Chapter 5: Time Value of Money

Answers and Solutions

101

4. He wants to withdraw, or have payments of, $74,012.21 per year for 25 years, with the first

payment made at the beginning of the first retirement year. So, we have a 25-year annuity

5. Since the original $90,000, which grows to $194,303.25, will be available, we must save

enough to accumulate $853,268.88 – $194,303.25 = $658,965.63.

So, the time line looks like this:

6. The $658,965.63 is the FV of a 10-year ordinary annuity. The payments will be deposited in

5-40 Step 1: Determine the annual cost of college. The current cost is $12,000 per year, but that is

escalating at a 6% inflation rate:

College Current Years Inflation Cash

Year Cost from Now Adjustment Required

1 $12,000 5 (1.06)5 $16,058.71

Now put these costs on a time line:

13 14 15 16 17 18 19 20 21

| | | | | | | | |

-16,059 –17,022 –18,044 –19,126

Chapter 5: Time Value of Money

Comprehensive/Spreadsheet Problem

103

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

5-41 a.

I = 10%

b.

c.

d.

e.

Inputs: PV = $1,000

Years (D11)

1,610.51$ 0% 5% 20%

0$1,000.00 $1,000.00 $1,000.00

Interest Rate (D10)

Inputs: FV = $1,000

I = 10%

Inputs: PV = –$1,000

FV = $2,000

Inputs: PV = –36.5

FV = 73

f.

h.

i.

PMT: Use function wizard (PMT) PMT = $149.03

j.

