1

2

3

4

5

6

7

8

9

10

11

12

13

14

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

56

57

58

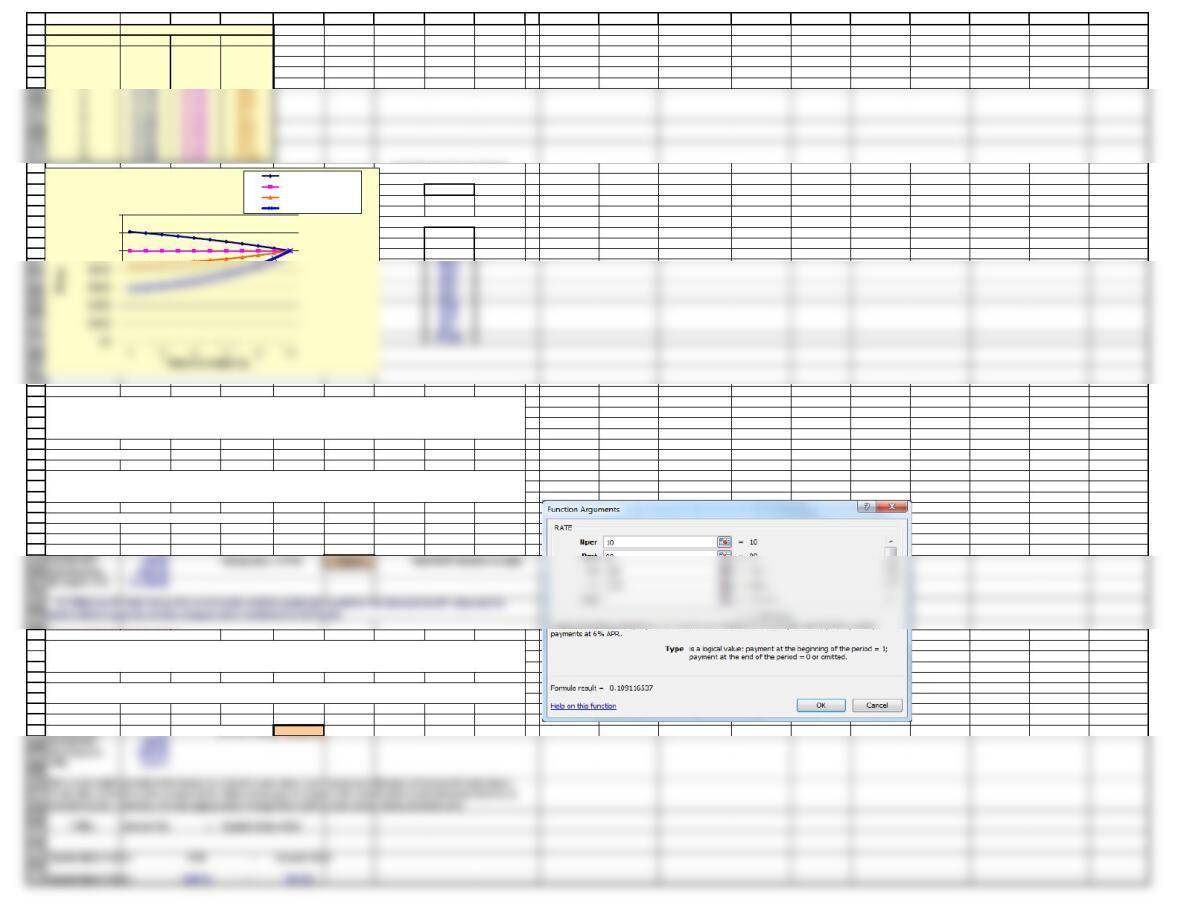

The easiest way to solve this problem is to use Excel’s PV function. Click fx, then financial, then PV. Then fill in the

menu items as shown in our snapshot in the screen shown just below.

59

60

61

62

63

64

65

66

67

68

69

70

74

75

76

77

78

data table to show the bond’s value at a range of rates, i.e., to show the bond’s sensitivity to changes in interest

rates. This is done below.

A B C D E F G H I J K L M N O P Q R S T

12/9/2012

Situation

Finding the “Fair Value” of a Bond

First, we list the key features of the bond as “model inputs”:

Years to Mat: 10

Coupon rate: 10%

Annual Pmt: $100

Par value = FV: $1,000

Going rate, rd:10%

Value of bond = $1,000.00

complete the operation and get the table.

