134

ADDITIONAL CASE STUDY

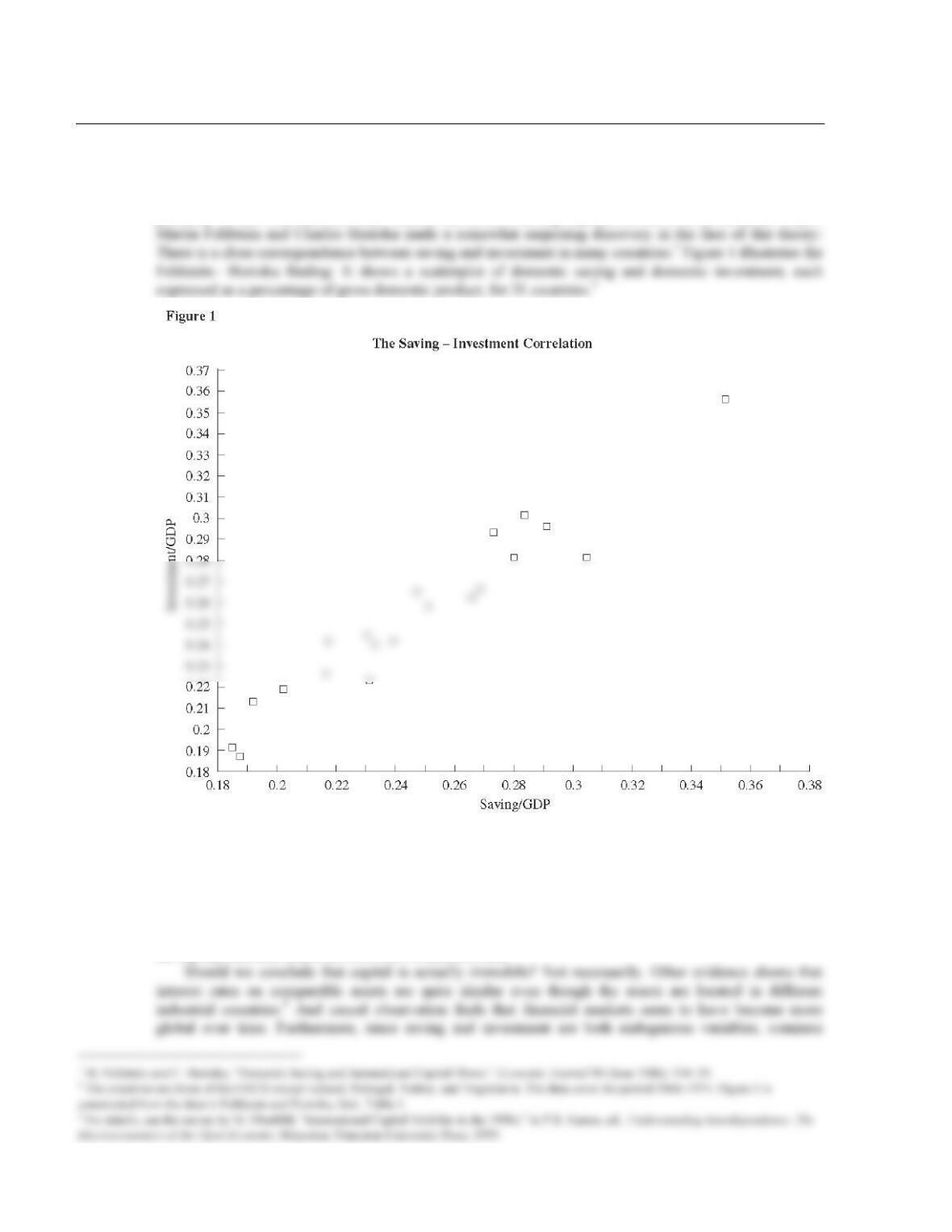

6-2 Saving and Investment in Open Economies

Our theory of the small open economy suggests that there should be no simple link between the level of

saving and the level of investment. With perfect capital mobility, the level of investment depends

primarily on the world interest rate, whereas the level of saving depends on the level of domestic output.

Source: M. Feldstein and C. Horioka, “Domestic Saving and International Capital Flows,” Economic Journal 90

(June 1980): 319.

Feldstein and Horioka’s work has been updated and modified by many authors over the years.

Although the correlation between saving and investment rates varies with particulars such as which

countries are included and which time periods are considered, the basic finding remains the same:

Countries that have high saving rates are also countries with high investment rates, and countries with low

saving rates are also countries with low investment rates.

