CHAPTER 4: CONSUMPTION, SAVING, AND INVESTMENT

LEARNING OBJECTIVES

I. Goals of Chapter 4

A. Examine the factors that underlie economywide demand for goods and

services

B. Assumes closed economy (for now, dropped in Chapter 5)

C. Focuses on consumption and investment

TEACHING NOTES

I. Consumption and Saving (Sec. 4.1)

People think about the present vs. the future in choosing saving and consumption

1. Increase in current income: both consumption and saving increase

A. The consumption and saving decision of an individual.

1. The rate a person trades off current and future consumption depends

on the real interest rate prevailing in the economy.

Consumption, Saving, and Investment 53

Theoretical Application

The classic discussions of consumption are the permanent-income hypothesis of Milton

Friedman (A Theory of the Consumption Function, Princeton: Princeton University

3. Keynesian consumption function: Cd = c0 +cyY (4.2)

a. Desired consumption depends on current aggregate output

Data Application

Recall from Chapter 2 that measured consumption in the national income accounts

includes spending on durable consumption goods, like autos and major appliances. But

consumption theory, including the Keynesian consumption function, requires that

consumption be defined to include only the services from durable consumer goods. So

empirical researchers must adjust the national income data to arrive at a measure of

consumption that matches the theory. For example, they might assume that durable

goods provide services proportional to the stock of durables.

C. Effects of changes in expected future income.

1. Higher expected future income leads to more consumption today, so

after the recent recession of 2008-2009.

D. Effects of changes in wealth

1. Increase in wealth raises current consumption, so lowers current

saving

2. Application: The 1987 stock market crash and consumer spending.

When the stock market crashed in 1987, wealth declined by about

$100 billion. Consumption fell somewhat less than might be expected,

and it wasn’t enough to cause a recession. There was a temporary

54 Chapter 4

E. Effect of changes in the real interest rate

1. Increased expected real interest rate has two opposing effects

a. The income effect of the real interest rate reflects a positive

effect on saving, since rate of return is higher; greater reward for

2. Taxes and the real return to saving

a. Expected after-tax real interest rate: r!-t = (1- t)i –

π

e

Data Application

Eytan Sheshinski, in “Treatment of Capital income in Recent Tax Reforms and the Cost

of Capital in Industrialized Countries,” in Larry Summers, ed., Tax Policy and the

Economy 4, Cambridge, Mass.: MIT Press, 1990, pp. 25-42, finds that real after-tax

3. A Closer Look 4.1: interest rates

Discusses different interest rates, default risk, term structure, tax status

Numerical Problem 1 explores how changes in income, future income, wealth, and

interest rates affect consumption.

F. Fiscal policy

1. Affects desired consumption through changes in current and expected

future income

2. Directly affects desired national saving, Sd = Y – Cd – G

3. Government purchases (temporary increase)

a. Higher G financed by current taxes reduces after-tax income,

Consumption, Saving, and Investment 55

4. Taxes

a. Lump-sum tax cut today, financed by higher future taxes

Data Application

This theory is confirmed by empirical data. Shaghil Ahmed, in “Temporary and

Permanent Government Spending in an Open Economy: Some Evidence for the United

Kingdom,” Journal of Monetary Economics, March 1986, pp. 197-224, finds, using a

long time series of British data, that temporary government purchases indeed crowd out

consumption spending, even though the expenditures are useful in increasing the

marginal productivity of private capital and providing a substitute for consumption

goods.

(1) If future income loss exactly offset current income gain, no

change in consumption

Theoretical Application

There are a number of reasons why Ricardian equivalence may not hold. The text notes

that if people don’t see that future taxes are equal (in present value) to a current tax cut,

then Ricardian equivalence may not hold. An additional reason for the failure of

Ricardian equivalence, liquidity constraints, is covered in Chapter 8. It may also be

possible for people to avoid future taxes, even if they foresee them, by moving or dying;