Chapter 5. Mini Case

Sam Strother and Shawna Tibbs are vice-presidents of Mutual of Seattle Insurance Company and co-directors of the

company’s pension fund management division. A major new client, the Northwestern Municipal Alliance, has

requested that Mutual of Seattle present an investment seminar to the mayors of the represented cities, and Strother

and Tibbs, who will make the actual presentation, have asked you to help them by answering the following

questions. Because the Boeing Company operates in one of the league’s cities, you are to work Boeing into the

presentation.

a. What are the key features of a bond? Answer: See Chapter 5 Mini Case Show

d. How is the value of a bond determined? What is the value of a 10-year, $1,000 par value bond with a 10 percent

annual coupon if its required rate of return is 10 percent?

Thus, this bond sells at its par value. That situation always exists if the going rate is

equal to the coupon rate.

The PV function can only be used if the payments are constant, but that is normally the case for bonds.

b. What are call provisions and sinking fund provisions? Do these provisions make bonds more or less risky?

e. (1.) What would be the value of the bond described in Part d if, just after it had been issued, the expected inflation

rate rose by 3 percentage points, causing investors to require a 13 percent return? Would we now have a discount

or a premium bond?

We could simply go to the input data section shown above, change the value for r from 10% to 13%. You can set up a

15

16

17

18

19

20

23

24

25

c. How is the value of any asset whose value is based on expected future cash flows determined? Answer: See

A call provision that allows the issuer to redeem the bond at a specified time before the maturity date. If interest

rates fall, the issuer can refund the bonds and issue new bonds at a lower rate. Because of this, borrowers are

willing to pay more and lenders require more on callable bonds.

In a sinking fund provision, the issuer pays off the loan over its life rather than all at the maturity date. A sinking

fund reduces the risk to the investor and shortens the maturity. This is not good for investors if rates fall after

79

80

81

82

83

84

85

86

A B C D E F G H I J K L M N O P Q R S T

To make the data table, first type the headings, then type the rates in

cells in the left column. Since the input values are listed down a column,

type the formula in the row above the first value and one cell to the right

of the column of values (this is B73; note that the formula in B73 actually

just refers to the bond pricing formula above in B60). Select the range of

cells that contains the formulas and values you want to substitute

(A73:B78). Then click Data, What-If-Analysis, and then Data Table to get

the menu. The input data are in a column, so put the cursor on “column

input cell” and enter the cell with the value for r (B37), then Click OK to

complete the operation and get the table.

