Chapter 5: Time Value of Money

Integrated Case

113

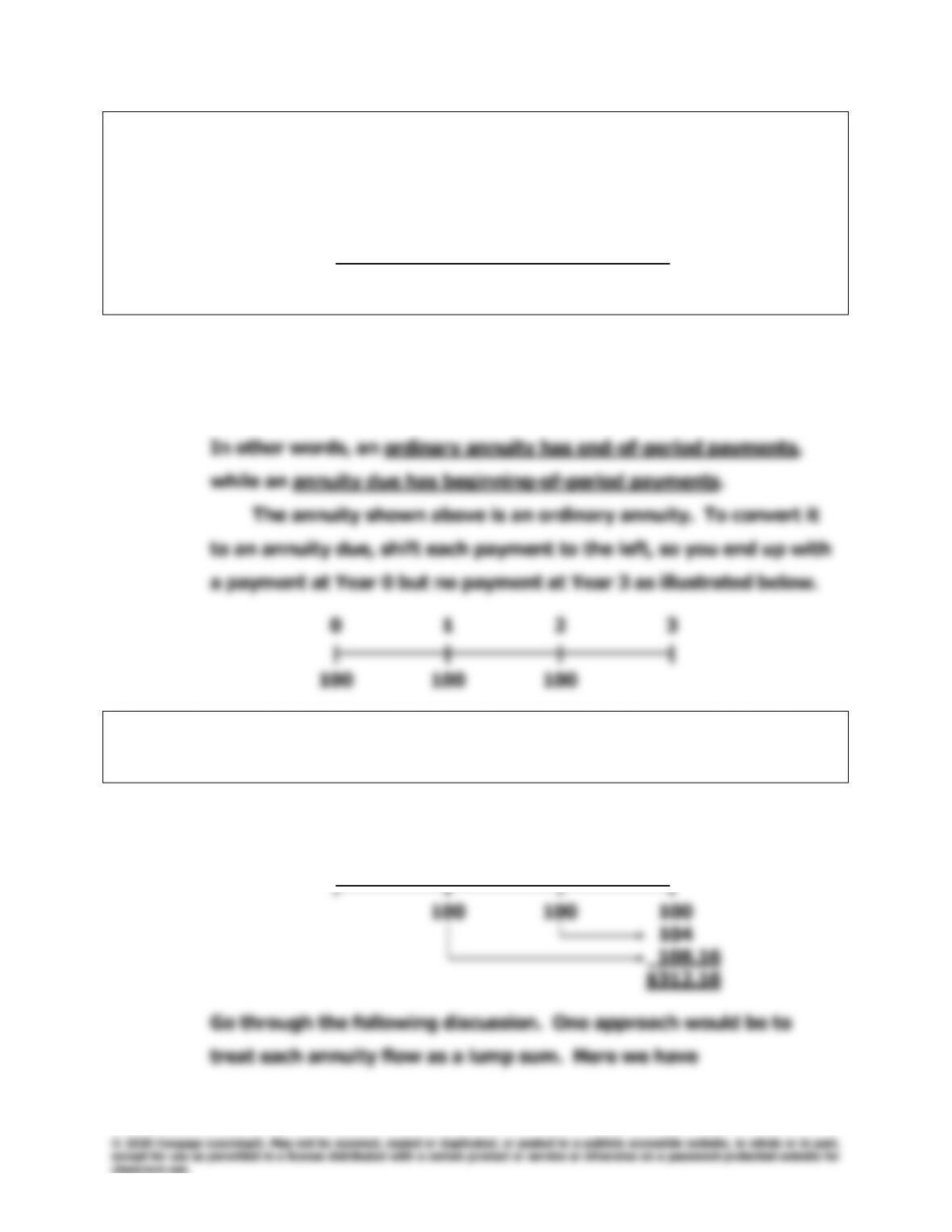

E. What’s the difference between an ordinary annuity and an annuity

due? What type of annuity is shown here? How would you change it

to the other type of annuity?

0 1 2 3

| | | |

0 100 100 100

ANSWER: [Show S5-14 here.] This is an ordinary annuity—it has its payments

at the end of each period; that is, the first payment is made 1 period

from today. Conversely, an annuity due has its first payment today.