II. Investment (Sec. 4.2)

A. Why is investment important?

1. Investment fluctuates sharply over the business cycle, so we need to

56 Chapter 4

1. Desired capital stock is the amount of capital that allows firms to earn

the largest expected profit

2. Desired capital stock

4. The user cost of capital

a. Example of Tony’s

Bakery: cost of

capital, depreciation

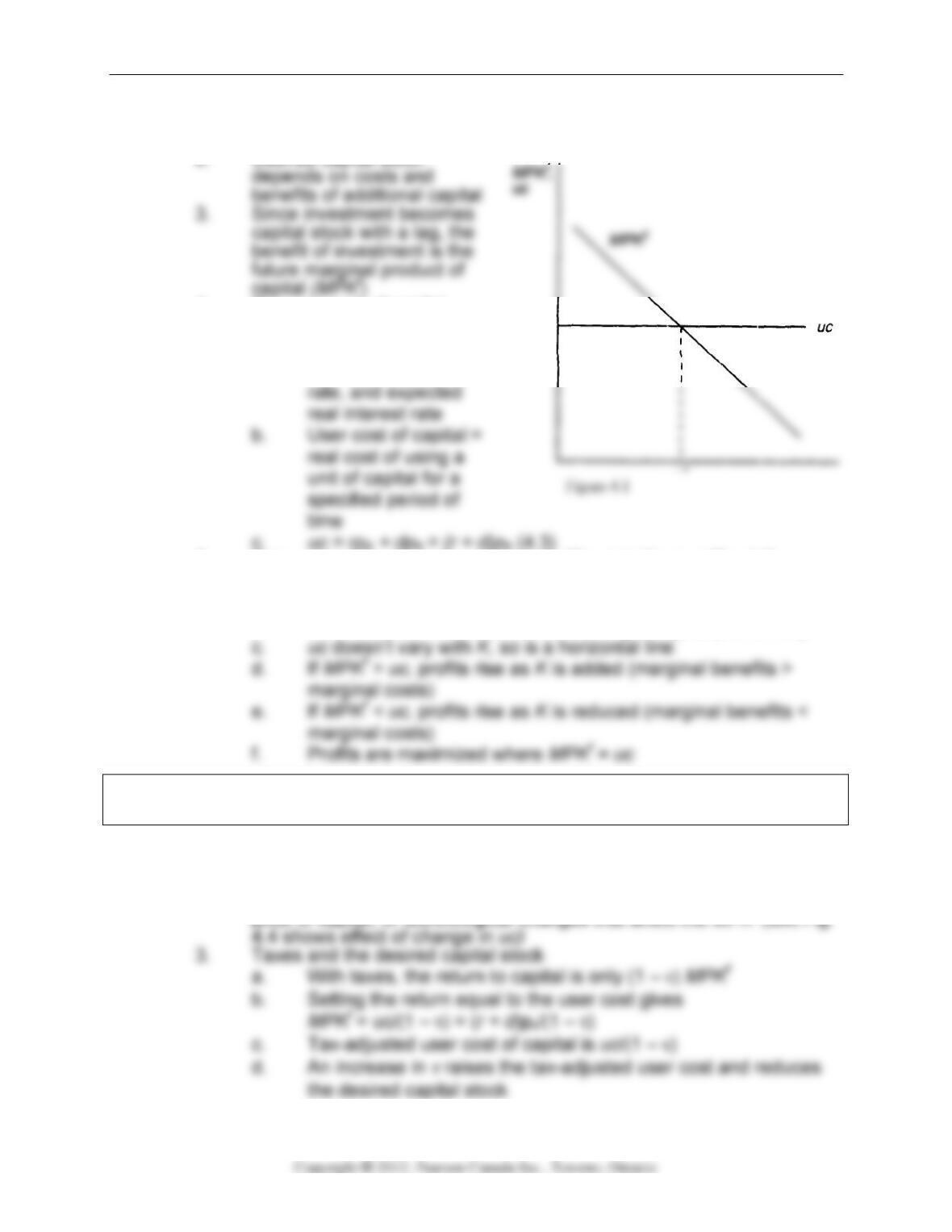

5. Determining the desired capital stock (Fig. 4.1; like text Fig. 4.3)

a. Desired capital stock is the level of capital stock at which MPKf

= uc

b. MPKf falls as K rises due to diminishing marginal productivity

See A Closer Look 4.2, “Investment and the Stock Market,” for an alternative method of

determining the desired stock of capital.

C. Changes in the desired capital stock

1. Factors that shift the MPKf curve or change the user cost of capital

cause the desired capital stock to change

2. These factors are changed in the real interest rate, depreciation rate,

Consumption, Saving, and Investment 57

Theoretical Application

The first general use of the user cost of capital concept was by Dale Jorgenson. “Capital

Theory and Investment Behavior,” American Economic Review Papers and

Proceedings, May 1963, pp. 247–259.