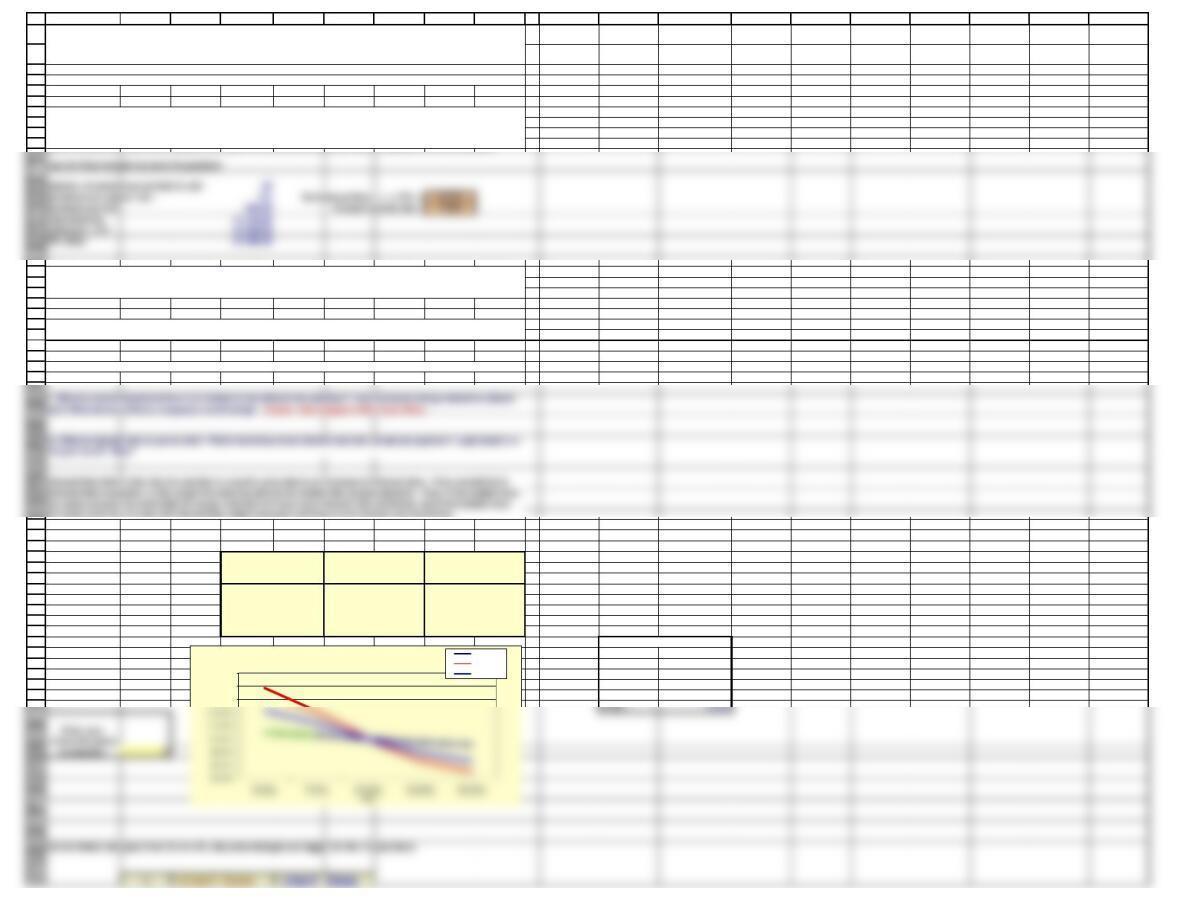

We can use the data table to construct a graph that

shows the bond’s sensitivity to changing rates.

$2,500

Interest Rate Sensitivity of a 10-Year Bond

Value at 7%

Value at 13%

87

88

89

90

91

92

93

94

95

96

97

99

100

101

102

103

104

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

$640

$667

$701

$741

$789

$847

$917

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

Annual Pmt: $90.00 Going rate, r =YTM: 10.91% See RATE function at right.

Current price: $887.00

Par value = FV: $1,000.00

(2.) What are the total return, the current yield, and the capital gains yield for the discount bond? (Assume the

bond is held to maturity and the company does not default on the bond.)

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

Annual Pmt: $90.00

Current price: $887.00

Current Yield

Capital Gains Yield = YTM – Current Yield

Capital Gains Yield = 10.91% – 10.15%

The current yield provides information on a bond‘s cash return, but it gives no indication of the bond’s total return.

To see this, consider a zero coupon bond. Since zeros pay no coupon, the current yield is zero because there is no

interest income. However, the zero appreciates through time, and its total return clearly exceeds zero.

A B C D E F G H I J K L M N O P Q R S T

N7% 10% 13%

0$1,211 $1,000 $837

1$1,195 $1,000 $846

2$1,179 $1,000 $856

3$1,162 $1,000 $867

You pick the rate for a bond:

Your choice:

20%

Resulting bond prices

$581

$597

$616

Yield to Maturity (YTM)

Use the Rate function to solve the problem.

Years to Mat: 10

Coupon rate: 9%

Current and Capital Gains Yields

Par value $1,000.00

Coupon rate: 9%

Current Yield =

10.15%

f. (1.) What is the yield to maturity on a 10-year, 9 percent annual coupon, $1,000 par value bond that sells for

$887.00? That sells for $1,134.20? What does the fact that a bond sells at a discount or at a premium tell you about

the relationship between rd and the bond’s coupon rate? What is the yield-to-maturity of the bond?

The current yield is the annual interest payment divided by the bond’s current price. The current yield provides

information regarding the amount of cash income that a bond will generate in a given year. However, it does not

account for any capital gains or losses that will be realized if the bond is held to maturity or call.

Simply divide the annual interest payment by the price of the bond. Even if the bond made semiannual payments,

we would still use the annual interest.

If rates fall, the bond goes to a premium, but it moves towards par as maturity approaches. The reverse hold if rates

rise and the bond sells at a discount. If the going rate remains equal to the coupon rate, the bond will continue to

sell at par. Note that the above graph assumes that interest rates stay constant after the initial change. That is most

unlikely–interest rates fluctuate, and so do the prices of outstanding bonds.

