1

2

3

4

5

7

8

11

12

A B C D E F G H I J K L M N O P

05 Chapter model 12/12/2018

FUTURE VALUES (Section 5-2)

Although answers to the Self-Test questions within the chapter are generally quite easy and were found with a

calculator, we also solved some of them with Excel as a check and to provide additional information on the

solutions in case students have questions. The tabs at the lower part of this screen take you to these solutions.

Even if students are not familiar with Excel, they should still be able to see the solution setup and then work out

the answer with a calculator. Although we did not create the model specifically for use in lectures, it could be

This model is STRICTLY OPTIONAL. Neither students nor instructors need to go through it. However, if

someone wants to practice with Excel, then the model can be useful. Also, on the tabs we show solutions for the

within-chapter self-test questions, if applicable.

••The “Main Model” performs the calculations required for Chapter 5, and was used to create many of the

chapter exhibits (Tables and Figures). We pasted in a few dialog boxes for specific Excel functions and features

and show then off to the right of where they apply. However, in general we encourage students who want to

know more about Excel to use the Excel Tutorial and refer to it as necessary. We also let students know that

Excel models can be used to create tables and graphs that can then be copied into Word documents, which is

the way we prepared the text manuscript for submission to the publisher. That procedure is used often in

business to prepare reports.

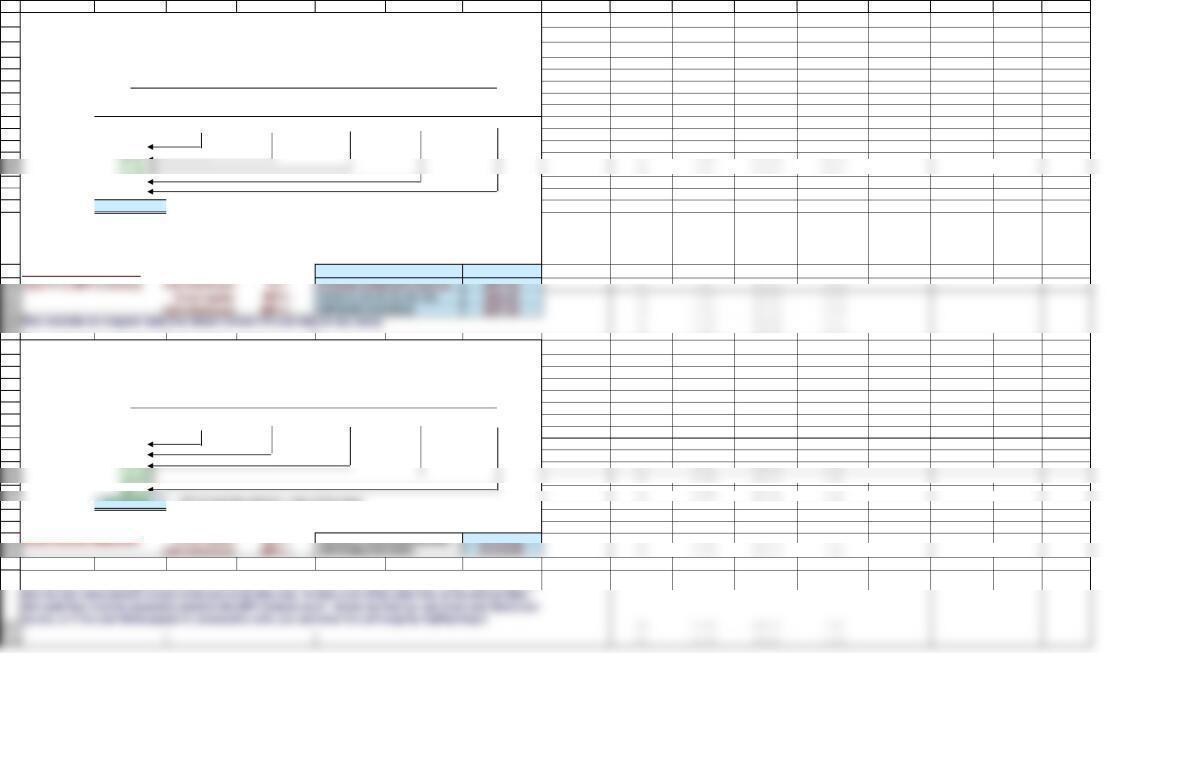

Chapter 5. The Time Value of Money

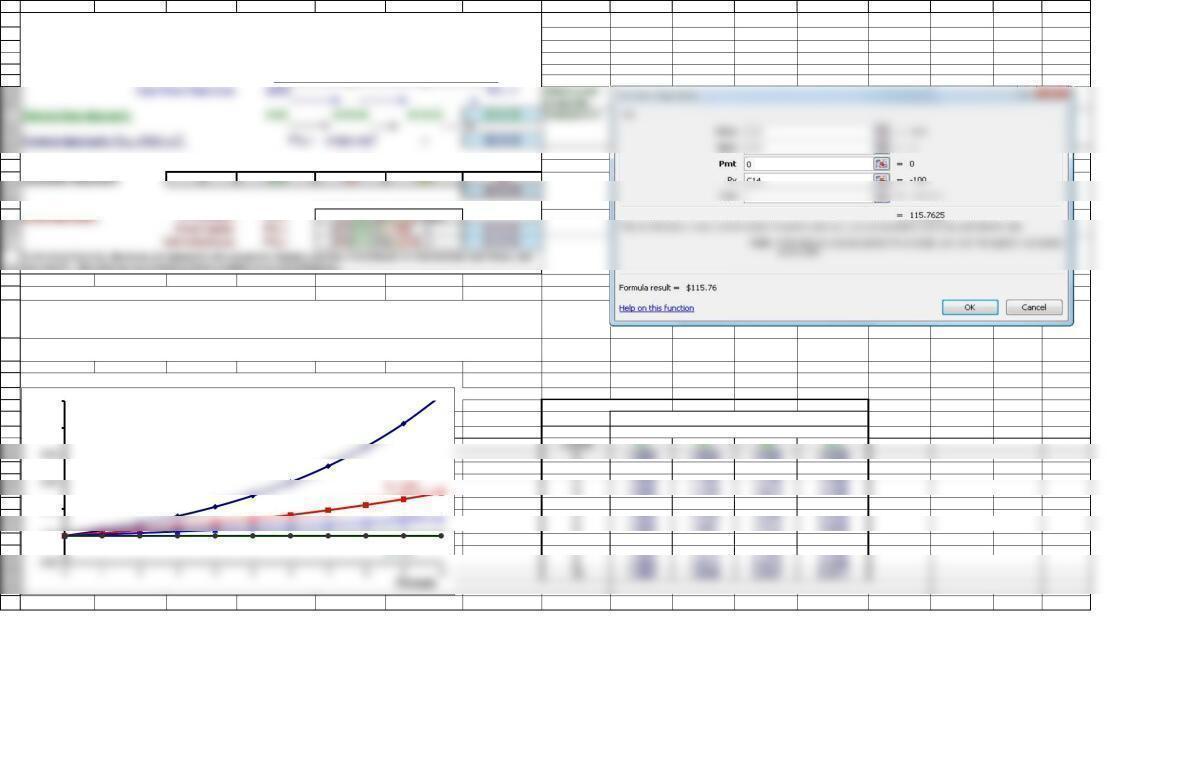

