1

6 Increasing Returns to Scale and Imperfect Competition

Notes to Instructor

Chapter Summary

In the Ricardian and modified specific-factors model as well as in the Heckscher–Ohlin

model, we assumed perfectly competitive markets, where there are many firms, each

producing a homogeneous product, and where no firm is able to influence the market

price. In this chapter, we drop the assumption of perfectly competitive markets. We will

now assume imperfect competition, where firms are now able to influence the price of

their product.

There are many forms of imperfect competition that result from the breakdown of

assumption(s) of perfect competition. The market power that originates from the

Two new explanations for trade will be explored in this chapter that arise as a direct

result of the monopolistic competition model. Both of these additional reasons for trade

are a result of the two main characteristics of this model. The first characteristic is

product differentiation and the second feature is increasing returns to scale, where the

average costs for a firm fall as greater output is produced.

The second feature of monopolistic competition is increasing returns to scale. Here, firms

specialize in the product lines that are most successful, and by selling more of those

products, the average costs of production fall for them. Firms can lower their average

costs by selling not just in their own home markets but can achieve even lower costs by

selling in larger foreign markets, thereby increasing the size of the markets they reach.

3

Comments

By now, students should have a good understanding of the concept of comparative

advantage as the basis for trade. To get them thinking about the monopolistic competition

model and product differentiation, find out how many prefer Coca Cola versus Pepsi

