1

2

3

4

5

6

7

8

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

A B C D E F G H I J K L M N O P Q R

12/9/2012

Situation

Uneven cash flow stream.

I%

Time period 0 1 2 3

FV at year end -50 100 75 50

Interest rate 0.1 These are the basic inputs, in blue.

Cash flow 100

Time period 0 1 2 3

FV at year end

100 110.00 121 133.10

Chapter 4. Mini Case

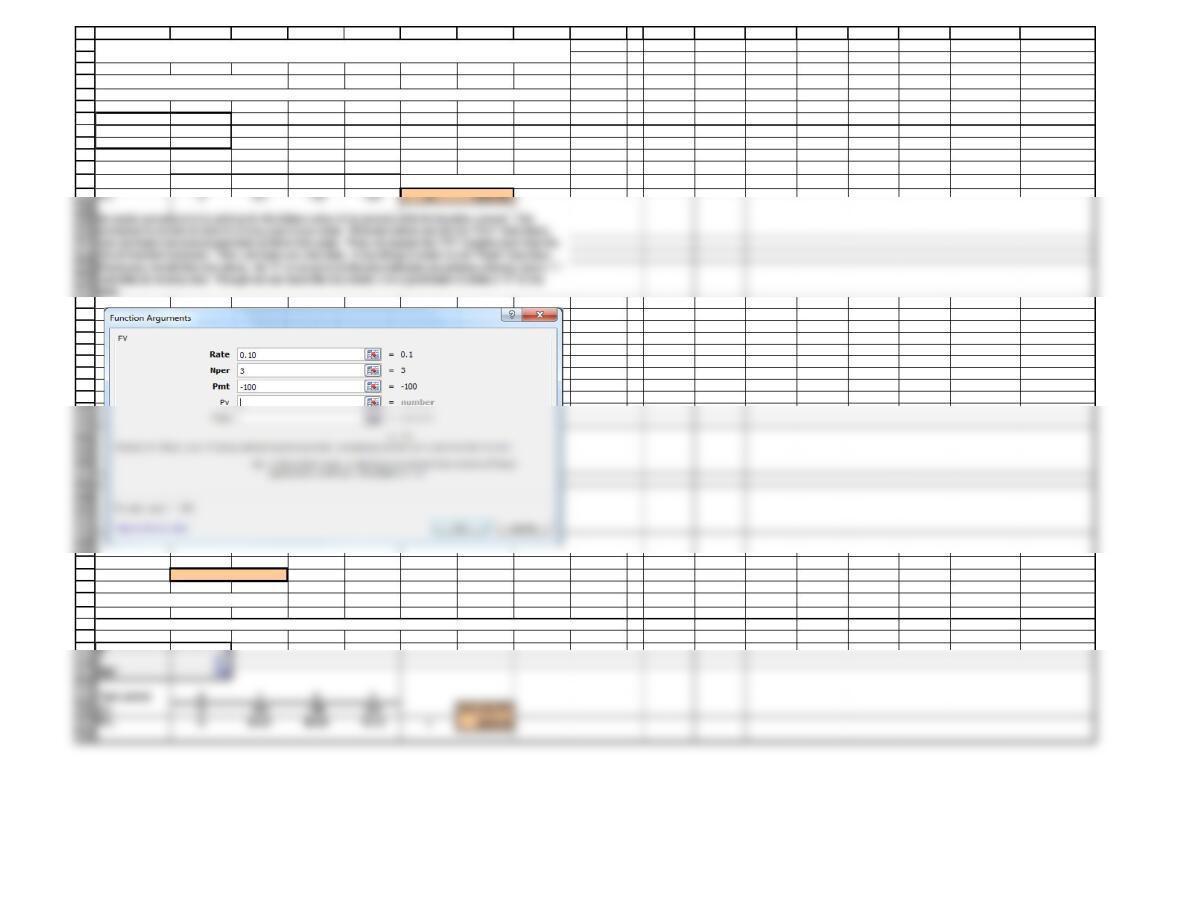

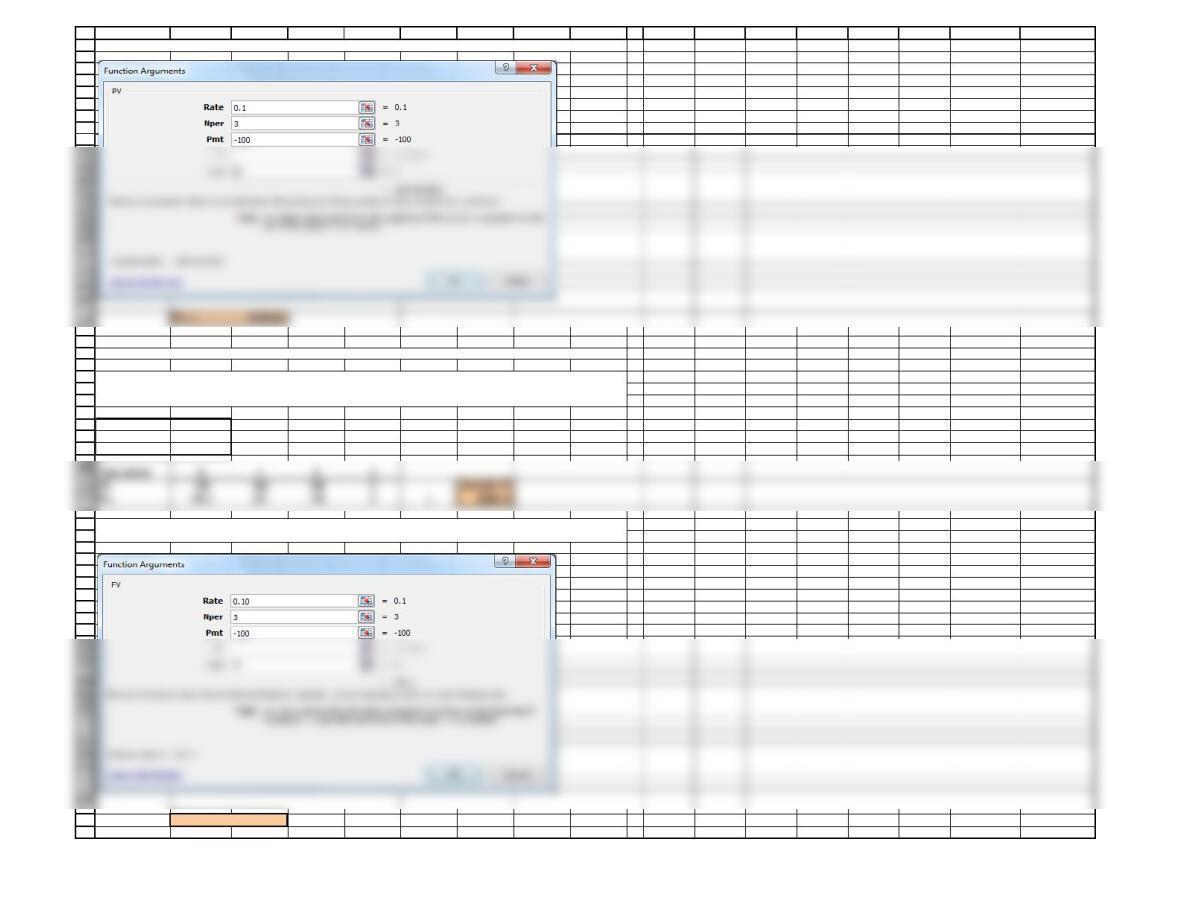

b. (1.) What’s the future value of an initial $100 after 3 years if it is invested in an account paying 10%

annual interest?

Assume that you are nearing graduation and have applied for a job with a local bank. As part of the

bank’s evaluation process, you have been asked to take an examination that covers several financial