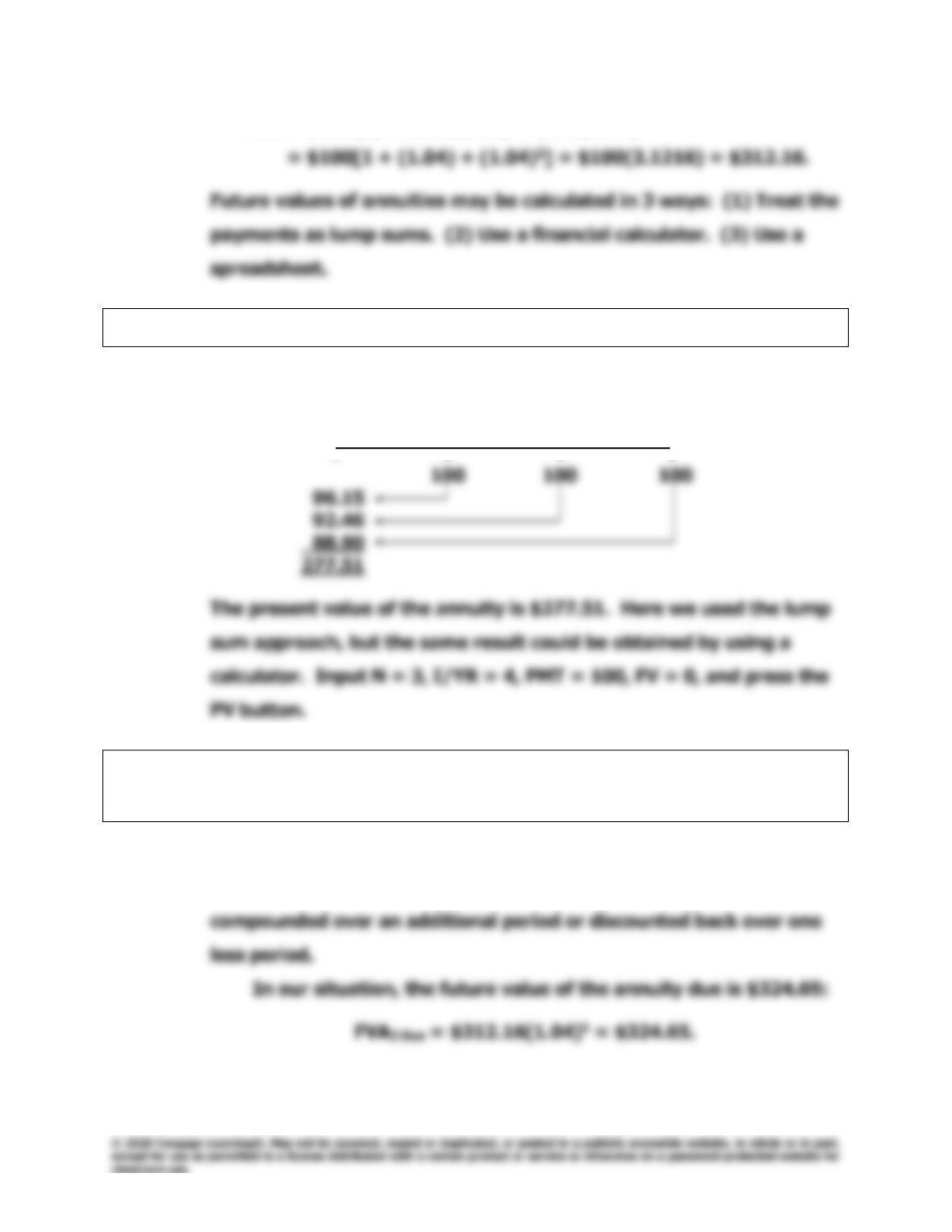

F. (1) What is the future value of a 3-year, $100 ordinary annuity if the

annual interest rate is 4%?

ANSWER: [Show S5-15 here.]

0 1 2 3

| | | |

4%

114

Integrated Case

Chapter 5: Time Value of Money

FVAN = $100(1) + $100(1.04) + $100(1.04)2

F. (2) What is its present value?

ANSWER: [Show S5-16 here.]

0 1 2 3

| | | |

F. (3) What would the future and present values be if it was an annuity

due?

ANSWER: [Show S5-17 and S5–18 here.] If the annuity were an annuity due,

each payment would be shifted to the left, so each payment is

4%

Chapter 5: Time Value of Money

Integrated Case

115

This same result could be obtained by using the time line:

$112.49 + $108.16 + $104.00 = $324.65.