Question: You plan to deposit $100 in a bank that pays a guaranteed 5% interest each year. How much would

you have at the end of Year 3?

Note on Excel: You can do calculations in Excel in several different ways. Always start with the pointer on the

cell where you want the answer displayed. Then do one of the following: (1) Enter an equal sign on the formula

bar (which is right after the fx), then write out an equation, like =(1.05)^3*100 to get 1.05 to the 3rd power times

1

13

14

15

16

17

18

24

25

26

27

FVN = =FV(0.05,3,0,-100) = $115.76

FVN = =FV(C15,C16,0,C14) = $115.76

28

29

32

33

34

35

36

37

38

39

01.0000 1.0000 1.0000 1.0000

21.0000 1.1025 1.2100 1.4400

31.0000 1.1576 1.3310 1.7280

51.0000 1.2763 1.6105 2.4883

61.0000 1.3401 1.7716 2.9860

54

91.0000 1.5513 2.3579 5.1598

40

41

42

45

48

51

52

57

A B C D E F G H I J K L M N O P

Table 5.1 Summary of Future Value Calculations

Investment = CF0 = PV = -$100.00

Interest rate = I = 5.00%

No. of periods = N = 3

Periods: 0 1 2 3

| | | |

35-$100.00 $0

Excel Approach: FV function:

FVN = =FV(rate,nper,pmt,pv,type)

The Compounding Process: A Graphic View

Data for Figure 5.1

Periods (n)

11.0000 1.0500 1.1000 1.2000

41.0000 1.2155 1.4641 2.0736

71.0000 1.4071 1.9487 3.5832

81.0000 1.4775 2.1436 4.2998

then the PV. The data can be entered as fixed numbers or as cell references.

Interest Factors, FVIFi,n

Interest Rate (i)

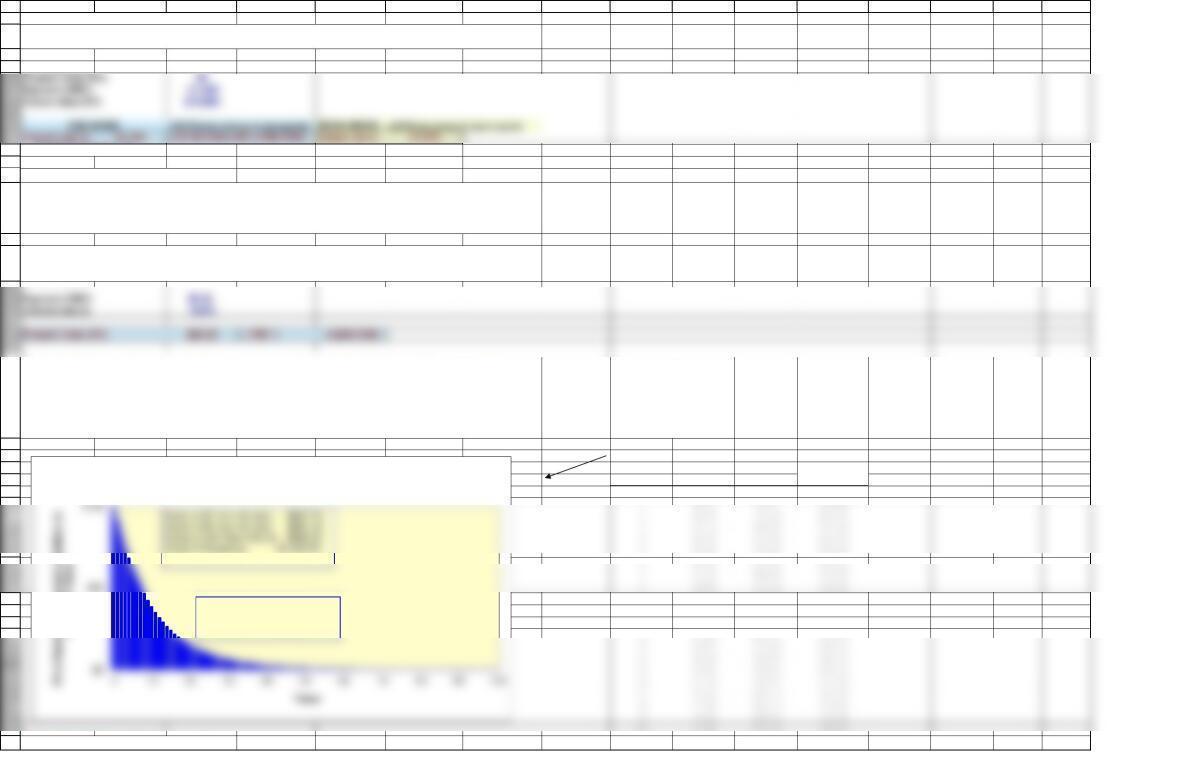

Figure 5.1 (shown below) shows how a $1 investment grows over time at different interest rates. The curves

were created by solving for FV at different values for N and I. This allows you to simultaneously see the effects

of varying time and the interest rate.