analysis techniques. The first section of the test addresses discounted cash flow analysis. See how

you would do by answering the following questions.

1 of 13

18

24

Time period 0 1 2

Time period 0 1 2

57

58

59

60

70

71

72

73

74

75

76

77

78

79

93

94

95

96

97

98

99

100

101

102

117

118

119

120

121

122

123

124

125

A B C D E F G H I J K L M N O P Q R

FV = $133.10

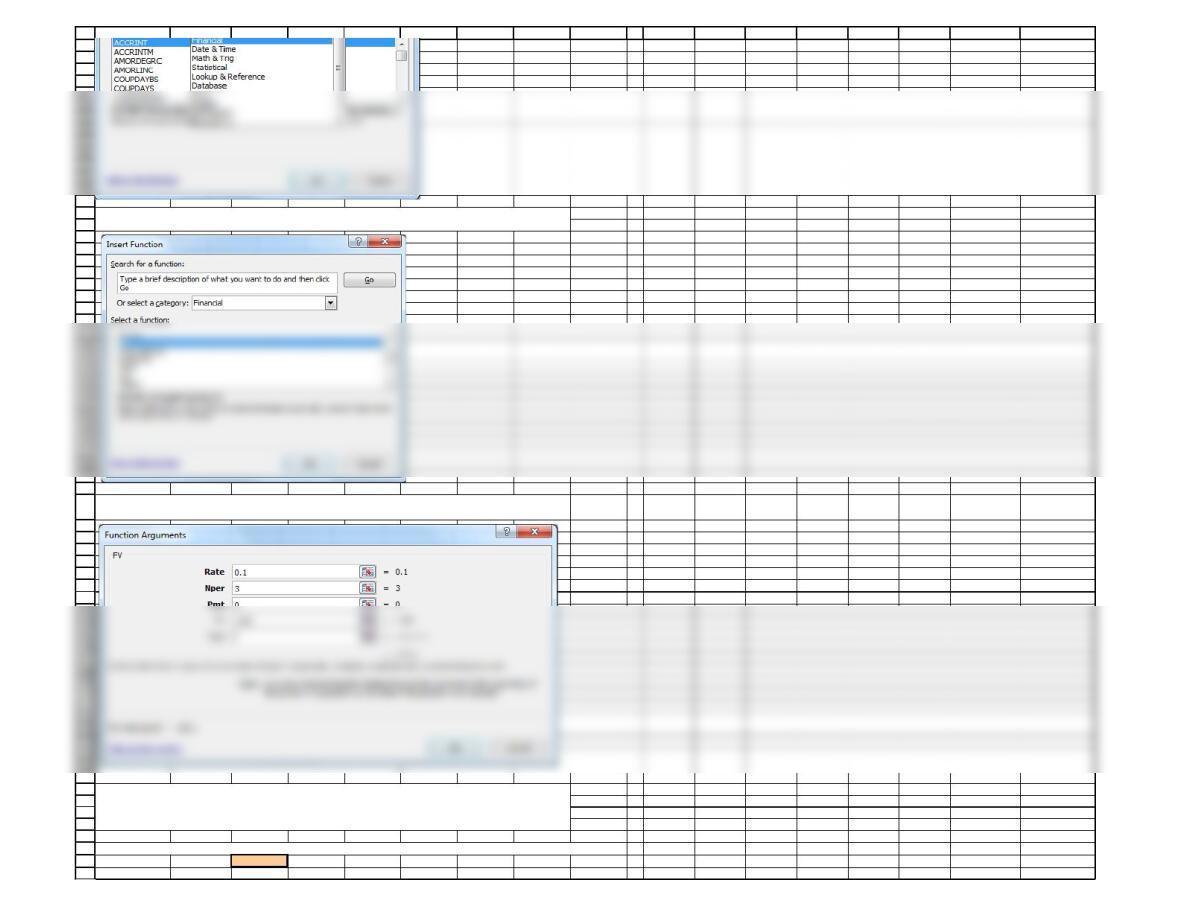

After selecting the “FV” function from the “Financial” category, we will be using the following dialog box

to input our data.

After selecting the category for Financial functions, scroll down until you can selet the FV function, as

show below. Alternatively, select the menu Formulas, then then select Financial, then pick FV.

