CHAPTER 5

Inflation: Its Causes, Effects, and

Social Costs

Notes to the Instructor

Chapter Summary

This chapter explains the classical theory of the causes, effects, and social costs of inflation. It

introduces topics that are central for understanding the economy and presents concepts used

elsewhere in the textbook. These topics include:

2. The effects of monetary policy when prices are flexible;

3. The social costs of inflation.

The material in this chapter builds upon the discussion of money and the monetary system

presented in Chapter 4.

Comments

This chapter can probably be covered in two lectures, although the material on hyperinflation is

difficult and so may require a little extra time. Since hyperinflations are both fascinating and

instructive, this part of the chapter is ultimately very rewarding for the students.

The Fisher equation and the distinction between nominal and real rates of interest are

Use of the Web Site

This is a good time to use the data plotter to explain and illustrate the Fisher equation.

Use of the Dismal Scientist Web Site

Go to the Dismal Scientist Web site and download annual data for the past 40 years for the two

key measures of the money supply: M1 and M2. Also download data over the same period for

nominal GDP. Compute two measures of the velocity of money by dividing GDP by each of the

two measures of the money supply. Discuss how the velocity of money has changed over time

for these two measures.

Chapter Supplements

This chapter includes the following supplements:

5-2 Data on Money Growth and Inflation (Case Study)

5-4 Deriving the Fisher Equation

5-6 Transactions Models of Money Demand

5-7 Inflation and Economic Growth

5-9 The Welfare Costs of Inflation Revisited

5-11 U.S. Treasury Issues Indexed Bonds

5-13 Are Monetary Allegories in the Eye of the Beholder? The Case of Mary Poppins (Case

5-14 How to Stop a Hyperinflation

5-16 Additional Readings

Lecture Notes | 89

Lecture Notes

Introduction

So far, our entire analysis of the economy has been in real terms, since economists think that

different goods. The weights are based on the relative importance of the goods in consumption.

The recent U.S. experience has been one of moderate but positive inflation. In recent

years, prices have been rising by around 2.5 percent per year on average, while the average rate

of inflation was somewhat higher in the 1970s and early 1980s and slightly lower in the 1950s

and 1960s. But this is not the experience of all countries at all times. Earlier in this century, the

= 1.32. Here, a pizza that cost $10 in 1990 would cost $12 in 1991 and $13.20 in 1992. Goods

are becoming more expensive over time, but prices rose more between 1990 and 1991 (20

percent) than between 1991 and 1992 (10 percent). This situation, in which prices are rising but

the rate of inflation is falling, is known as disinflation.

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

Having briefly considered the supply of money, we now turn to the demand for money. We

begin with a very simple theory of money demand, known as the quantity theory. The starting

point for this theory is the observation that people hold money largely to facilitate transactions.

90 | CHAPTER 5: Inflation: Its Causes, Effects, and Social Costs

From Transactions to Income

Suppose that each transaction represents one unit of GDP. This would be true if the only

transactions that took place were those that involved the final sale of newly produced goods.

Then, we could replace T with Y and get an amended form of the quantity equation:

V=PY /M

⇒MV =PY

.

If Y is proportional to T, the income velocity of money will be proportional to the transactions

velocity. For example, if there are three transactions for every transaction involving a unit of

GDP, then the transactions velocity of money is three times the income velocity of money.

The advantage of the income velocity of money is that we can easily measure it; it is

The Money Demand Function and the Quantity Equation

A simple idea about money demand is that people hold money to carry out transactions and that

the amount of money they want to hold is roughly proportional to the number of transactions

they want to perform. If the number of transactions is, in turn, proportional to income, then the

amount of money that people want to hold is proportional to income. Also, we might expect that

the amount of money that people want to hold will be proportional to the price of a transaction;

if the cost of the average transaction doubles, then we would expect that the demand for money

would double. This leads to a money demand function of the form

Md = kPY.

As elsewhere, we prefer to carry out our analysis in real terms. The term M/P is called real

money balances; it tells you the value of M in terms of goods. So we can rewrite our money

demand function in real terms as

The Assumption of Constant Velocity

The quantity equation, therefore, becomes a theory of the demand for money by supposing that

money demand is proportional to output. This means, in essence, that we are assuming that the

Lecture Notes | 91

!Figures 5–1, 5-2

!Supplement 5–2,

“Data on Money

Growth and

Inflation”

!Supplement 5–3,

“Seignorage as an

Inflation Tax”

velocity of money is constant. The assumption of constant velocity is not fully satisfactory, for

reasons that we will come to, but it is a useful starting point. Note, moreover, where this theory

leads us. If V is fixed (V), then nominal GDP must be proportional to the money supply. If Y is

also fixed, then the price level is proportional to the money supply.

