1

2

3

4

5

6

7

10

11

12

13

14

A B C D E F G H

SECTION 5-8 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N5

I4%

N5

I4%

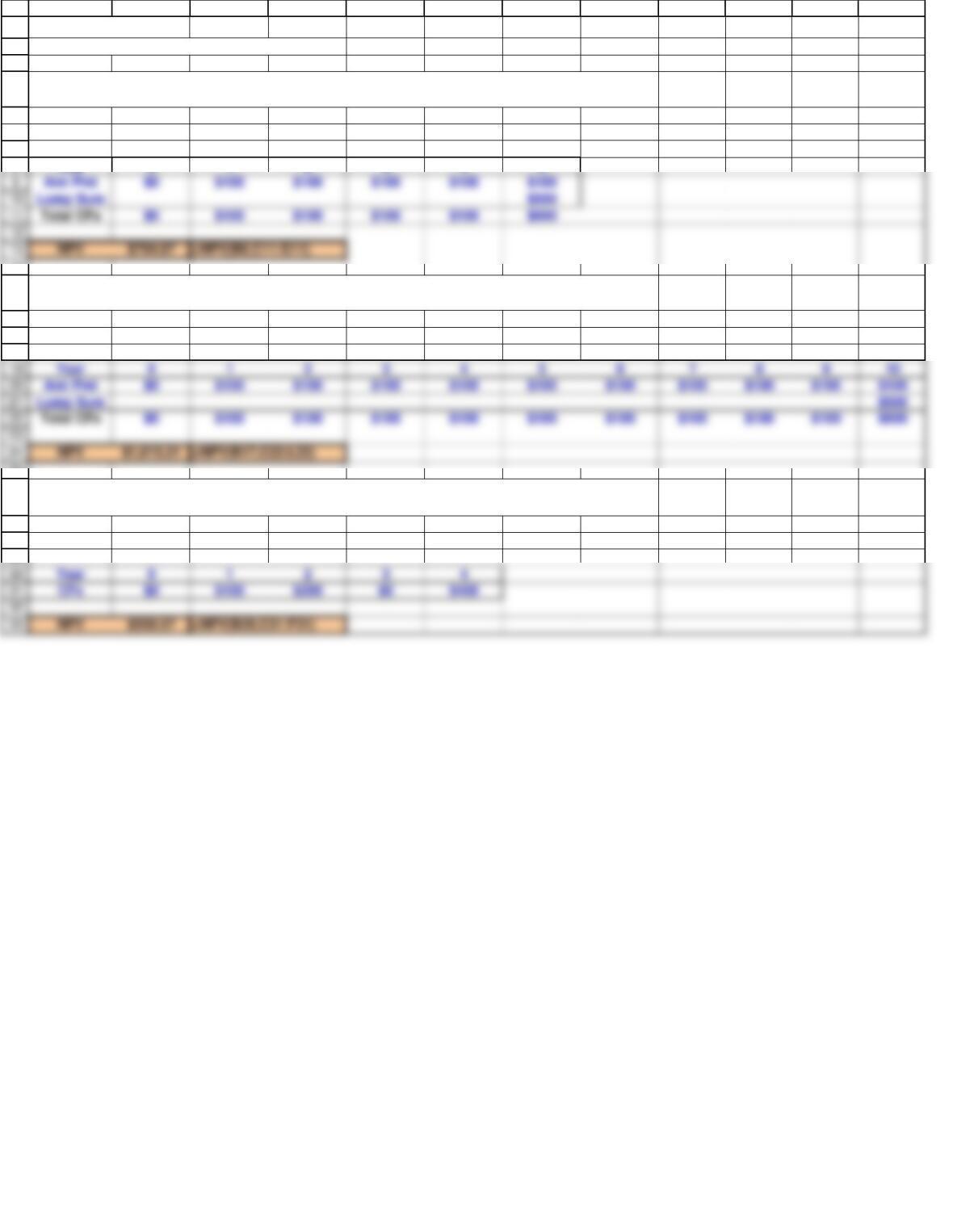

3a. Assume that you plan to buy a condo 5 years from now, and you need to save for a down

payment. You plan to save $2,500 per year (with the first deposit made immediately ), and you

will deposit the funds in a bank account that pays 4% interest. How much will you have after 5

years?