135

influences on saving and investment could yield a positive correlation even if capital is completely mobile

across national boundaries.

Concern about common influences is the main reason why Feldstein and Horioka averaged saving and

investment rates across long periods of time and studied the cross–country relationship. This technique

allowed them to separate the effect from short–run business cycle fluctuations that may induce a

correlation between saving and investment within a country from year to year. But even over long periods

of time, saving and investment continue to be endogenously determined, and common influences may still

be important.

One way that a correlation might occur is in response to sustained shifts in a country’s productivity or

demographics that lead to an increase in its long–run investment rate and its long–run saving rate.44 For

instance, a technological advance in one country may increase investment at the world interest rate and,

136

LECTURE SUPPLEMENT

6-3 The Open Economy in the Very Long Run

The small open economy model of Chapter 6 explains that the trade balance is determined in the long run

by the levels of domestic saving and investment. For example, if domestic saving is less than domestic

investment at the world interest rate, then net exports are negative, and there is a trade deficit. The

counterpart to this trade deficit is an increase in indebtedness to foreigners.

The model of Chapter 6 evidently cannot describe the economy in the very long run because a country

cannot run large trade deficits forever.1 At some point, the foreign debt must be repaid. Something is,

therefore, missing from the Chapter 6 model if we wish to talk about the very long run.

ADDITIONAL CASE STUDY

6-4 Tourism and the Exchange Rate

Expenditures on international tourism are likely to be sensitive to changes in exchange rates because a

significant amount of tourism probably represents discretionary purchases that are sensitive to relative

prices. Vacations taken abroad by Americans contribute to U.S. imports, while expenditures by foreigners

on visits to the United States add to U.S. exports. Table 1 (see next page) presents the percentage change

138

Table 1 Tourism Trade and the Real Exchange Rate

Year

Real Tourism

Exports (%

change)

Real Tourism

Imports (%

change)

Real Exchange

Rate (Index,

March 1973 =

100)

1973

14.9

–5.7

99.0

1975

8.1

–3.5

94.5

1976

13.9

6.4

94.5

1977

0.2

3.0

92.9

1978

7.4

3.3

87.3

1979

7.2

–2.4

88.4

1980

11.7

–0.1

89.8

1981

33.1

9.0

96.6

1982

–7.7

18.6

106.1

1983

–11.2

13.3

110.6

1984

Break in series

Break in series

117.9

1985

0.1

10.3

122.7

1986

10.3

–6.9

107.4

1987

8.5

18.4

98.7

1988

16.6

2.9

92.1

1989

18.1

3.1

93.8

1990

12.3

6.8

91.2

1991

4.7

–9.2

89.7

1992

10.1

3.1

87.8

1993

4.6

5.0

89.1

1994

1.2

3.6

89.0

1995

6.3

1.1

86.5

1996

6.5

4.0

88.5

1997

2.9

8.7

93.2

1998

–2.7

13.2

101.2

1999

5.6

0.1

100.3

2000

3.7

12.8

104.1

2001

–14.4

–7.0

110.1

2002

–5.8

–4.8

110.3

2003

–4.6

–4.8

103.6

2004

10.4

13.0

99.0

2005

–4.4

2.0

97.3

2006

–1.0

0.2

96.2

2007

9.0

–2.1

91.7

2008

7.2

–2.7

87.8

2009

–8.0

–9.0

91.4

2010

10.8

4.1

87.2

2011

4.8

0.8

82.7

2012

3.9

11.7

84.4

2013

6.4

2.7

84.5

2014

4.2

6.9

86.3

Source: U.S. Department of Commerce, Bureau of Economic Analysis and Federal Reserve Board.

Note: Real tourism exports and imports are exports and imports of travel as reported in the National Income and

Product Accounts. The real exchange rate is a weighted average of the foreign exchange values of the U.S. dollar

