Chapter 4: Analysis of Financial Statements

Learning Objectives

49

Chapter 4

Analysis of Financial Statements

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Explain what ratio analysis is.

◆ List the five groups of ratios and identify, calculate, and interpret the key ratios in each group.

◆ Discuss each ratio’s relationship to the balance sheet and income statement.

◆ Discuss why return on equity (ROE) is the key ratio under management’s control and how the other

ratios impact ROE, and explain how to use the DuPont equation for improving ROE.

◆ Compare a firm’s ratios with those of other firms (benchmarking) and analyze a given firm’s ratios

over time (trend analysis).

◆ Discuss the tendency of ratios to fluctuate over time (which may or may not be problematic); explain

how they can be influenced by accounting practices as well as other factors; and explain why they

must be used with care.

50

Lecture Suggestions

Chapter 4: Analysis of Financial Statements

Lecture Suggestions

Chapter 4 shows how financial statements are analyzed to determine the firm’ strengths and weaknesses.

Based on this information, management can take actions to exploit the firm’s strengths and correct its

weaknesses.

At Florida, we find a significant difference in preparation between our accounting and non-

accounting students. The accountants are relatively familiar with financial statements, and they have

covered in depth in their financial accounting course many of the ratios discussed in Chapter 4. We pitch

our lectures to the non-accountants, which means concentrating on the use of statements and ratios, and

DAYS ON CHAPTER: 3 OF 56 DAYS (50–minute periods)

Chapter 4: Analysis of Financial Statements

Answers and Solutions

51

Answers to End-of–Chapter Questions

4-1 The emphasis of the various types of analysts is by no means uniform nor should it be.

Management is interested in all types of ratios for two reasons. First, the ratios point out

weaknesses that should be strengthened; second, management recognizes that the other parties

4-2 The inventory turnover ratio is important to a grocery store because of the much larger inventory

required and because some of that inventory is perishable. An insurance company would have

4-3 Given that sales have not changed, a decrease in the total assets turnover means that the

company’s assets have increased. Also, the fact that the fixed assets turnover ratio remained

4-4 Differences in the amounts of assets necessary to generate a dollar of sales cause asset turnover

ratios to vary among industries. For example, a steel company needs a greater number of

4-5 Inflation will cause earnings to increase, even if there is no increase in sales volume. Yet, the

book value of the assets that produced the sales and the annual depreciation expense remain at

historic values and do not reflect the actual cost of replacing those assets. Thus, ratios that

compare current flows with historic values become distorted over time. For example, ROA will

increase even though the same assets are generating the same sales volume.

When comparing different companies, the age of the assets will greatly affect the ratios.

4-6 ROE is calculated as the return on assets multiplied by the equity multiplier. The equity

4-7 a. Cash, receivables, and inventories, as well as current liabilities, vary over the year for firms

with seasonal sales patterns. Therefore, those ratios that examine balance sheet figures will

vary unless averages (monthly ones are best) are used.

4-8 Firms within the same industry may employ different accounting techniques that make it difficult

to compare financial ratios. More fundamentally, comparisons may be misleading if firms in the

4-9 The three components of the DuPont equation are profit margin, assets turnover, and the equity

multiplier. One would not expect the three components of the discount merchandiser and high-

4-10 A review of Yahoo! Finance on 04/07/18 showed that the trailing twelve-month P/E ratio for

Alphabet Inc. (Google’s parent company) was 55.96 compared to 26.43 for Walmart. The P/E

ratio indicates how much investors are willing to pay per dollar of reported profits. Alphabet’s

4-11 ROE measures the rate of return on common stockholders’ investment, while ROIC measures the

rate of return to investors—both debtholders and common stockholders. Since ROE measures

Chapter 4: Analysis of Financial Statements

Answers and Solutions

53

4-12 Total Current Effect on

Current Assets Ratio Net Income

a. Cash is acquired through issuance of additional

common stock. + + 0

b. Merchandise is sold for cash. + + +

c. Federal income tax due for the previous year is paid. – + 0

d. A fixed asset is sold for less than book value. + + –

e. A fixed asset is sold for more than book value. + + +

j. Short-term notes receivable are sold at a discount. – – –

k. Marketable securities are sold below cost. – – –

l. Advances are made to employees. 0 0 0

m. Current operating expenses are paid. – – –

n. Short-term promissory notes are issued to trade creditors

in exchange for past due accounts payable. 0 0 0

o. 10-year notes are issued to pay off accounts payable. 0 + 0

54

Answers and Solutions

Chapter 4: Analysis of Financial Statements

Solutions of End-of-Chapter Problems

4-1 DSO = 23 days; S = $3,650,000; AR = ?