3b. How much will you have if you make the deposits at the end of each year?

21

1

2

3

4

5

6

7

I4%

10

11

12

13

17

18

19

20

21

N10 N10 N10

I10% I4% I0%

3d. How would the PVA values differ if we were dealing with annuities due?

34

35

36

37

38

N10

I8%

4b. If the payments began immediately, how much would the annuity be worth?

A B C D E F G H I

SECTION 5-9 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N10

I10%

N10

N10

I0%

N10

I8%

4a. Assume that you are offered an annuity that pays $100 at the end of each year for 10

years. You could earn 8% on your money in other investments with equal risk. What is the

most you should pay for the annuity?

3a. What is the PVA of an ordinary annuity with 10 payments of $100 if the appropriate

interest rate is 10%?

3b. What would the PVA be if the interest rate was 4%?

3c. What if the interest rate was 0%?

22

1

2

3

4

5

6

7

I7%

10

11

12

13

17

18

19

20

21

PV $100,000

24

25

26

27

PV $100,000

31

32

33

34

38

39

40

41

42

45

46

47

48

49

52

53

A B C D E F G H

SECTION 5-10 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N10

I7%

N10

I7.0%

PV $100,000

I0.0%

I7.0%

N12

PMT $12,000

N10

PMT -$10,000

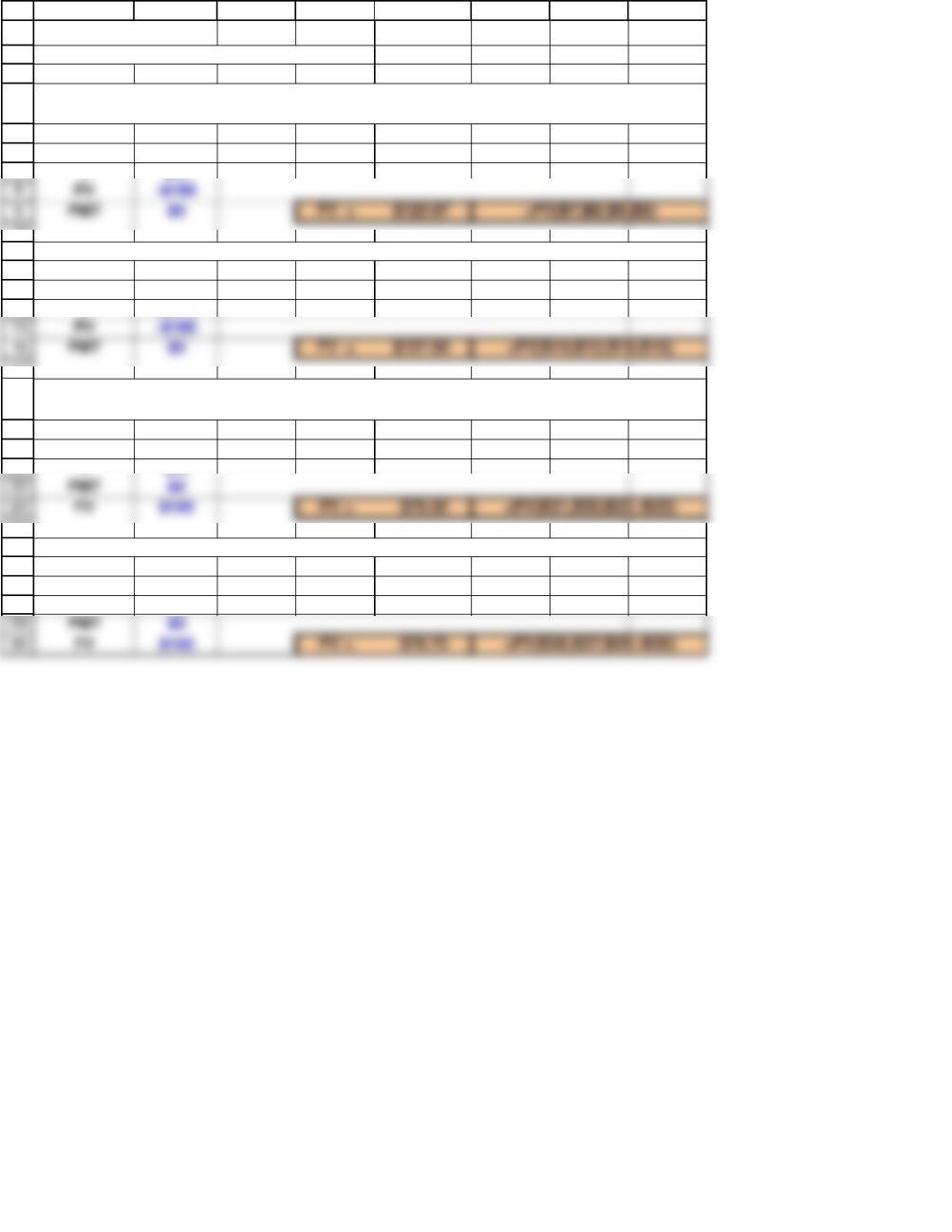

4b. If you think a “fair” return would be 6%, how much should you ask for the annuity?

2c. How long would they last if you earned the 7% but limited your withdrawals to $7,000 per year?

3. Your uncle named you as the beneficiary of his life insurance policy. The insurance company

gives you a choice of $100,000 today or a 12-year annuity of $12,000 at the end of each year. What

rate of return is the insurance company offering?

1a. Suppose you inherited $100,000 and invested it at 7% per year. What is the most you could

withdraw at the end of each of the next 10 years and have a zero balance at Year 10?

1b. How would your answer change if you made withdrawals at the beginning of each year?

2a. If you had $100,000 that was invested at 7% and you wanted to withdraw $10,000 at the end of

each year, how long would your funds last?

2b. How long would they last if you earned 0%?

4a. Assume that you just inherited an annuity that will pay you $10,000 per year for 10 years, with

the first payment being made today. A friend of your mother offers to give you $60,000 for the

annuity. If you sell it, what rate of return would your mother’s friend earn on his investment?

