Chapter 5: Time Value of Money

Learning Objectives

79

Chapter 5

Time Value of Money

Learning Objectives

After reading this chapter, students should be able to:

◆ Explain how the time value of money works and discuss why it is such an important concept in finance.

◆ Calculate the present value and future value of lump sums.

◆ Identify the different types of annuities, calculate the present value and future value of both an

ordinary annuity and an annuity due, and calculate the relevant annuity payments.

◆ Calculate the present value and future value of an uneven cash flow stream. You will use this

knowledge in later chapters that show how to value common stocks and corporate projects.

◆ Explain the difference between nominal, periodic, and effective interest rates. An understanding of

these concepts is necessary when comparing rates of returns on alternative investments.

◆ Discuss the basics of loan amortization and develop a loan amortization schedule that you might use

when considering an auto loan or home mortgage loan.

Lecture Suggestions

We regard Chapter 5 as the most important chapter in the book, so we spend a good bit of time on it. We

approach time value in three ways. First, we try to get students to understand the basic concepts by use of

time lines and simple logic. Second, we explain how the basic formulas follow the logic set forth in the time

lines. Third, we show how financial calculators and spreadsheets can be used to solve various time value

problems in an efficient manner. Once we have been through the basics, we have students work problems

and become proficient with the calculations and also get an idea about the sensitivity of output, such as

present or future value, to changes in input variables, such as the interest rate or number of payments.

Some instructors prefer to take a strictly analytical approach and have students focus on the

formulas themselves. The argument is made that students treat their calculators as “black boxes,” and that

they do not understand where their answers are coming from or what they mean. We disagree. We think

that our approach shows students the logic behind the calculations as well as alternative approaches, and

because calculators are so efficient, students can actually see the significance of what they are doing better

if they use a calculator. We also think it is important to teach students how to use the type of technology

(calculators and spreadsheets) they must use when they venture out into the real world.

Our research suggests that the best calculator for the money for most students is the HP-10BII.

Finance and accounting majors might be better off with a more powerful calculator, such as the HP-17BII.

We recommend these two for people who do not already have a calculator, but we tell them that any

financial calculator that has an IRR function will do.

We also tell students that it is essential that they work lots of problems, including the end–of–

chapter problems. We emphasize that this chapter is critical, so they should invest the time now to get the

material down. We stress that they simply cannot do well with the material that follows without having this

material down cold. Bond and stock valuation, cost of capital, and capital budgeting make little sense, and

one certainly cannot work problems in these areas, without understanding time value of money first.

We base our lecture on the integrated case. The case goes systematically through the key points

in the chapter, and within a context that helps students see the real world relevance of the material in the

chapter. We ask the students to read the chapter, and also to “look over” the case before class. However,

our class consists of about 1,000 students, many of whom view the lecture on TV, so we cannot count on

them to prepare for class. For this reason, we designed our lectures to be useful to both prepared and

unprepared students.

Since we have easy access to computer projection equipment, we generally use the

PowerPoint

slides as the core of our lectures. We make these slides available to our students, and we strongly suggest

Chapter 5: Time Value of Money

Lecture Suggestions

81

provide an additional example, or the like, we use post-it notes attached at the proper spot. The

advantages of this system are (1) that we have a carefully structured lecture that is easy for us to prepare

DAYS ON CHAPTER: 4 OF 56 DAYS (50-minute periods)

82

Answers and Solutions

Chapter 5: Time Value of Money

Answers to End-of-Chapter Questions

5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk

5-2 True. The second series is an uneven cash flow stream, but it contains an annuity of $400 for 8

5-3 True, because of compounding effects—growth on growth. The following example demonstrates

5-7 The annual percentage rate (APR) is the periodic rate times the number of periods per year. It is

also called the nominal, or stated, rate. With the “Truth in Lending” law, Congress required that

Chapter 5: Time Value of Money

Answers and Solutions

83

Solutions to End-of–Chapter Problems

5-1 0 1 2 3 4 5

| | | | | |

PV = 10,000 FV5 = ?