The data table used to create this figure is shown to the right. For instruction on data tables and graphs, refer

to the Excel Tutorial.

Figure 5.1 Growth of $1 at Various Interest Rates and Time Periods

1.00

2.00

5.00

6.00

Future Value

of $1

I= 20%

I= 0%

I= 5%

2

19

58

59

60

61

62

63

64

65

66

67

68

69

78

81

82

83

84

85

86

87

88

89

90

15 1.0000 0.4810 0.2394 0.0649

20 1.0000 0.3769 0.1486 0.0261

25 1.0000 0.2953 0.0923 0.0105

35 1.0000 0.1813 0.0356 0.0017

40 1.0000 0.1420 0.0221 0.0007

45 1.0000 0.1113 0.0137 0.0003

91

92

95

99

103

104

105

A B C D E F G H I J K L M N O P

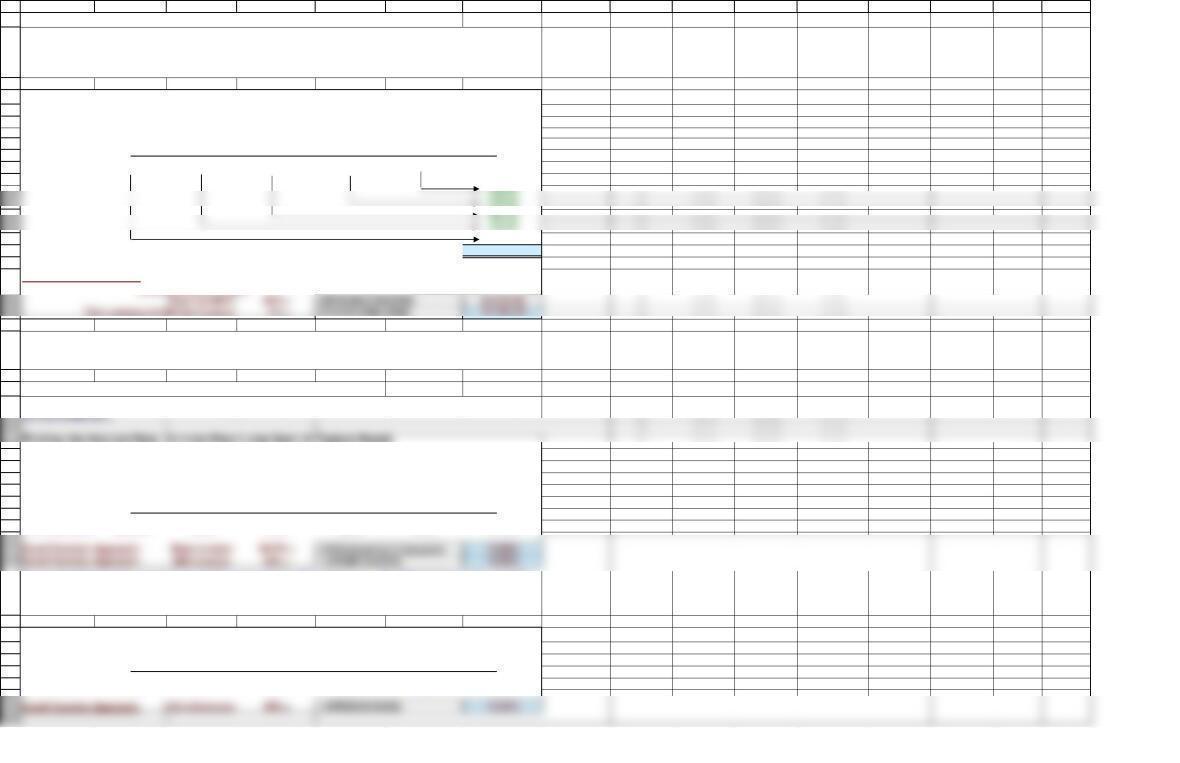

PRESENT VALUES (Section 5-3)

Table 5.2 Summary of Present Value Calculations

Future payment = CFN = FV = $115.76

Interest rate = I = 5.00%

No. of periods = N = 3

Periods: 0 1 2 3

| | | |

Cash Flow Time Line: PV = ? $115.76

Excel Approach: PV function:

PV = =PV(rate,nper,pmt,fv,type)

The Discounting Process: A Graphic View

Figure 5.2 Present Value of $1 at Various Interest Rates and Time Periods

Data for Figure 5.2

Periods (n)