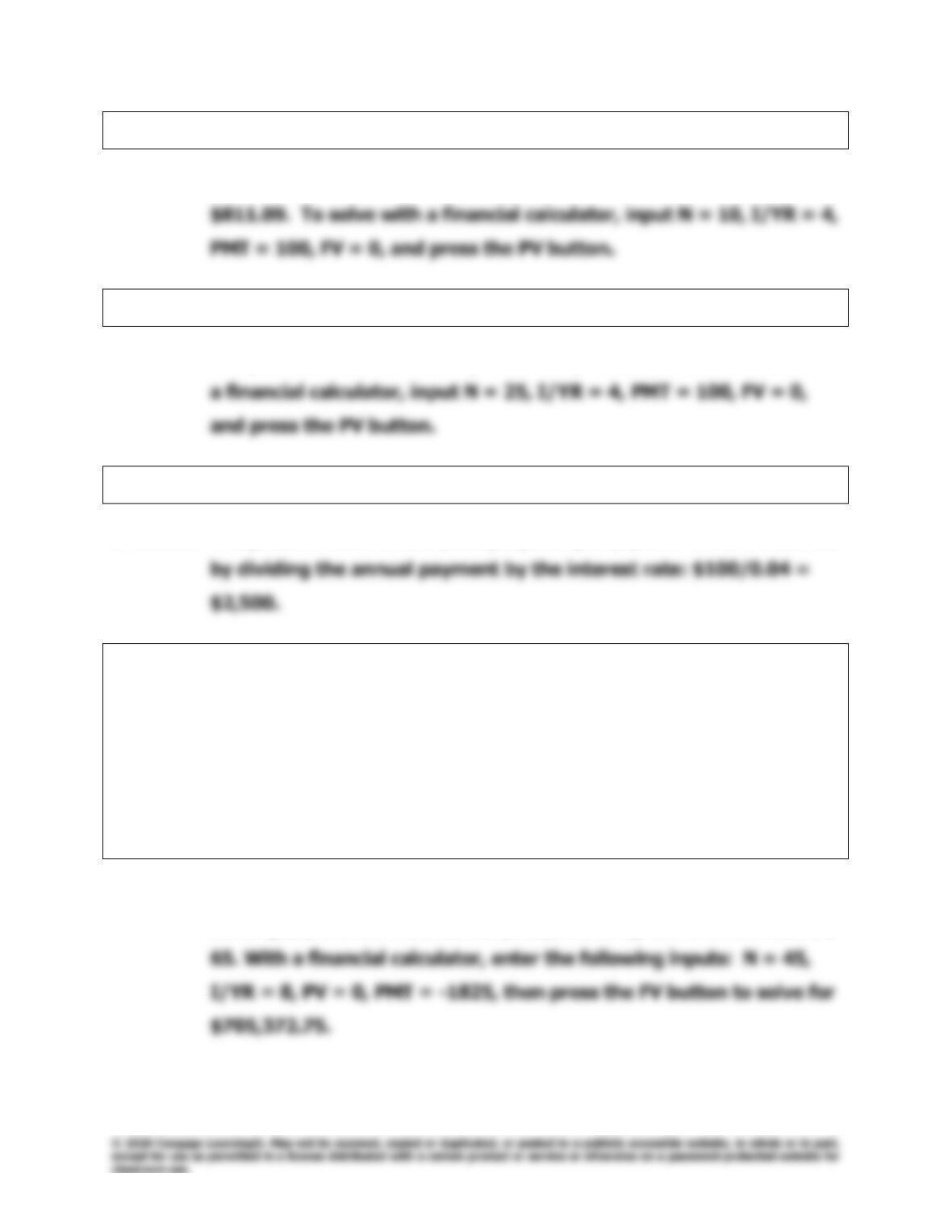

G. A 5-year $100 ordinary annuity has an annual interest rate of 4%.

(1) What is its present value?

ANSWER: [Show S5-19 here.]

0 1 2 3 4 5

| | | | | |

100 100 100 100 100

92.46

85.48

The present value of the annuity is $445.18. Here we used the lump

4%

116

Integrated Case

Chapter 5: Time Value of Money

G. (2) What would the present value be if it was a 10-year annuity?

ANSWER: [Show S5–20 here.] The present value of the 10–year annuity is

G. (3) What would the present value be if it was a 25-year annuity?

ANSWER: The present value of the 25-year annuity is $1,562.21. To solve with

G. (4) What would the present value be if this was a perpetuity?

ANSWER: The present value of the $100 perpetuity is $2,500. The PV is solved

H. A 20-year-old student wants to save $5 a day for her retirement.

Every day she places $5 in a drawer. At the end of each year, she

invests the accumulated savings ($1,825) in a brokerage account

with an expected annual return of 8%.

(1) If she keeps saving in this manner, how much will she have

accumulated at age 65?

ANSWER: [Show S5-21 and S5–22 here.] If she begins saving today, and sticks

to her plan, she will have saved $705,372.75 by the time she reaches

Chapter 5: Time Value of Money

Integrated Case

117

H. (2) If a 40-year-old investor began saving in this manner, how much

would he have at age 65?