Money, Prices, and Inflation

Let us explore this a little further. Writing the quantity equation in terms of growth rates gives

As we will see in Chapters 8 and 9, the growth of output depends on exogenous factors such as

population growth and technical progress. It follows that the inflation rate depends on the growth

rate of the money supply. If the Fed keeps the money supply stable, prices will be stable. To put

it another way, if the Fed wishes the inflation rate to be zero, it should increase the money

supply at a rate equal to that of output growth. In that case, there would be just enough extra

money each year to absorb the extra demand due to extra transactions.

Case Study: Inflation and Money Growth

Data for the U.S. economy since 1870 provide broad support for the link between money growth

and inflation implied by the quantity theory. Decadal averages over this period reveal a positive

relationship between the GDP deflator and the growth of M2. International data show the

correlation even more clearly.

5-2 Seigniorage: The Revenue from Printing Money

The discussion of the circular flow of income in Chapter 3 revealed that the government deficit

equals the difference between government spending and government income from taxation. The

government can finance its deficit by borrowing from the public or by printing money. New

money is a source of government revenue, like taxation. The revenue that the government

obtains by printing money is known as seigniorage.

Case Study: Paying for the American Revolution

The Continental Congress depended significantly on seigniorage to finance the Revolution. New

issues of continental currency grew approximately twentyfold between 1775 and 1779, leading

in turn to substantial inflation.

5-3 Inflation and Interest Rates

Two Interest Rates: Real and Nominal

We now turn to the distinction between nominal and real interest rates. This is an occasion when

macroeconomics teaches an important, simple, yet often overlooked, insight. The interest rate

quoted in the newspapers is a nominal interest rate. It gives the number of dollars that will be

92 | CHAPTER 5: Inflation: Its Causes, Effects, and Social Costs

!Figures 5–3, 5-4

!Supplement 5–5,

“Using Interest

Rates to Forecast

Inflation”

paid next year for a dollar deposited today. For example, a 10 percent interest rate implies that

$100 deposited today earns $110 next year. But suppose that prices also rise at 10 percent per

The Fisher Effect

Notice that we now have two implications of an increase in the money growth rate. First, our

theory predicts that an increase in the money growth rate of, say, 1 percent should increase the

inflation rate by 1 percent. In turn, this should imply a 1 percent increase in the nominal interest

rate. This link between the inflation rate and the nominal interest rate is known as the Fisher

effect.

Case Study: Inflation and Nominal Interest Rates

The data for the U.S. and other economies clearly reveal the connection between the inflation

rate and the nominal interest rate suggested by the Fisher effect. They also reveal that the real

interest rate changes over time.

Two Real Interest Rates: Ex Ante and Ex Post

The previous discussion is misleading in one respect. When people make intertemporal

economic decisions, they don’t know for sure what the inflation rate will be. This means that,

rather than the actual inflation rate, we should use the expected inflation rate. The relevant real

Case Study: Nominal Interest Rates in the Nineteenth Century

The Fisher effect is not evident in U.S. data the late nineteenth and early twentieth centuries.

Years when the inflation rate was high were not necessarily years when nominal interest rates

5-4 The Nominal Interest Rate and the Demand for Money

Our earlier discussion of money demand noted that one function of money is that it serves as a

store of value. In times of inflation, it serves less well in this role. If prices are rising, a dollar

bill buys less and less as time goes by. This suggests that our previous analysis of the demand

for money, where money demand depends only on income, is incomplete.

Lecture Notes | 93

!Supplement 5–6,

“Transactions

Models of Money

Demand”

!Supplement 5–7,

“Inflation and

The Cost of Holding Money

The observation that inflation reduces the value of money suggests that, if the inflation rate is

high, people will be less inclined to hold their wealth in the form of money. This intuition is

basically correct, but not complete. It turns out that money demand depends on the nominal

interest rate and, hence, indirectly (through the Fisher effect) on the inflation rate.

