61

LECTURE SUPPLEMENT

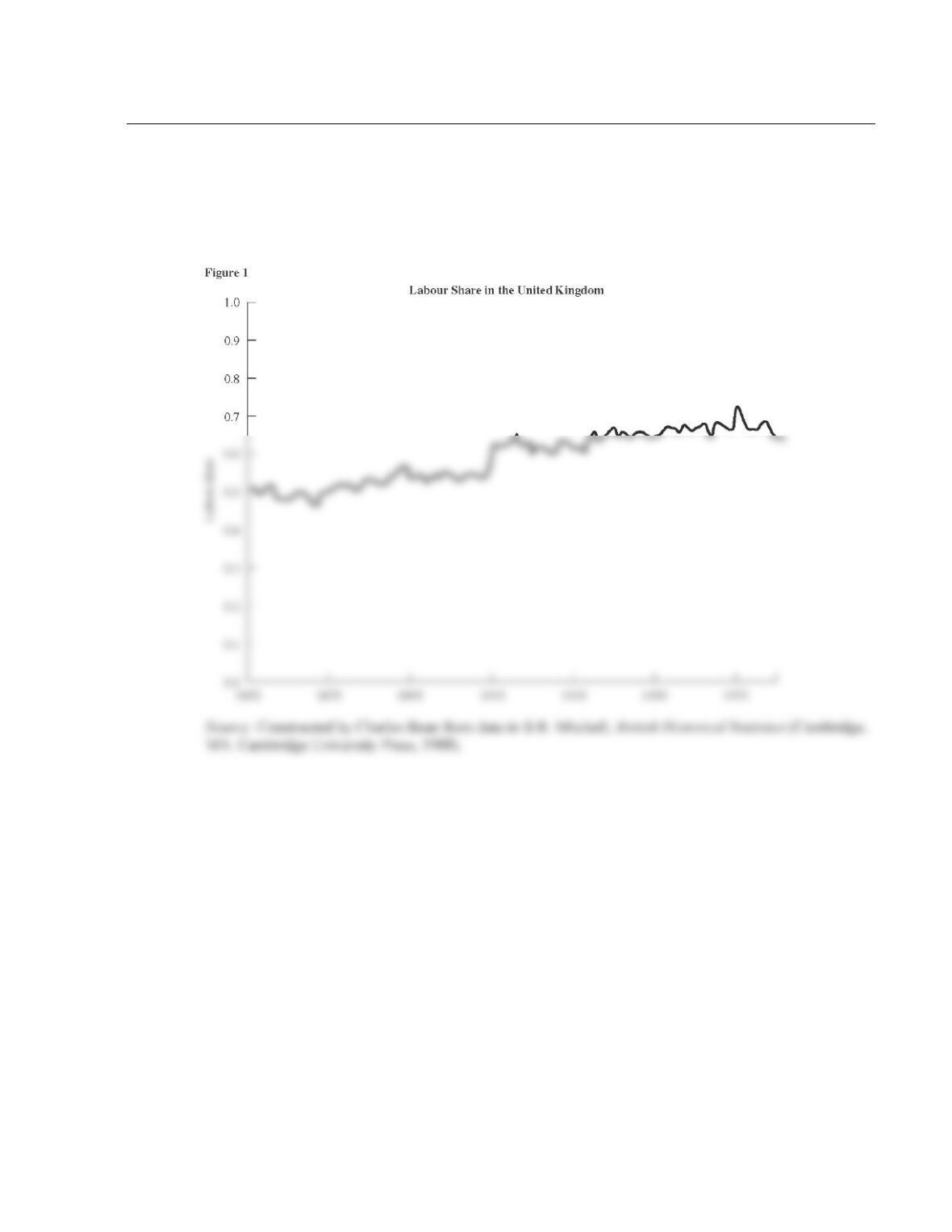

3-3 Labor’s Share of Output in the United Kingdom

Figure 3–5 in the textbook reveals that the division of U.S. output between capital and labor has been

roughly constant for the last 60 years, suggesting that the Cobb–Douglas production function is a useful

approximation. This stylized fact can be observed in other countries as well: Figure 1 graphs labor’s share

of output in the United Kingdom over the last century and a half.

