investors have the same types of psychological

6-2 a. The probability distribution for complete certainty is a vertical line.

b. The probability distribution for total uncertainty is the X axis from – to +.

6-3 Security A is less risky if held in a diversified portfolio because of its lower beta and

6-4 The risk premium on a high beta stock would increase more.

RPj = Risk Premium for Stock j = (rM – rRF)bj.

6-5 According to the Security Market Line (SML) equation, an increase in beta will increase

a company’s expected return by an amount equal to the market risk premium times the

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

6-1 Investment Beta

$20,000 0.7

6-2 rRF = 4%; rM = 12%; b = 0.8; rs = ?

6-3 rRF = 5%; RPM = 7%; rM = ?

rM = 5% + (7%)1 = 12% = rs when b = 1.0.

rs when b = 1.7 = ?

6-5

r

= (0.1)(-50%) + (0.2)(-5%) + (0.4)(16%) + (0.2)(25%) + (0.1)(60%)

= 11.40%.

σ2 = (-50% – 11.40%)2(0.1) + (-5% – 11.40%)2(0.2) + (16% – 11.40%)2(0.4)

Answers and Solutions: 6 – 6

6-6 a.

r

m= (0.3)(15%) + (0.4)(9%) + (0.3)(18%) = 13.5%.

6-7 a. rA = rRF + (rM – rRF)bA

12% = 5% + (10% – 5%)bA

12% = 5% + 5%(bA)

7% = 5%(bA)

6-8 a. ri = rRF + (rM – rRF)bi = 5% + (12% – 5%)1.4 = 14.8%.

b. 1. rRF increases to 6%:

c. 1. rM increases to 14%:

ri = rRF + (rM – rRF)bi = 5% + (14% – 5%)1.4 = 17.6%.

Answers and Solutions: 6 – 8

6-9 Old portfolio beta =

5,0007$

000,70$

(b) +

5,0007$

000,5$

(0.8)

Alternative Solutions:

1. Old portfolio beta = 1.2 = (0.0667)b1 + (0.0667)b2 +…+ (0.0667)b20

1.2 = (bi)(0.0667)

bi = 1.2/0.0667 = 18.0.

Answers and Solutions: 6 – 9

6-10 Portfolio beta =

$4,000,000

$400,000

(1.50) +

$4,000,000

$600,000

(-0.50)

+

$4,000,000

$1,000,000

(1.25) +

$4,000,000

$2,000,000

(0.75)

Stock Investment Beta r = rRF + (rM – rRF)b Weight

A $ 400,000 1.50 18% 0.10

B 600,000 (0.50) 2 0.15

C 1,000,000 1.25 16 0.25

D 2,000,000 0.75 12 0.50

Total $4,000,000 1.00

rp = 18%(0.10) + 2%(0.15) + 16%(0.25) + 12%(0.50) = 12.1%.

6-12 We know that bR = 1.50, bS = 0.75, rM = 13%, rRF = 7%.

ri = rRF + (rM – rRF)bi = 7% + (13% – 7%)bi.

rR = 7% + 6%(1.50) = 16.0%

rS = 7% + 6%(0.75) = 11.5

4.5%

6-13 The answers to a, b, and c are given below:

Answers and Solutions: 6 – 10

alone, since the portfolio offers the same expected return but with less risk. This

result occurs because returns on A and B are not perfectly positively correlated (ρAB =

-0.13).

6-14 a. bX = 1.3471; bY = 0.6508. These can be calculated with a spreadsheet.

b. rX = 6% + (5%)1.3471 = 12.7355%.

Answers and Solutions: 6 – 12

SOLUTION TO SPREADSHEET PROBLEM

6-14 The detailed solution for the spreadsheet problem is available in the file Ch06-P15 Build

a Model Solution.xls at the textbook’s Web site.

Mini Case: 6 – 13

Assume that you recently graduated with a major in finance, and you just landed a job as a

financial planner with Barney Smith Inc., a large financial services corporation. Your first

assignment is to invest $100,000 for a client. Because the funds are to be invested in a new

business the client plans to start at the end of one year, you have been instructed to plan for

a one-year holding period. Further, your boss has restricted you to the investment

alternatives shown in the table below. (Disregard for now the items at the bottom of the

data; you will fill in the blanks later.)