To see this, note that money is simply one way in which people can hold wealth. The

advantage of money is that it is convenient for transactions. But it has an associated

disadvantage: If an individual holds wealth in the form of money, she gives up the interest she

could earn if she instead put her wealth into interest–bearing assets. The interest that she could

have earned but didn’t is an opportunity cost. An interest–bearing asset pays an interest rate of i;

Future Money and Current Prices

We have now made life, or at least our theory, more complicated. Suppose that we see a 1

percent increase in the growth rate of the money supply. This will increase the inflation rate. But

through the Fisher effect, this will, in turn, increase the nominal interest rate and so decrease the

5-5 The Social Costs of Inflation

The Layman’s View and the Classical Response

The general public views inflation as a major social problem because of the mistaken belief that

rising prices make a person poorer. This notion reflects a lack of understanding about how a

Case Study: What Economists and the Public Say About

Inflation

The economist Robert Shiller used a survey to examine the attitudes of economists and the

general public with respect to inflation. He discovered that the public was more inflation averse

The Costs of Expected Inflation

94 | CHAPTER 5: Inflation: Its Causes, Effects, and Social Costs

!Supplement 5–8,

“The Welfare

Costs of Inflation

and the Optimum

Quantity of

Money”

!Supplement 5–9,

“The Welfare

Costs of Inflation

Revisited”

!Supplement 5–11,

“U.S. Treasury

Issues Indexed

Bonds”

In considering the social costs of inflation, a useful starting point is the distinction between

anticipated and unanticipated inflation. First, consider those costs of inflation that exist when all

prices and wages are rising at some steady, well–understood rate.

The first social cost of inflation is shoe–leather costs. Remember that the demand for

money depends negatively on the nominal interest rate and, hence, on the inflation rate. When

the interest rate is high, it is worthwhile for people to put some time and effort into economizing

on their holdings of cash; they go to the bank more often and, metaphorically, wear out their

shoes more quickly.

A second cost of steady, anticipated inflation is also referred to in metaphorical terms:

menu costs. The idea here is that, in times of inflation, restaurants have to print new menus with

changed prices. More generally, the act of changing prices may absorb real resources in the

economy. While this cost is undoubtedly real, it seems unlikely that it is substantial.

A third cost of inflation arises because it may introduce unwanted variation in relative

The Costs of Unexpected Inflation

Unanticipated inflation introduces extra uncertainty into the economic environment. Generally,

we think that people dislike uncertainty; in economists’ terminology, they are risk averse. Thus,

unanticipated inflation hurts people because it leads to arbitrary and unpredictable

redistributions. Consider two people who enter into a contract specified in nominal terms. If

inflation is higher than predicted, then the debtor “wins”—she pays less in real terms than she

expected—and the creditor loses since, he gets less in real terms than he expected.

From a social point of view, such redistributions are not themselves necessarily costly, but

it is important to recognize that they do occur. Furthermore, if increased uncertainty discourages

Lecture Notes | 95

!Supplement 5–12,

“A Guide to Oz”

!Supplement 5–13,

“Are Monetary

Allegories in the

Eye of the

Beholder? The

Case of Mary

Poppins”

!Supplement 5–14,

“How to Stop a

Hyperinflation”

!Figure 5-6

Case Study: The Free Silver Movement, the Election of 1896,

and the Wizard of Oz

The Wizard of Oz has been argued to be an allegory of the debate over the gold standard during

the 1896 presidential election. Some people believe that this reveals more about economists than

it does about the Wizard of Oz.

One Benefit of Inflation

The costs associated with both anticipated and unanticipated inflation have often been cited as

justification for why policymakers should target a zero rate of inflation. But it may be the case

5-6 Hyperinflation

Hyperinflation simply means very rapid inflation, usually 50 percent per month or more.

Inflation at this rate means that goods become more than 100 times more expensive over the

course of a year. Lenin is reported to have said that the best way to destroy capitalism was

through such inflation.

The Costs of Hyperinflation

Some of the costs of inflation discussed in the previous section become very severe in the case

of a hyperinflation. Shoe–leather costs are probably small under low inflation but become very

The Causes of Hyperinflation

If the quantity theory were correct, so that real money demand were simply proportional to GDP,

then analyzing hyperinflations would be straightforward. Excessive money growth would lead to

large inflation; to stop a hyperinflation, it would be sufficient to control the growth rate of the

money supply. But the quantity theory is not a good guide to the demand for money in this

Case Study: Hyperinflation in Interwar Germany

During the period 1922 to 1924, Germany experienced a massive hyperinflation. Over the last 15

months of this inflation, prices rose at an average of well over 300 percent per month. The

hyperinflation arose because the German government resorted to money creation to pay for