Lecture Notes

Introduction

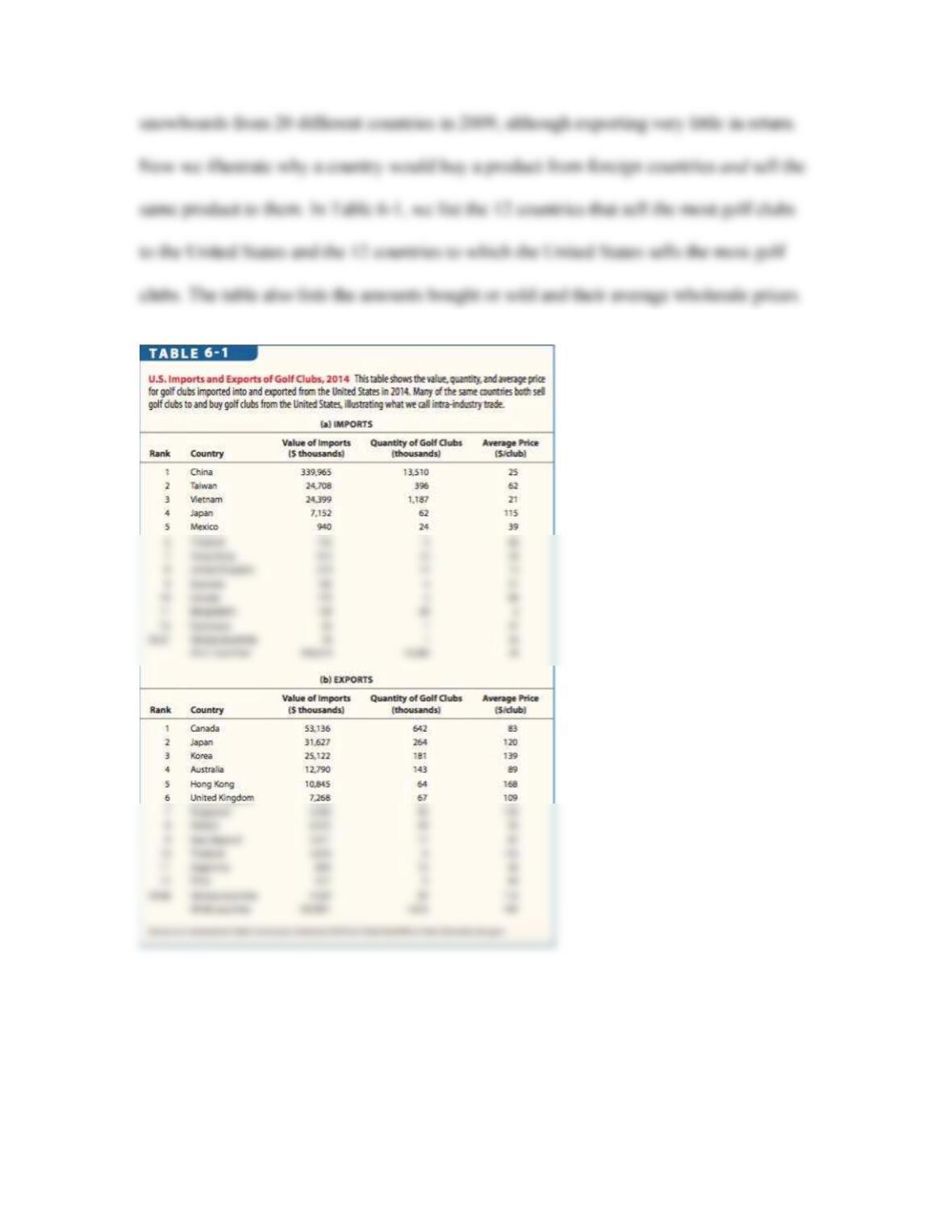

Due to proximity, resources, and comparative advantage, the United States imported

4

By contrast, the United States imported golf clubs valued at $399 million from 25

countries and exported $157 million of the product to about 66 countries in 2014. Panel

5

(a) of Table 6-1 shows that China is the top-selling country of golf clubs to the United

States, with $340 million sold at an average price of $25 each. Taiwan comes in at a

distant second at $25 million; however, its average price is considerably higher at $62

To explain why the United States is both an importer and exporter of golf clubs, we

introduce a market structure called monopolistic competition, whereby countries trade

goods that are similar but not identical to each other. In other words, a firm is able to

maintain some monopoly power by differentiating its products from those of its

6

1 Basics of Imperfect Competition

Monopoly Equilibrium We begin by reviewing the monopoly and duopoly market

cases. Understanding how demand is determined within these two types of markets will

help to explain how demand is determined in the monopolistic competitive market.

Recall from your principles course that as the sole producer in a market, the demand

curve faced by the monopolist is the industry demand curve. As shown in Figure 6-1, the

industry demand curve, D, is downward-sloping, which means that the monopolist must

7

Demand with Duopoly By adding one additional firm to the industry, we have a

duopoly, where the industry demand curve, D (illustrated in Figure 6–2), is shared

between the two competitors. If they charge identical prices, each firm faces one half of