Value of Bond in Given Year:

$1,000

$1,200

$1,400

Value of the bond over time Rates fall to 7%

Rates stay the same

Rates increase to 13%

Your choice

105

106

107

108

109

110

111

4$1,143 $1,000 $880

5$1,123 $1,000 $894

6$1,102 $1,000 $911

7$1,079 $1,000 $929

8$1,054 $1,000 $950

9$1,028 $1,000 $973

180

181

182

183

184

185

186

187

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

Value of bond = $83.4737 or $834.74

Settlement (today) 3/25/2014

Maturity 12/31/2023

Coupon rate 10.00%

Going rate, r 13.00%

Redemption (par value) 100

Frequency (for semiannual) 2

the correct price. See the example below.

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

Accrued interest = $2.3333 or $23.33

Suppose the bond’s price is $1,150. You can also calculate the yield using the YIELD function, as shown below.

Curent price 1,150.00$

Settlement (today) 1/1/2014

Maturity 12/31/2023

Coupon rate 10.00%

Redemption (par value) 100

Frequency (for semiannual) 2

Basis (360 or 365 day year) 0

A B C D E F G H I J K L M N O P Q R S T

Capital Gains Yield = 0.76%

Bonds with Semiannual Coupons

Excel Bond Functions

Suppose today’s date is January 1, 2014, and the bond matures on December 31, 2023

Settlement (today) 1/1/2014

Maturity 12/31/2023

Coupon rate 10.00%

Going rate, r 13.00%

Redemption (par value) 100

Frequency (for semiannual) 2

Basis (360 or 365 day year) 0

Basis (360 or 365 day year) 0

Value of bond = $83.6307 or $836.31

Issue date 1/1/2014

First interest date 6/30/2014

Settlement (today) 3/25/2014

Maturity 12/31/2023

Coupon rate 10.00%

Going rate, r 13.00%

Redemption (par value) 100

Frequency (for semiannual) 2

Basis (360 or 365 day year) 0

This is the value of the bond, but it does not include the accrued interest you would pay. The ACCRINT function will

calculate accrued interest, as shown below.

g. How does the equation for valuing a bond change if semiannual payments are made? Find the value of a 10-year,

semiannual payment, 10 percent coupon bond if nominal rd = 13%.

188

189

190

191

192

193

194

195

196

197

198

199

200

Periods to maturity = 10*2 = 20

Coupon rate: 10%

Semiannual pmt = $100/2 = $50.00 PV = $834.72

Future Value: $1,000.00

Periodic rate = 13%/2 = 6.5%

Note that the bond is now more valuable, because interest payments come in faster.

three modifications to our original valuation model: (1) divide the coupon payment by 2, (2) multiply the years to

maturity by 2, and (3) divide the nominal interest rate by 2.

Use the Rate function with adjusted data to solve the problem.

260

261

262

263

264

265

266

267

268

269

280

281

282

283

284

285

286

287

288

289

290

291

292

293

294

295

296

297

298

299

300

301

302

303

Interest Rate Risk is the risk of a decline in a bond’s price due to an increase in interest rates. Price sensitivity to

interest rates is greater (1) the longer the maturity and (2) the smaller the coupon payment. Thus, if two bonds have

the same coupon, the bond with the longer maturity will have more interest rate sensitivity, and if two bonds have

m. What is interest rate (or price) risk? Which bond has more interest rate risk, an annual payment 1-year bond or a

10-year bond? Why?

l. What is a bond spread and how is it related to the default risk premium? How are bond ratings related to default