!Supplement 5-15,

96 | CHAPTER 5: Inflation: Its Causes, Effects, and Social Costs

Case Study: Hyperinflation in Zimbabwe

Over the past couple of decades, the government of Robert Mugabe in Zimbabwe implemented

land reforms intended to redistribute wealth from the white minority to the historically

disenfranchised black population. Productivity and output in farming fell as experienced white

farmers left the country. The drop in output caused government tax revenue to decline. With tax

5-7 Conclusion: The Classical Dichotomy

The analysis of Chapter 3 revealed that, in the long run, real variables in the economy (that is,

quantities such as GDP and relative prices such as the real wage) can be determined

independently of nominal variables. This separation of real and nominal variables is known as

Appendix: The Cagan Model: How Current and Future Money

Affect the Price Level

Chapter 5 explains that the demand for real money balances depends on the nominal interest rate

and, hence, on the inflation rate. For a given supply of nominal money, therefore, the current

price level depends on the expected future price level. Consequently, the current price level

depends on both the current money supply and the expected future money supply.

We can see this more formally by assuming that money market equilibrium can be written

as

where Mt is the money supply, Pt is the price level, πt is the inflation rate, γ measures the

sensitivity of money demand to the nominal interest rate, and k is an unimportant constant. By

writing the money demand function in this form, we are assuming that income and real interest

rates are constant (their effects are subsumed in the constant k), so we can focus attention on the

effects of changes in the inflation rate. Letting lowercase letters denote logarithms (and ignoring

Lecture Notes | 97

pt=1

1+

γ

mt+

γ

1+

γ

mt+1+

γ

1+

γ

2

mt+2+

γ

1+

λ

3

mt+3+

.

So the current price level depends upon the entire future path of the money supply. If money

98

LECTURE SUPPLEMENT

5-1 The Velocity of Money in Poetry and Song

The subject matter of economics does not usually provide a great deal of inspiration for songwriters and

poets. The velocity of money seems to be an exception.

The Dollar Bill Song1

She took a dollar bill from her pocket

She picked up a fountain pen.

She wrote the words “I love you”

By the picture of George Washington.

Anyway the Rabbi spent the bill on a ham and cheese to go.

They gave the bill to a guy named Phil who gave it to his best friend Joe.

Joe had planned to spend the bill on some flowers for his bride

But he was mugged by a junkie named Doug in the parking lot outside.

Doug’s old lady spent the bill on a couple of bottles of beer.

She eventually becomes a very famous poet, but that don’t matter here.

The liquor store guy put the dollar bill in his register but then

Doug the junkie said “Stick ’em up” and the dollar was his again.

99

You know I will be there.

My friend you don’t need no dime

You don’t need no subway fare

Just give a tug along the line

I’m with you everywhere.

Ten Pence Story2

My lowest ebb was a seven month spell

spent head down in a stagnant wishing well,

half eclipsed by an oxidized tuppence

which impressed me with its green circumference.

When they fished me out I made a few phone calls,

fed a few meters, hung round the pool halls.

I slotted in well, but all that vending

blunted my edges and did my head in.

100

My own ambition? Well, that was simple:

to be flipped in Wembley’s centre circle,

to twist, to turn, to hang like a planet,

to touch down on that emerald carpet.