4-2 Since the firm’s M/B ratio = 1, then its total market value of equity is equal to its book value of equity.

Total invested capital = Debt + Equity

Total debt to total capital =

Equity Debt

Debt

+

4-3 ROA = 11%; PM = 6%; ROE = 23%; S/TA = ?; TA/E = ?

ROA = NI/TA; PM = NI/S; ROE = NI/E.

ROA = PM S/TA

NI/TA = NI/S S/TA

4-4 TA = $17,000,000,000; Cash and equivalents = $100,000,000; CL = $1,700,000,000; NP =

$1,000,000,000; LT debt = $10,200,000,000; CE = $5,100,000,000; Shares outstanding =

300,000,000; P0 = $20; EBITDA = $1,368,000,000; M/B = ?; EV/EBITDA = ?

Chapter 4: Analysis of Financial Statements

Answers and Solutions

55

M/B =

00.17$

00.20$

= 1.1765.

EV/EBITDA = (MVEquity + MVDebt + MVOther Claims – Cash and Equivalents)/EBITDA

4-5 EPS = $2.40; BVPS = $21.84; M/B = 2.7; P/E = ?

P/$21.84 = 2.7×

4-6 NI/S = 3%; TA/E = 1.9; Sales = $150,000,000; Assets = $60,000,000; ROE = ?

4-7 Given: Net income = $24,000; Common equity = $250,000

To calculate ROIC we need to find EBIT and total invested capital.

Step 1: To calculate EBIT, we use the income statement and calculate up the income statement

beginning with net income as follows:

EBIT $37,000 EBT + Int = $32,000 + $5,000

Interest 5,000 Given

Step 2: Calculate total invested capital as follows:

Notes payable $ 27,000

56

Answers and Solutions

Chapter 4: Analysis of Financial Statements

4-8 Step 1: Calculate total assets from information given.

Sales = $17 million.

3.2 = Sales/TA

3.2 =

Assets

000,000,17$

$451,562.50 = NI.

4-9

Calculate BEP:

ROA = 10%; Net income = $615,000; TA = ?

ROA =

TA

NI

Chapter 4: Analysis of Financial Statements

Answers and Solutions

57

Calculate ROE:

We need to determine common equity from total assets calculated above and the accounts

payable and accrual balance given in the problem.

Therefore, Debt + Equity = $5,200,000 = Total invested capital.

Debt = 0.4 × Total invested capital

Now, we can calculate ROE as follows:

4-10 Stockholders’ equity = $6,500,000,000; M/B = 2.0; P0 = ?

Total market value = $6,500,000,000 (2) = $13,000,000,000.

Market value per share = $13,000,000,000/180,000,000 = $72.22.

58

Answers and Solutions

Chapter 4: Analysis of Financial Statements

4-11 We are given ROA = 4% and Sales/Total assets = 1.3.

From the DuPont equation:

ROA = Profit margin Total assets turnover

4% = Profit margin(1.3)

4-12 TA = $12,000,000,000; T = 25%; EBIT/TA = 10%; ROA = 5.25%; TIE = ?

EBIT/$12,000,000,000 = 0.10

EBIT = $1,200,000,000.

NI/$12,000,000,000 = 0.0525

NI = $630,000,000.

4-13

Calculate TIE:

TIE = EBIT/INT, so find EBIT and INT.

Interest = $600,000 0.07 = $42,000.

Calculate ROIC:

4-14 ROE = Profit margin TA turnover Equity multiplier

= NI/Sales Sales/TA TA/Equity.

