110

Integrated Case

Chapter 5: Time Value of Money

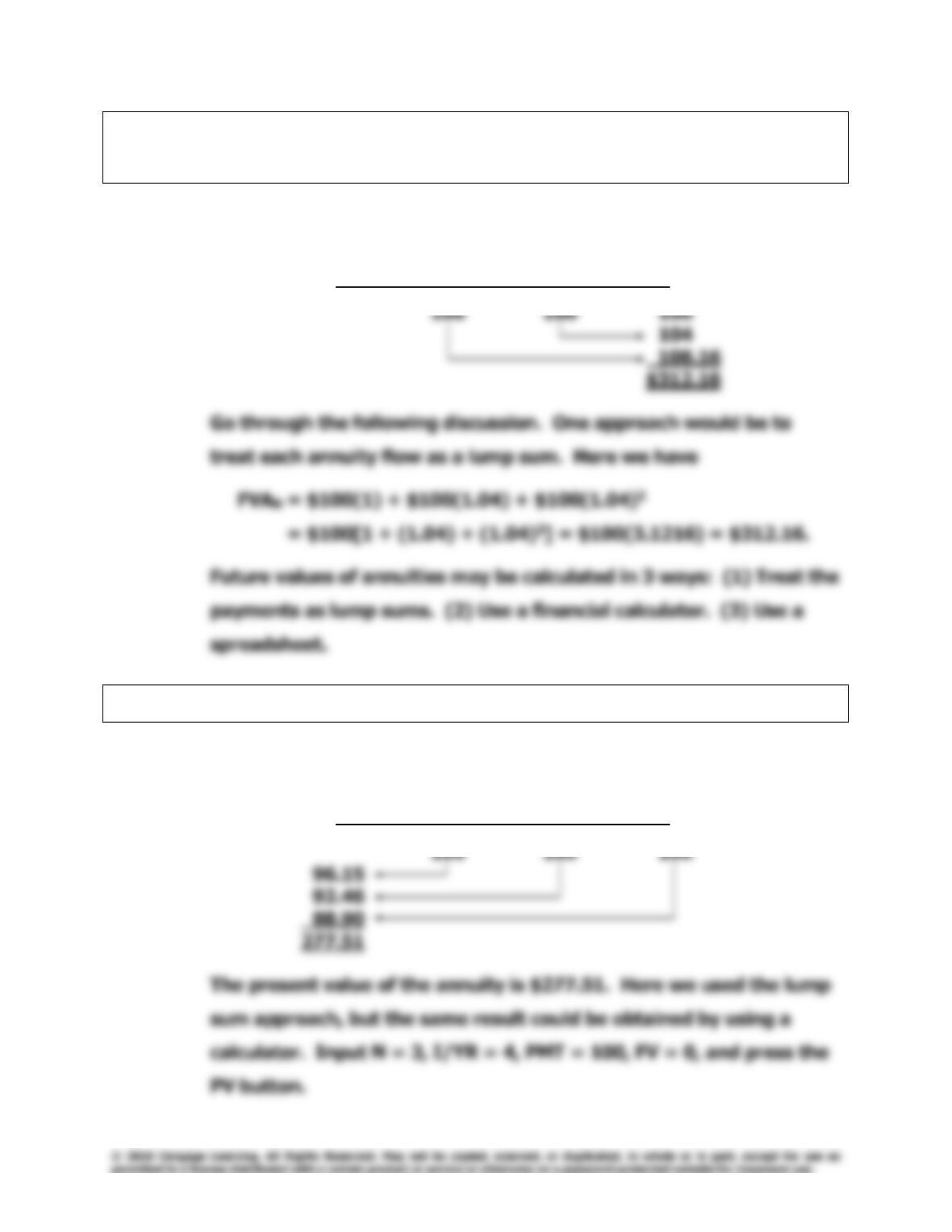

F. (1) What is the future value of a 3-year, $100 ordinary annuity if the

annual interest rate is 4%?

ANSWER: [Show S5–14 here.]