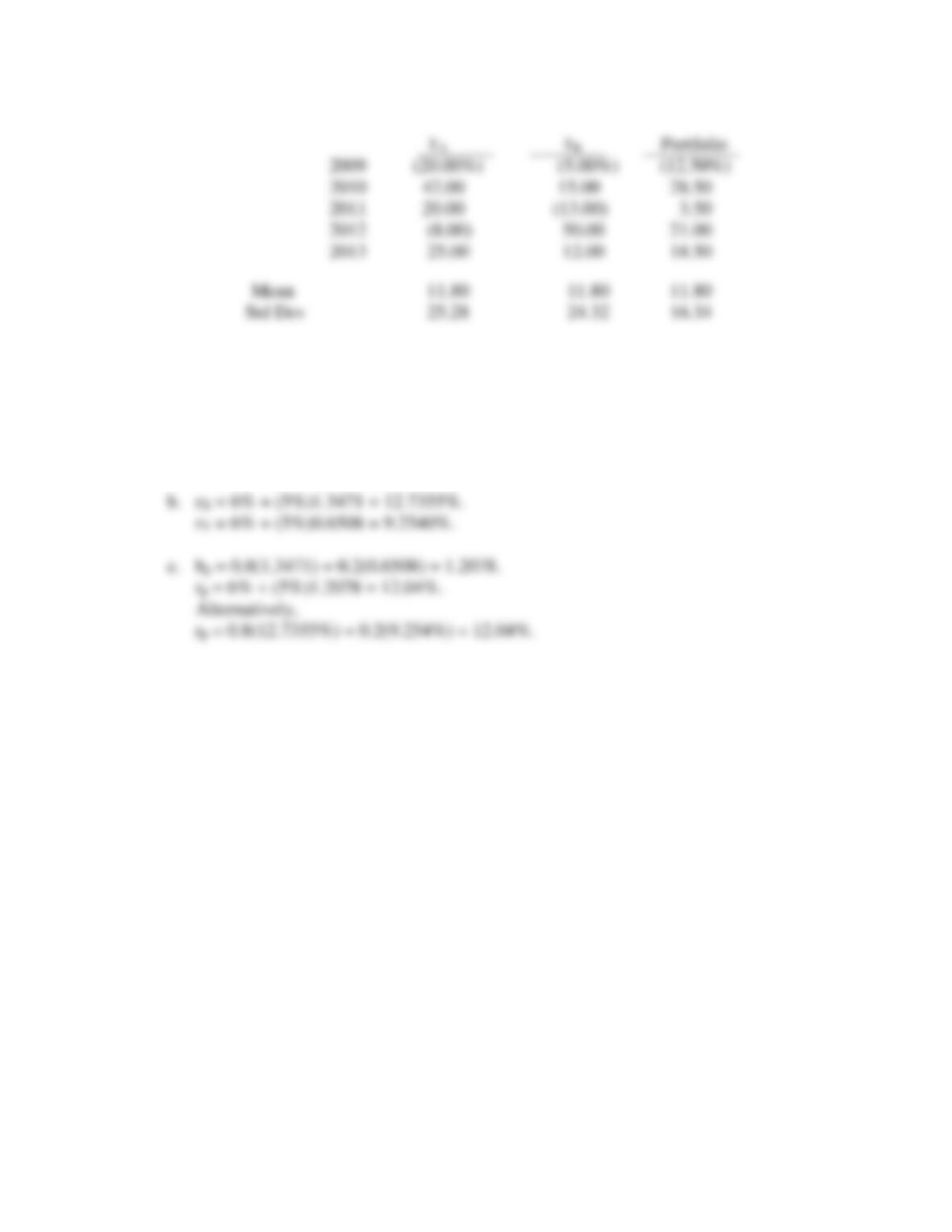

Returns On Alternative Investments

Estimated Rate Of Return

State of the T- Alta Repo Am. Market 2-stock

economy Prob. Bills Inds Men Foam portfolio portfolio

Recession 0.1 8.0% -22.0% 28.0% 10.0%* -13.0% 3.0%

Below avg 0.2 8.0 -2.0 14.7 -10.0 1.0

Average 0.4 8.0 20.0 0.0 7.0 15.0 10.0

Above avg 0.2 8.0 35.0 -10.0 45.0 29.0

Boom 0.1 8.0 50.0 -20.0 30.0 43.0 15.0

MINI CASE

Mini Case: 6 – 14

Barney Smith’s economic forecasting staff has developed probability estimates for the

state of the economy, and its security analysts have developed a sophisticated computer

program that was used to estimate the rate of return on each alternative under each state

of the economy. Alta Industries is an electronics firm; Repo Men collects past-due debts;

and American Foam manufactures mattresses and various other foam products. Barney

Smith also maintains an “index fund” which owns a market-weighted fraction of all

publicly traded stocks; you can invest in that fund, and thus obtain average stock market

results. Given the situation as described, answer the following questions.

a. What are investment returns? What is the return on an investment that costs

$1,000 and is sold after one year for $1,100?

Answer: Investment return measures the financial results of an investment. They may be

b. 1. Why is the t-bill’s return independent of the state of the economy? Do t-bills

promise a completely risk-free return?

Answer: The 8 percent t-bill return does not depend on the state of the economy because the

treasury must (and will) redeem the bills at par regardless of the state of the economy.