Notice that we entered a value instead of a cell reference as the input for the problem for instructional

purposes. It’s really better to enter cell values so that your spreadsheet can automatically reflect any

changes to the input data. This is one of the features that makes the spreadsheet such a valuable tool.

Using the function wizard yields the following result:

2 of 13

126

127

128

129

130

131

132

133

134

A B C D E F G H I J K L M N O P Q R

Period (N) 0% 5% 10% 15%

01.0000 1.0000 1.0000 1.0000

21.0000 1.1025 1.2100 1.3225

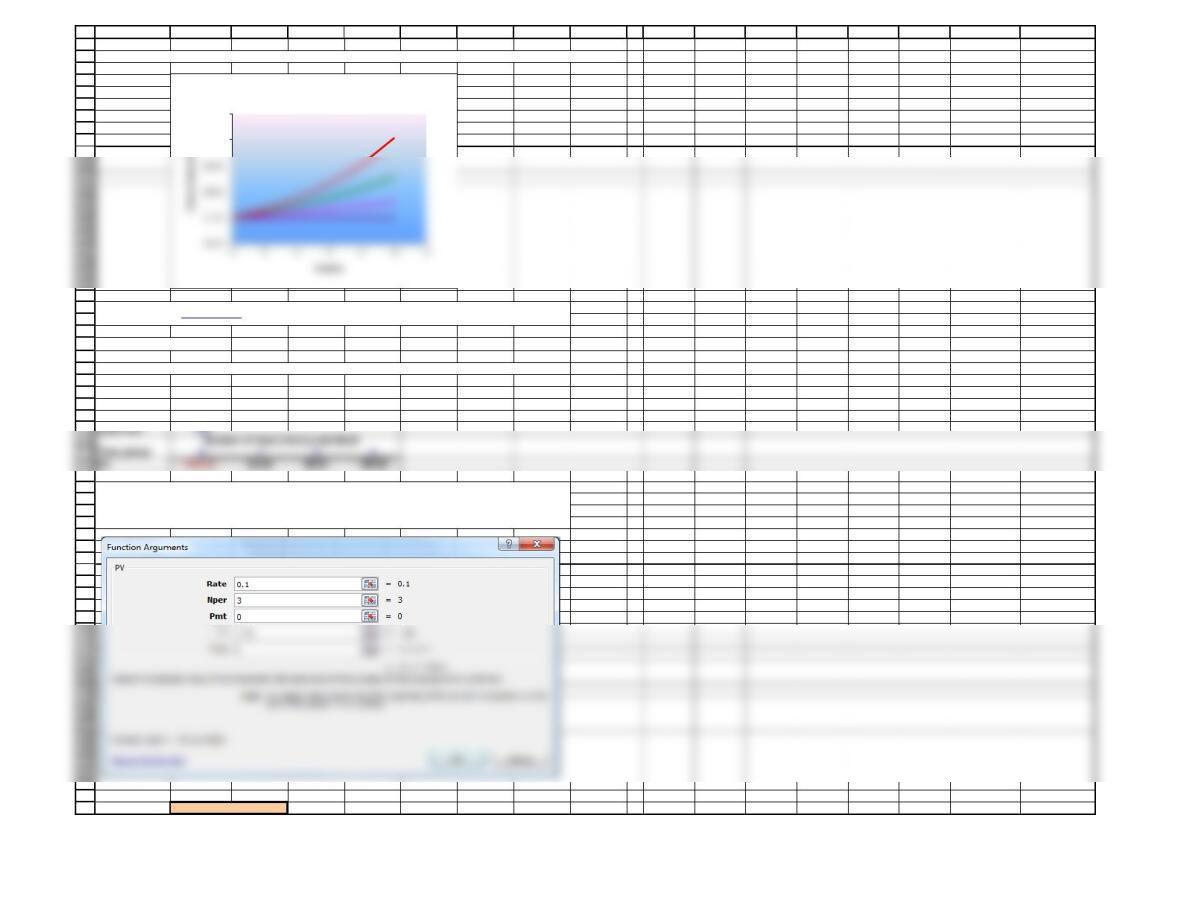

With a spreadsheet, calculating FVIF’s is a simple operation, and we can use it to graph the relationship

between future value, growth, interest rates, and time. A similar table can be found in the textbook,

along with a corresponding graph.

Future Value Interest Factors

3 of 13

174

Cash flow 100

140

141

142

143

144

145

146

147

148

149

161

162

163

164

165

166

167

168

169

170

171

176

177

178

179

180

181

182

183

184

185

186

187

188

202

203

204

A B C D E F G H I J K L M N O P Q R

PRESENT VALUE (PV)