the industry demand, D/2. Namely, at the price of P1, the industry demand is at point A so

that each firm sells the quantity Q2, which is half of the total market demand Q1. If the

product is homogeneous, one of the firms will be able to capture the entire market simply

8

the price to P2 if the first firm maintains its price at P1.

2 Trade Under Monopolistic Competition

We will now turn to the monopolistic competition model beginning with assumption 1.

Assumption 1: Each firm produces a good that is similar to but differentiated from the

goods that other firms in the industry produce.

Assumption 2: There are many firms in the industry.

Assumption 3: Firms produce using a technology with increasing returns to scale.

Increasing returns to scale technology means that the average cost of production

10

Numerical Example For simplicity, let’s look at a numerical example with a firm that

has constant marginal costs similar to those depicted in Figure 6-3. Suppose the firm has

the following costs of production:

From the following table, we see that average cost for the first ten units of output is $20

each. Notice that marginal cost is lower at $10 per unit. Because MC is less than AC, the

firm would be able to lower its average costs by increasing the quantity produced. With

the next additional 10 units produced, the firm’s AC decreases to $15 per unit.

Quantity, Q

Variable costs

= Q • MC

Total Costs =

Variable Costs+

Fixed Costs (FC =

$100)

Average Costs =

Total Costs/Quantity

10

$100

$200

20

20

200

300

15

30

300

400

13.33

40

400

500

12.5

50

500

600

12

11

Assumption 4: Firms can enter and exit the industry freely, so monopoly profits are zero

in the long run.