Mini Case: 6 – 15

b. 2. Why are Alta Ind.’s returns expected to move with the economy whereas Repo

Men’s are expected to move counter to the economy?

Answer: Alta Industries’ returns move with, hence are positively correlated with, the economy,

because the firm’s sales, and hence profits, will generally experience the same type of

c. Calculate the expected rate of return on each alternative and fill in the blanks on

the row for

r

in the table.

Answer: The expected rate of return,

r

, is expressed as follows:

Mini Case: 6 – 16

d. You should recognize that basing a decision solely on expected returns is

appropriate only for risk-neutral individuals. Because your client, like virtually

everyone, is risk averse, the riskiness of each alternative is an important aspect

of the decision. One possible measure of risk is the standard deviation of

returns.

1. Calculate this value for each alternative, and fill in the blank on the row for σ in

the table.

Answer: The standard deviation is calculated as follows:

d. 2. What type of risk is measured by the standard deviation?

Answer: The standard deviation is a measure of a security’s (or a portfolio’s) stand-alone risk.

Mini Case: 6 – 17

d. 3. Draw a graph that shows roughly the shape of the probability distributions for

Alta Industries, American Foam, and T-bills.

Answer:

Mini Case: 6 – 18

e. Suppose you suddenly remembered that the coefficient of variation (CV) is

generally regarded as being a better measure of stand-alone risk than the

standard deviation when the alternatives being considered have widely differing

expected returns. Calculate the missing CVs, and fill in the blanks in the row for

CV in the table. Does the CV produce the same risk rankings as the standard

deviation?

Answer: The coefficient of variation (CV) is a standardized measure of dispersion about the

expected value; it shows the amount of risk per unit of return.

f. Suppose you created a 2-stock portfolio by investing $50,000 in Alta Industries

and $50,000 in Repo Men.

1. Calculate the expected return (

p

r

), the standard deviation (σp), and the

coefficient of variation (CVp) for this portfolio and fill in the appropriate blanks

in the table.

Mini Case: 6 – 19

Answer: To find the expected rate of return on the two-stock portfolio, we first calculate the

rate of return on the portfolio in each state of the economy. Since we have half of our

money in each stock, the portfolio’s return will be a weighted average in each type of

However, this is not correct—it is necessary to use a different formula, the one for σ

that we used earlier, applied to the two-stock portfolio’s returns.

The portfolio’s σ depends jointly on (1) each security’s σ and (2) the correlation

between the securities’ returns. The best way to approach the problem is to estimate

the portfolio’s risk and return in each state of the economy, and then to estimate σp

with the σ formula. Given the distribution of returns for the portfolio, we can

Mini Case: 6 – 20

f. 2. How does the risk of this 2-stock portfolio compare with the risk of the

individual stocks if they were held in isolation?

Answer: Using either σ or CV as our stand-alone risk measure, the stand-alone risk of the