0.8638 0% 5% 10% 20%

10 1.0000 0.6139 0.3855 0.1615

30 1.0000 0.2314 0.0573 0.0042

50 1.0000 0.0872 0.0085 0.0001

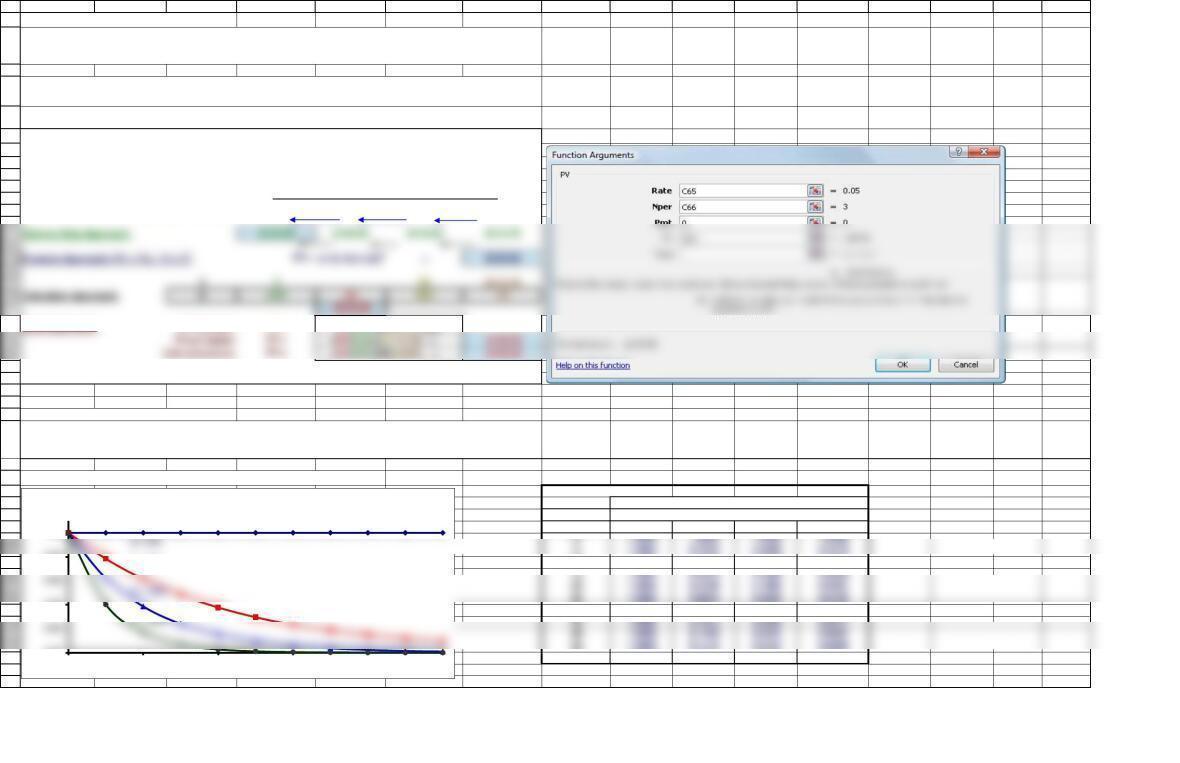

The present value is the opposite of the future value. Instead of compounding a value forward, you discount it

back. If you know the PV, you can compound to find the FV, while if you know the FV, you can discount to find

the PV.

In the Excel formula, 0 indicates that there are no intermediate cash flows.

You must make a payment of $115.76 in 3 years. If a bank pays a guaranteed 5% interest rate each year, how

much would you need to deposit now to have $115.76 in 3 years?

You can work this problem in the same ways that we discussed above.

Figure 5.2 shows how a $1 payment in the future has a lower and lower present value as the interest rate and

time until receipt increase. The data table to the right provides the data used to draw the figure.

Interest Factors, PVIFi,n

Interest Rate (i)

0.00

0.40

0.80

1.00

010 20 30 40 50

Present Value

of $1

Periods

I= 5%

3

106

107

108

109

114

115

116

117

118

Future value (FV) $1,000,000

Interest rate (I) 4.50%

119

120

125

126

127

128

129

130

134

135

136

137

138

141

142

139

149

150

151

155

156

A B C D E F G H I J K L M N O P

FINDING THE INTEREST RATE, I (Section 5-4) This calculation assumes that the 1st interest payment will come in 1 year. If not true, use Excel’s Yield function.

Present value (PV) -$100.00

FINDING THE NUMBER OF YEARS, N (Section 5-5)

Present value (PV) -$500,000

FUTURE VALUE OF AN ORDINARY ANNUITY (Section 5-7)

Table 5.3 Summary: Future Value of an Ordinary Annuity

Periods: 0 1 2 3

| | | |

Cash Flow Time Line: -$100 -$100 -$100

Step-by-Step Approach:

Multiply each payment by -$100.00

35$0 -$100.00

Calculator Approach: NI/YR PV PMT FV

$315.25

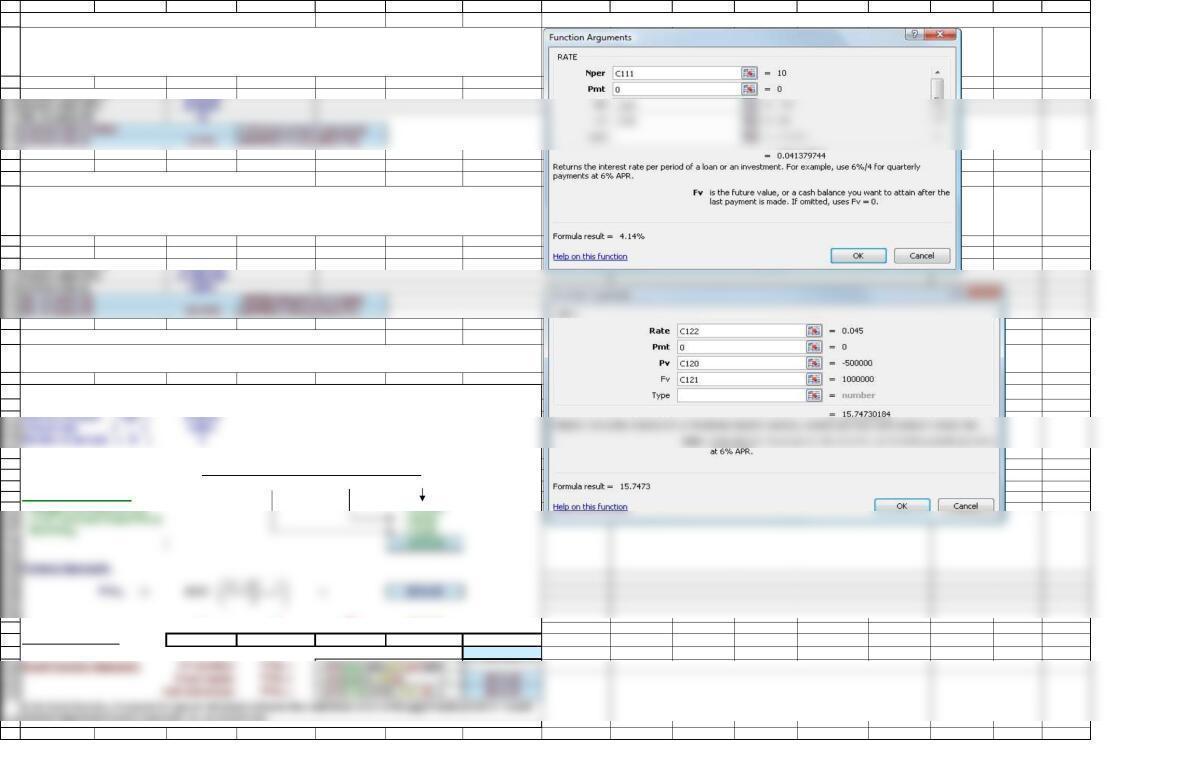

Sometimes we need to know how long it will take to accumulate a given sum of money, given our beginning

funds and the rate we will earn on those funds. For example, suppose we believe that we could retire

comfortably if we had $1 million, and we want to find how long it will take us to reach that goal, assuming that we

now have $500,000 invested at 4.5%.

An ordinary annuity has regular, periodic payments that occur at the end of each period. Methods for solving the

future value of an ordinary annuity are shown below.

Previously, we solved equations to find FV and PV. However, we could just as easily solve for I or N. For

example, suppose we know that a given bond has a cost of $100 and that it will return $150 after 10 years. It

makes no annual payments, so PMT = 0. Thus, we know PV, FV, and N, and we want to find the rate of return we

would earn if we bought the bond.

4

Future value (FV) $150.00

No. of years (N) 10

157

158

159

160

165

166

167

168

169

174

175

176

179

180

181

182

187

188

189

190

191

192

193

194

195

200

202

Interest rate = I = 5.00%

Periods: 0 1 2 3

| | | |

Cash Flow Time Line: -$100 -$100 -$100

196

203

208

209

213

214

A B C D E F G H I J K L M N O P

FUTURE VALUE OF AN ANNUITY DUE (Section 5-8)

Summary: Future Value of an Annuity Due (Diagram Not in Text)

Periods: 0 1 2 3

| | | |

Cash Flow Time Line: -$100 -$100 -$100

Formula Approach:

BEG MODE 350-$100.00

Calculator Approach: NIPV PMT FV

$331.01

PRESENT VALUE OF AN ORDINARY ANNUITY (Section 5-9)

Summary: Present Value of an Ordinary Annuity

Payment amount = PMT = $100.00

Formula Approach:

35-$100.00 0

The present value of an ordinary annuity is the sum of the PVs of the individual cash flows. Methods for solving

the present value of an ordinary annuity are shown below.

An annuity due also has regular, periodic payments, but unlike an ordinary annuity, the payments occur at the

beginning of each period.

In the Excel formula, the 1 at the end of the formula indicates that cash flows occur at the beginning of each period. A 0 or

no entry (blank) would indicate end-of-period payments, i.e., an ordinary annuity.

−

1

1

N

N

5

161

Payment amount = PMT = $100.00

Interest rate = I = 5.00%

Number of periods = N = 3

215

222

A B C D E F G H I J K L M N O P

Calculator Approach: NIPV PMT FV

6

216

223

224

225

226

227

231

232

233

234

235

236

246

240

241

242

247

248

Excel Function Approach:

Interest rate (I) 6%

Present value (PV) $0

Future value (FV) $10,000

252

253

254

255

256

257

258

259

260

261

265

268

269

270

271

272

273

274

275

A B C D E F G H I J K L M N O P

PRESENT VALUE OF AN ANNUITY DUE (Not in Text)

Summary: Present Value of an Annuity Due (Not in text; this is a “bonus”)

Periods: 0 1 2 3

| | | |

Cash Flow Time Line: -$100 -$100 -$100

Step-by-Step Approach: -$100.00

Formula Approach:

Calculator Approach: NIPV PMT FV

$285.94

Excel entries correspond with these calculator keys: I N PMT FV TYPE PV

FINDING ANNUITY PAYMENTS, PERIODS, AND INTEREST RATES (Section 5-10)

FINDING ANNUITY PAYMENTS, PMT

No. of years (N) 5

FINDING THE NUMBER OF PERIODS, N

Interest rate (I) 6%

Present value (PV) $0

The difference between the present value of an ordinary annuity and an annuity due is that payments are

received earlier in an annuity due.

Fundamentally, this section is no different than previous TVM exercises. When solving for PMT, N, or I, you

must be given values for the other variables, and then you solve the problem.

For the preceding question, suppose you decide to make end-of-year deposits, but you can only save $1,200 per

year. Again assuming that you would earn 6%, how long would it take you to reach your $10,000 goal?

Suppose we need to accumulate $10,000 and have it available 5 years from now. Suppose further that we can

earn a return of 6% on our savings, which are currently zero.

Trick question: Notice the problem setup didn’t specify when payments would be made. Therefore, consider

both possibilities (END and BEGIN modes).

Question: The PV of the annuity due is larger than the PV of the ordinary annuity. Why is that? Answer:

Because each of the annuity due’s payments is discounted back one less year.