Now we need to determine the inputs for the DuPont equation from the data that were given.

On the left we set up an income statement, and we substitute values on the right:

Sales (given) $17,000,000

4-15 Currently, ROE is ROE1 = $15,000/$200,000 = 7.5%.

The current ratio will be set such that 2.5 = CA/CL. CL is $50,000, and it will not change, so

we can solve to find the new level of current assets: CA = 2.5(CL) = 2.5($50,000) = $125,000.

This is the level of current assets that will produce a current ratio of 2.5.

60

Answers and Solutions

Chapter 4: Analysis of Financial Statements

4-16 Known data:

TA = $3,000,000; Int. rate = 8%; T = 25%; BEP = 0.35 = EBIT/Total assets, so EBIT =

0.35($3,000,000) = $1,050,000; Equity = 0.7 × $3,000,000 = $2,100,000.

No Debt Debt = 30%

EBIT $1,050,000 $1,050,000

4-17 Statement a is correct. Refer to the solution setup for Problem 4-16 and think about it this way:

(1) Adding assets will not affect common equity if the assets are financed with debt. (2) Adding

assets will cause expected EBIT to increase by the amount EBIT = BEP(Added assets). (3)

Interest expense will increase by the amount Int. rate(Added assets). (4) Pre-tax income will rise

4-18 TA = $6,000,000,000; T = 25%; EBIT/TA = 11%; ROA = 6%; TIE ?

11.0

,000$6,000,000

EBIT

=

Chapter 4: Analysis of Financial Statements

Answers and Solutions

61

4-19 Present current ratio =

625,076,1$

2,5009,32$

= 2.22.

4-20 Step 1: Solve for current annual sales using the DSO equation:

71 = $205,000/(Sales/365)

71Sales = $74,825,000

4-21 The current EPS is $8,000,000/540,000 shares or $14.8148. The current P/E ratio is then

4-22 1. Total assets = Total liabilities and equity = $300,000.