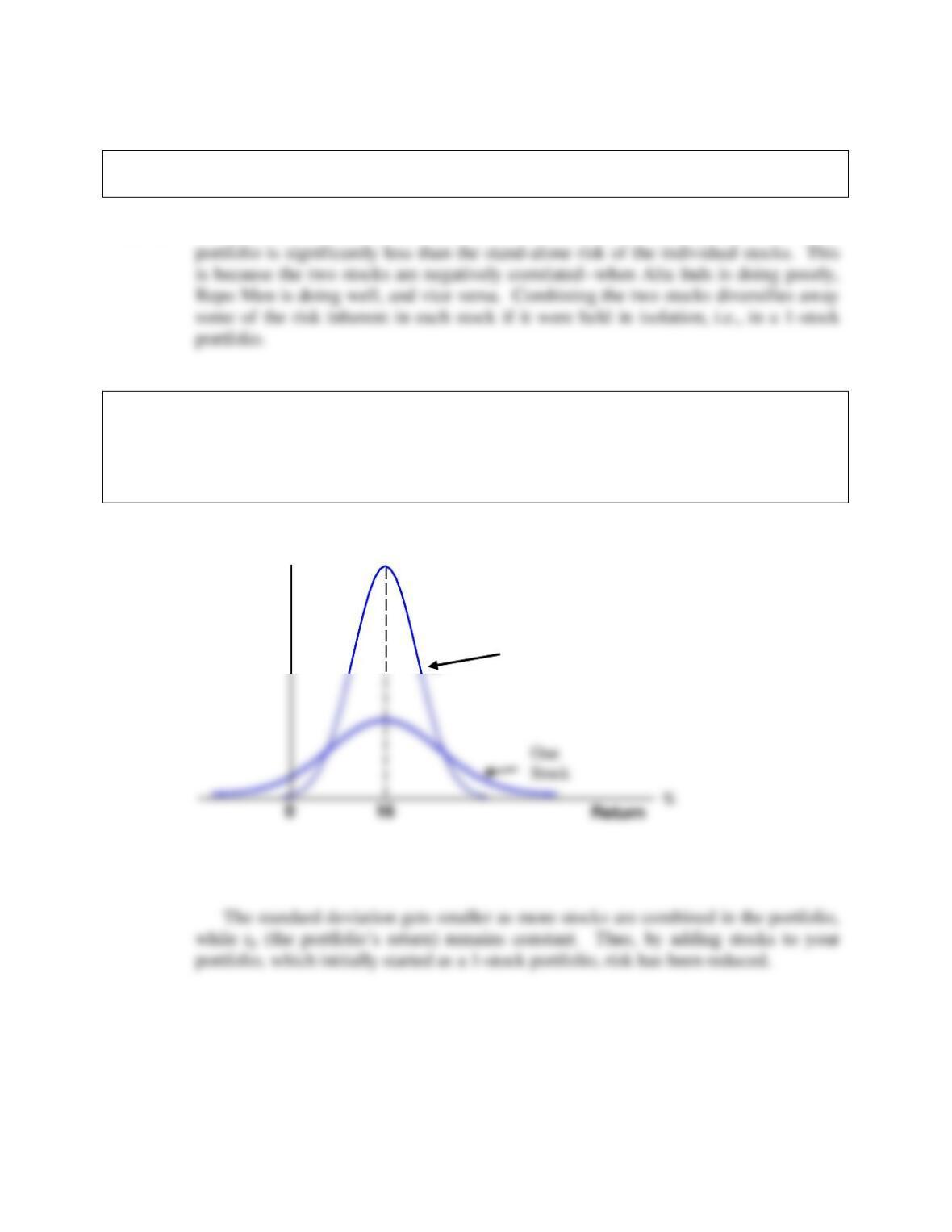

g. Suppose an investor starts with a portfolio consisting of one randomly selected

stock. What would happen (1) to the risk and (2) to the expected return of the

portfolio as more and more randomly selected stocks were added to the

portfolio? What is the implication for investors? Draw a graph of the two

portfolios to illustrate your answer.

Answer:

Density

Portfolio of stocks

with rp= 16%

Density

Portfolio of stocks

with rp= 16%

Mini Case: 6 – 21

h. 1. Should portfolio effects impact the way investors think about the risk of

individual stocks?

Answer: Portfolio diversification does affect investors’ views of risk. A stock’s stand-alone

risk as measured by its σ or CV, may be important to an undiversified investor, but it

Mini Case: 6 – 22

h. 2. If you decided to hold a 1-stock portfolio, and consequently were exposed to

more risk than diversified investors, could you expect to be compensated for all

of your risk; that is, could you earn a risk premium on that part of your risk

that you could have eliminated by diversifying?

Answer: If you hold a one-stock portfolio, you will be exposed to a high degree of risk, but

you won’t be compensated for it. If the return were high enough to compensate you

i. How is market risk measured for individual securities? How are beta

coefficients calculated?

Answer: Market risk, which is relevant for stocks held in well-diversified portfolios, is defined

j. Suppose you have the following historical returns for the stock market and for

another company, P.Q. Unlimited. Explain how to calculate beta, and use the

historical stock returns to calculate the beta for PQU. Interpret your results.

YEAR

MARKET

PQU

1

25.7%

40.0%

2

8.0%

-15.0%

3

-11.0%

-15.0%

4

15.0%

35.0%

5

32.5%

10.0%

6

13.7%

30.0%

7

40.0%

42.0%

8

10.0%

-10.0%

9

-10.8%

-25.0%

10

-13.1%

25.0%

Answer: Betas are calculated as the slope of the “characteristic” line, which is the regression

line showing the relationship between a given stock and the general stock market.

Show the graph with the regression results. Point out that the beta is the slope

coeeficient, which is 0.83. State that an average stock, by definition, moves with the

market. Beta coefficients measure the relative volatility of a given stock relative to