101

CASE STUDY EXTENSION

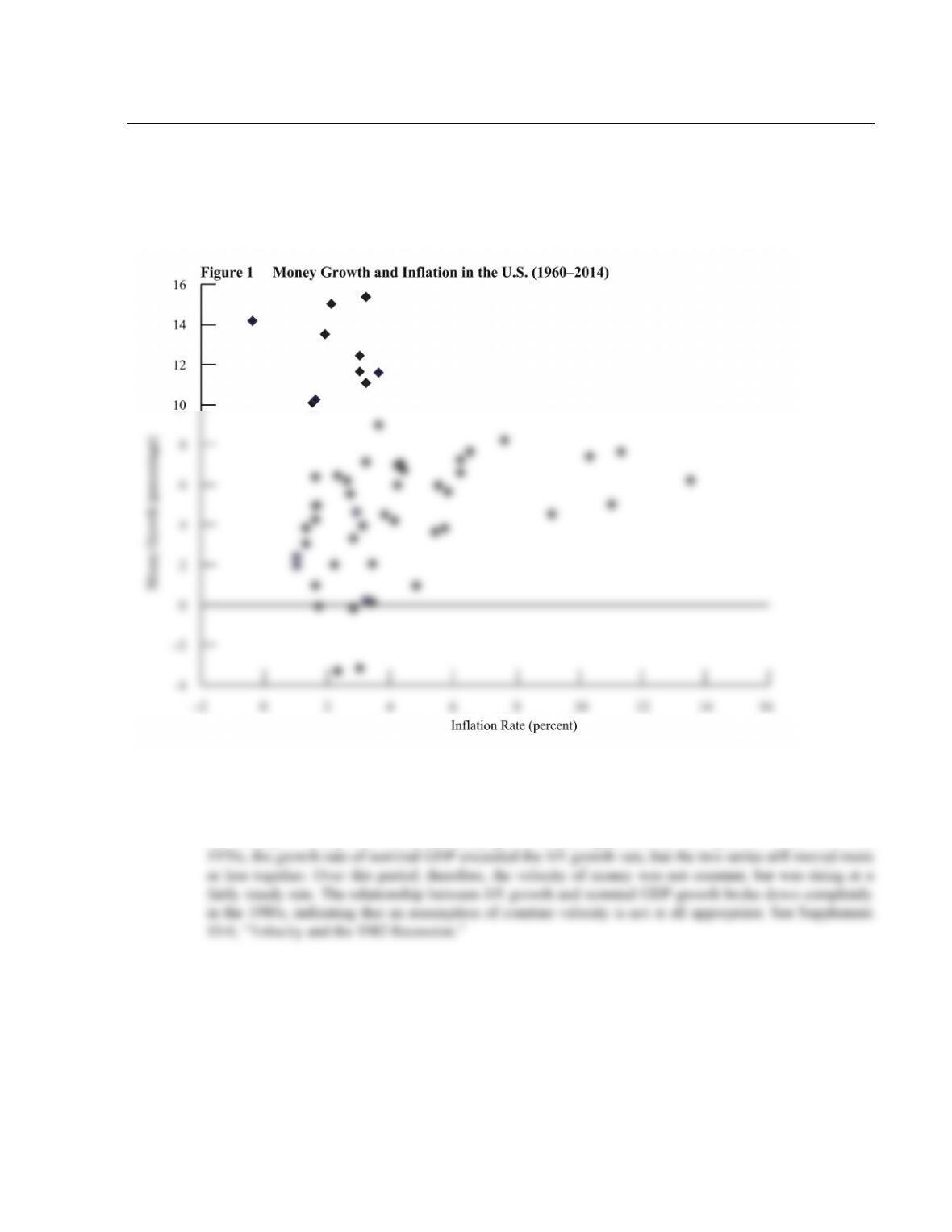

5-2 Data on Money Growth and Inflation

The case study “Inflation and Money Growth” shows the relationship between money growth (M1) and

inflation that exists in long–run data and notes that such a relationship is not evident in short–run data.

Figure 1 illustrates this by showing annual data on money growth and inflation in the United States for the

last half century.

Note: Money growth is annual percentage change in M1. Inflation is annual percentage change in official CPI.

Source: Federal Reserve Board and U.S. Department of Labor, Bureau of Labor Statistics.