ANSWER: [Show S5–23 here.] This question demonstrates the power of

compound interest and the importance of getting started on a regular

H. (3) How much would the 40-year-old investor have to save each year to

accumulate the same amount at 65 as the 20-year-old investor?

ANSWER: [Show S5-24 here.] Again, this question demonstrates the power of

compound interest and the importance of getting started on a

I. What is the present value of the following uneven cash flow stream?

The annual interest rate is 4%.

0 1 2 3 4 Years

| | | | |

0 100 300 300 –50

ANSWER: [Show S5-25 and S5-26 here.] Here we have an uneven cash flow

stream. The most straightforward approach is to find the PVs of each

cash flow and then sum them as shown below:

0 1 2 3 4 Years

| | | | |

Note that the $50 Year 4 outflow remains an outflow even when

discounted. There are numerous ways of finding the present value

of an uneven cash flow stream. But by far the easiest way to deal

with uneven cash flow streams is with a financial calculator.

4%

4%

Chapter 5: Time Value of Money

Integrated Case

119

J. (1) Will the future value be larger or smaller if we compound an initial

amount more often than annually (e.g., semiannually, holding the

stated (nominal) rate constant)? Why?

ANSWER: [Show S5-27 here.] Accounts that pay interest more frequently than

once a year, for example, semiannually, quarterly, or daily, have

J. (2) Define (a) the stated (or quoted or nominal) rate, (b) the periodic

rate, and (c) the effective annual rate (EAR or EFF%).

ANSWER: [Show S5-28 and S5-29 here.] The quoted, or nominal, rate is

merely the quoted percentage rate of return, the periodic rate is the

J. (3) What is the EAR corresponding to a nominal rate of 4% compounded

semiannually? Compounded quarterly? Compounded daily?

ANSWER: [Show S5-30 through S5-32 here.] The effective annual rate for 4%

semiannual compounding, is 4.04%:

120

Integrated Case

Chapter 5: Time Value of Money

If INOM = 4% and interest is compounded semiannually, then:

J. (4) What is the future value of $100 after 3 years under 4% semiannual

compounding? Quarterly compounding?

ANSWER: [Show S5-33 here.] Under semiannual compounding, the $100 is

compounded over 6 semiannual periods at a 2% periodic rate:

INOM = 4%.

Chapter 5: Time Value of Money

Integrated Case

121

K. When will the EAR equal the nominal (quoted) rate?

ANSWER: [Show S5-34 here.] If annual compounding is used, then the

L. (1) What is the value at the end of Year 3 of the following cash flow

stream if interest is 4% compounded semiannually? (Hint: You can

use the EAR and treat the cash flows as an ordinary annuity or use

the periodic rate and compound the cash flows individually.)

0 2 4 6 Periods

| | | | | | |

0 100 100 100

ANSWER: [Show S5-35 through S5-37 here.]

122

Integrated Case

Chapter 5: Time Value of Money

L. (2) What is the PV?

ANSWER: [Show S5-38 here.]

0 2 4 6 Periods

| | | | | | |

100 100 100

L. (3) What would be wrong with your answer to parts (1) and (2) of this

question if you used the nominal rate, 4%, rather than the EAR or

the periodic rate, INOM/2 = 4%/2 = 2% to solve the problems?

ANSWER: INOM can be used in the calculations only when annual compounding

M. (1) Construct an amortization schedule for a $1,000, 4% annual interest

loan with three equal installments.

(2) What is the annual interest expense for the borrower and the annual

interest income for the lender during Year 2?

ANSWER: [Show S5-39 through S5-46 here.] To begin, note that the face

amount of the loan, $1,000, is the present value of a 3-year annuity

at a 4% rate:

2%

Chapter 5: Time Value of Money

Integrated Case

123

0 1 2 3

| | | |

-1,000 PMT PMT PMT

Amortization Schedule:

Beginning Payment of Ending

Period Balance Payment Interest Principal Balance

1 $1,000.00 $360.35 $40.00 $320.35 $679.65

Now make the following points regarding the amortization

schedule:

• The $360.35 annual payment includes both interest and principal.

Interest in the first year is calculated as follows:

4%

124

Integrated Case

Chapter 5: Time Value of Money

• We would continue these steps in the following years.

• Notice that the interest each year declines because the beginning

loan balance is declining. Since the payment is constant, but the

• The interest component is an expense that is deductible to a

business or a homeowner, and it is taxable income to the lender.

If you buy a house, you will get a schedule constructed like ours,

• The payment may have to be increased by a few cents in the final

year to take care of rounding errors and make the final payment

produce a zero ending balance.