Equilibrium Without Trade

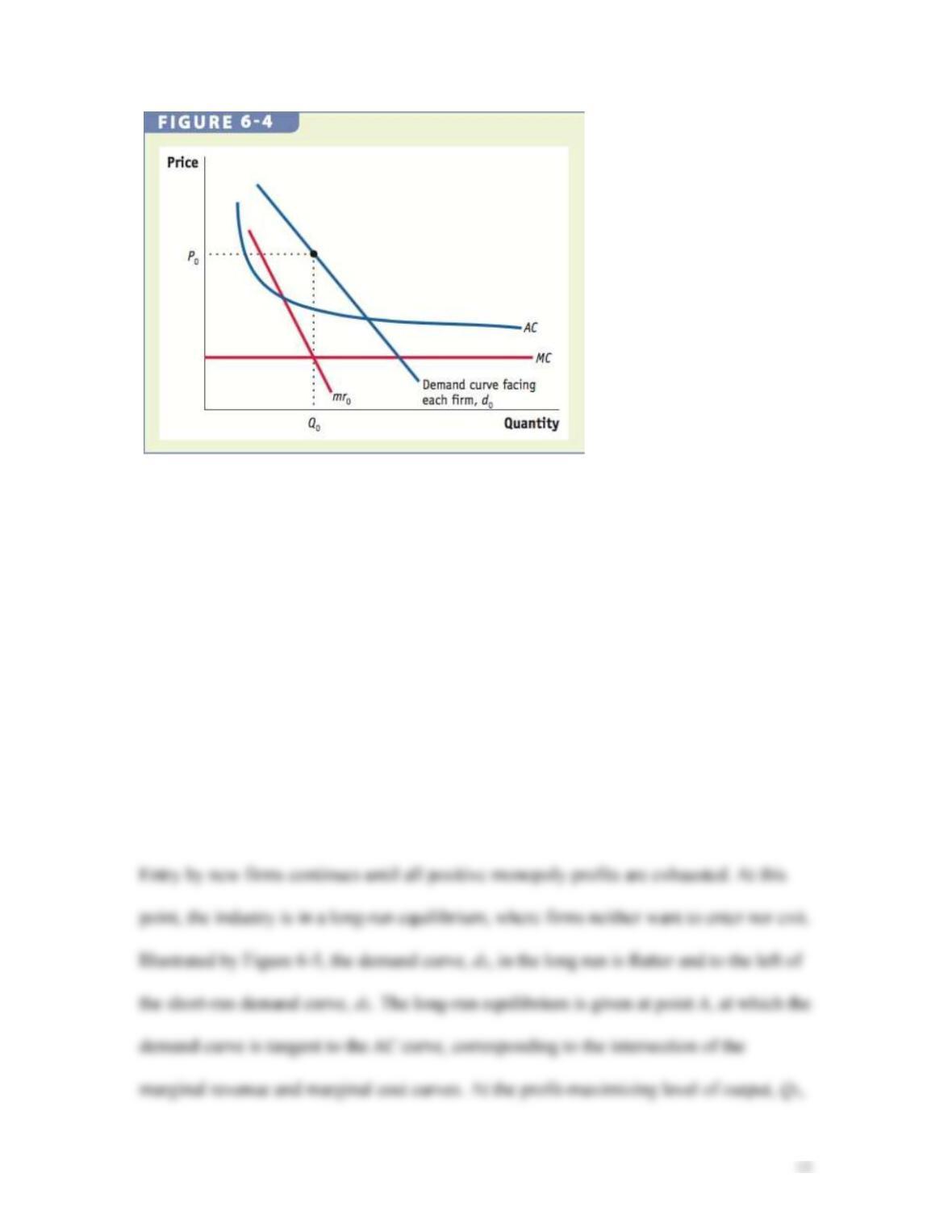

Short–Run Equilibrium As shown in Figure 6-4, a firm in a monopolistic competition

faces a downward-sloping demand curve, d0. This is because consumers view its product

to be different from that of other firms in the industry. In the short run, a monopolistically