I)(1

1

1

N

+

−

7

A B C D E F G H I J K L M N O P

8

656.45 435.53 564.25

751.32 486.84 512.93

846.65 533.49 466.28

Payment (PMT) $2.50

Interest rate (I) 10.0%

Present Value (PV) $25.00 = PMT/ I =C299/C300

Present value (PV) $0

Payment (PMT) -$1,200

Future value (FV) $10,000

Interest rate (I) 25.78% =RATE(C285,C287,C286,C288) Interest rate (I) 17.54%

12 31.86 681.37 318.40

13 28.97 710.34 289.44

14 26.33 736.67 263.10

15 23.94 760.61 239.16

16 21.76 782.37 217.40

17 19.78 802.16 197.62

18 17.99 820.14 179.63

19 16.35 836.49 163.28

282

283

284

285

292

293

294

295

296

297

304

305

306

307

308

309

314

318

319

320

329

330

A B C D E F G H I J K L M N O P

FINDING THE INTEREST RATE, I

No. of years (N) 5

Would be tough to do!

PERPETUITIES (Section 5-11)

Annuity PMT 100

Interest Rate 10%

Pmt # PV this PMT Ann Value

0100.00

562.09 379.08 620.69

942.41 575.90 423.87

10 38.55 614.46 385.32

11 35.05 649.51 350.27

20 14.86 851.36 148.42

UNEVEN CASH FLOWS (Section 5-12) 21 13.51 864.87 134.90

Perpetuities are securities that promise to make payments forever. The present value of a perpetuity can be

found with a simple formula: Value = PMT / I . Note that we do not attempt to calculate the future value of a

perpetuity. Because the payments go on forever, the future value would be infinitely large and thus

meaningless.

Consider a preferred stock that pays a $2.50 annual dividend. If we assume that the company will go on

indefinitely, the preferred stock can be valued as a perpetuity. If the discount rate is 10%, what is the value of the

preferred stock?

Contribution to

100yr Ann Value

Now suppose you can only save $1,200 annually, but you still must have $10,000 in only 5 years. What rate of

return would you have to earn to achieve your goal?

An annuity makes constant payments, those payments are discounted, and the longer before a payment is

received, the smaller its PV. Therefore, adding more payments to the security adds less value for each additional

payment. This helps explain why perpetuities’ present values are finite, while future values are infinite. To see

this better, consider the figure shown below. The data used to construct the graph are shown to the right in

columns I through L. One hundred payments are analyzed and their present values, the total value of an annuity

of N number of years, and the contribution of the Nth payment are all shown in the table off to the right.

Annuity’s Value

Contribution of Each $100 Payment to the Value of a $100 Annuity

at a 10% Rate

Bars indicate PV of each

payment. Sum of PVs from 0 to

N = Value of the Annuity

9

190.91 90.91 908.86

282.64 173.55 826.22

375.13 248.69 751.09

468.30 316.99 682.79

A B C D E F G H I J K L M N O P

An annuity has constant payments. Although many financial decisions do involve annuities, many others

involve uneven, or nonconstant, cash flows. With a spreadsheet, the present value of a series of uneven cash

10

335

336

337

338

339

340

341

342

343

344

345

348

349

350

213.53 59 0.361 996.39 3.38

190.66 60 0.328 996.72 3.06

PV ==PV(C337,G339,C341,G342,0) $927.90 44 1.51 984.91 14.86

47 1.134 988.66 11.11

283.71 61 0.299 997.01 2.76

351

352

357

358

359

360

361

362

363

364

365

366

367

371

69 0.139 998.61 1.165

372

373

376

A B C D E F G H I J K L M N O P

Summary: Uneven Cash Flow Present Value Calculations (Annuity plus Lump Sum) 26 8.39 916.09 83.68

This is the cash flow pattern for a typical bond. 27 7.63 923.72 76.05

Interest rate (I) = 12% 28 6.93 930.66 69.12

29 6.30 936.96 62.81

Periods: 0 1 2 3 4 5 30 5.73 942.69 57.08

| | | | ||31 5.21 947.90 51.87

Annuity CFs: $0 $100 $100 $100 $100 $100 32 4.74 952.64 47.13

Lump sum CFs:

$1,000 33 4.31 956.94 42.83

Total CFs: $0 $100 $100 $100 $100 $1,100 34 3.91 960.86 38.91

PV of CFs 35 3.56 964.42 35.36

$89.29 36 3.23 967.65 32.12

63.55 39 2.43 975.70 24.08

624.17 40 2.21 977.91 21.87

$927.90 = PV of cash flow stream = value of the asset 41 2.01 979.91 19.86

42 1.83 981.74 18.03

Excel Function Approach:

Fixed inputs:

PV ==PV(0.12,5,-100,-1000) $927.90 43 1.66 983.40 16.37

48 1.031 989.69 10.08

Figure 5.3 PV of an Uneven Cash Flow Stream 49 0.937 990.63 9.14

50 0.852 991.48 8.29

Interest rate (I) = 12% 51 0.774 992.26 7.52

52 0.704 992.96 6.81

Periods: 0 1 2 3 4 5 53 0.640 993.60 6.17

| | | | ||54 0.582 994.18 5.59

CF Time Line: $0 $100 $300 $300 $300 $500 55 0.529 994.71 5.06

PV of CFs 56 0.481 995.19 4.58

$89.29 57 0.437 995.63 4.14

239.16 58 0.397 996.03 3.75

$1,016.35 = PV of cash flow stream = value of the asset 62 0.271 997.29 2.49

63 0.247 997.53 2.24

64 0.224 997.76 2.02

67 0.169 998.31 1.46

The NPV Excel formula ignores the initial cash flow (in Year 0). When entering a cash flow range, Excel assumes

The time line shows what’s happening with a step-by-step solution. To actually work the problem with a

calculator, use the cash flow register. With Excel, use the NPV function. Could use the NPV dialog box.