the stock market. The average stock’s beta is 1.0. Most stocks have betas in the

Mini Case: 6 – 24

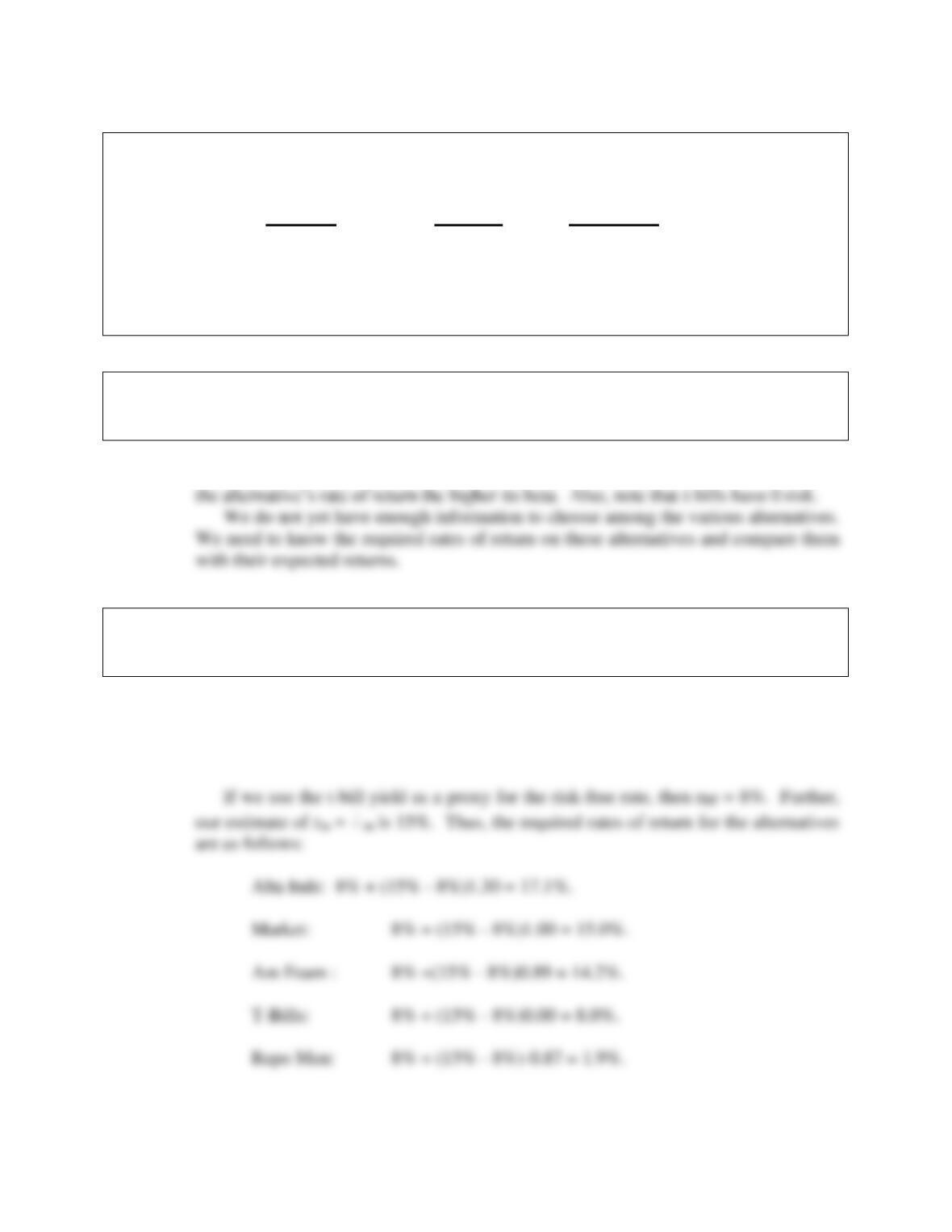

k. The expected rates of return and the beta coefficients of the alternatives as

supplied by Barney Smith’s computer program are as follows:

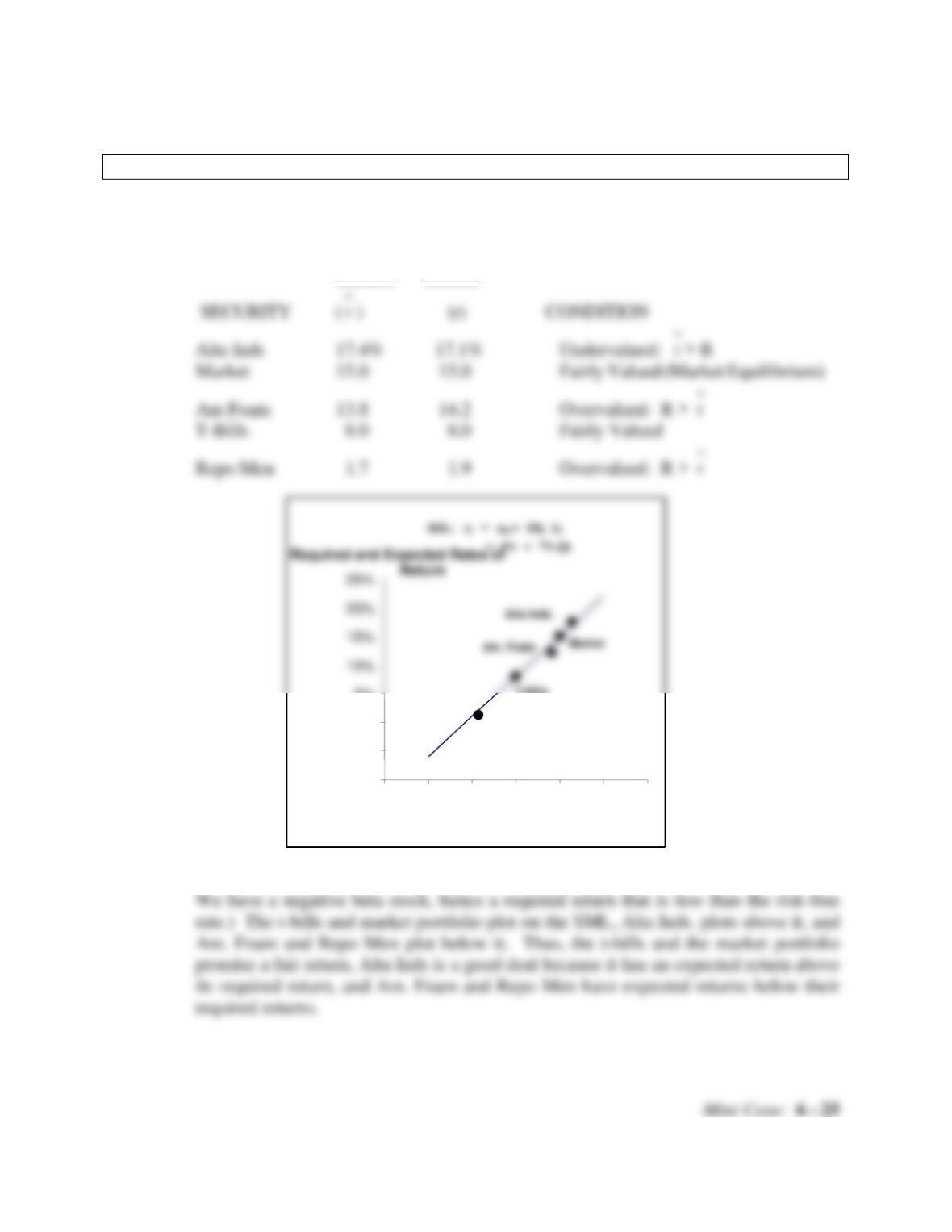

Security Return (

r

) Risk (Beta)

Alta Inds 17.4% 1.30

Market 15.0 1.00

Am. Foam 13.8 0.89

T-Bills 8.0 0.00

Repo Men 1.7 (0.87)

(1) Do the expected returns appear to be related to each alternative’s market risk?

(2) Is it possible to choose among the alternatives on the basis of the information

developed thus far?

Answer: The expected returns are related to each alternative’s market risk—that is, the higher