PROBLEM

Interest rate 10%

PV = $75.13

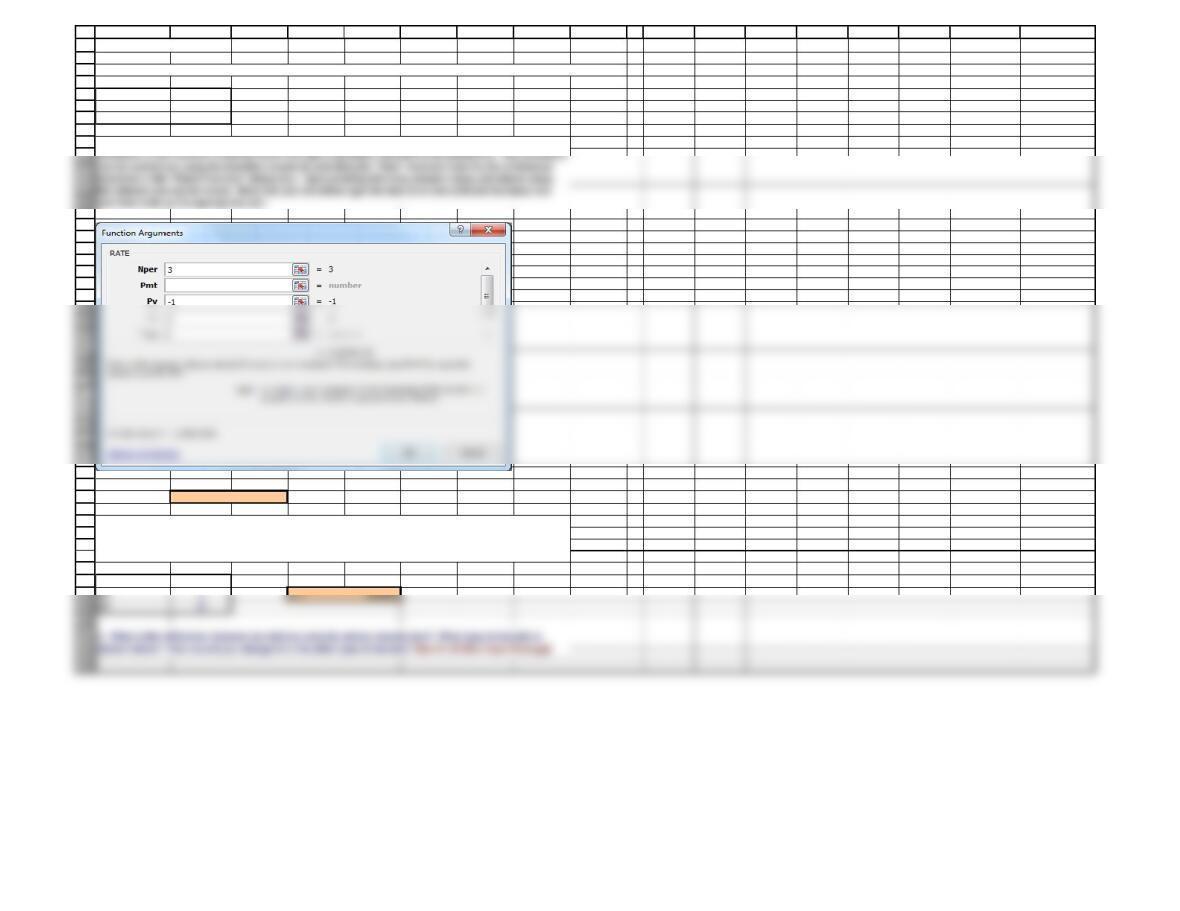

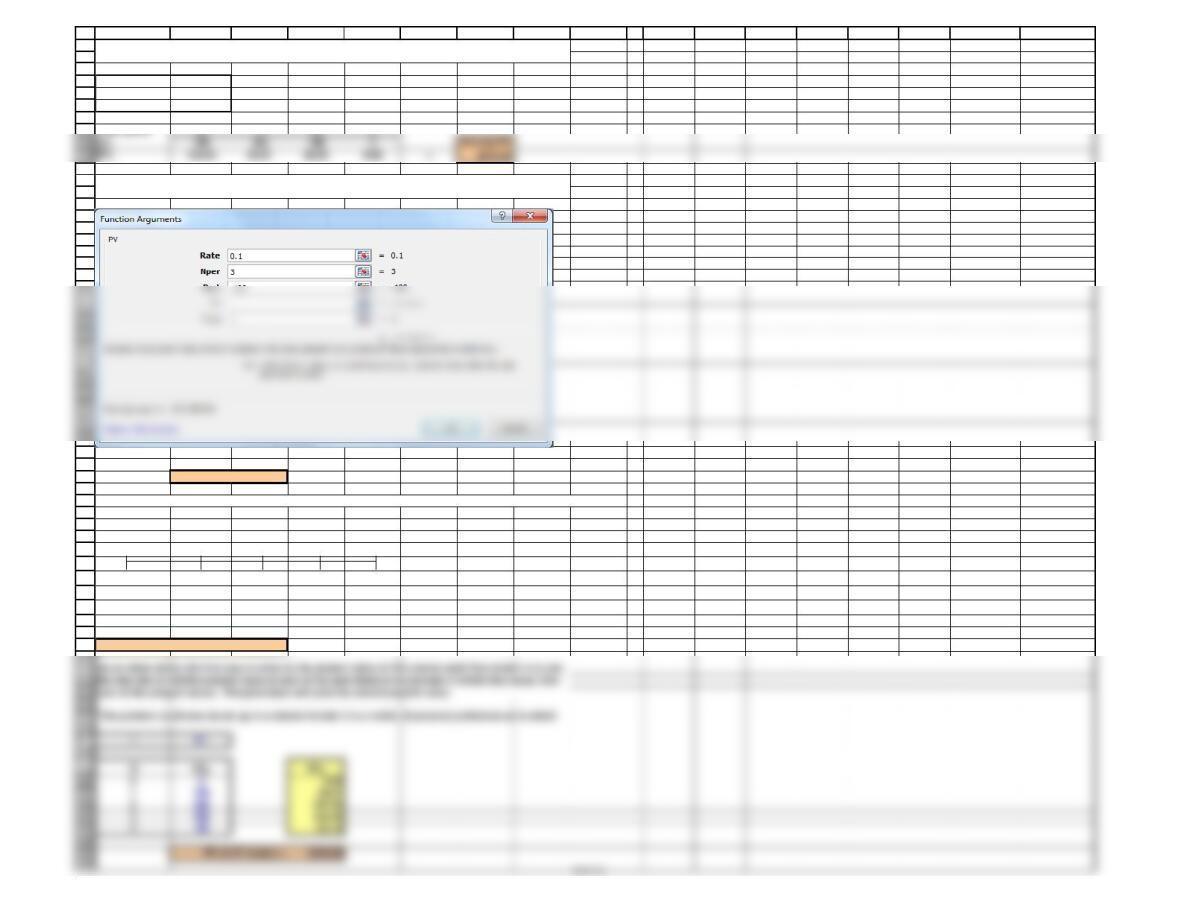

b. (2) What is the present value of $100 to be received in 3 years if the appropriate interest rate is 10%?

Simply put, the present value (PV) is the value today of some future cash flow (or series of cash flows).

This problem can also be solved using the function wizard using a procedure similar to that for the FV

function. Begin by putting the pointer on the cell in which you want to display the result. Then, after

selecting the “PV” function from the “Paste Function” box, the input data for the problem must be

entered. Then click OK to get the result, $75.13.