Alternatively, type, just to the right of the fx, =NPV( see the formula, and make the cell entries by clicking on

them. This also works for the PV or any other function.

11

79.72 37 2.94 970.59 29.18

71.18 38 2.67 973.27 26.51

379

380

381

382

383

384

385

386

387

388

389

394

395

96 0.011 999.89 -0.121

396

397

400

401

402

403

406

407

408

409

410

411

412

413

417

418

419

420

421

422

423

A B C D E F G H I J K L M N O P

FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM (Section 5-13) 70 0.127 998.73 1.038

71 0.115 998.85 0.923

72 0.105 998.95 0.819

Figure 5.4 FV of an Uneven Cash Flow Stream 73 0.095 999.05 0.724

74 0.086 999.14 0.637

Interest rate (I) = 12% 75 0.079 999.21 0.558

76 0.071 999.29 0.487

Periods: 0 1 2 3 4 5 77 0.065 999.35 0.422

| | | | ||78 0.059 999.41 0.363

CF Time Line: $0 $100 $300 $300 $300 $500 79 0.054 999.46 0.309

$500.00 80 0.049 999.51 0.260

0.00 85 0.030 999.70 0.075

= FV of cash flow stream $1,791.15 86 0.028 999.72 0.048

87 0.025 999.75 0.023

88 0.023 999.77 0.000

91 0.017 999.83 -0.057

92 0.016 999.84 -0.072

93 0.014 999.86 -0.086

SOLVING FOR I WITH UNEVEN CASH FLOWS (Section 5-14) 94 0.013 999.87 -0.099

Finding the Interest Rate, Annuity Plus Lump Sum (A Typical Bond) 97 0.010 999.90 -0.131

98 0.009 999.91 -0.140

Annuity pmts $100 99 0.008 999.92 -0.148

Future lump sum

$1,000 100 0.007 999.93 -0.155

Periods: 0 1 2 3 4 5

| | | | ||

CF Time Line: -$927.90 $100 $100 $100 $100 $1,100

Finding the Interest Rate of an Uneven Cash Flow Stream with a Cost of $1,000

Periods: 0 1 2 3 4 5

| | | | ||

CF Time Line: -$1,000 $100 $300 $300 $300 $500

To use the Rate function, we need an annuity or an annuity with a lump sum. The IRR function can be used for

any set of uneven cash flows, provided the first one is negative. (You need an investment to find the rate of

return on the investment.) See the next example, where the IRR approach is required.

Assume that an investment with the following positive cash flows has a cost of $927.90. Find the rate of return

We find the future value of uneven cash flow streams by compounding rather than discounting. The step-by-

step approach works the same as for PVs, but unfortunately, Excel does not have a net future value (NFV)

function. One way around this is to solve for the NPV and then find the FV of this amount by compounding it to

the end of the cash flow stream.

The FV result using the Excel formulas is a negative number. This is because we used Excel’s FV function and

entered the NPV as a positive value as the PV. Put a minus sign in just after the equal sign to make the answer

positive.

Excel Function Approach: (Some versions of Excel do not have a NFV function, requiring the

procedure shown here.)

12

427

428

429

430

431

432

439

440

441

442

443

444

445

446

452

453

454

455

462

463

464

465

466

467

468

469

475

A B C D E F G H I J K L M N O P

SEMIANNUAL AND OTHER COMPOUNDING PERIODS (Section 5-15)

Periods/Year 1 2

N10 20 = 2 × 10

N40 N120 N3650

I1.25% I0.417% I0.0137%

N10 N20

COMPARING INTEREST RATES (Section 5-16)

The future value under semiannual compounding, $163.86, exceeds the FV under annual compounding, $162.89,

because interest starts accruing sooner and thus produces more interest on interest.

This can be further illustrated by considering the example of quarterly, monthly, and daily compounding.

Using the Excel function, if the nominal rate is 10% with semiannual compounding, the effective annual rate is:

SEMIANNUAL

Assume that you deposit $100 in an account that pays 5% and leave it there for 10 years. Here’s what would

happen under annual and semiannual compounding. Notice that with semiannual compounding, there are twice

as many periods, but the periodic interest rate is half the nominal rate.

ANNUAL COMPOUNDING

SEMIANNUAL COMPOUNDING

QUARTERLY

MONTHLY

DAILY

Different compounding periods are used for different types of investments. If we compare investments or loans

with different compounding periods, we need to put them on a common basis. Excel has a function that solves

for the effective annual rate by using the following formula:

Just as more frequent compounding increases the future value of a lump sum, it also decreases the present

value of a lump sum. Consider the example of $100 to be received 10 years from now, with annual versus

semiannual compounding and a 10% interest rate.

ANNUAL

1 –

M

I

1 (EFF%) rate annual Effective

M

NO M

+=

13

Table 5.4 Loan Amortization Schedule, $100,000 at 6% for 5 Years

3$63,456.34 $23,739.64 $3,807.38 $19,932.26 $43,524.08

4$43,524.08 $23,739.64 $2,611.44 $21,128.20 $22,395.89

5$22,395.89 $23,739.64 $1,343.75 $22,395.89 $0.00

476

477

478

479

480

491

492

493

494

495

496

497

498

499

500

501

507

508

509

510

511

512

513

514

515

516

521

522

A B C D E F G H I J K L M N O P

FRACTIONAL TIME PERIODS (Section 5-17 )

Amount borrowed $100

Days in year 365

Nominal interest rate 10.00%

AMORTIZED LOANS (Section 5-18)

N5

I6%

PV $100,000

Amount borrowed: $100,000

Years: 5

Rate: 6%

PMT: -$23,739.64

Beginning

Repayment of

Ending Balance

Amount Payment InterestaPrincipalbBalance

Year (1) (2) (3) (4) (5)

1$100,000.00 $23,739.64 $6,000.00 $17,739.64 $82,260.36

2$82,260.36 $23,739.64 $4,935.62 $18,804.02 $63,456.34

Table 5.4 (shown below) illustrates the amortization process. A homeowner borrows $100,000 on a mortgage

loan, and the loan is to be repaid in 5 equal payments at the end of each of the next 5 years. The lender charges

6% on the balance at the beginning of each year.

b Repayment of principal is equal to the payment of $23,739.64 minus the interest charge for the year.