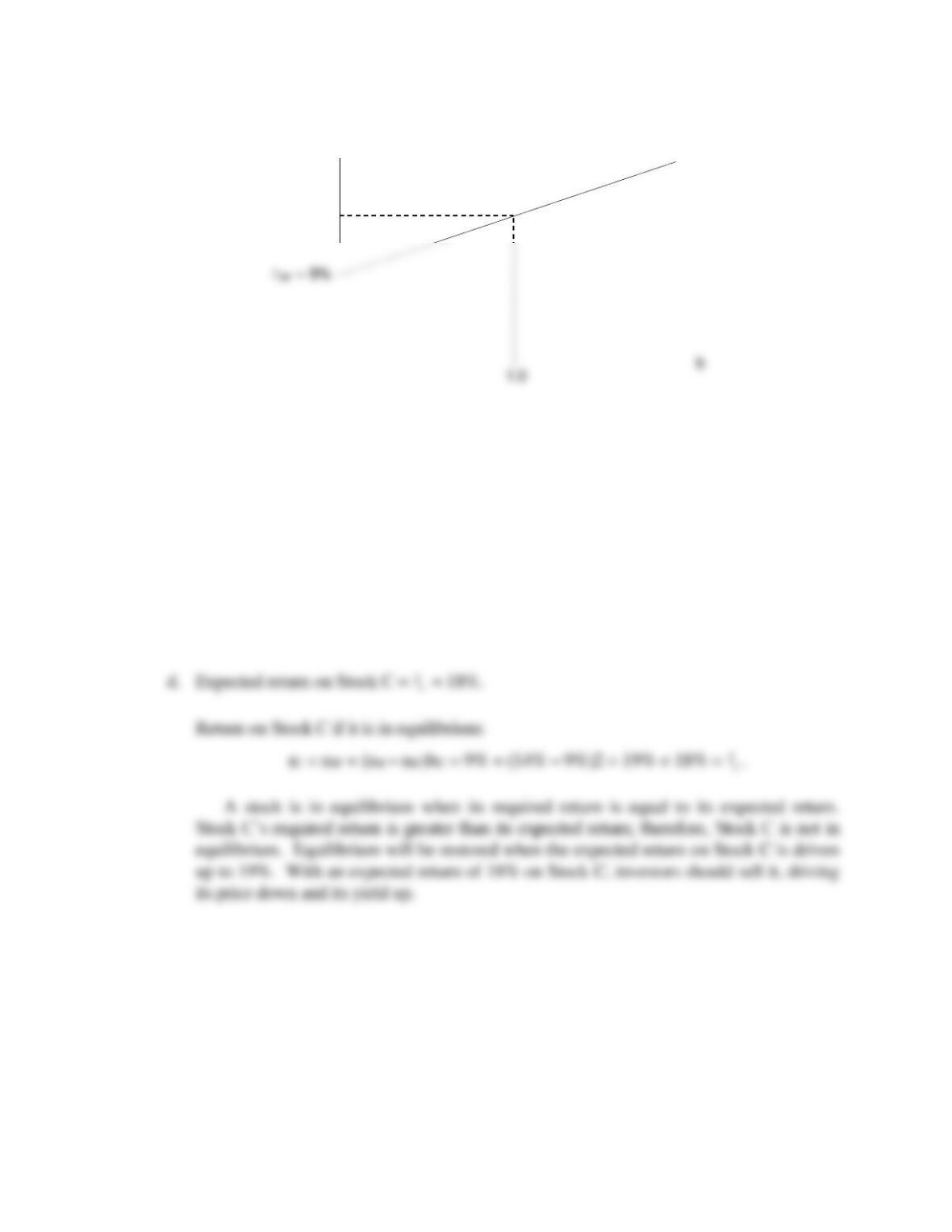

l. 1. Write out the Security Market Line (SML) equation, use it to calculate the

required rate of return on each alternative, and then graph the relationship

between the expected and required rates of return.

Answer: Here is the SML equation:

ri = rrf + (rm – rrf)bi.

10%

15%

20%

25%

Return

Market

Alta Inds.

l. 2. How do the expected rates of return compare with the required rates of return?

Answer: We have the following relationships:

Expected Required

Return Return

(Note: the plot looks somewhat unusual in that the x axis extends to the left of zero.

–10%

–5%

0%

5%

-3

-2

-1

0

1

2

3

Beta

Repo Men

T-Bills

Mini Case: 6 – 26

l. 3. Does the fact that Repo Men has an expected return that is less than the T-bill

rate make any sense?

Answer: Repo Men is an interesting stock. Its negative beta indicates negative market risk—

including it in a portfolio of “normal” stocks will lower the portfolio’s risk.

l. 4. What would be the market risk and the required return of a 50-50 portfolio of

Alta Industries and Repo Men? Of Alta Industries and American Foam?

Answer: Note that the beta of a portfolio is simply the weighted average of the betas of the

stocks in the portfolio. Thus, the beta of a portfolio with 50 percent Alta Inds and 50

percent Repo Men is:

Mini Case: 6 – 27

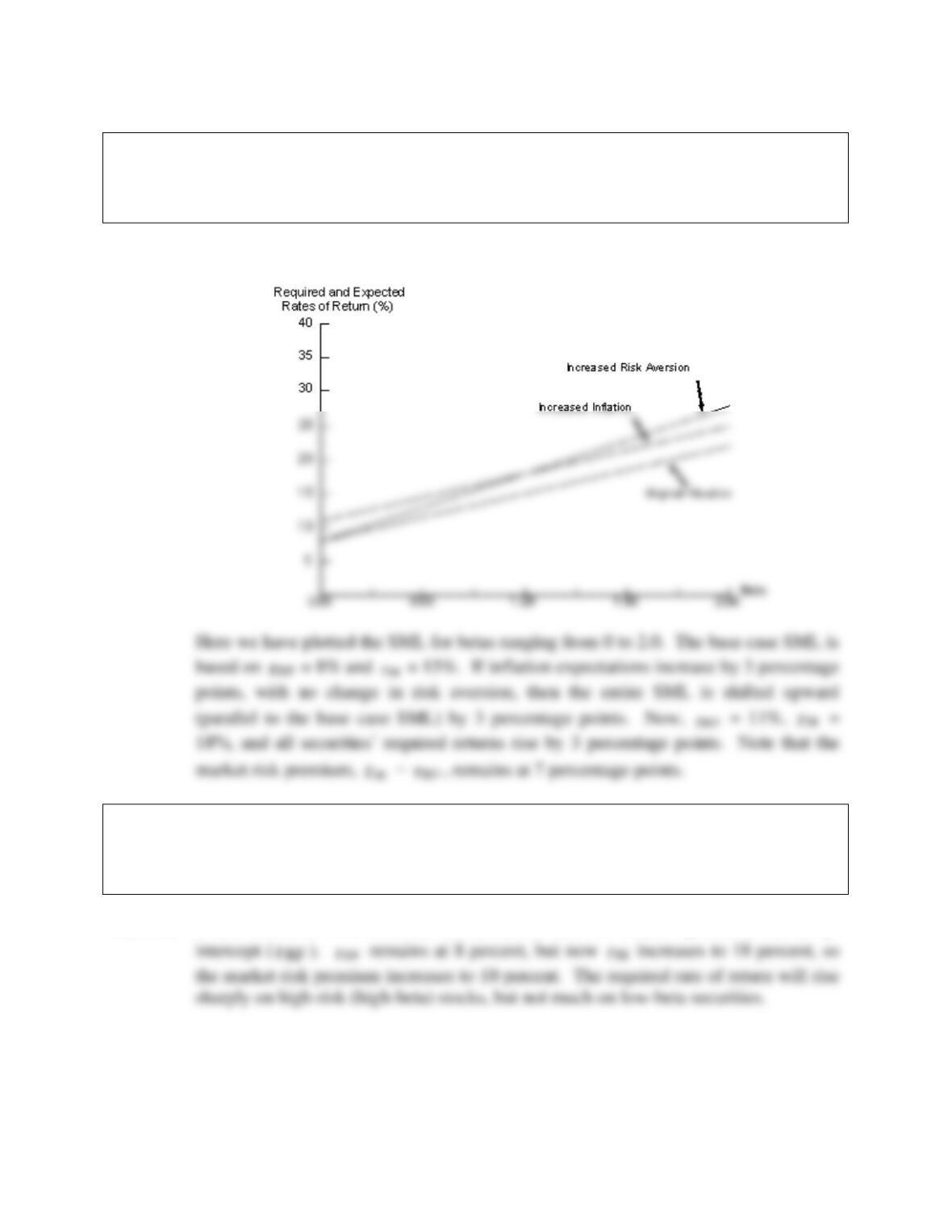

m. 1. Suppose investors raised their inflation expectations by 3 percentage points over

current estimates as reflected in the 8 percent T-bill rate. What effect would

higher inflation have on the SML and on the returns required on high– and low-

risk securities?

Answer:

m. 2. Suppose instead that investors’ risk aversion increased enough to cause the

market risk premium to increase by 3 percentage points. (Inflation remains

constant.) What effect would this have on the SML and on returns of high– and

low-risk securities?

Answer: When investors’ risk aversion increases, the SML is rotated upward about the y–

(%)rM

Web Appendix 6B

Calculating Beta Coefficients With a Financial Calculator

Solutions to Problems

6B-1 a.

b. Because b = 0.62, Stock Y is about 62% as volatile as the market; thus, its relative risk is

about 62% that of an average stock.

c. 1. Stand-alone risk as measured by would be greater, but beta and hence systematic

(relevant) risk would remain unchanged. However, in a 1-stock portfolio, Stock Y

would be riskier under the new conditions.

2. CAPM assumes that company-specific risk will be eliminated in a portfolio, so the

d. 1. The stock‘s variance and would not change, but the risk of the stock to an investor

holding a diversified portfolio would be greatly reduced, because it would now have

a negative correlation with rM.

(%)rY

40

30

e. The following figure shows a possible set of probability distributions. We can be

reasonably sure that the 100-stock portfolio comprised of b = 0.62 stocks as described in

Condition 2 will be less risky than the “market.” Hence, the distribution for Condition 2

will be more peaked than that of Condition 3.

Stock Y has b = 0.62, while the average stock (M) has b = 1.0; therefore,

ry = rRF + (rM – rRF)0.62 < rM = rRF + (rM – rRF)1.0.

A disequilibrium exists—Stock Y should be bid up to drive its yield down. More likely,

however, the data simply reflect the fact that past returns are not an exact basis for

expectations of future returns.

Web Solutions: 6B – 30

periods of transition, when the risk of the firm is changing, the beta can yield conclusions

that are exactly opposite to the actual facts. Once the company‘s risk stabilizes, the

calculated beta should rise and should again approximate the true beta.

6B-2 a.

The slope of the characteristic line is the stock’s beta coefficient.

Slope =

M

i

r

r

Run

Rise

=

.

The graph of the SML is as follows:

30

35

ri(%)

Stock A

30

35

ri(%)

Stock A

Web Solutions: 6B – 31

The equation of the SML is thus:

ri = rRF + (rM – rRF)bi = 9% + (14% – 9%)bi = 9% + (5%)bi.

c. Required rate of return on Stock A:

rA = rRF + (rM – rRF)bA = 9% + (14% – 9%)1.0 = 14%.

Required rate of return on Stock B:

rB = 9% + (14% – 9%)0.5 = 11.50%.

SML

ri

E(r M) = 14%

SML

ri

E(r M) = 14%

SML

ri

E(r M) = 14%E(r M) = 14%