Chapter 3: Financial Statements, Cash Flow, and Taxes

Learning Objectives

23

Chapter 3

Financial Statements, Cash Flow, and Taxes

Learning Objectives

After reading this chapter, students should be able to:

◆ List each of the key financial statements and identify the kinds of information they provide to

corporate managers and investors.

◆ Estimate a firm’s free cash flow and explain why free cash flow has such an important effect on firm

value.

◆ Discuss the major features of the federal income tax system.

24

Lecture Suggestions

Chapter 3: Financial Statements, Cash Flow, and Taxes

Lecture Suggestions

The goal of financial management is to take actions that will maximize the value of a firm’s stock. These

actions will show up, eventually, in the financial statements, so a general understanding of financial

statements is critically important.

Note that Chapter 3 provides a bridge between accounting, which students have just covered,

and financial management. Unfortunately, many non-accounting students did not learn as much as they

DAYS ON CHAPTER: 2 OF 56 DAYS (50-minute periods)

Chapter 3: Financial Statements, Cash Flow, and Taxes

Answers and Solutions

25

Answers to End-of–Chapter Questions

3-2 Bankers and investors use financial statements to make intelligent decisions about what firms to

3-4 The balance sheet shows the firm’s financial position on a specific date, for example, December

3-5 Investors need to be cautious when they review financial statements. While companies are

required to follow GAAP, managers still have quite a lot of discretion in deciding how and when

b. Although not broken down on a per-household level, updated information on aggregate

26

Answers and Solutions

Chapter 3: Financial Statements, Cash Flow, and Taxes

3-7 Free cash flow is the amount of cash that could be withdrawn without harming the firm’s ability

to operate and to produce future cash flows. It is calculated as after-tax operating income plus

3-9 MVA is the difference between a firm’s market value and the book value of its equity. The higher

a firm’s MVA, the better the job management is doing for the firm’s shareholders. EVA is the

3-11 Double taxation refers to the fact that corporate income is subject to an income tax, and then

Chapter 3: Financial Statements, Cash Flow, and Taxes

Answers and Solutions

27

Solutions to End-of–Chapter Problems

3-1 From the data given in the problem, we know the following:

Current assets $ 500,000c Accounts payable and accruals $ 100,000e

a. Total debt = Short-term debt + Long-term debt

Total debt = $900,000.

b. We are given that the firm’s total assets equal $2,500,000. Since both sides of the balance

e. Current liabilities = Accounts payable and accruals + Notes payable

28

Answers and Solutions

Chapter 3: Financial Statements, Cash Flow, and Taxes

3-3 EBITDA $7,500,000 (Given)

3-6 Book value of equity = $35,000,000.

Chapter 3: Financial Statements, Cash Flow, and Taxes

Answers and Solutions

29

3-7 EVA = EBIT(1 – T) –

capital

ofcost

%tax –After

capital

inv ested

Total

3-8 a. Federal tax liability = $28,925.00 + ($165,000 – $148,850)0.28

3-9 Statements b and d will decrease the amount of cash on a company’s balance sheet.

3-12 a. From the statement of cash flows the change in cash must equal cash flow from operating

activities plus long-term investing activities plus financing activities. First, we must identify

the change in cash as follows:

30

Answers and Solutions

Chapter 3: Financial Statements, Cash Flow, and Taxes

b. Since we determined that the firm’s cash flow from operations totaled $50,000 in Part a of

this problem, we can now calculate the firm’s net income as follows:

3-13 Statement of Cash Flows

I. Operating Activities

Chapter 3: Financial Statements, Cash Flow, and Taxes

Answers and Solutions

31

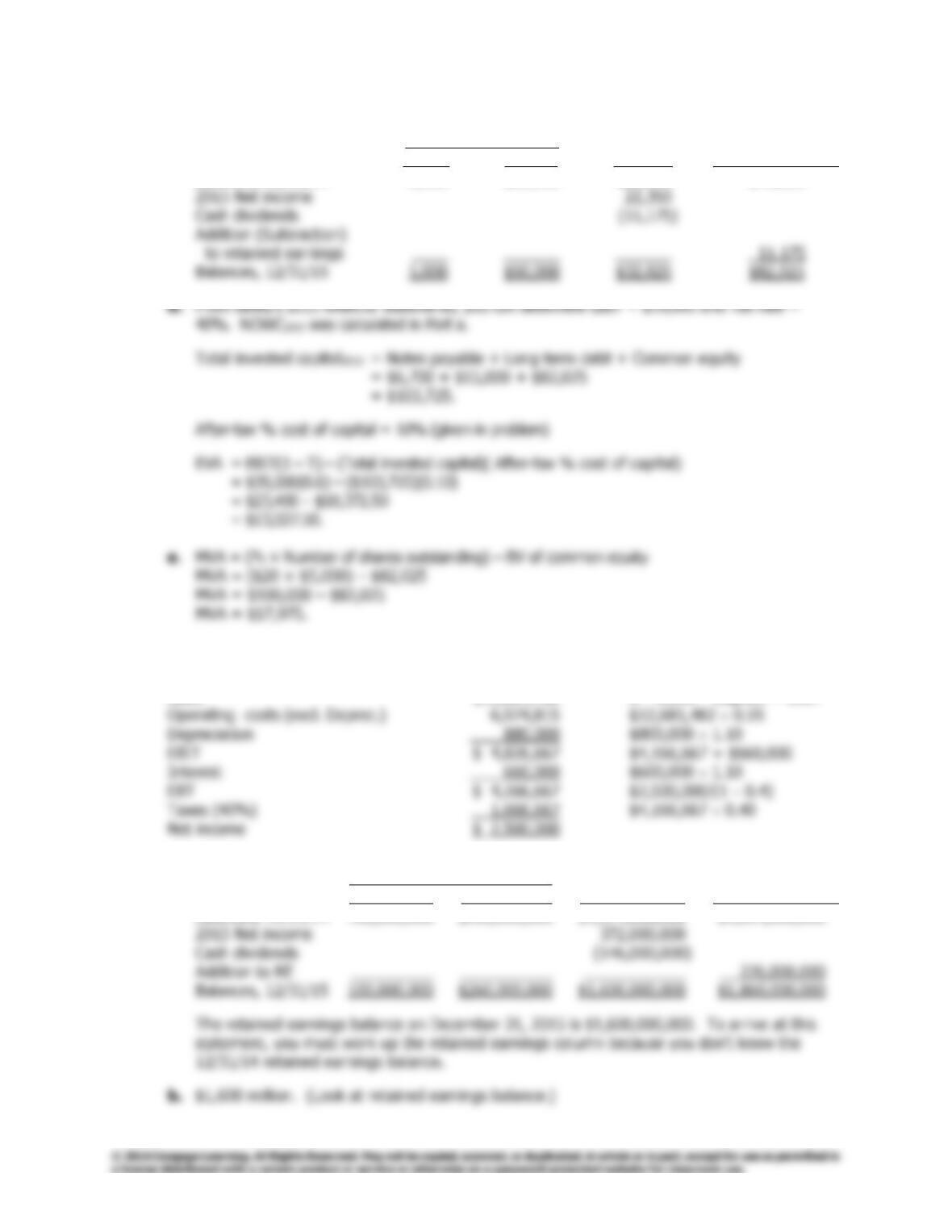

c. Statement of Stockholders’ Equity, 2015

Common Stock Retained Total Stockholders’

Shares Amount Earnings Equity

Balances, 12/31/14 5,000 $50,000 $20,850 $70,850

3-15 Working up the income statement you can calculate the new sales level would be $12,681,482.

Sales $12,681,482 S – 0.55S – Deprec. = EBIT

3-16 a. Common Stock Retained Total Stockholders’

Shares Amount Earnings Equity

Balances, 12/31/14 100,000,000 $260,000,000 $1,374,000,000 $1,634,000,000

32

Answers and Solutions

Chapter 3: Financial Statements, Cash Flow, and Taxes

3-17 a.

capital working

capital working

operatingNet

= Current assets – (Current liabilities – Notes payable)

b. FCF2015 = [EBIT(1 – T) + Deprec.] – [Cap. expend. + NOWC]

Note that depreciation must be added to Net P&E to arrive at capital expenditures.

c. The large increase in dividends for 2015 can most likely be attributed to a large increase in

3-18 a. First, you need to calculate taxable income. Note, we need to treat the tax on dividend

income and long-term capital gains separately.

Be careful to use the Individual Tax Rate Table:

Chapter 3: Financial Statements, Cash Flow, and Taxes

Answers and Solutions

33

34

Comprehensive/Spreadsheet Problem

Chapter 3: Financial Statements, Cash Flow, and Taxes

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

3-19

a.

The input information required for the problem is outlined in the “Key Input Data“ section below. Using

Laiho Industries December 31 Balance Sheets

(in thousands of dollars)

2015 2014

Assets