23

54

55

56

A B C D E F G H

N10

I6%

24

1

2

3

4

5

6

7

8

9

10

A B C D E F G H

SECTION 5-11 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

PMT $1,000

I5% PV $20,000 =B6/B7

**The perpetuity value formula

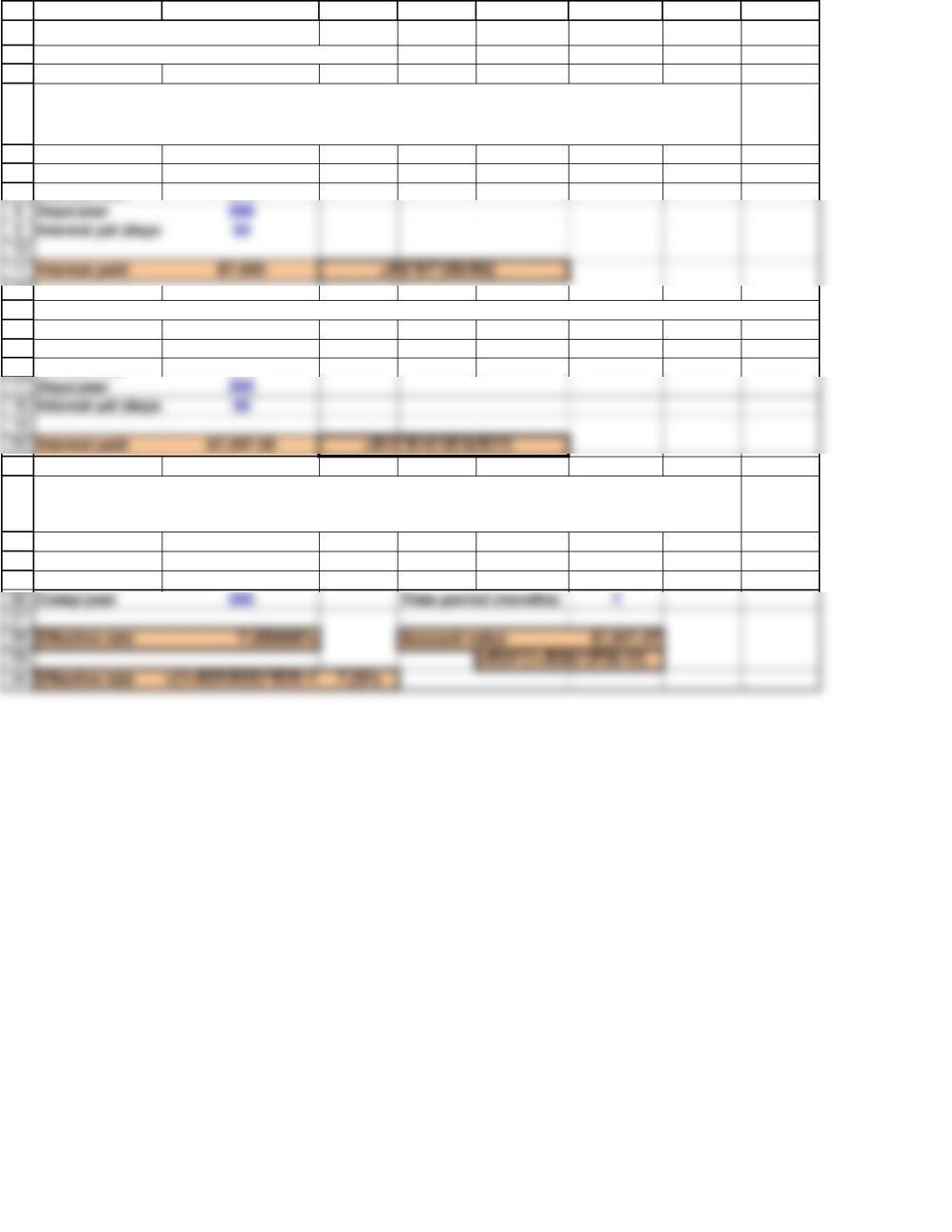

1a. What’s the present value of a perpetuity that pays $1,000 per year, beginning one year from

now, if the appropriate interest rate is 5%?

1b. What would the value be if payments on the annuity began immediately?

25

PMT $1,000

I5% PV $21,000

1

2

3

4

5

6

7

8

14

15

16

17

18

25

26

27

28

29

A B C D E F G H I J K L

SECTION 5-12 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Interest rate 6%

Year 0 1 2 3 4 5

Interest rate 6%

Interest rate 8%

2a. What’s the present value of a 5-year ordinary annuity of $100 plus an additional $500 at the end

of Year 5 if the interest rate is 6%?

2b. What is the PV if the $100 payments occur in Years 1 through 10 and the $500 comes at the end

of Year 10?

3. What’s the present value of the following uneven cash flow stream: $0 at Time 0, $100 in Year 1

(or at Time 1), $200 in Year 2, $0 in Year 3, and $400 in Year 4 if the interest rate is 8%?

26

1

2

3

4

5

6

A B C D E

SECTION 5-13 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Interest rate 15%

2. What is the future value of this cash flow stream: $100 at the end of 1 year, $150 due after 2 years, and $300 due

after 3 years if the appropriate interest rate is 15%?