Numerical Problems 2 and 4 give students practice in working with the marginal product

of capital and the user cost of capital.

e. In reality, there are complications to the tax-adjusted user cost

(1) We assumed that firm revenues were taxed

(a) In reality, profits, not revenues, are taxed

Data Application

Another simplification that is used in this chapter is the assumption that taxes are based

on a firm’s real revenue. In reality, taxes on nominal revenue combine with inflation to

(5) Table 4.3 shows effective tax rates on capital across

sectors and over time in Canada,

D. Application: Measuring the effects of taxes on investment

1. Two problems in measuring tax effects: controlling for other influences

Theoretical Application

For a detailed discussion about the effects of tax policy on investment, see Chapter 24

in Rosen, Boothe, Dahlby, and Smith, Public Finance in Canada, Toronto: McGraw-Hill

Ryerson, 1999.

E. From the desired capital stock to investment

1. The capital stock changes from two opposing channels

a. New capital increases the capital stock; this is gross investment

58 Chapter 4

d. Text Fig. 4.6 shows gross and net investment for the Canada

from 1926–2009

2. Rewriting (4.5) gives It = Kt+1 – Kt + dKt

a. If firms can change their capital stocks in one period, then the

Theoretical Application

Acknowledging that it may take time to get capital in place may be crucial to modeling

the business cycle. See Finn E. Kydland and Edward C. Prescott, “Time to Build and

Numerical Problem 3 applies the user-cost concept to the purchase or rental of a home.