Relationships among Future Value, Growth, Interest Rates, and Time

$4.00

$5.00

Relationships among Future Value, Growth, Interest

Rate, and Time

4 of 13

205

206

207

208

209

210

211

212

216

217

218

219

220

221

222

223

224

225

226

A B C D E F G H I J K L M N O P Q R

Finding Time to Double

I = 0.2

3.8 Use the function NPER, as shown below.

Finding N, the number of

periods

c. We sometimes need to find how long it will take a sum of money (or anything else) to grow to some

specified amount. For example, if a company’s sales are growing at a rate of 20% per year, how long will

it take sales to double?

5 of 13

214

242

243

244

245

246

247

248

249

250

256

257

258

259

260

261

262

263

277

278

279

280

281

282

283

284

285

286

287

288

289

FV 2

A B C D E F G H I J K L M N O P Q R

SOLVING FOR I

PROBLEM

N3

PV -1

FV 2

I = 25.99%

N3

We noted above the difficulty of solving this problem mathematically. This is because it involves taking

the Nth root of a value (an operation which generally requires either a calculator or a computer).

However, if you would like to know how to solve the problem mathematically, the formula is (FVn/PV)(1/N) –

1, which is derived from the FV formula.

Once again, Excel has a special function for this calculation. We suggest using either a financial

d. If you want an investment to double in three years, what interest rate must it earn?

6 of 13

295

296

297

298

299

300

301

302

303

304

305

306

316

317

318

319

320

321

322

323

324

337

338

339

340

341

342

343

344

347

349

A B C D E F G H I J K L M N O P Q R

FUTURE VALUE OF AN ANNUITY

N3

I0.1

PMT 100

Time period 0 1 2 3

CFt0100 100 100 Annuity’s FV:

FV = $331.00

PRESENT VALUE OF AN ANNUITY

As explained below, one way to solve this problem is to find the future value of each of the annuity

f. (1.) What is the future value of a 3-year ordinary annuity of $100 if the appropriate interest rate is 10%?

f. (2.) What is the present value of the annuity?

7 of 13

353

354

355

356

357

358

359

360

361

377

378

379

380

381

382

383

384

385

386

387

389

392

393

394

395

396

397

398

399

400

401

402

417

418

419

A B C D E F G H I J K L M N O P Q R

N3

I0.1

PMT 100

FV = $364.10

f. (3.) What would the future and present values be if the annuity were an annuity due?

Additionally, using the function wizard for this problem is exactly like above, but we enter a “1” instead of a “0” into

the “Type” field.

The procedure for solving this problems follows the previous example with one notable exception. Since, the

payments occur at the beginning of each year, the first annuity payment occurs in time period 0, and the last occurs

in time period 2.

Or, you could use the function wizard for this ordinary annuity.