0 1 2 3

| | | |

F. (2) What is its present value?

ANSWER: [Show S5–15 here.]

0 1 2 3

| | | |

4%

4%

Chapter 5: Time Value of Money

Integrated Case

111

F. (3) What would the future and present values be if it was an annuity

due?

ANSWER: [Show S5–16 and S5-17 here.] If the annuity were an annuity due,

each payment would be shifted to the left, so each payment is

compounded over an additional period or discounted back over one

less period.

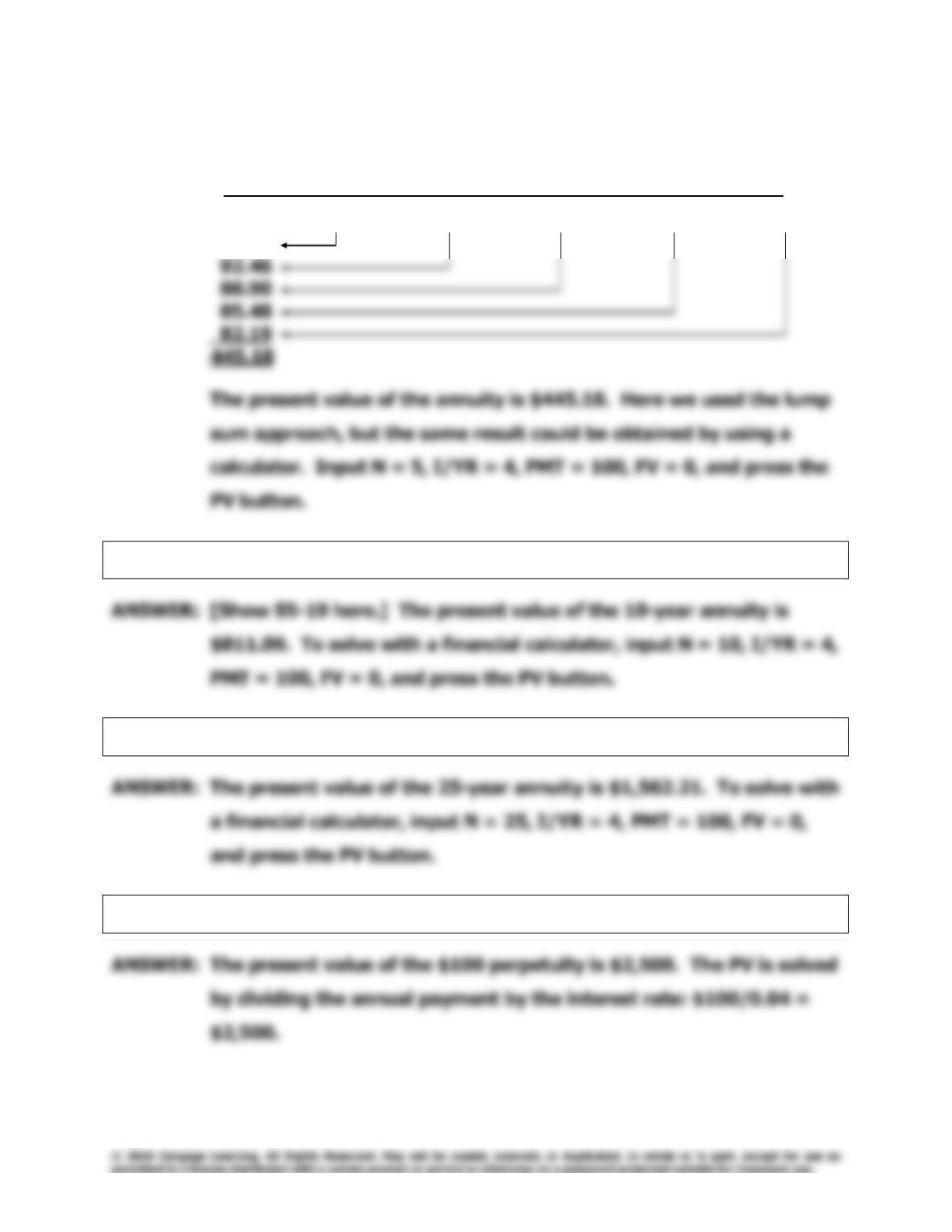

G. A 5-year $100 ordinary annuity has an annual interest rate of 4%.

(1) What is its present value?