1974

8.8

–10.2

95.6

139

CASE STUDY EXTENSION

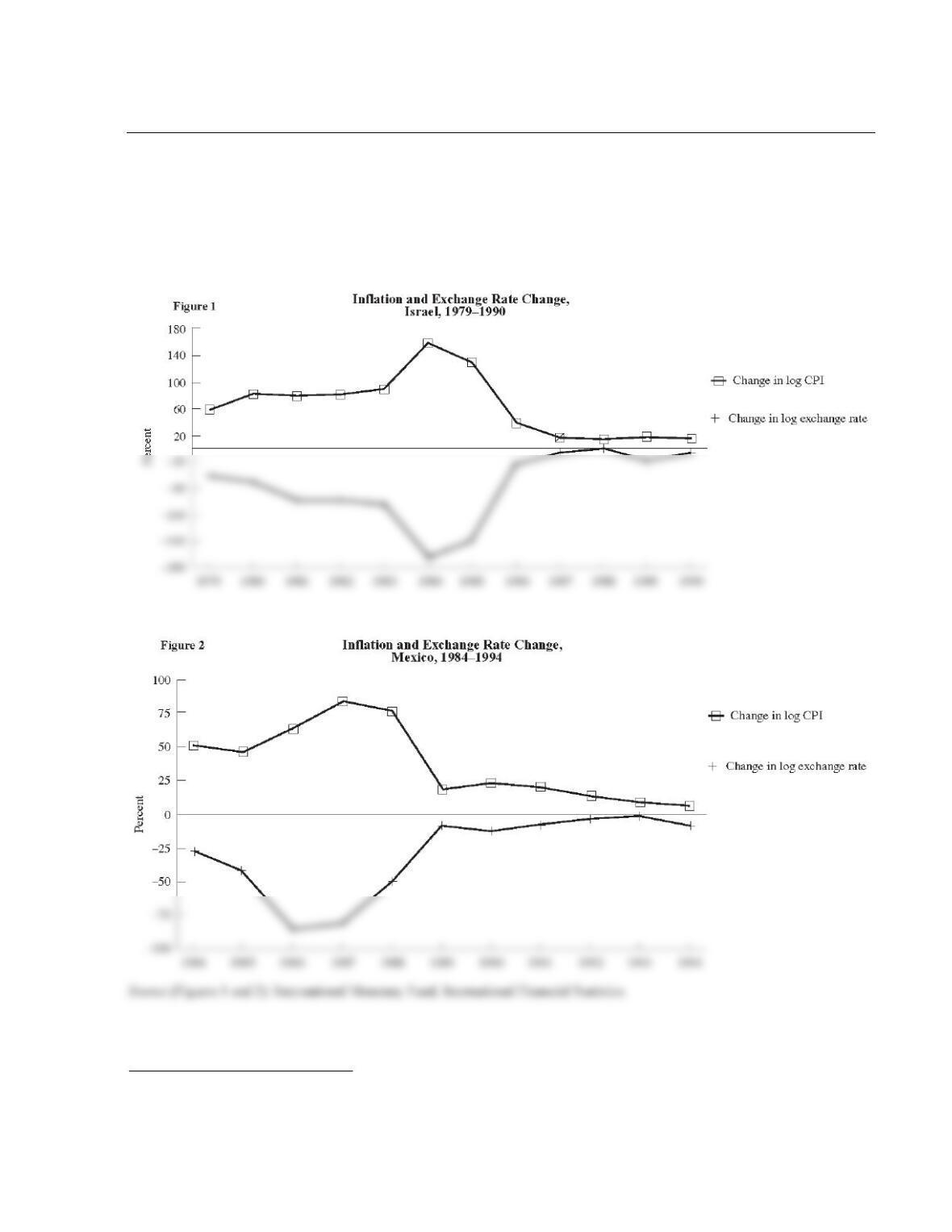

6-5 The Exchange Rate and the Inflation Rate

The relationship between the nominal exchange rate and the inflation rate is particularly evident for

countries experiencing hyperinflation. If the price level in one country is increasing rapidly, then

movements in foreign prices and in the real exchange rate will be relatively insignificant. We therefore

expect to see depreciation of the domestic currency at a rate approximately equal to the inflation rate.

Figures 1 and 2 illustrate this for the Israeli and Mexican hyperinflations of the 1980s.1

1 Figures 1 and 2 present changes in the logarithms of the two variables. The change in the logarithm is a measure of the growth rate of a variable.

The close negative relationship between the inflation rate and the change in the exchange rate thus illustrates that price level increases were indeed

matched by currency depreciation. See Supplement 8–5, “Growth Rates, Logarithms, and Elasticities,” for more information on growth rates and

logarithms.

ADVANCED TOPIC

6-6 Covered Interest Parity

Suppose that a U.S. company wishes to purchase goods from a producer in the United Kingdom. The U.S.

firm agrees to take delivery of the goods three months hence and to pay an agreed–upon price in U.K.

pounds at that time. The U.S. company, however, might be concerned about exactly what was going to

happen to the dollar–pound exchange rate over the next three months.1 It can avoid this uncertainty by

buying U.K. pounds at the forward rate. International financial institutions not only buy and sell currencies

at the current (spot) rate, they are also willing to write an agreement to exchange currencies at a future date

and at a prespecified rate. Thus, if the U.S. company needs 10,000 pounds in three months’ time, it knows

1 + i = (e/f)(1 + i*).