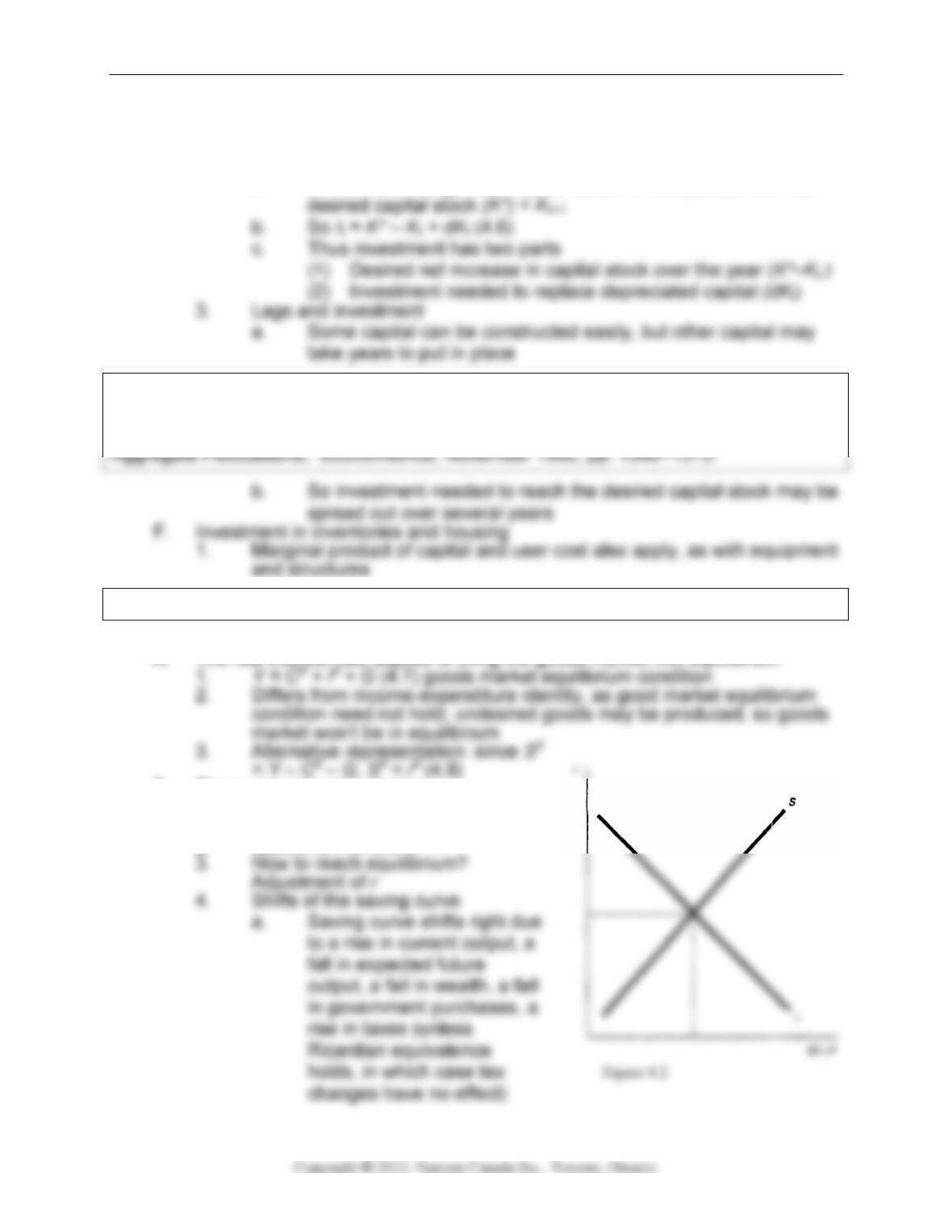

III. Goods Market Equilibrium (Sec. 4.3)

B. The saving-investment diagram

1. Plot Sd vs. Id (Fig. 4.2; Key

Diagram 3; like text Fig. 4.7

2. Equilibrium where Sd = /d

Consumption, Saving, and Investment 59

Numerical Problems 5 and 6 and Analytical Problem 5 examine what happens when

government spending changes.

Theoretical Application

What happens to the economy if government taxes change? Under Ricardian

equivalence a tax cut today that is financed by higher future taxes has no effect on

5. Shifts of the investment curve

a. Investment curve shifts right due to a fall in the effective tax rate

or a rise in expected future marginal productivity of capital (text

Figure 4.9)

b. Result of increased investment: higher r, higher S and /

Policy Application

Should tax policy be used to promote savings or investment? Many policymakers and

economists have argued that obtaining the correct amount of future economic growth

requires us to have a higher capital stock, so that we need more investment than we

have. They suggest tax policies like RRSPs to encourage saving and tax breaks for

60 Chapter 4

ADDITIONAL ISSUES FOR CLASSROOM DISCUSSIONS

1. Saving, Investment, and the Baby Boomers

Recently, saving has been relatively low in Canada compared to other countries and

other times. Is this because a large portion of the adult population was born in the late

1940s and the 1950s and these people are in the phase of life when they spend

heavily? Probably not.

Relatively few children were born during the Great Depression of the 1930s and World

War II in the first half of the 1940s. Shortly after the war ended, the birth rate rose and

stayed high for over 10 years. The children born during this period are called the “baby

boomers.”

2. Concern About the Level of Saving

While Canadian saving is not low by OECD standards, it is much lower than that of the

fast growing Asian economies. On average high savings countries tend to be high

growth countries.

Consumption, Saving, and Investment 61

3. What Should Be Included in Investment?

Investment is the sum of business fixed investment (structures and equipment),

residential investment, and the change in inventories. But if investment is the purchase

of goods and services that will increase productive capacity in the long run, then several

important categories, such as education, are left out.

Spending on education, infrastructure, and health and nutrition programs should be

included in investment. People are frequently the crucial factor in determining whether

an enterprise is successful or not. When businesses, individuals, and government

spend money on education, they are helping to increase human productivity and thus

4. Housing as an Investment Good

Residential construction, which is just investment in housing (including apartment

buildings) represents a large component of total fixed investment in Canada. For

instance, in Table 2.1 of the text, it is shown that for 2006 residential construction

62 Chapter 4

What particular aspects of the investment decision are specific to housing investment?

One is that housing investment is exceptionally sensitive to movements in interest rates.

One reason for this is that depreciation in housing in very low at annual rates. This

make the user-cost of capital very sensitive to the interest rate. Generally we see that

Consumption, Saving, and Investment 63

ANSWERS TO TEXTBOOK PROBLEMS

Review Questions

1. Saving is current income minus consumption. For given income, any increase in

2. When a consumer gets an increase in current income, both current consumption

and future consumption increase. Since current consumption rises, but by less

than the increase in current income, saving increases. When the consumer gets an

increase in expected future income, again both current and future consumption

3. The effect on desired saving of an increase in the expected real interest rate is

potentially ambiguous. An increase in the real interest rate has two effects on

desired saving: (1) the substitution effect increases saving, because the amount of

future consumption that can be obtained in exchange for giving up a unit of current

4. When government purchases increase temporarily, consumers see that higher

taxes will be required in the future to pay off the deficit. They reduce both current

consumption and future consumption, but current consumption declined by less