27

1

2

3

4

5

6

7

8

9

14

15

16

17

A B C D E F G H

SECTION 5-14 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Interest rate 6%

Year 0 1 2 3 4

Ann Pmt -$465 $100 $100 $100 $100

Year 0 1 2 3

1. An investment costs $465 and is expected to produce cash flows of $100 at the end of each of

the next 4 years, then an extra lump sum payment of $200 at the end of the 4th year. What is the

expected rate of return on this investment?

2. An investment costs $465 and is expected to produce cash flows of $100 at the end Year 1, $200

at the end or Year 2, and $300 at the end of Year 3. What is the expected rate of return on this

investment?

28

1

2

3

4

5

6

7

10

11

12

13

14

I8%

17

18

19

20

24

25

26

27

28

A B C D E F G H

SECTION 5-15 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N3

I8%

N36

I0.67%

N3

N36

I1%

2a. What’s the future value of $100 after 3 years if the appropriate interest rate is 8%,

compounded annually?

2b. Compounded monthly?

3a. What’s the present value of $100 due in 3 years if the appropriate interest rate is 8%,

compounded annually?

3b. Compounded monthly?

29

1

2

3

4

5

6

A B C D E F G H

SECTION 5-16 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Nominal rate 18%

3. By law, credit card issuers must print their annual percentage rate (APR) on their

monthly statements. A common APR is 18% with interest paid monthly. What is the EFF%

on such a loan?