Long–Run Equilibrium Attracted by the monopoly profits and given the assumption of

free entry into the industry, new firms will provide similar, albeit not identical, products

to existing consumers. With the availability of new product varieties, some consumers

will switch their purchases to the new firms, causing the demand curve, d0, for the

established firm to shift to the left. In addition to losing some consumers who opt to try

the new varieties, the firm faces a more elastic demand curve as consumers become more

price–sensitive given the increasing number of close substitutes.

13

and price, PA, the firm is making zero profits because price equals average costs.

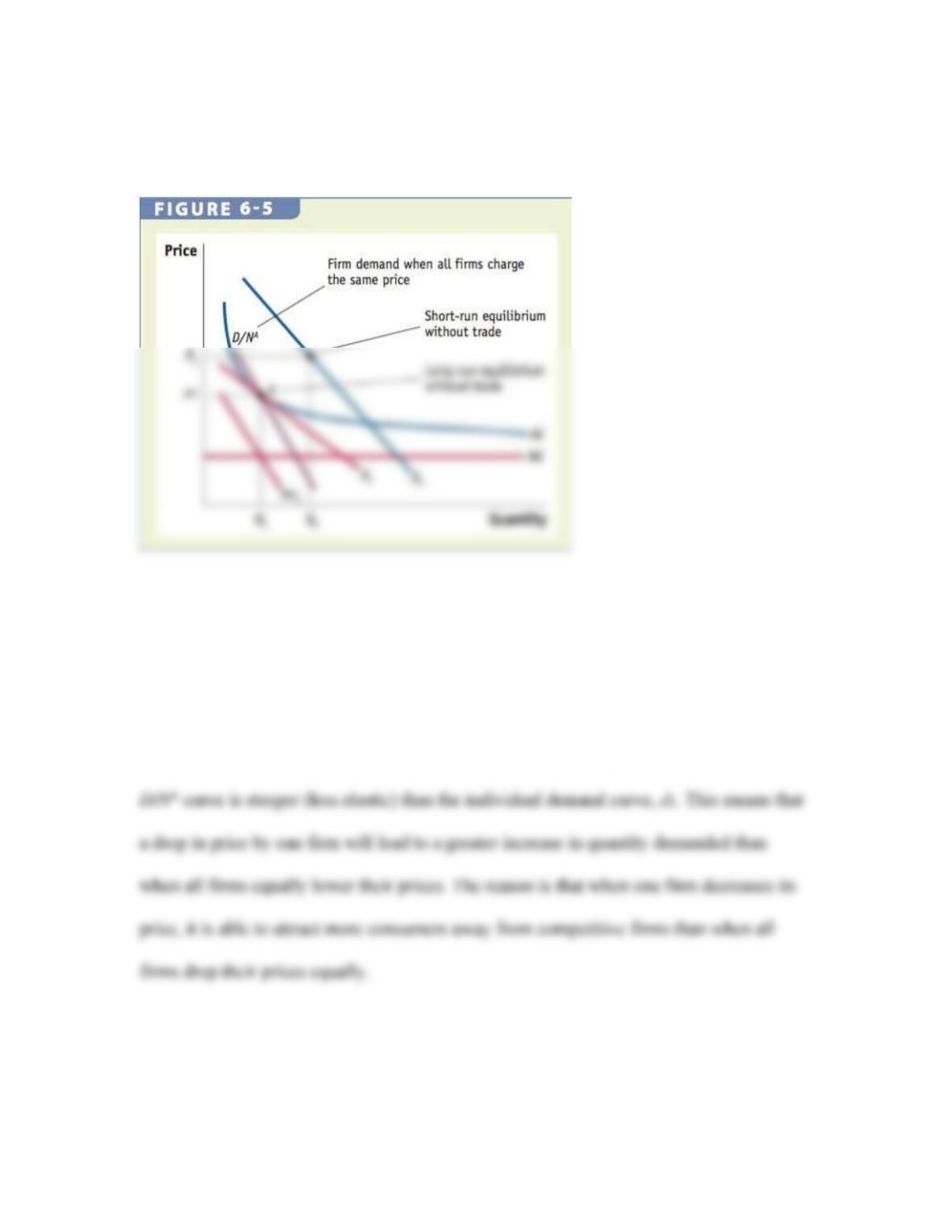

We now introduce another demand curve, D/NA, to Figure 6-5 before examining trade

under monopolistic competition. This demand curve, derived from dividing the total

market demand, D, by the number of firms in autarky, NA, reflects the quantity that

demanded that is faced by each firm when all competitors charge the same price. The

Equilibrium with Free Trade

Suppose firms in both Home and Foreign are monopolistically competitive. For

14

simplicity, further assume that the two countries are identical in terms of size, number of

consumers and firms, and technology and cost curves. Note that without the assumption

of increasing returns to scale, the two countries would not engage in trade given their