112

Integrated Case

Chapter 5: Time Value of Money

ANSWER: [Show S5–18 here.]

0 1 2 3 4 5

| | | | | |

100 100 100 100 100

96.15

G. (2) What would the present value be if it was a 10-year annuity?

G. (3) What would the present value be if it was a 25-year annuity?

G. (4) What would the present value be if this was a perpetuity?

4%

Chapter 5: Time Value of Money

Integrated Case

113

H. A 20-year-old student wants to save $5 a day for her retirement.

Every day she places $5 in a drawer. At the end of each year, she

invests the accumulated savings ($1,825) in a brokerage account

with an expected annual return of 8%.

(1) If she keeps saving in this manner, how much will she have

accumulated at age 65?

ANSWER: [Show S5–20 and S5-21 here.] If she begins saving today, and sticks

H. (2) If a 40-year-old investor began saving in this manner, how much

would he have at age 65?

ANSWER: [Show S5–22 here.] This question demonstrates the power of

H. (3) How much would the 40-year-old investor have to save each year to

accumulate the same amount at 65 as the 20-year-old investor?

ANSWER: [Show S5–23 here.] Again, this question demonstrates the power of

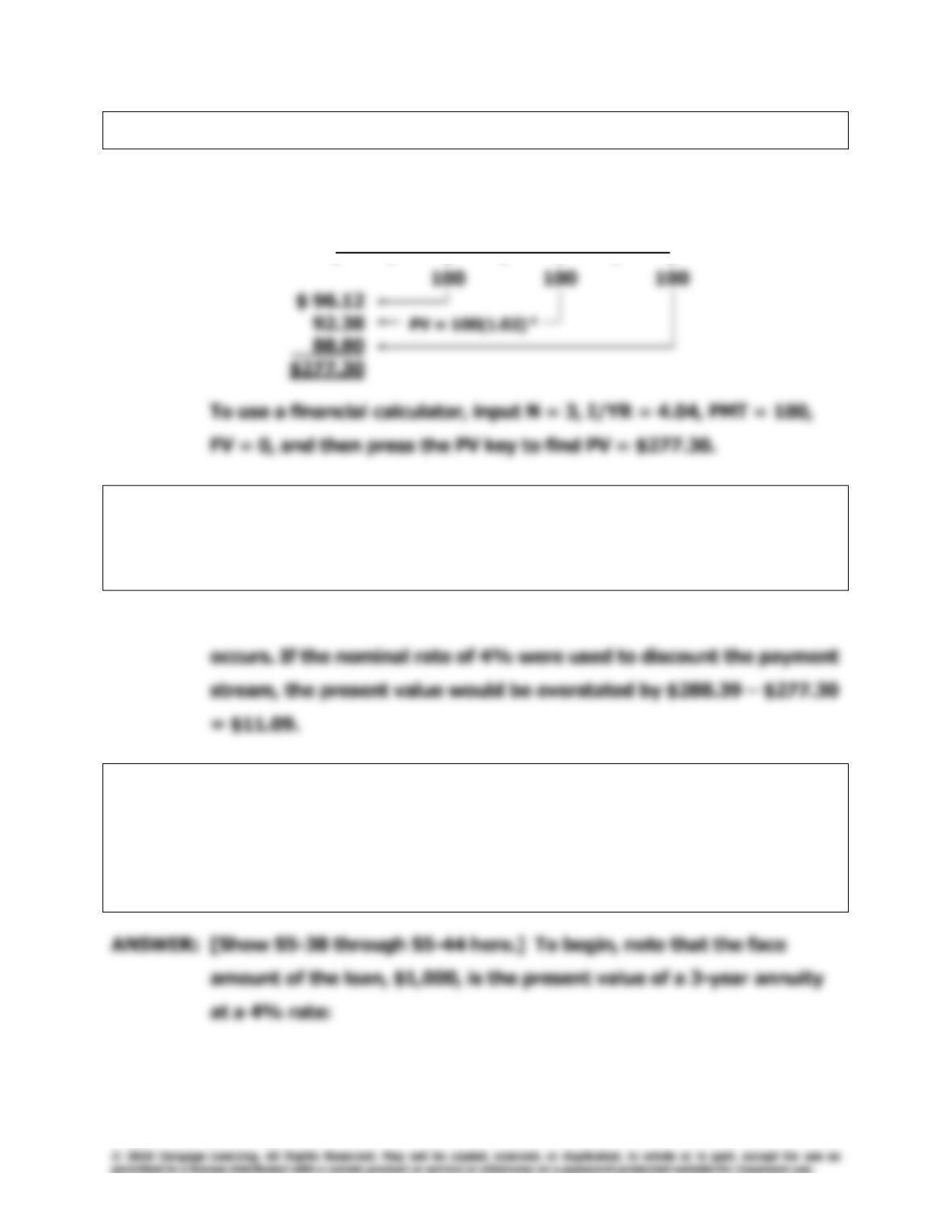

I. What is the present value of the following uneven cash flow stream?

The annual interest rate is 4%.

0 1 2 3 4 Years

| | | | |

0 100 300 300 –50

ANSWER: [Show S5–24 and S5-25 here.] Here we have an uneven cash flow

stream. The most straightforward approach is to find the PVs of each

4%

Chapter 5: Time Value of Money

Integrated Case

115

J. (1) Will the future value be larger or smaller if we compound an initial

amount more often than annually (e.g., semiannually, holding the

stated (nominal) rate constant)? Why?

ANSWER: [Show S5–26 here.] Accounts that pay interest more frequently than

J. (2) Define (a) the stated (or quoted or nominal) rate, (b) the periodic

rate, and (c) the effective annual rate (EAR or EFF%).