5-2 0 5 10 15 20

5-3 0 18

5-4 0 N = ?

| |

5-5 0 1 2 N – 2 N – 1 N

| | | • • • | | |

10%

7%

6.5%

12%

I/YR = ?

84

Answers and Solutions

Chapter 5: Time Value of Money

5-6 Ordinary annuity:

0 1 2 3 4 5

| | | | | |

300 300 300 300 300

FVA5 = ?

5-7 0 1 2 3 4 5 6

| | | | | | |

100 100 100 200 300 500

PV = ? FV = ?

5-8 Using a financial calculator, enter the following: N = 60, I/YR = 1, PV = -20000, and FV = 0.

Solve for PMT = $444.89.

7%

8%

Chapter 5: Time Value of Money

Answers and Solutions

85

5-9 a. 0 1

| | $500(1.06) = $530.00.

-500 FV = ?

b. 0 1 2

| | | $500(1.06)2 = $561.80.

-500 FV = ?

c. 0 1

| | $500(1/1.06) = $471.70.

PV = ? 500

d. 0 1 2

| | | $500(1/1.06)2 = $445.00.

PV = ? 500

5-10 a. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | | $500(1.06)10 = $895.42.

-500 FV = ?

b. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | | $500(1.12)10 = $1,552.92.

-500 FV = ?

6%

6%

6%

6%

6%

6%

12%

86

Answers and Solutions

Chapter 5: Time Value of Money

d. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

PV = ? 1,552.90

e. The present value is the value today of a sum of money to be received in the future. For

5-11 a. 2009 2010 2011 2012 2013 2014

| | | | | |

-6 12 (in millions)

5-12 These problems can all be solved using a financial calculator by entering the known values shown

on the time lines and then pressing the I/YR button.

a. 0 1

| |

+700 –749

?

12%

I/YR = ?

Chapter 5: Time Value of Money

Answers and Solutions

87

c. 0 10

| |

+85,000 -201,229

5-13 a. ?

| |

-200 400

100%

5-14 a. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

400 400 400 400 400 400 400 400 400 400

FV = ?

b. 0 1 2 3 4 5

| | | | | |

200 200 200 200 200

FV = ?

I/YR = ?

7%

10%

5%

88

Answers and Solutions

Chapter 5: Time Value of Money

c. 0 1 2 3 4 5

| | | | | |

400 400 400 400 400

FV = ?

d. To solve part d using a financial calculator, repeat the procedures discussed in parts a, b, and c,

but first switch the calculator to “BEG” mode. Make sure you switch the calculator back to “END”

mode after working the problem.

1. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

400 400 400 400 400 400 400 400 400 400 FV = ?

5%

5-15 a. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

PV = ? 400 400 400 400 400 400 400 400 400 400

0%

0%

10%

10%

Chapter 5: Time Value of Money

Answers and Solutions

89

d. 1. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

400 400 400 400 400 400 400 400 400 400

PV = ?

2. 0 1 2 3 4 5

| | | | | |

200 200 200 200 200

PV = ?

3. 0 1 2 3 4 5

| | | | | |

400 400 400 400 400

PV = ?

5-17 0 1 2 3 4 30

| | | | | • • • |

85,000 -8,273.59 -8,273.59 -8,273.59 -8,273.59 -8,273.59

5-18 a. Cash Stream A Cash Stream B

0 1 2 3 4 5 0 1 2 3 4 5

| | | | | | | | | | | |

PV = ? 100 400 400 400 300 PV = ? 300 400 400 400 100

I/YR = ?