Inputs: PMT (1,000)$

N 5

I15%

PV: Use function wizard (PV) PV = $3,352.16

Inputs: N 10

Year Payment

1100

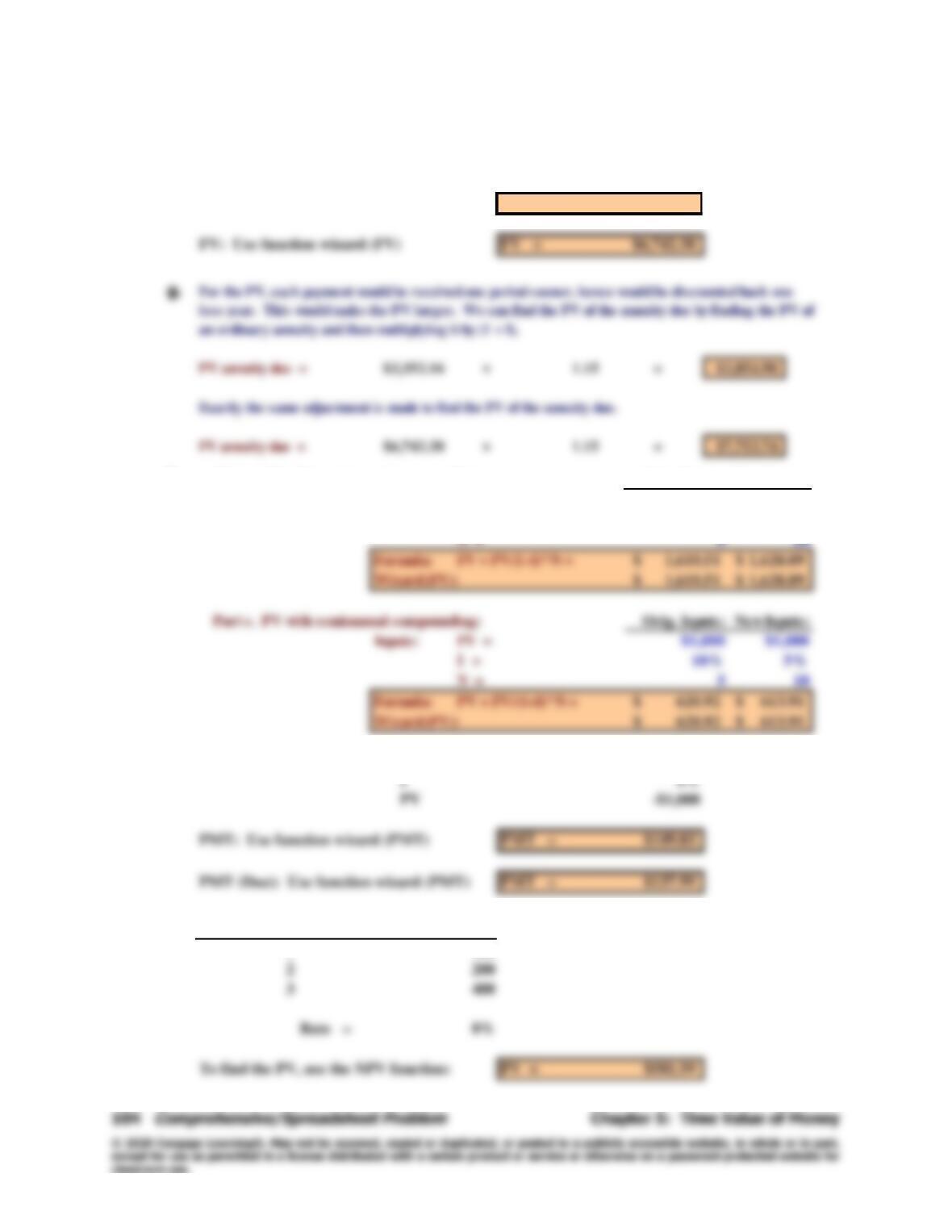

Part a. FV with semiannual compounding: Orig. Inputs: New Inputs:

Inputs: PV = $1,000 $1,000

I = 10% 5%

Chapter 5: Time Value of Money

Comprehensive/Spreadsheet Problem

105

Excel does not have a function for the sum of the future values for a set of uneven payments. Therefore,

we must find this FV by some other method. Probably the easiest procedure is to simply compound each

k.

5 banks offer nominal rates of 6% , but differ in their compounding frequency.

A = annually; B = semiannually; C = quarterly; D = monthly; and E = daily.

I NOM 6%

Deposit $5,000

(1) A B C D E

(i) EAR 6.00% 6.09% 6.14% 6.17% 6.18%

(2) Would they be equally able to attract funds? No. People would prefer more compounding to less.

(i) What nominal rate would cause all banks to provide same EAR as Bank A?

(3) You need $5,000 at the end of the year. How much do you need to deposit annually for A,

semiannually, for B, etc. beginning today, to have $5,000 at the end of the year?

An alternative procedure for finding the FV would be to find the PV of the series using the NPV

function, then compound that amount for 3 years at 8% , as is done below:

106

Comprehensive/Spreadsheet Problem

Chapter 5: Time Value of Money

l.

Original amount of mortgage: $15,000

Term to maturity: 4

Interest rate: 8%

Chapter 5: Time Value of Money

Integrated Case

107

Integrated Case

5-42

First National Bank

Time Value of Money Analysis

You have applied for a job with a local bank. As part of its evaluation process,

you must take an examination on time value of money analysis covering the

following questions.

A. Draw time lines for (1) a $100 lump sum cash flow at the end of

Year 2; (2) an ordinary annuity of $100 per year for 3 years; and (3)

an uneven cash flow stream of –$50, $100, $75, and $50 at the end

of Years 0 through 3.

ANSWER: [Show S5-1 through S5-5 here.] A time line is a graphical

representation that is used to show the timing of cash flows. The

tick marks represent end of periods (often years), so Time 0 is today;

108

Integrated Case

Chapter 5: Time Value of Money

An annuity is a series of equal cash flows occurring over equal

intervals, as illustrated in the middle time line.

B. (1) What’s the future value of $100 after 3 years if it earns 4%, annual

compounding?

ANSWER: [Show S5-6 through S5-8 here.] Show dollars corresponding to

question mark, calculated as follows:

0 1 2 3

| | | |

100 FV = ?

After 1 year:

4%

Chapter 5: Time Value of Money

Integrated Case

109

Note that this equation has 4 variables: FVN, PV, I/YR, and N. Here,

we know all except FVN, so we solve for FVN. We will, however, often

• Regular calculator:

1. $100(1.04)(1.04)(1.04) = $112.49.

• Financial calculator:

This is especially efficient for more complex problems, including

110

Integrated Case

Chapter 5: Time Value of Money

B. (2) What’s the present value of $100 to be received in 3 years if the

interest rate is 4%, annual compounding?