J. (3) What is the EAR corresponding to a nominal rate of 4% compounded

semiannually? Compounded quarterly? Compounded daily?

ANSWER: [Show S5–29 through S5-31 here.] The effective annual rate for 4%

116

Integrated Case

Chapter 5: Time Value of Money

J. (4) What is the future value of $100 after 3 years under 4% semiannual

compounding? Quarterly compounding?

ANSWER: [Show S5–32 here.] Under semiannual compounding, the $100 is

Chapter 5: Time Value of Money

Integrated Case

117

K. When will the EAR equal the nominal (quoted) rate?

ANSWER: [Show S5–33 here.] If annual compounding is used, then the

L. (1) What is the value at the end of Year 3 of the following cash flow

stream if interest is 4% compounded semiannually? (Hint: You can

use the EAR and treat the cash flows as an ordinary annuity or use

the periodic rate and compound the cash flows individually.)

0 2 4 6 Periods

| | | | | | |

0 100 100 100

ANSWER: [Show S5–34 through S5-36 here.]

0 2 4 6 Periods

118

Integrated Case

Chapter 5: Time Value of Money

L. (2) What is the PV?

ANSWER: [Show S5–37 here.]

0 2 4 6 Periods

| | | | | | |

L. (3) What would be wrong with your answer to parts L(1) and L(2) if you

used the nominal rate, 4%, rather than the EAR or the periodic rate,

INOM/2 = 4%/2 = 2% to solve the problems?

ANSWER: INOM can be used in the calculations only when annual compounding

M. (1) Construct an amortization schedule for a $1,000, 4% annual interest

loan with three equal installments.

(2) What is the annual interest expense for the borrower and the annual

interest income for the lender during Year 2?

2%

Chapter 5: Time Value of Money

Integrated Case

119

Amortization Schedule:

Beginning Payment of Ending

Period Balance Payment Interest Principal Balance

Now make the following points regarding the amortization

schedule:

120

Integrated Case

Chapter 5: Time Value of Money

• Notice that the interest each year declines because the beginning