10%

5%

0%

8%

8%

90

Answers and Solutions

Chapter 5: Time Value of Money

5-19 a. Begin with a time line:

40 41 64 65

| | • • • | |

5,000 5,000 5,000

FV = ?

b. 40 41 69 70

| | • • • | |

5,000 5,000 5,000

FV = ?

c. 1. 65 66 67 84 85

| | | • • • | |

423,504.48 PMT PMT PMT PMT

2. 70 71 72 84 85

| | | • • • | |

681,537.69 PMT PMT PMT PMT

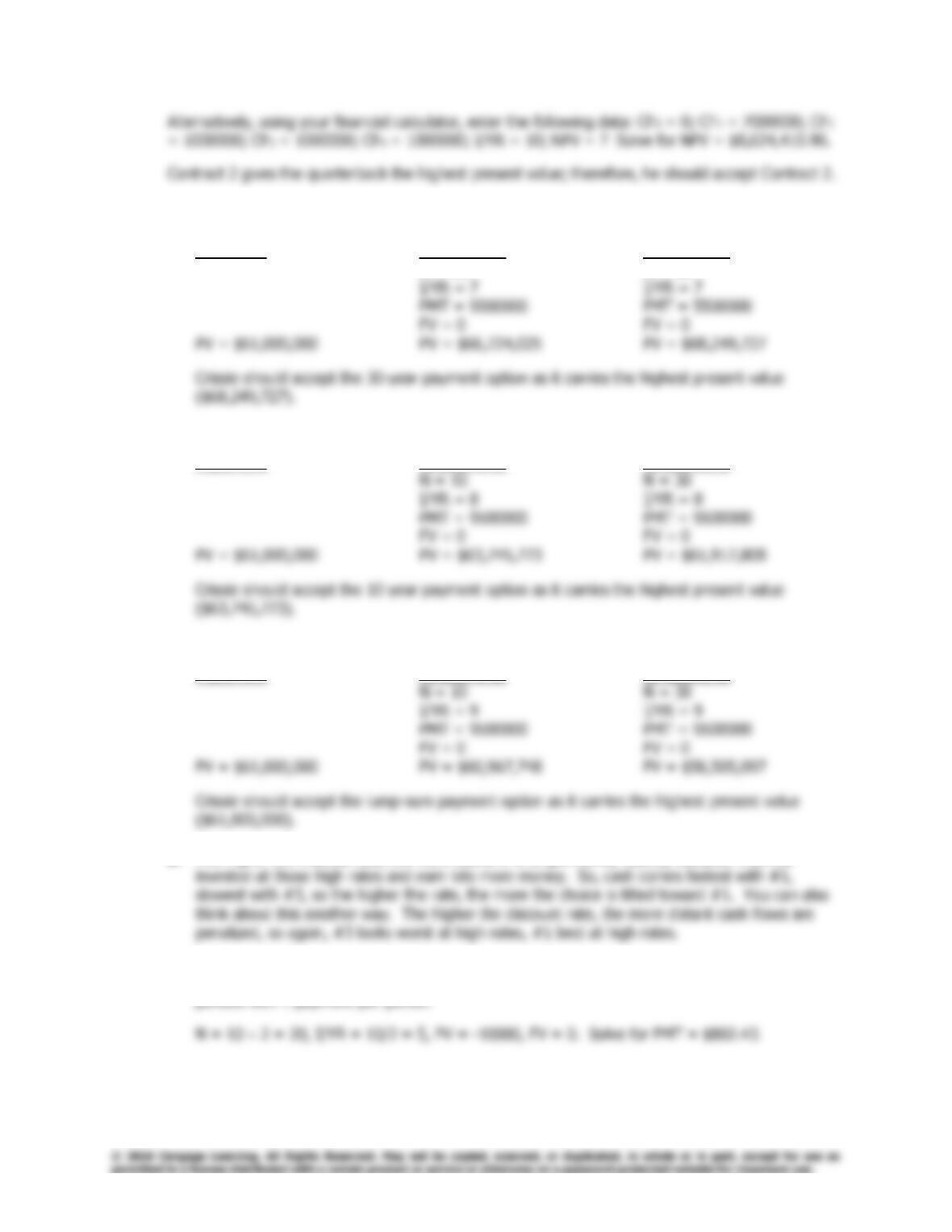

5-20 Contract 1: PV =

432 )10.1(

000,000,3$

)10.1(

000,000,3$

)10.1(

000,000,3$

10.1

000,000,3$ +++

9%

9%

9%

9%

Chapter 5: Time Value of Money

Answers and Solutions

91

5-21 a. If Crissie expects a 7% annual return on her investments:

1 payment 10 payments 30 payments

N = 10 N = 30

b. If Crissie expects an 8% annual return on her investments:

1 payment 10 payments 30 payments

c. If Crissie expects a 9% annual return on her investments:

1 payment 10 payments 30 payments

d. The higher the interest rate, the more useful it is to get money rapidly, because it can be

5-22 a. This can be done with a calculator by specifying an interest rate of 5% per period for 20

92

Answers and Solutions

Chapter 5: Time Value of Money

b. Set up an amortization table:

Beginning Payment of Ending

Period Balance Payment Interest Principal Balance

5-23 a. 0 1 2 3 4 5

| | | | | |

-500 FV = ?

b. 0 1 2 3 4 5 6 7 8 9 10

| | | | | | | | | | |

-500 FV = ?

c. 0 4 8 12 16 20

| | | | | |

-500 FV = ?

1%

12%

6%

3%

Chapter 5: Time Value of Money

Answers and Solutions

93

e. 0 365 1,825

| | • • • |

-500 FV = ?

5-24 a. 0 2 4 6 8 10

| | | | | |

PV = ? 500

b. 0 4 8 12 16 20

| | | | | |

PV = ? 500

c. 0 1 2 12

| | | • • • |

PV = ? 500

6%

3%

1%

0.0329%

94

Answers and Solutions

Chapter 5: Time Value of Money

5-25 a. 0 1 2 3 9 10

| | | | • • • | |

-400 -400 -400 -400 -400

FV = ?

5-26 Using the information given in the problem, you can solve for the maximum car price attainable.

5-27 a. Bank A: INOM = Effective annual rate = 4%.

b. If funds must be left on deposit until the end of the compounding period (1 year for Bank A

6%

Chapter 5: Time Value of Money

Answers and Solutions

95

5-28 Here you want to have an effective annual rate on the credit extended that is 2% more than what

5-30 a. Using the information given in the problem, you can solve for the length of time required to

reach $1 million.

b. Using the 16.043713 year target, you can solve for the required payment:

c. Erika is investing in a relatively safe fund, so there is a good chance that she will achieve her

96

Answers and Solutions

Chapter 5: Time Value of Money

5-31 a. 0 1 2 3 4

| | | | |

PV = ? -10,000 –10,000 -10,000 -10,000

5-32 0 1 2 3 4 5 6

| | | | | | |

1,500 1,500 1,500 1,500 1,500 ?

5-33 Begin with a time line:

0 1 2 3

| | | |

5,000 5,500 6,050

FV = ?

Use a financial calculator to calculate the present value of the cash flows and then determine the

future value of this present value amount:

5%

8%

7%

Chapter 5: Time Value of Money

Answers and Solutions

97

5-34 a. With a financial calculator, enter N = 3, I/YR = 10, PV = -25000, and FV = 0, and solve for

b. % Interest % Principal

Year 1: $2,500/$10,052.87 = 24.87% $7,552.87/$10,052.87 = 75.13%

5-35 a. Using a financial calculator, enter N = 3, I/YR = 7, PV = -90000, and FV = 0, then solve for

c. 30-year amortization with balloon payment at end of Year 3:

Beginning Principal Ending

98

Answers and Solutions

Chapter 5: Time Value of Money

5-36 a. Begin with a time line:

0 1 2 3 4 5 6 6-mos.

0 1 2 3 Years

| | | | | | |

1,000 1,000 1,000 1,000 1,000 FVA = ?

b. Here’s the time line:

0 1 2 3 4 Qtrs

| | | | |

PMT = ? PMT = ? FV = 10,000

5-37 a. Using the information given in the problem, you can solve for the length of time required to

pay off the card.

2%

1%