304

305

306

307

308

309

310

311

312

313

314

315

316

317

318

319

320

321

322

324

325

326

327

328

329

330

331

332

333

334

335

336

337

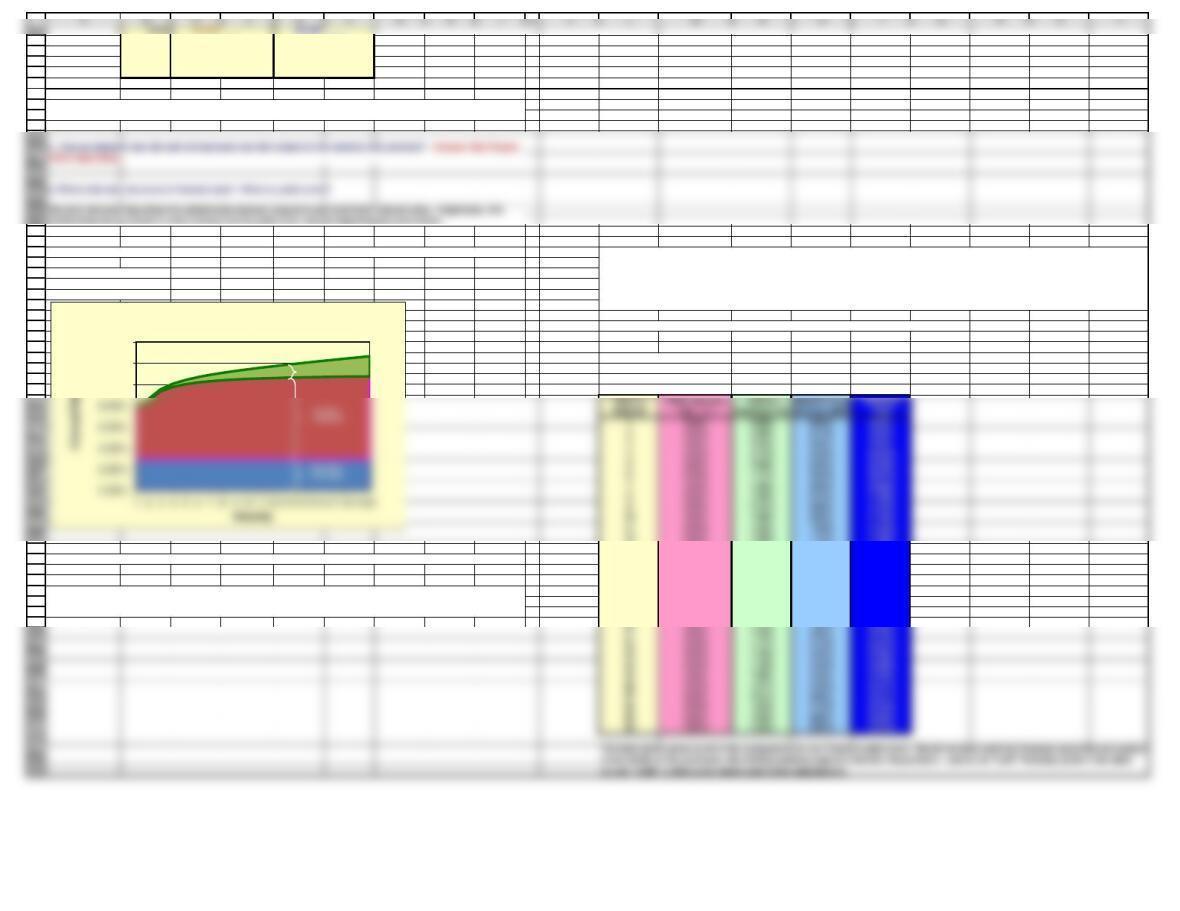

As the interst rate goes from 5% to 15%, the price changes are bigger for the 10-year bond.

A B C D E F G H I J K L M N O P Q R S T

Yield to Call

Your Choice of Maturity

Years to Mat: 10 Rate Price Rate Price Rate Price

Coupon rate: 10% $966.65 $946.77 $991.88

Annual Pmt: $100.00 5.0% 1,216.47 5.0% $1,386.09 5.0% $1,047.62

Current price: $946.77 7.0% 1,123.01 7.0% $1,210.71 7.0% $1,028.04

Par value = FV: $1,000.00 10.0% 1,000.00 10.0% $1,000.00 10.0% $1,000.00

YTM = 10.9% 13.0% 894.48 13.0% $837.21 13.0% $973.45

15.0% 832.39 15.0% $749.06 15.0% $956.52

Years to Mat: 1Scratch sheet for Your Choice

Coupon rate: 10% Years to Mat: 5

Annual Pmt: $100.00 Coupon rate: 10%

Current price: $991.88 Annual Pmt: $100.00

Par value = FV: $1,000.00

Current price:

$966.65

YTM = 10.9%

Par value = FV:

$1,000.00

the same maturity, the one with the smaller coupon payment will have more interest rate sensitivity.

h. Suppose a 10-year, 10 percent, semiannual coupon bond with a par value of $1,000 is currently selling for

$1,135.90, producing a nominal yield to maturity of 8 percent. However, the bond can be called after 5 years for a

price of $1,050.

(1.) What is the bond‘s nominal yield to call (YTC)?

(2.) If you bought this bond, do you think you would be more likely to earn the YTM or the YTC? Why?

k. Describe a way to estimate the inflation premium (IP) for a T-Year bond. Answer: See Chapter 5 Mini Case Show.