62

Answers and Solutions

Chapter 4: Analysis of Financial Statements

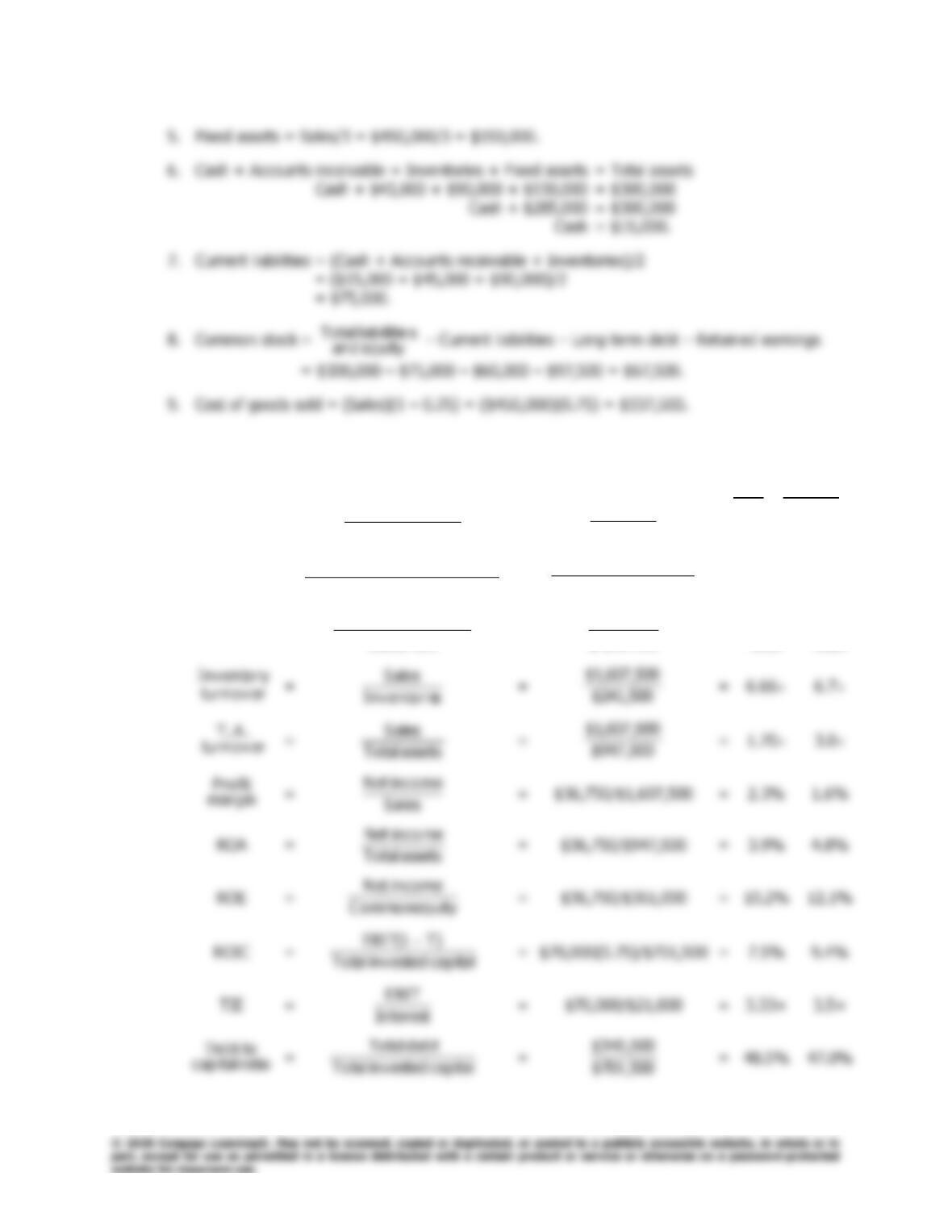

4-23 a. (Dollar amounts in thousands.)

Industry

Firm Average

ratio

C urrent

=

sliabilitieCurrent

assetsCurrent

=

000,330$

000,655$

=

1.98

2.0

ratio

Quick

=

sliabilitieCurrent

sInventorie assetsCurrent −

=

000,330$

500,241$0005,65$−

=

1.25×

1.3×

DSO

=

536Sales/

receivable Accounts

=

=

=

6.66

6.7

=

=

=

=

=

=

=

11.404$4,

000,336$

=

76.3

days

35

days

Chapter 4: Analysis of Financial Statements

Answers and Solutions

63

b. For the firm, ROE = NI/S S/TA TA/E = 2.3% 1.7

$361,000

$947,500

= 10.2%.

c. The firm’s days sales outstanding ratio is more than twice the industry average, indicating

that the firm should tighten credit or enforce a more stringent collection policy. The total

assets turnover ratio is well below the industry average, so sales should be increased, assets

d. If 2019 represents a period of supernormal growth for the firm, ratios based on this year will

4-24 a. Industry

Firm Average

Current ratio

=

sliabilitieCurrent

assetsC urrent

=

85$

$303

=

3.56

3

capital total

toDebt

=

capital invested Total

debt Total

=

394$

79$

=

20.05%

20.00%

=

=

=

11

7

=

=

=

5

10

=

=

=

30.3 days

64

Answers and Solutions

Chapter 4: Analysis of Financial Statements

turnov er

A .T.

=

assets Total

Sales

=

$450

$795

=

1.77

3

assets Total

b. ROE = Profit margin Total assets turnover Equity multiplier

=

Sales

incomeNet

assets Total

Sales

equity Common

assets Total

c. Analysis of the DuPont equation and the set of ratios shows that the turnover ratio of sales to

assets is quite low; however, its profit margin compares favorably with the industry average.

d. The comparison of inventory turnover ratios shows that other firms in the industry seem to

be getting along with about half as much inventory per unit of sales as the firm. In addition,

the firm’s days’ sales outstanding is higher than the industry average, which could indicate

that the firm’s collections need to be reviewed. If the firm isn’t careful it could end up with

e. If the firm had a sharp seasonal sales pattern, or if it grew rapidly during the year, many

ratios might be distorted. Ratios involving cash, receivables, inventories, and current