Bank loans are often for fractional periods. Say you borrow $100 on January 2, 2019 and plan to repay the loan

on October 3, 2019. The loan has a rate of 10% and is based on a 365-day year. Interest is earned (charged) on a

daily basis, and is compounded. How much will you have to pay when the loan matures? Assume (a) simple

interest and (b) compound interest.

forth.

First, we solve for the required payment, then we construct an amortization table.

If a loan is to be repaid in equal amounts on a monthly, quarterly, or annual basis it is said to be an amortized

loan.

14

Rate per day. Fraction, not % 0.000273973 =C480/C479

Number of days: 274

Simple interest, cost per day: $0.02740 =C478*C481

Total interest: $7.51 =C484*C482

Ending amount: $107.51 =C478+C485

Rate per day: 0.000273973 =C481

1

2

3

4

5

6

15

16

PMT $0 FV = $150.00

10

11

12

13

17

18

19

20

21

22

23

3b. How would your answer change if the interest rate were 5%, or 6%, or 20%?

24

32

33

34

35

36

37

PMT $0 FV ($M) = $215.89

43

44

I5%

PMT $0 FV = $131.50

38

39

40

41

45

A B C D E F G H

SECTION 5-2 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N5

N5Annual interest $10.00

N3

I4%

PV $2,000

PMT $0 FV = $2,249.73

N10

I8%

N100

4. A company’s sales in 2019 were $100 million. If sales grow at 8%, what will they be 10

years later, in 2029?

5a. How much would $1, growing at 5% per year, be worth after 100 years?

2a. What would the future value of $100 be after 5 years at 10% compound interest?

2b. At 10% simple interest?

3a. Suppose you currently have $2,000 and plan to purchase a 3-year certificate of deposit

(CD) that pays 4% interest compounded annually. How much will you have when the CD

matures?

15

46

47

48

N100

5b. What would FV be if the growth rate were 10%?

PMT $0 FV = $161.05 =FV(B7,B6,B9,-B8)

1

2

3

4

5

6

7

I4%

10

11

12

13

I6%

17

18

19

20

24

25

26

27

28

N100

31

32

33

A B C D E F G H

SECTION 5-3 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N3

I4%

N5

N5

N100

I5%

4b. If the discount rate was 20%?

3a. Suppose a U.S. government bond promises to pay $2,249.73 three years from now. If the

going interest rate on 3-year government bonds is 4%, how much is the bond worth today?

3b. How would your answer change if the bond matured in 5 rather than 3 years?

3c. What if the interest rate on the 5-year bond was 6% rather than 4%?

4a. How much would $1,000,000 due in 100 years be worth today if the discount rate was 5%?

17

1

2

3

4

5

6

10

11

12

13

14

PMT $0

18

19

20

PMT $0

24

25

26

27

PMT $0

31

32

33

34

A B C D E F G H

SECTION 5.4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N10

N10

PMT $0

N10

N10

N10

2b. If EPS in 2017 had been $2.40 rather than $3.08, what would the growth rate have been?

1a. The U.S. Treasury offers to sell you a bond for $585.43. No payments will be made until the

bond matures 10 years from now, at which time it will be redeemed for $1,000. What interest rate

would you earn if you bought this bond for $585.43?

1b. What rate would you earn if you could buy the bond for $550?

1c. For $600?

2a. Microsoft earned $1.42 per share in 2007. Ten years later, in 2017, it earned $3.08. What was

the growth rate in Microsoft’s earnings per share (EPS) over the 10-year period?

18

PMT $0

1

2

3

4

5

6

10

11

12

13

17

18

19

20

A B C D E F G H

SECTION 5-5 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

I6%

I10%

I8.05%

1a. How long would it take $1,000 to double if it were invested in a bank that pays 6% per year?

1b. How long would it take if the rate was 10%?

2a. Microsoft’s 2017 earnings per share were $3.08, and its growth rate during the prior 10 years was

8.05% per year. If that growth rate was maintained, how long would it take for Microsoft’s EPS to

double?

19

1

2

3

4

5

10

11

12

13

14

15

16

PV $0 Val of Pmt $100.00 =FV(B14,F14,,B15)

17

18

19

20

21

22

23

29

30

34

35

N5

I6%

PMT -$2,500

PV $0 FV $14,092.73 =FV(B28,B27,B29,-B30)

N5

I3%

PMT -$2,500

PV $0

24

25

26

A B C D E F G H

SECTION 5-7 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

N5

I10% Years of interest 0

N5

I4%

PMT -$2,500

PV $0 FV $13,540.81 =FV(B21,B20,B22,-B23)

1a. For an ordinary annuity with 5 annual payments of $100 and a 10% interest rate, how many

years will the 1st payment earn interest, and what will this payment’s value be at the end?

1b. Answer this same question for the 5th payment.

2a. Assume that you plan to buy a condo 5 years from now, and you estimate that you can save

$2,500 per year. You plan to deposit the money in a bank that pays 4% interest, and you will make

the first deposit at the end of the year. How much will you have after 5 years?

2b. How will your answer change if the interest rate is increased to 6%, or lowered to 3%?

20

N5

I10% Years of interest 4

PV $0 Val of Pmt $146.41 =FV(B7,F7,,B8)