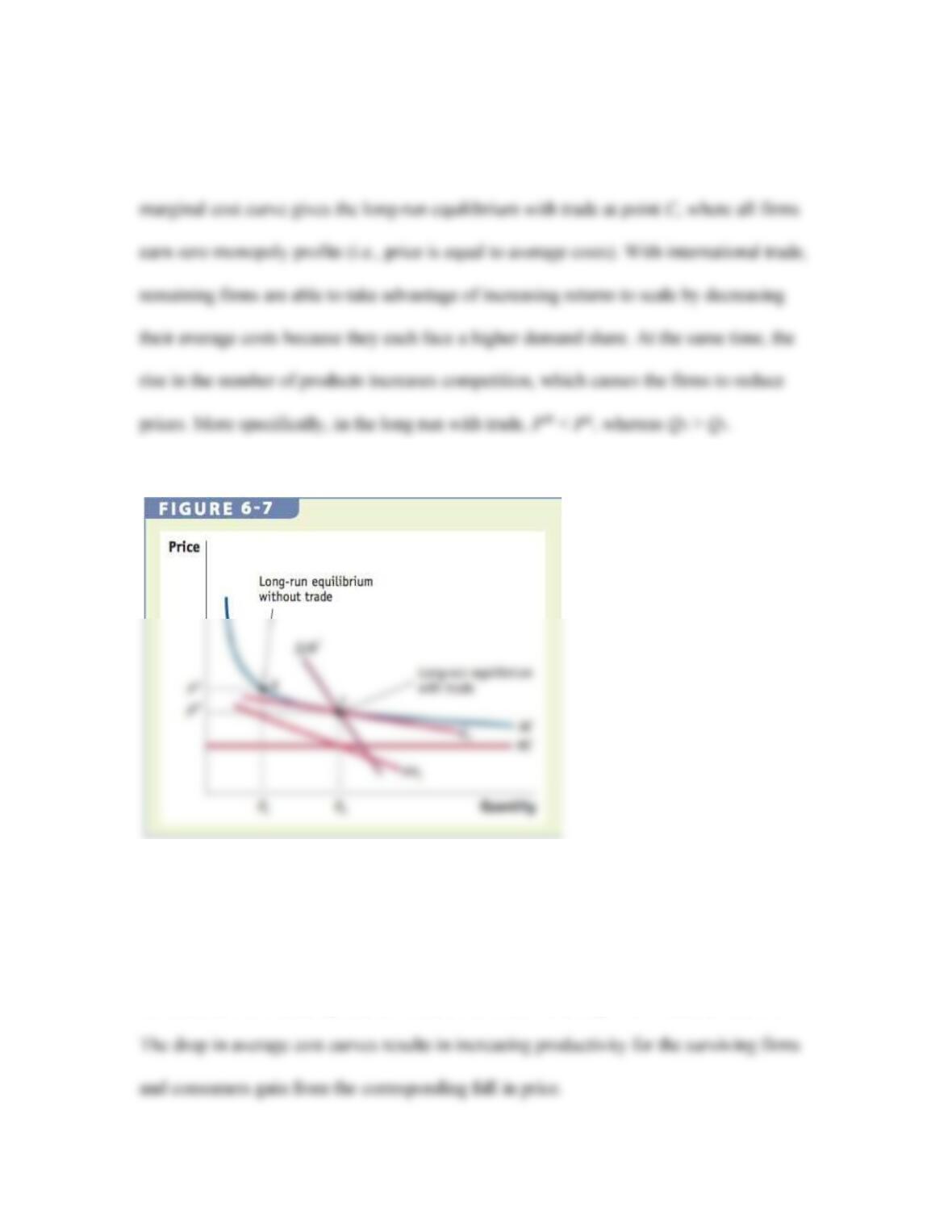

Short–Run Equilibrium with Trade We begin with the no-trade equilibrium given by

point A in Figure 6-5, which is reproduced in Figure 6-6. As the two countries engage in

trade, the number of consumers each firm can serve doubles. Likewise, there are twice as

many firms available to consumers in each country so that the demand curve, D/NA,

remains the same (i.e., 2D/2NA = D/NA). However, with the doubling of the number of

However, motivated by the same incentive to attract consumers from other firms by

15

lowering prices, every firm in the industry will make the same decision. This collective

Long–Run Equilibrium with Trade The losses will cause some firms to leave the

industry, reducing the product varieties available to consumers and increasing demand for

surviving firms. The number of firms remaining in each country after trade, NT, is less

16

greater product variety with trade, the demand curve, d3, facing each firm is more elastic

than with absence of trade. The intersection of the marginal revenue curve, mr3, with the

Gains from Trade In general, consumers gain as a result of trade under monopolistic

competition. In particular, consumers benefit because of the reduction in the price, as

reflected by the increasing returns to scale the firms remaining in the industry receive.

17

Adjustment Costs from Trade Nevertheless, to fully examine the overall effect of trade

when firms compete under imperfect competition, we need to also analyze the short-run

3 The North American Free Trade Agreement

Although the notion that trade could lead to an increase in product varieties was

discussed earlier by David Ricardo, the introduction of the monopolistic competition

Gains and Adjustment Costs for Canada Under NAFTA

The gains and losses for Canada after joining the Canada–U. S. Free Trade Agreement

(CUSFTA) were examined by economist Daniel Trefler at the University of Toronto.

18

However, real earnings in Canada rose by a modest 2.4% for production workers or .3%

per year in spite of the 0.7% per year in productivity growth in manufacturing, suggesting

that perhaps manufacturing workers did not entirely share in the gains from productivity.

Gains and Adjustment Costs for Mexico Under NAFTA

As part of its economic reforms, Mexico joined NAFTA along with the United States and

Canada in 1994. Under NAFTA, Mexican tariffs on U.S. goods declined from 14% in

H E A D L I N E S

Nearly 20 Years After NAFTA, First Mexican Truck Arrives in U.S. Interior

On October 21, 2011, the first big-rig truck from Mexico crossed the border into Laredo,

Texas, under a trucking program that was agreed to in NAFTA, but took nearly 20 years

to implement. The Obama administration finally signed an agreement with Mexico to end

the long dispute over the NAFTA provisions that Mexican trucks be permitted into the