30

1

2

3

4

5

6

7

Interest pd (days)

12

13

14

15

16

21

22

23

24

25

A B C D E F G H

SECTION 5-17 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Loan $1,000,000

Interest rate 9%

Loan $1,000,000

Interest rate 9%

Loan $1,000

Interest rate 7%

1b. What would the interest be if the bank used a 365-day year?

1a. Suppose a company borrowed $1 million at a rate of 9%, simple interest, with interest paid

at the end of each month. The bank uses a 360-day year. How much interest would the firm

have to pay in a 30-day month?

2a. Suppose you deposited $1,000 in a credit union that pays 7% with daily compounding and

a 365-day year. What is the EFF%, and how much could you withdraw after 7 months,

assuming this is 7/12 of a year?

31

Interest pd (days)

1

2

3

4

5

6

7

12

13

14

15

18

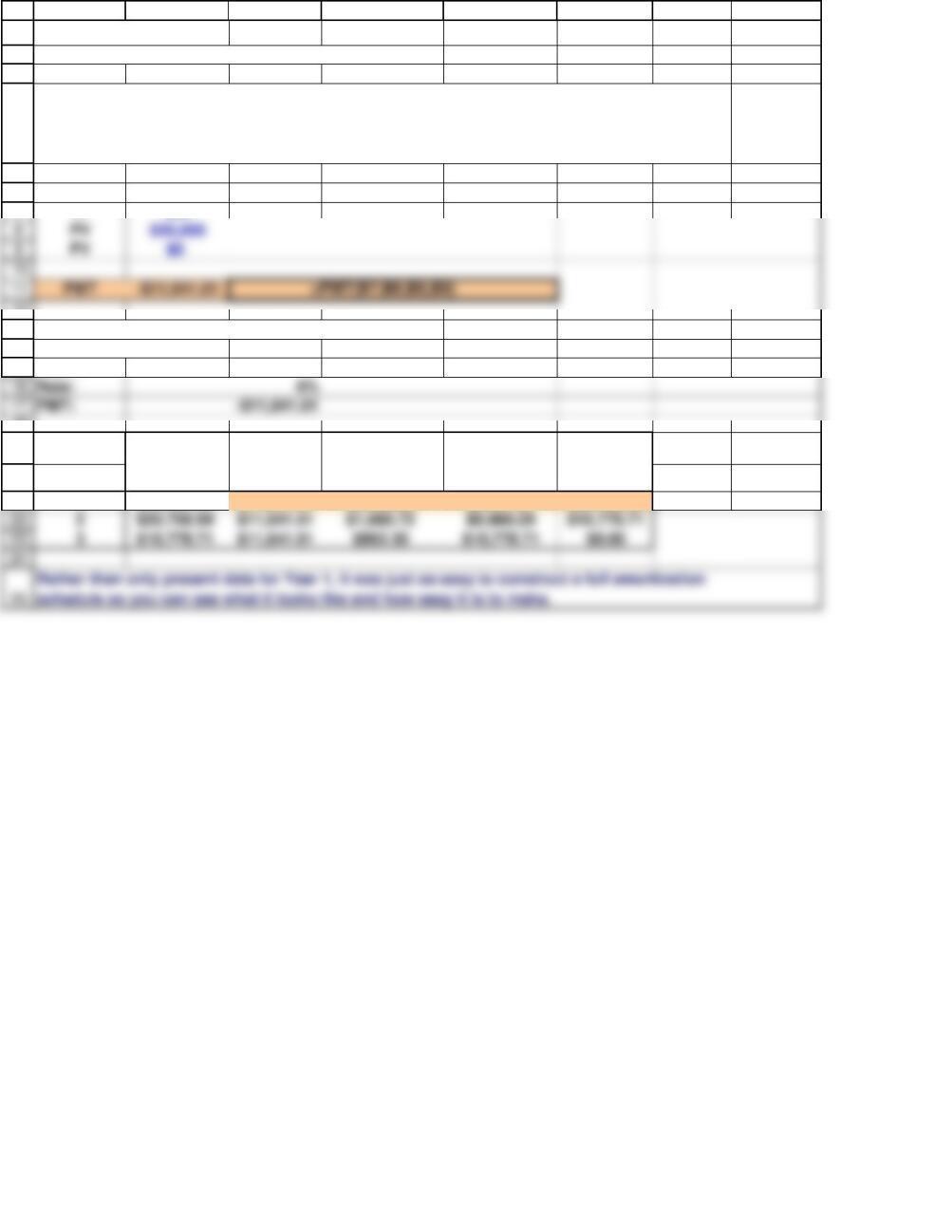

2$20,758.99 $11,641.01 $1,660.72 $9,980.29 $10,778.71

3$10,778.71 $11,641.01 $862.30 $10,778.71 $0.00

19

20

21

A B C D E F G H

SECTION 5-18 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N3

I8%

Loan Amortization Schedule, $30,000 at 8% for 3 Years

Amount borrowed: $30,000

Years: 3

Year

1$30,000.00 $11,641.01 $2,400.00 $9,241.01 $20,758.99

1. Suppose you borrowed $30,000 on a student loan at a rate of 8% and must repay it in 3

equal installments at the end of each of the next 3 years. How large would your payments be,

how much of the first payment would represent interest, how much would be principal, and

what would your ending balance be after the first year?