8 of 13

375

376

420

421

422

423

424

425

426

427

430

431

432

433

434

435

436

437

438

439

453

454

455

456

457

458

459

460

461

462

463

464

465

466

467

468

469

476

477

478

484

485

486

A B C D E F G H I J K L M N O P Q R

N3

I0.1

PMT 100

Time period 0 1 2 3

PV = $273.55

I = 10%

Time period

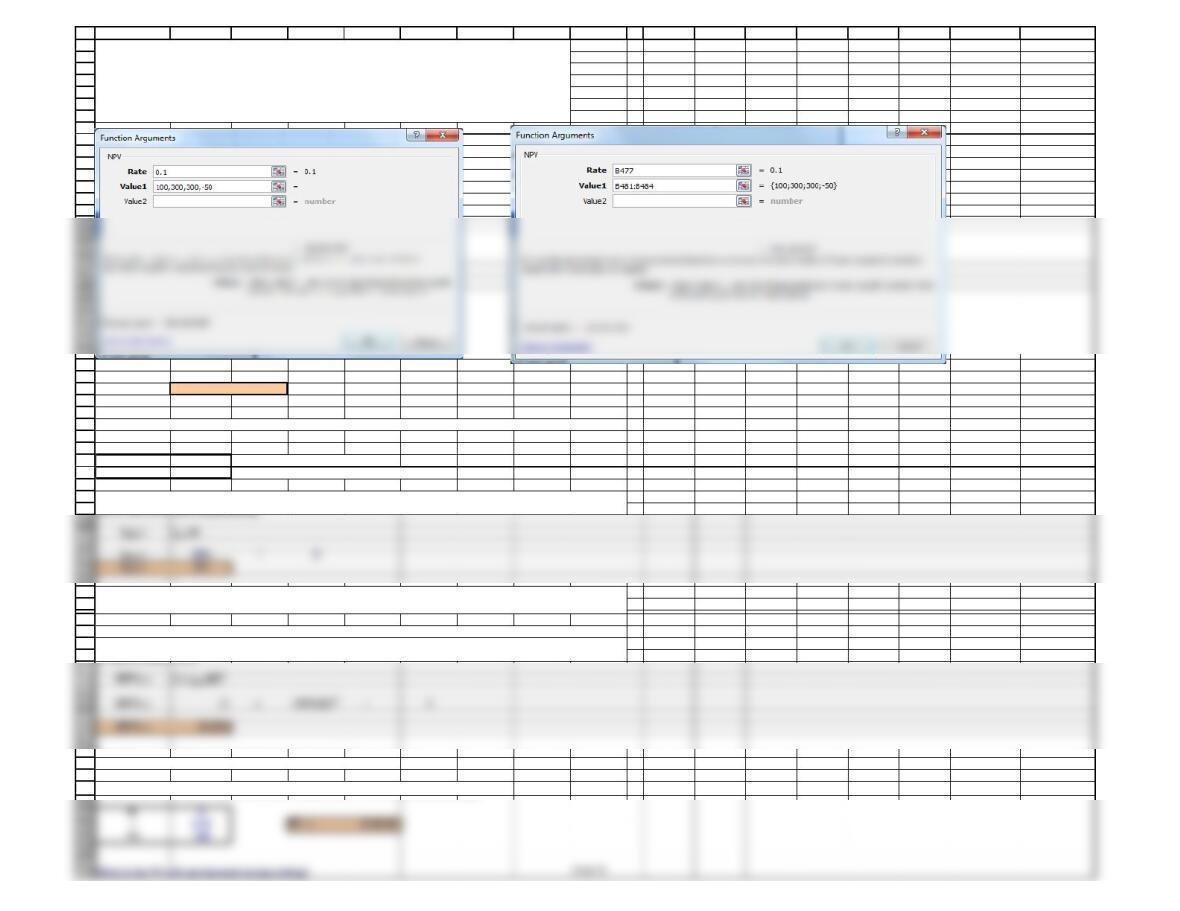

0 1 2 3 4

0100 300 300 -50

Cash Flows

PV of Cash Flows

0 90.91 247.93 225.39 -34.15

NPV = = Σ of PVs = $530.09

To find the present value of the annuity due, this problem is solved just like the previous problem,

except that the payments occur in periods 0 through 2.

g. What is the present value of the following uneven cash flow stream? The appropriate interest rate is 10%,

Using the function wizard, we follow the same procedure as above, except remember to enter a “1” to

tell Excel that in this problem the payments occur at the beginning of the periods.

6

488

489

490

491

492

493

494

495

496

497

498

499

500

501

502

514

515

516

517

518

519

520

521

522

523

524

529

525

526

527

533

534

535

536

542

545

546

537

538

539

540

548

549

550

551

552

553

554

555

558

A B C D E F G H I J K L M N O P Q R

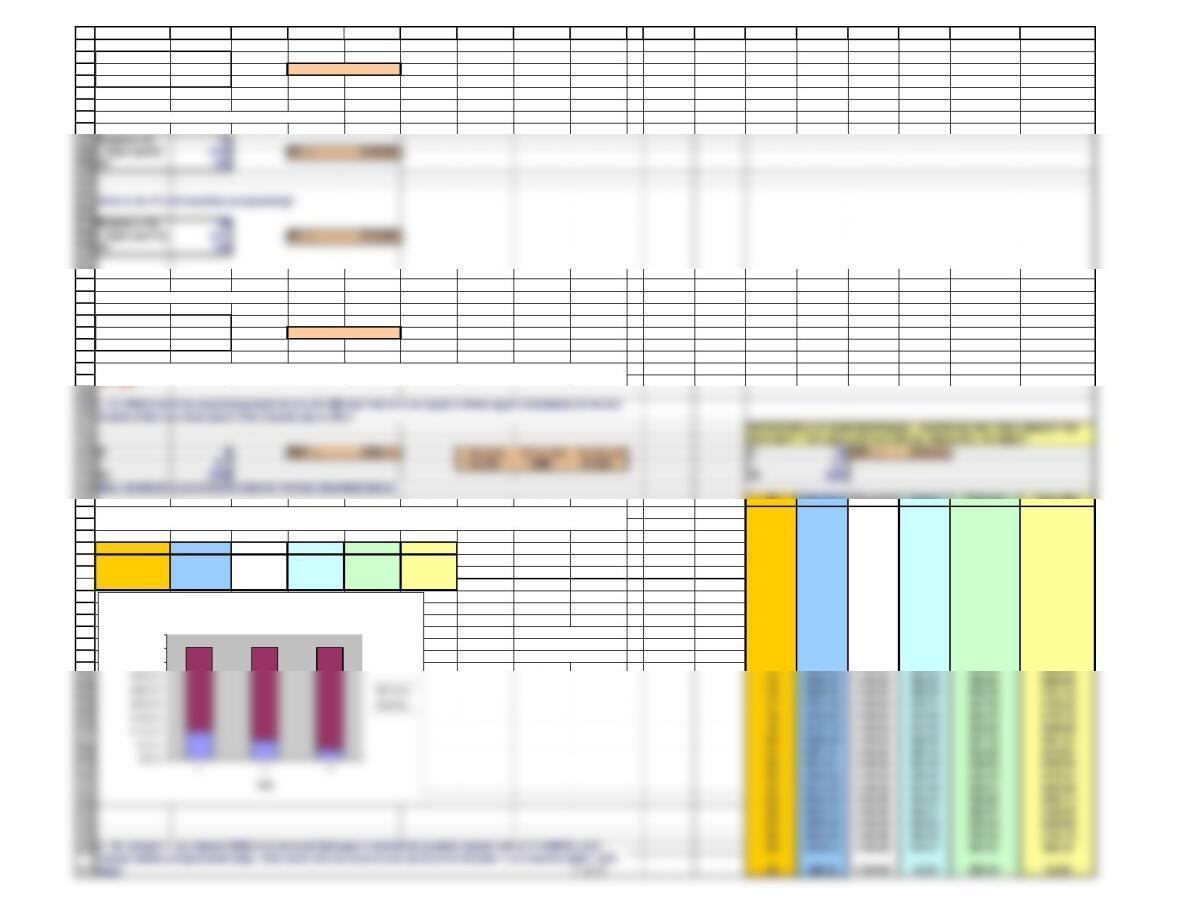

Or

PV = $530.09

Inputs

INOM (quarterly) 0.1 This is the rate stated in contracts.

m=periods/yr 2This is the number of periods per year, m.

SEMIANNUAL AND OTHER COMPOUNDING PERIODS

h. (3.) What is the future value of $100 after 5 years under 12% annual compounding?

The periodic is associated with the number of compounding periods per year. M = 4 quarterly, 12 for monthly, and

360 or 365 for annual compounding.

The effective annual rate is the annual rate that causes the PV to grow to the same FV as under multiple

compounding periods.

With, the financial calculator, we could enter each of these cash flows and the discount rate, and simply

press NPV for the present value of the cash flow stream. In Excel, we can perform a similar calculation

by using the “NPV” function. While this function is very similar, there is a key distinction. In the cash

flow register of your calculator, the first entry you make would be the cash flow to occur in time period

zero. However, the “NPV” function interprets the first data entry as being the cash flow in time period

one. Therefore, the initial cash flow must be added seperately. In this particular example, the initial

cash flow is zero.