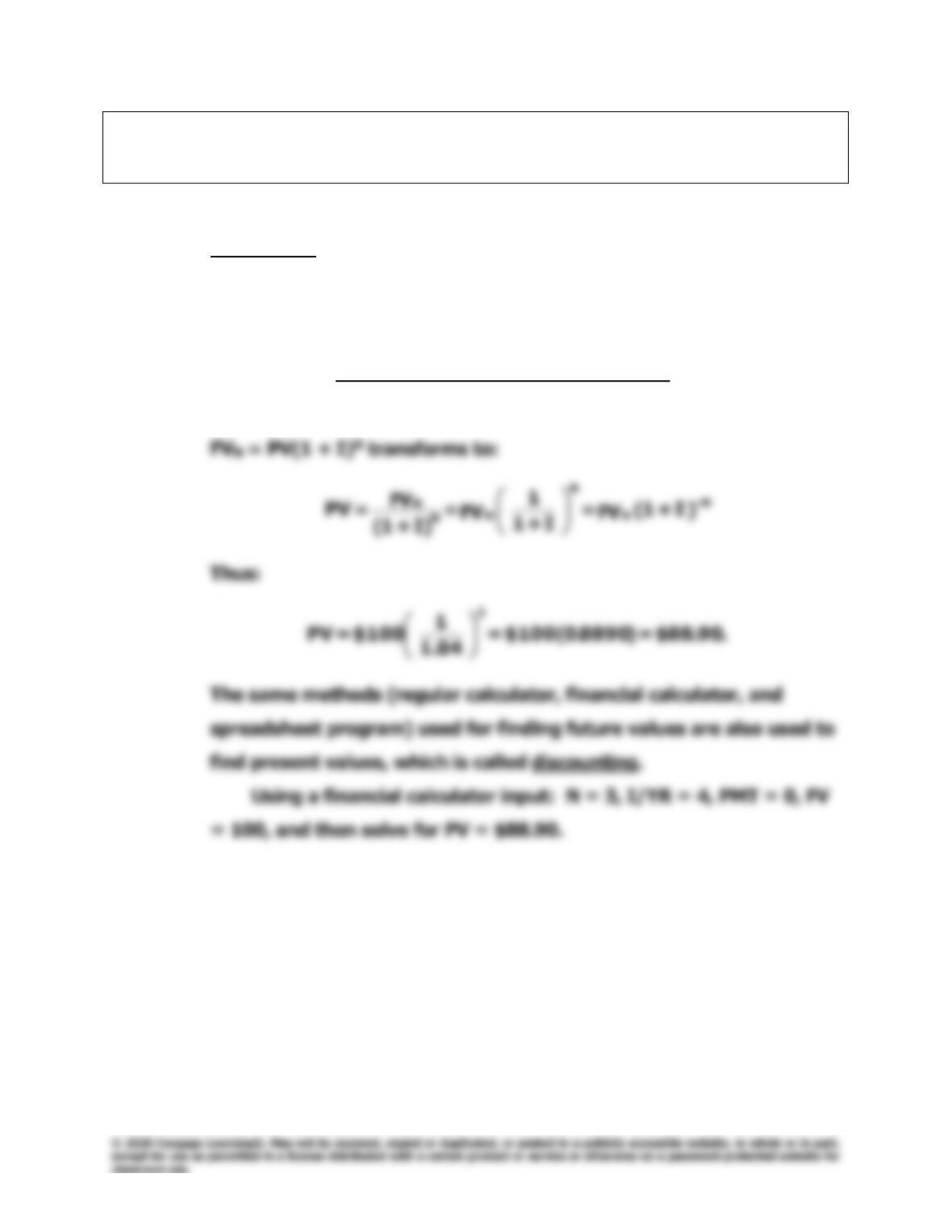

Answer: [Show S5-9 through S5-11 here.] Finding present values, or

discounting (moving to the left along the time line), is the reverse of

compounding, and the basic present value equation is the reciprocal

of the compounding equation:

0 1 2 3

| | | |

PV = ? 100

4%

Chapter 5: Time Value of Money

Integrated Case

111

C. What annual interest rate would cause $100 to grow to $119.10 in 3

years?

ANSWER: [Show S5-12 here.]

0 1 2 3

| | | |

–100 119.10

$100(1 + I) $100(1 + I)2

$100(1 + I)3

FV = $100(1 + I)3 = $119.10.