1-Yr Maturity

10-Yr Maturity

The yield to call is the rate of return investors will receive if their bonds are called. If the issuer has the right to call

the bonds, and if interest rates fall, then it would be logical for the issuer to call the bonds and replace them with

new bonds that carry a lower coupon. The yield to call (YTC) is found similarly to the YTM. The same formula is

used, but years to maturity is replaced with years to call, and the maturity value is replaced with the call price.

i. Write a general expression for the yield on any debt security (rd) and define these terms: real risk-free rate of

interest (r*), inflation premium (IP), default risk premium (DRP), liquidity premium (LP), and maturity risk premium

(MRP). Answer: See Chapter 5 Mini Case Show.

j. Define the nominal risk-free rate (rRF). What security can be used as an estimate of rRF? Answer: See Chapter 5

Mini Case Show.

$1,300.00

$1,400.00

$1,500.00

10 Yr. versus 1 Yr.

Your Choice

270

271

272

273

274

275

276

277

278

279

Use the Rate function to solve the problem.

Number of semiannual periods to call: 10

Seminannual coupon rate: 5% Semiannual Rate = I = YTC = 3.77%

Seminannual Pmt: $50.00 Annual nominal rate = 7.53%

Current price: $1,135.90

Call price = FV $1,050.00

Par value $1,000.00

340

341

342

343

344

345

346

347

348

349

350

351

352

353

354

355

356

357

o. How are interest rate risk and reinvestment rate risk related to the maturity risk premium? Answer: See Chapter

5 Mini Case Show.

358

359

360

361

362

363

364

365

366

367

368

369

370

371

372

373

374

375

376

378

379

380

381

382

383

384

385

386

10 3.00% 7.50% 0.90% 11.40%

11 3.00% 7.55% 1.00% 11.55%

387

388

389

390

391

392

393

394

395

396

397

398

399

400

401

402

403

404

405

406

407

408

409

21 3.00% 7.76% 2.00% 12.76%

22 3.00% 7.77% 2.10% 12.87%

23 3.00% 7.78% 2.20% 12.98%

24 3.00% 7.79% 2.30% 13.09%

25 3.00% 7.80% 2.40% 13.20%

26 3.00% 7.81% 2.50% 13.31%

27 3.00% 7.81% 2.60% 13.41%

28 3.00% 7.82% 2.70% 13.52%

29 3.00% 7.83% 2.80% 13.63%

we can “build” a yield curve based upon these expectations.

4.8% 38.6%

10.0% $1,000 $1,000

4.5% 33.5%

15.0% $957 $749

Hypothetical Inputs See to right for actual date used in graph.

Real risk free rate 3.00%

Expected inflation of 5% for the next 1 years.

Expected inflation of 6% for the next 1 years.

Expected inflation of 8% thereafter.

Now, we want to set up a table that encompasses all of the information for our yield curve.

INPUT DATA

Real risk free rate 3.00%

Expected inflation of 5% for the next 1 years.

Expected inflation of 6% for the next 1 years.

Expected inflation of 8% thereafter.

12 3.00% 7.58% 1.10% 11.68%

13 3.00% 7.62% 1.20% 11.82%

The yield is upward sloping due to increasing expected inflation and an increasing maturity risk premium 14 3.00% 7.64% 1.30% 11.94%

15 3.00% 7.67% 1.40% 12.07%

16 3.00% 7.69% 1.50% 12.19%

17 3.00% 7.71% 1.60% 12.31%

18 3.00% 7.72% 1.70% 12.42%

19 3.00% 7.74% 1.80% 12.54%

20 3.00% 7.75% 1.90% 12.65%

Suppose most investors expect the inflation rate to be 5 percent next year, 6 percent the following year, and 8 percent thereafter. The

real risk-free rate is 3 percent. The maturity risk premium is zero for securities that mature in 1 year or less, 0.1 percent for 2-year

securities, and then the MRP increases by 0.1 percent per year thereafter for 20 years, after which it is stable. What is the interest

rate on 1-year, 10-year, and 20-year Treasury securities? Draw a yield curve with these data. What factors can explain why this

constructed yield curve is upward sloping?

n. What is reinvestment rate risk? Which has more reinvestment rate risk, a 1-year bond or a 10-year bond?

Answer: See Chapter 5 Mini Case Show.

q. Briefly describe bankruptcy law. If a firm were to default on the bonds, would the company be immediately

liquidated? Would the bondholders be assured of receiving all of their promised payments? Answer: See Chapter 5

Mini Case Show.

10.00%

12.00%

14.00%

Hypothetical Treasury Yield Curve

MRP

339