Larger, because interest is earned on interest.

h. (2.) Will the future value be larger or smaller if we compound an initial amount more often than annually, for

example, every 6 months (semiannually), holding the stated interest rate constant? Why?

h. (1.) Identify (a) the stated, or quoted, or nominal rate (iNom) and (b) the periodic rate (iPER).

559

560

561

562

563

564

565

566

578

579

580

581

582

583

584

585

586

587

588

590

592

593

594

595

596

j. (1.) What would the required payment be on a $1,000 loan that is to be repaid in three equal installments at the end

of each of the next three years if the interest rate is 10%?

597

598

599

600

601

602

603

604

627

605

606

607

608

609

610

A B C D E F G H I J K L M N O P Q R

N (years x 2) 6

I (I per year/2) 0.06 FV = $141.85

PV 100

What is the FV with quarterly compounding?

What is the FV with daily compounding?

N (years x 365) 1095

I (I per year/12) 0.00032877 FV = $143.32

PV 100

NBeg. Amt. Payment Interest Principal End. Amt.

1 $1,000.00 $106.08 $100.00 $6.08 $993.92

2 $993.92 $106.08 $99.39 $6.69 $987.23

3 $987.23 $106.08 $98.72 $7.36 $979.88

NBeg. Amt. Payment Interest Principal End. Amt. 4 $979.88 $106.08 $97.99 $8.09 $971.79

1 $1,000.00 $402.11 $100.00 $302.11 $697.89 5 $971.79 $106.08 $97.18 $8.90 $962.89

2 $697.89 $402.11 $69.79 $332.33 $365.56 6 $962.89 $106.08 $96.29 $9.79 $953.09

3 $365.56 $402.11 $36.56 $365.56 $0.00 7 $953.09 $106.08 $95.31 $10.77 $942.33

8 $942.33 $106.08 $94.23 $11.85 $930.48

9 $930.48 $106.08 $93.05 $13.03 $917.45

10 $917.45 $106.08 $91.74 $14.33 $903.11

Note: See Columns M 11 $903.11 $106.08 $90.31 $15.77 $887.34

through R for a 30 year 12 $887.34 $106.08 $88.73 $17.34 $870.00

mortgage example. 13 $870.00 $106.08 $87.00 $19.08 $850.92

j. (2.) What is the annual interest expense for the borrower, and the annual interest income for the lender, during

Year 2?

I. Will the effective annual rate ever be equal to the nominal (quoted) rate? Only if the compounding period is equal

to 1 year.