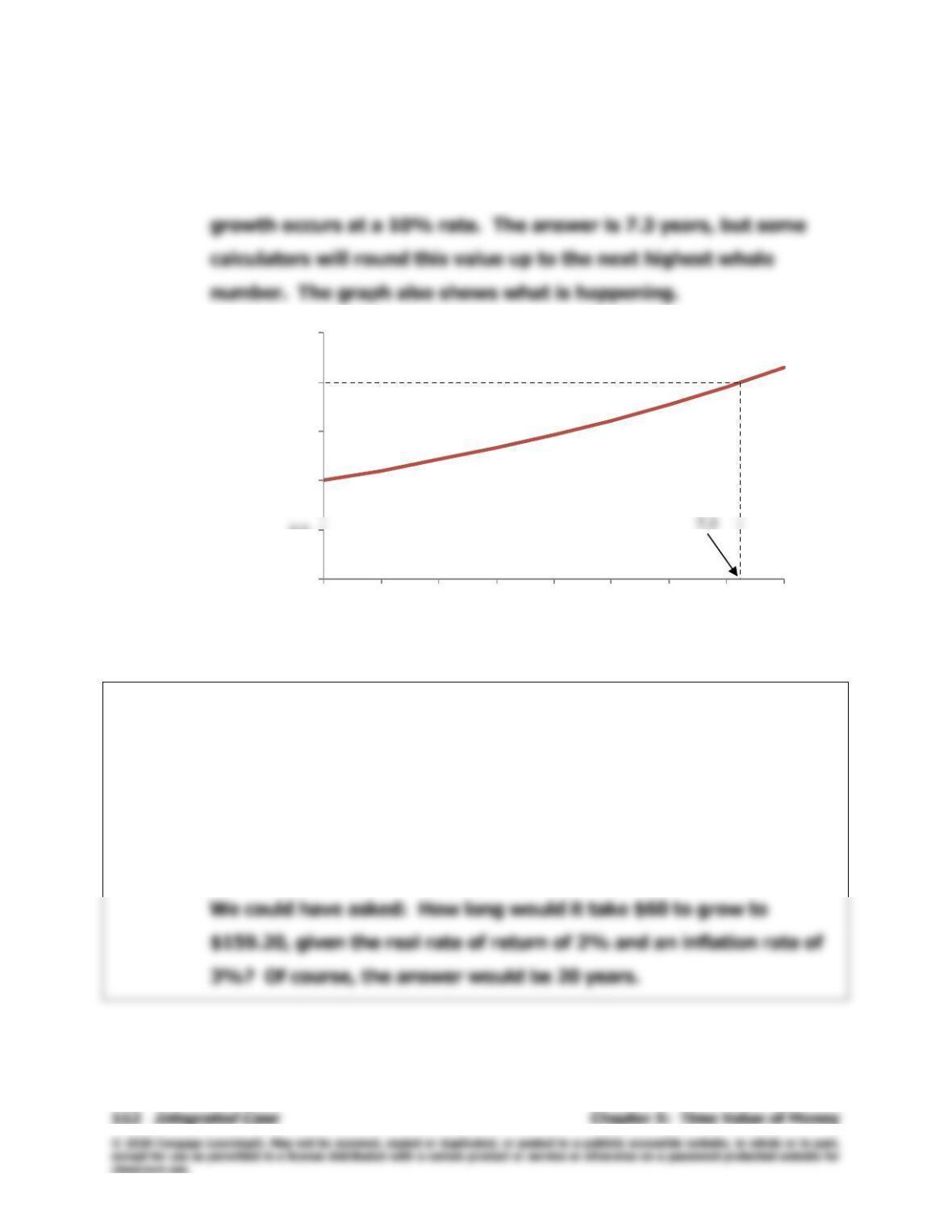

D. If a company’s sales are growing at a rate of 10% annually, how

long will it take sales to double?

ANSWER: [Show S5-13 here.] We have this situation in time line format:

0 1 2 7.3 8

| | | | |

-1 2

Say we want to find out how long it will take us to double our money

10%

We would plug I/YR = 10, PV = –1, PMT = 0, and FV = 2 into our

calculator, and then press the N button to find the number of years

it would take $1 (or any other beginning amount) to double when

0

0.5

1

1.5

2

2.5

0

1

2

3

4

5

6

7

8

FV

Years

Optional Question

A farmer can spend $60/acre to plant pine trees on some marginal land. The

expected real rate of return is 2%, and the expected inflation rate is 3%. What

is the expected value of the timber after 20 years?

ANSWER: FV20 = $60(1 + 0.02 + 0.03)20 = $60(1.05)20 = $159.20 per acre.