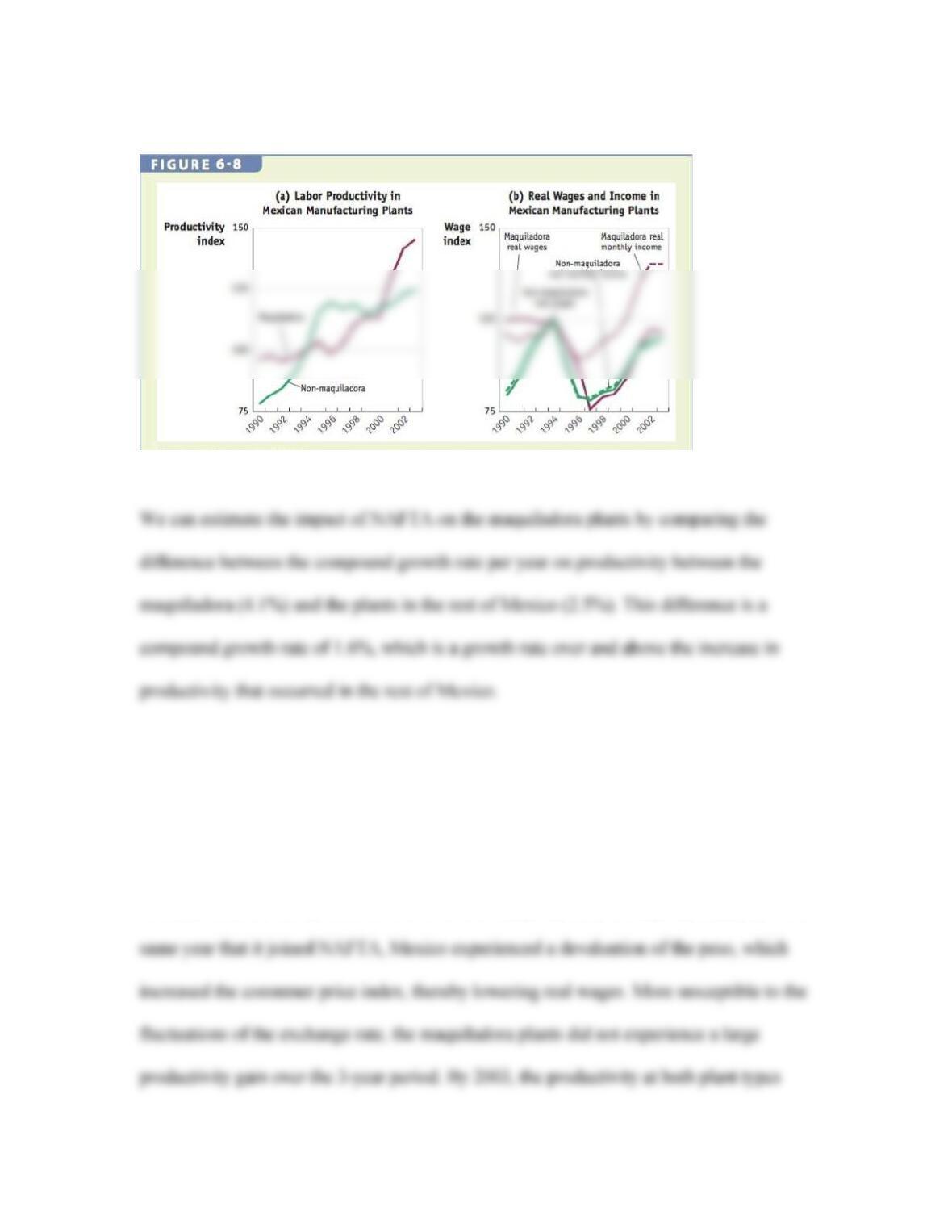

Productivity in Mexico We can examine the growth in labor productivity in Mexico, as

shown in panel (a) of Figure 6-8 for maquiladora plants—those near the U.S. border,

producing mostly for export to United States—and for all other non-maquiladora

20

Real Wages and Incomes Panel (b) of Figure 6–8 shows the real wages in the

maquiladora and non-maquiladora plants. Between 1994 and 1997, the real wages for

Mexican workers fell by over 20% in both non-maquiladora and maquiladora plants. The