Beginning

Amount

(1)

Payment

(2)

Interest (3)

Repayment of

Principal (4)

Ending

Balance

(5)

32

1

2

3

7

8

9

10

11

12

13

18

19

20

21

22

23

24

25

A B C D E F G H

WEB APPENDIX 5A: CONTINUOUS COMPOUNDING AND DISCOUNTING 12/12/2018

FVN = PV (e)IN

PV

$100.00

I

10.00%

PV = FVN (e)-IN

FV

$100.00

I

10.00%

When more frequent compounding occurs, the future value of an amount can be calculated as follows:

Continuous compounding is a situation in which interest is added continuously rather than at discrete

points in time. The equation for continuous compounding is:

If we deposit $100 today in an account that pays 10% interest compounded continuously, what amount

will be in the account at the end of 5 years?

Continuous discounting is the reverse of continuous compounding. It is equal to the value today of a

future amount discounted at an interest rate with continuous compounding rather than at discrete points

in time. The equation for continuous discounting is:

What is the value today of $100 withdrawn in 5 years from an account that pays 10% interest

compounded continuously?

33

FVN = PV (1 + INOM/M)MN

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

20

21

22

23

24

25

A B C D E F G H I J K L

WEB APPENDIX 5B: GROWING ANNUITIES 12/12/2018

EXAMPLE 1: FINDING A CONSTANT REAL INCOME, IMMEDIATE FIRST WITHDRAWAL

PROBLEM

Use Financial Calculator

Step 1:

Real rate = (1 + rNOM)/(1 + Inflation) – 1.0

rNOM 8.00%

Inflation 3.00%

Step 2:

BEGIN

N20

I4.85%

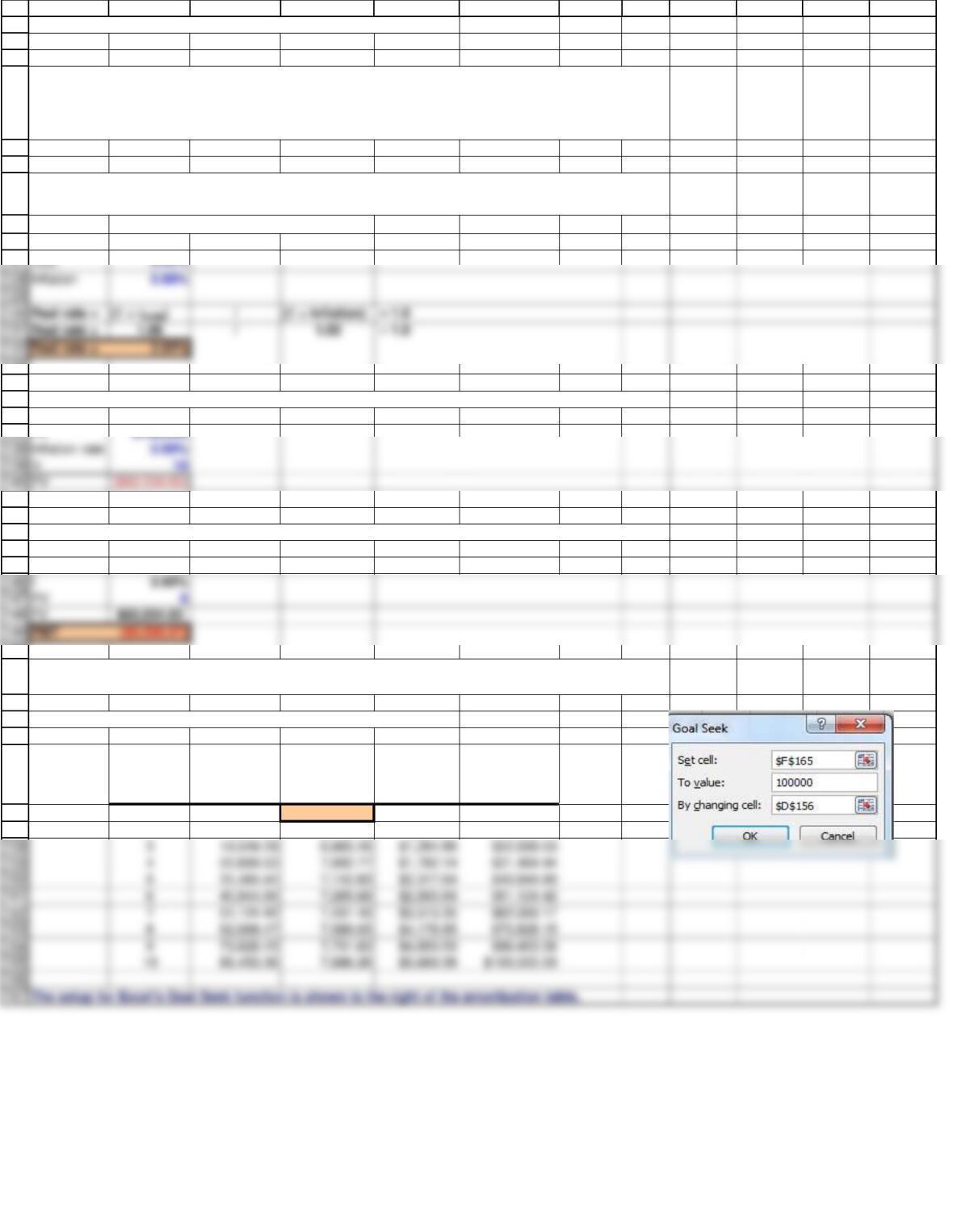

A growing annuity is a series of payments that grow at a constant rate. Growing annuities are often

used in the area of financial planning. Suppose a prospective retiree wants to determine the

constant real, or inflation-adjusted, withdrawals he or she can make from a given amount of money

over a specified number of years. This problem can be solved in one of two ways. (1) Use a financial

calculator, where we first calculate the real rate of return, which is the nominal rate adjusted for

inflation, and use it for I to find the withdrawal. (2) Set up a spreadsheet model similar to an

amortization table and use Excel’s Goal Seek function to find the initial inflation-adjusted withdrawal.

Suppose your uncle, who is 65 years old, is contemplating retirement. He expects to live for another

20 years, has a $1 million nest egg, expects to earn 8% on his investments, expects inflation to

average 3% per year, and wants to withdraw a constant real amount annually over the next

remaining 20 years. If the first withdrawal is to be made today , what is the amount of the initial

withdrawal?

Before we can use a financial calculator, we must first find the expected real , or inflation-adjusted ,

rate of return. The real rate is calculated as follows:

Now we have all the inputs needed to solve this problem with the financial calculator.

34

32

33

34

35

36

41

42

43

44

45

46

47

A B C D E F G H I J K L

Use Amortization Schedule and Excel’s Goal Seek Function

Year

Age at

Beg. of Year

Beginning

Balance

Withdrawal

Made at Beg.