$350.00

$400.00

$450.00

Payment

Payment Distribution

567

568

569

573

574

575

576

N (years x 4) 12

I (I per year/4) 0.03 FV = $142.58

PV 100

N (years x 12) 36

I (I per year/12) 0.01 FV = $143.08

PV 100

628

629

630

631

632

633

634

635

636

637

638

639

646

647

648

655

657

658

663

664

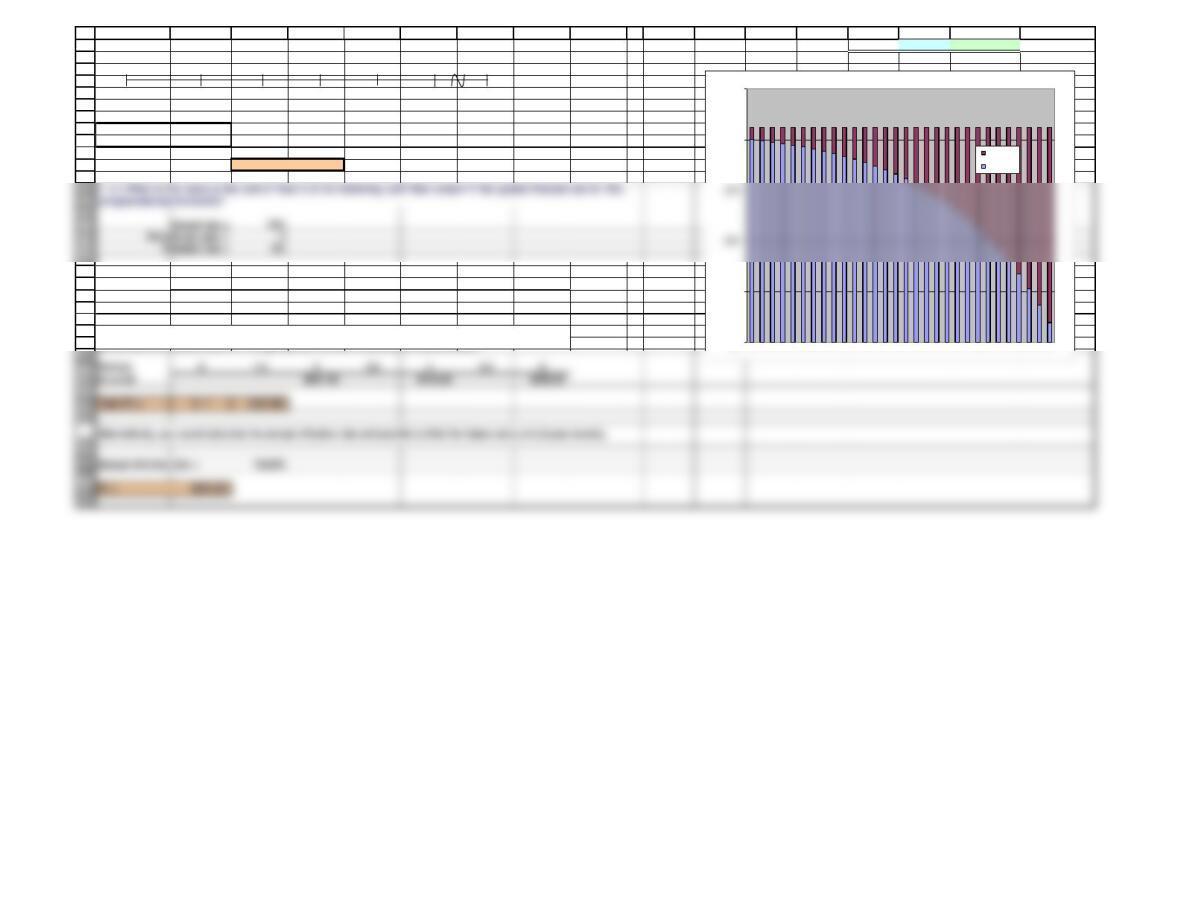

Periods 0 1.0 2 3.0 4 5.0 6

FV of CF $121.55 $110.25 $100.00

Annual effective rate = 10.25%

649

650

651

652

653

A B C D E F G H I J K L M N O P Q R

$3,182.38 $2,182.38 $1,000.00

0 1 2 3 4 5273

100

I0.00031054

N273

FV $108.85

Years 0 0.5 1 1.5 2 2.5 3

Periods 0 1.0 2 3.0 4 5.0 6

Cash Flow 0 100 0100 0100

There are two approaches. First, you could simply find the future value of each cash flow using the

period rate and compounded for the appropriate number of periods, as shown below.

$0

$25

$100

$125

Principal

Interest

12 of 13

666

667

668

669

670

671

672

681

682

683

684

685

686

695

696

697

698

699

700

701

702

703

704

705

713

715

716

717

0 1 2 3 4 5456

N456

0 1 2 3 4 5456

See which has the higher effective rate of return, EFF%

See which has the greater present value

724

725

726

727

728

729

A B C D E F G H I J K L M N O P Q R

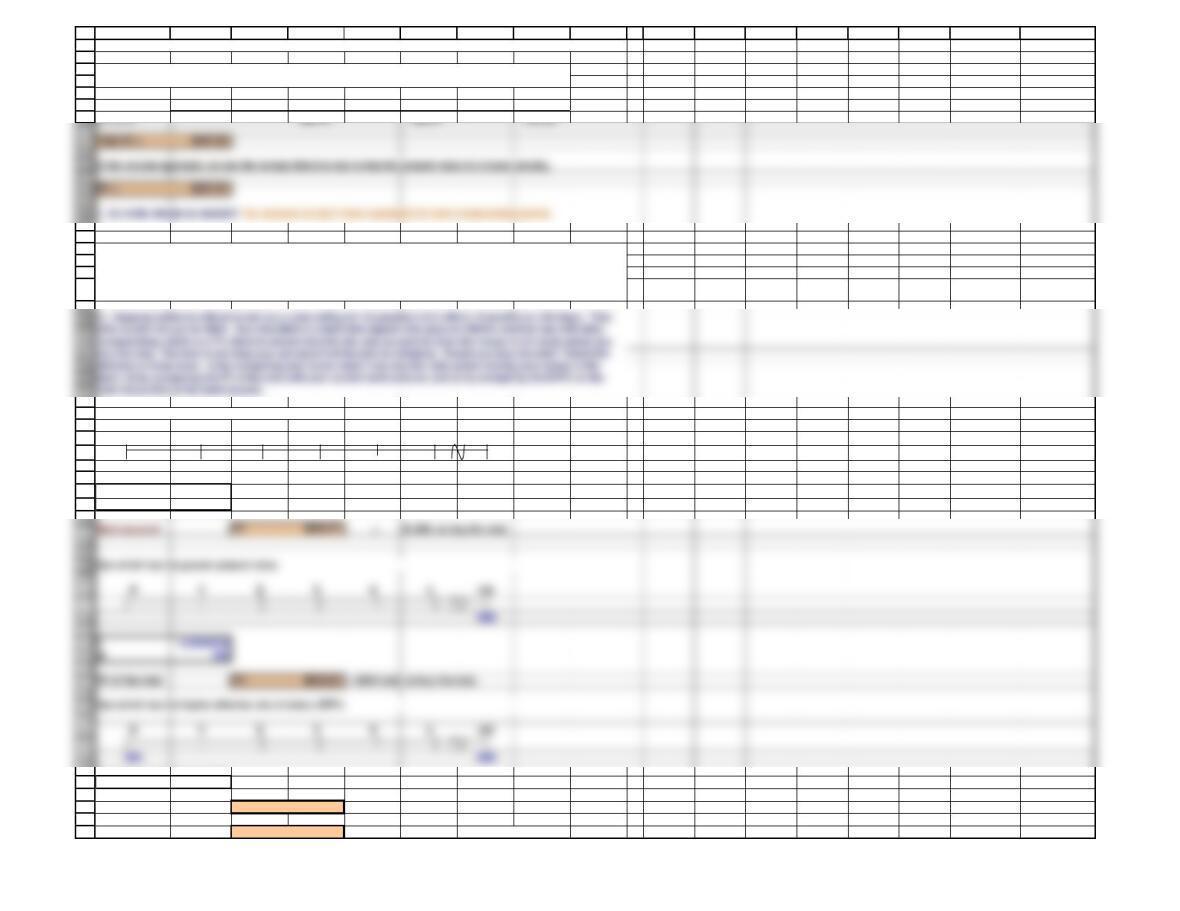

Periods 0 1 2 3.0 4 5.0 6

PV of CF $90.70 $82.27 $74.62

See which provides the greater future wealth

0 1 2 3 4 5456

850

I0.00018538

N456

N456

I 0.035646% per day

EAR 13.89% > 7% so buy the note.

l. (4.) An important rule is that you should never show a nominal rate on a time line or use it in calculations unless

what condition holds? (Hint: Think of annual compounding, when iNOM = EAR = iPER.) What would be wrong with

your answer to questions l(1) and l(2) if you used the nominal rate (10%) rather than the periodic rate (iNOM/2 = 10%/2

= 5%)? Use the nominal rate only for annual compounding.

l. (2.) What is the PV of the same stream?

Using the first approach, we find the present value of each individual cash flow using the periodic rate

and the number of periods.

13 of 13

673

674

677

678