If we define the forward premium to be (f – e)/e, then we have a good approximation3:

Premium ≅ i* – i.

The premium will be positive (i.e., the forward rate will be above the spot rate) if the U.K. interest rate

exceeds the U.S. interest rate. The premium will be negative if the opposite is true.

The forward rate should be a good predictor of the future spot rate. To see this, note that if investors

1 This is a particular concern since exchange rates can be quite volatile in the short run. See Chapter 13 of the textbook and Supplement 13–11,

141

ADDITIONAL CASE STUDY

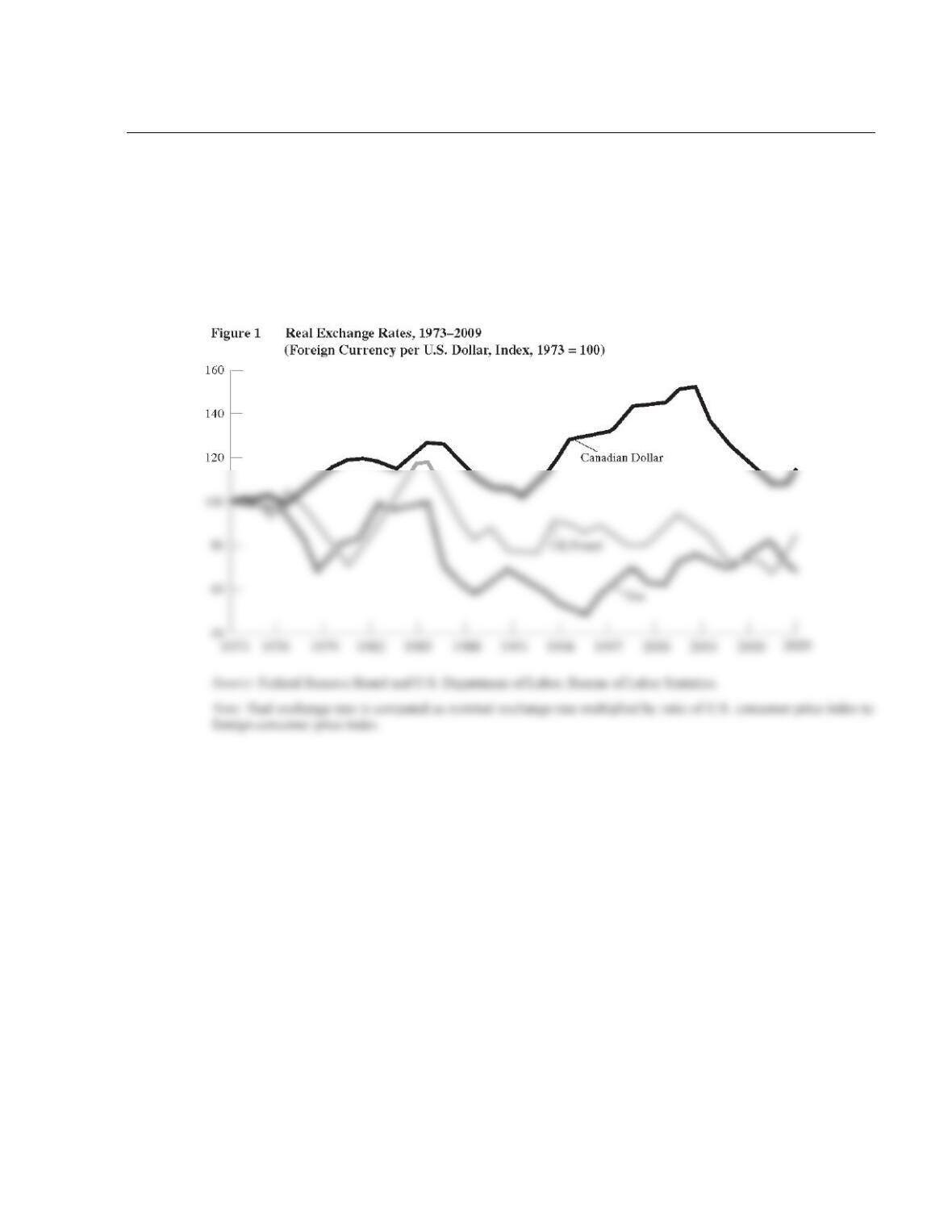

6-7 Purchasing–Power Parity and Real Exchange Rates

If the principle of purchasing–power parity provided an accurate theory of real exchange rate

determination, then we would expect real exchange rates to be relatively stable. Major short–run

fluctuations in the real exchange rate would not occur because of arbitrage in goods markets. Such

stability is, quite simply, not observed in the data. As an example, Figure 1 shows the real exchange rates

for Canada, the United Kingdom, and Japan. Economists, therefore, look to behavior in financial markets

rather than goods markets for explanations of short–run fluctuations in exchange rates.