Of Year

Interest

Earned

During Year

Ending Balance

Age at

End of

Year

165 $1,000,000.00 $75,585.53 $73,953.16 $998,367.62 66

266 998,367.62 77,853.10 73,641.16 994,155.68 67

367 994,155.68 80,188.69 73,117.36 987,084.35 68

872 923,703.83 92,960.67 66,459.45 897,202.61 73

973 897,202.61 95,749.49 64,116.25 865,569.37 74

10 74 865,569.37 98,621.98 61,355.79 828,303.18 75

11 75 828,303.18 101,580.64 58,137.80 784,860.35 76

12 76 784,860.35 104,628.06 54,418.58 734,650.88 77

13 77 734,650.88 107,766.90 50,150.72 677,034.70 78

14 78 677,034.70 110,999.91 45,282.78 611,317.58 79

35

58

59

60

61

62

63

64

65

66

67

76

77

78

79

84

85

86

87

A B C D E F G H I J K L

EXAMPLE 2: CONSTANT REAL INCOME, END-OF-YEAR WITHDRAWALS

PROBLEM

Use Financial Calculator

Step 1:

Real rate = (1 + rNOM)/(1 + Inflation) – 1.0

Step 2:

END

N20

PMT × (1 + Inflation)

Suppose your uncle, who is 65 years old, is contemplating retirement. He expects to live for another

20 years, has a $1 million nest egg, expects to earn 8% on his investments, expects inflation to

average 3% per year, and wants to withdraw a constant real amount annually over the next

remaining 20 years. If the first withdrawal is to be made one year from today , what is the amount of

the initial withdrawal?

Before we can use a financial calculator, we must first find the expected real , or inflation-adjusted ,

rate of return. The real rate is calculated as follows:

Now we have all the inputs needed to solve this problem with the financial calculator.

This amount needs to be adjusted for inflation during the year because this amount is in beginning-

of- year dollars, so this PMT amount must be multiplied by 1 + Inflation rate. The initial withdrawal

should be calculated as follows:

36

73

74

92

93

94

95

96

97

102

103

104

105

106

107

A B C D E F G H I J K L

Use Amortization Schedule and Excel’s Goal Seek Function

Year

Age at

Beg. of Year

Beginning

Balance

Interest

Earned During

Year

Withdrawal

Made at End

Of Year

Ending Balance

Age at

End of

Year

165 $1,000,000.00 $80,000.00 $81,632.38 $998,367.62 66

266 998,367.62 $79,869.41 84,081.35 994,155.68 67

367 994,155.68 $79,532.45 86,603.79 987,084.35 68

872 923,703.83 $73,896.31 100,397.53 897,202.61 73

973 897,202.61 $71,776.21 103,409.45 865,569.37 74

10 74 865,569.37 $69,245.55 106,511.74 828,303.18 75

11 75 828,303.18 $66,264.25 109,707.09 784,860.35 76

12 76 784,860.35 $62,788.83 112,998.30 734,650.88 77

13 77 734,650.88 $58,772.07 116,388.25 677,034.70 78

37

118

119

120

121

122

123

124

125

126

127

133

134

135

136

141

142

143

144

145

150

151

152

153

154

155

156

157

A B C D E F G H I J K L

EXAMPLE 3: INITIAL DEPOSIT TO ACCUMULATE A FUTURE SUM

PROBLEM

Step 1:

Real rate = (1 + rNOM)/(1 + Inflation) – 1.0

rNOM 6.00%

Step 2:

Step 3:

BEGIN

N10

Use Amortization Schedule and Excel’s Goal Seek Function

Year

Beginning

Balance

Deposit Made

at Beg. Of

Year

Interest

Earned

During Year

Ending Balance

1 $0.00 $6,598.87 $395.93 $6,994.80

2 6,994.80 6,730.85 $823.54 $14,549.19

Calculate the size of the required initial payment.

A deposit of $6,598.87 made today and growing by 2% per year will accumulate to $100,000 by Year

10 if the interest rate is 6%.

Suppose you need to accumulate $100,000 in 10 years. You plan to make a deposit now, at Time 0,

and then to make 9 more deposits at the beginning of the following 9 years, for a total of 10 deposits.

The bank pays 6% interest, and you expect to increase your initial deposit amount by the 2% inflation

rate each year.

Before we can use a financial calculator, we must first find the expected real , or inflation-adjusted ,

rate of return. The real rate is calculated as follows:

Need to calculate the purchasing power of $100,000 in 10 years, i.e., calculate PV.

38

131

132