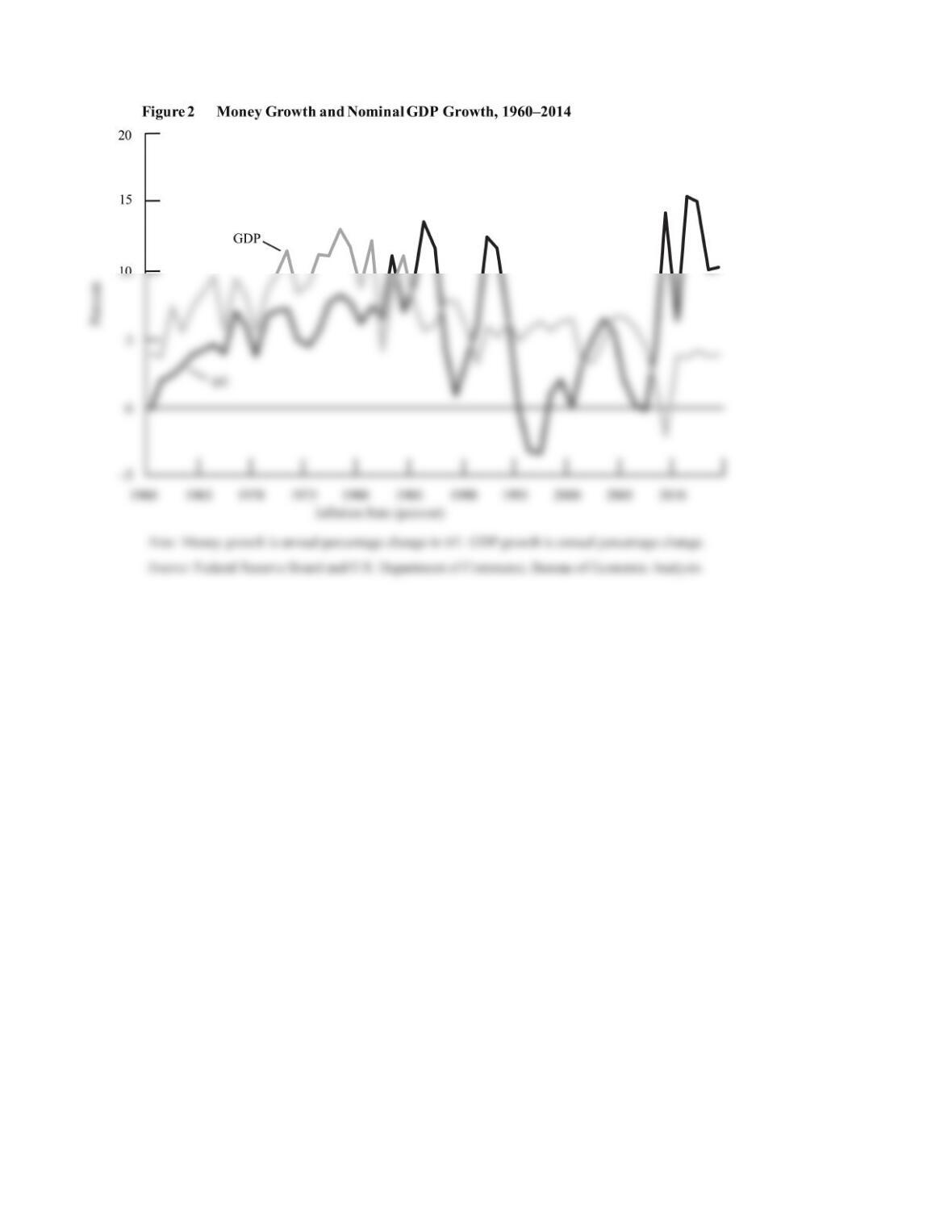

Figure 2 shows the relationship between money growth and nominal GDP growth for the same period. If

the velocity of money were constant, money growth would equal nominal GDP growth. In the 1960s and

102

LECTURE SUPPLEMENT

5-3 Seigniorage as an Inflation Tax

The textbook explains that seigniorage arises because a government can print money at essentially zero

cost and use it to buy goods. It also describes seigniorage as an inflation tax, because holders of existing

money balances see the real value of their money decline with inflation. The equivalence of the two may

not be immediately obvious, however.

( )

We therefore find an equivalence between the two measures of seigniorage if the inflation rate (∆P/P)

equals the money growth rate (∆M/M). As explained in the textbook, the two will be equal in the long run

in an economy without output growth.

If output is growing, the money growth rate will exceed the inflation rate. In a growing economy,

money demand is increasing through time, so the monetary authorities can print money to accommodate

104

LECTURE SUPPLEMENT

5-4 Deriving the Fisher Equation

Section 4–4 of the textbook explains the Fisher equation—that is, the relationship between the real interest

rate, the nominal interest rate, and the rate of inflation. Specifically, the real interest rate is shown to equal

the nominal interest rate minus the inflation rate (r = i – π). Here, we derive that relationship more

formally.

Think about two people (Bill and Hillary) who agree to a loan specified in real terms. Hillary agrees

to give goods (units of GDP) to Bill today on the understanding that, for every unit Bill receives, he will

repay 1 + r units next year. In this setup, r is the real interest rate; that is, it is the interest rate in terms of

commodities.

units of GDP next period. Thus, the real return on this dollar–denominated loan is (1 + i)/(1 + π).

We thus find that

1+r=

1+i

( )

1+

π

( )

⇒1+r

( )

1+

π

( )

=1+i

( )

.

Multiplying out the left–hand side and subtracting 1 from each side gives