142

CASE STUDY EXTENSION

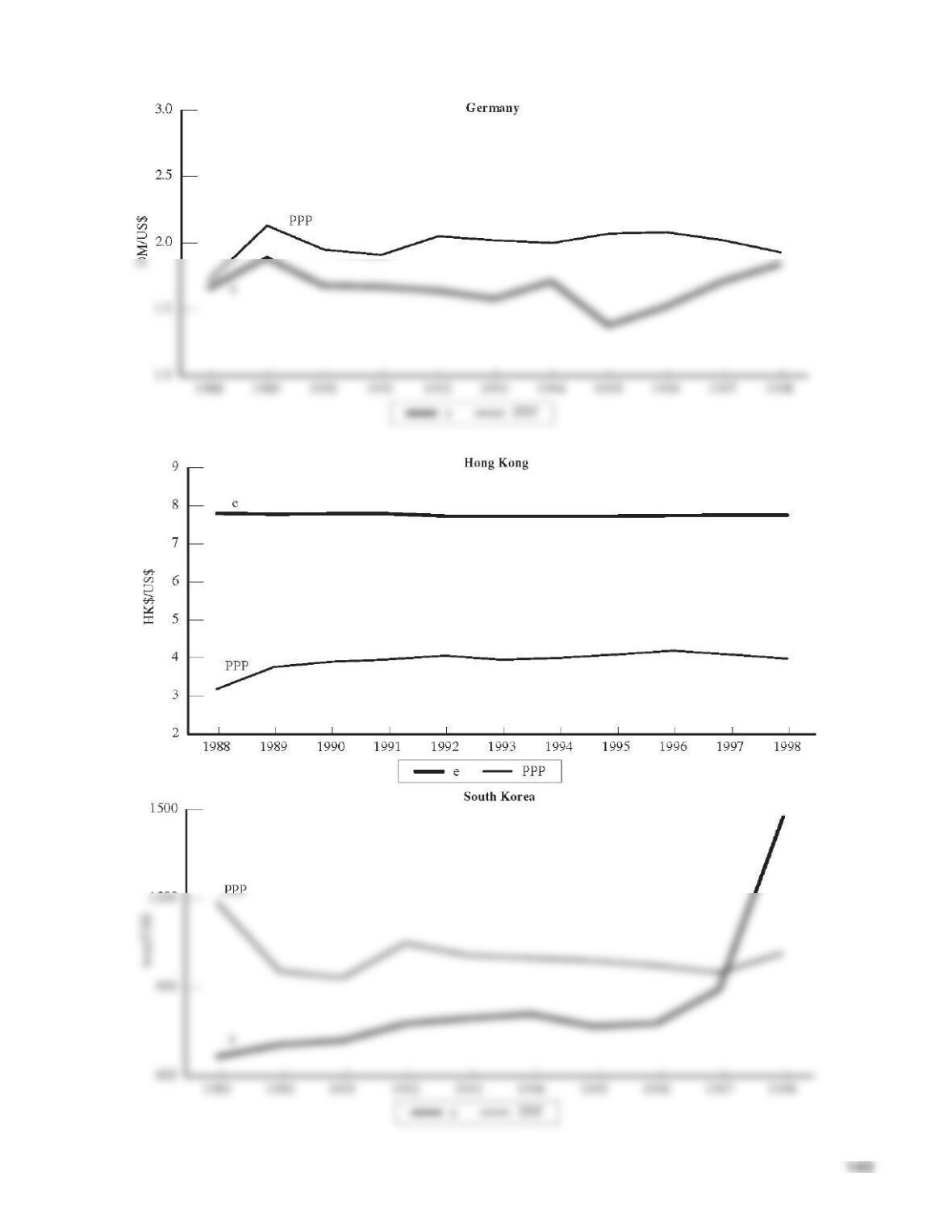

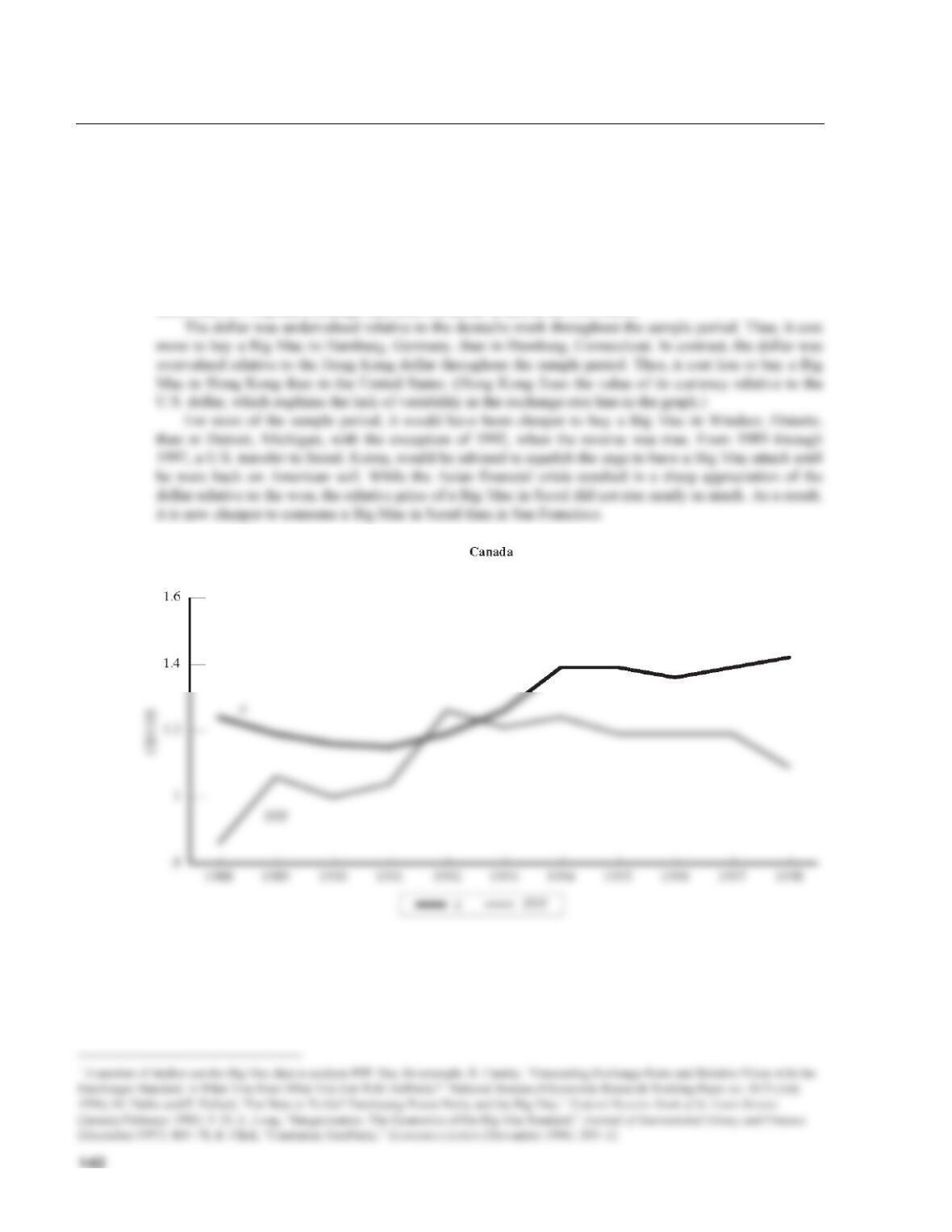

6-8 More on the Big Mac and PPP

The following graphs use the series of Big Mac prices and exchange rates collected by The Economist to

illustrate the failure of PPP.11 For each of the four countries (Canada, Germany, Hong Kong, and South

Korea), the graph shows the actual exchange rate (foreign currency per U.S. dollar) and the exchange rate

implied by PPP. The latter is simply the ratio of the price of a Big Mac in each country to the price of a

Big Mac in the United States, both prices measured in local currency terms. If PPP held, the actual

exchange rate and the PPP implied exchange rate would be the same. If the actual exchange rate is above

the PPP implied exchange rate, then the dollar is said to be undervalued. If the actual exchange rate is

below the PPP implied exchange rate, then the dollar is said to be overvalued.