62

ADDITIONAL CASE STUDY

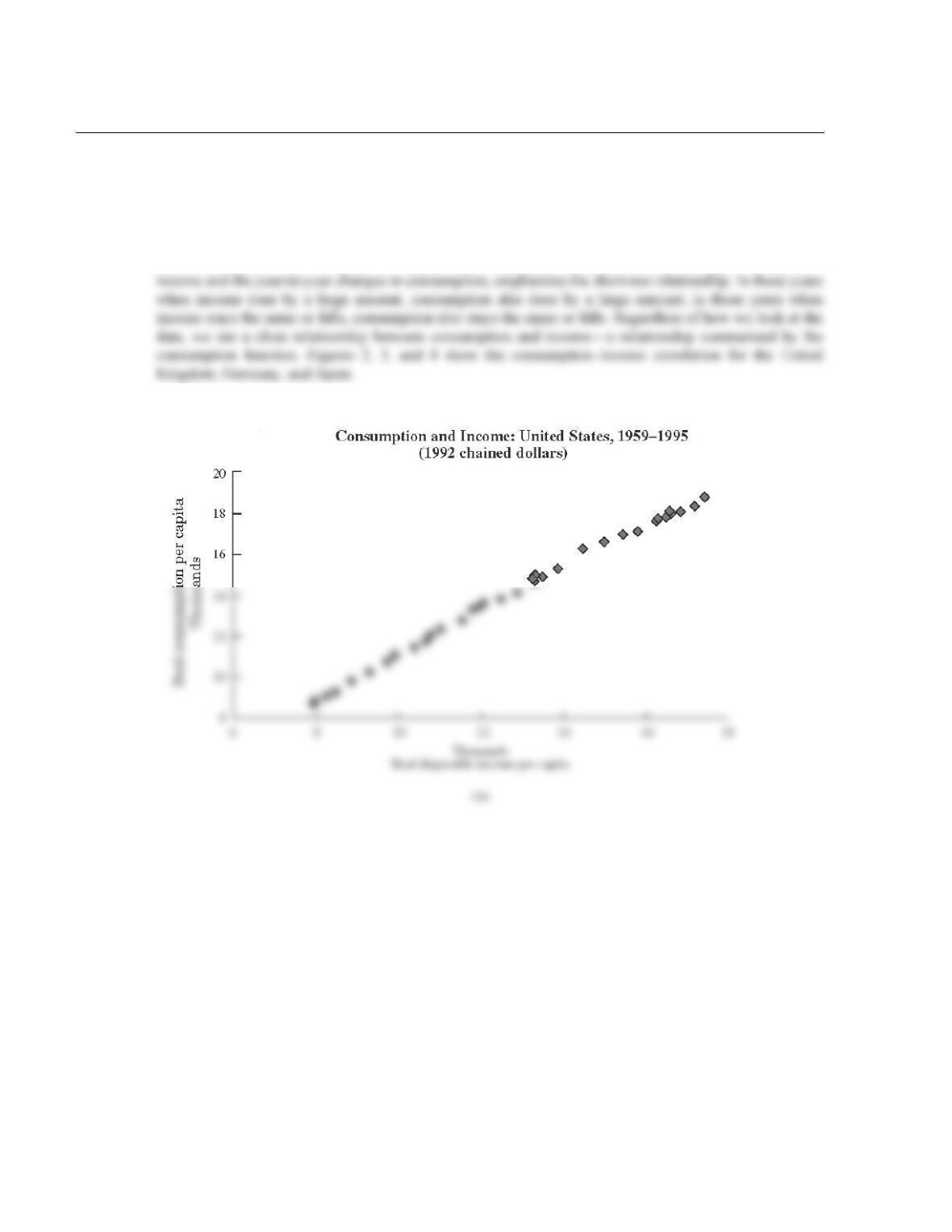

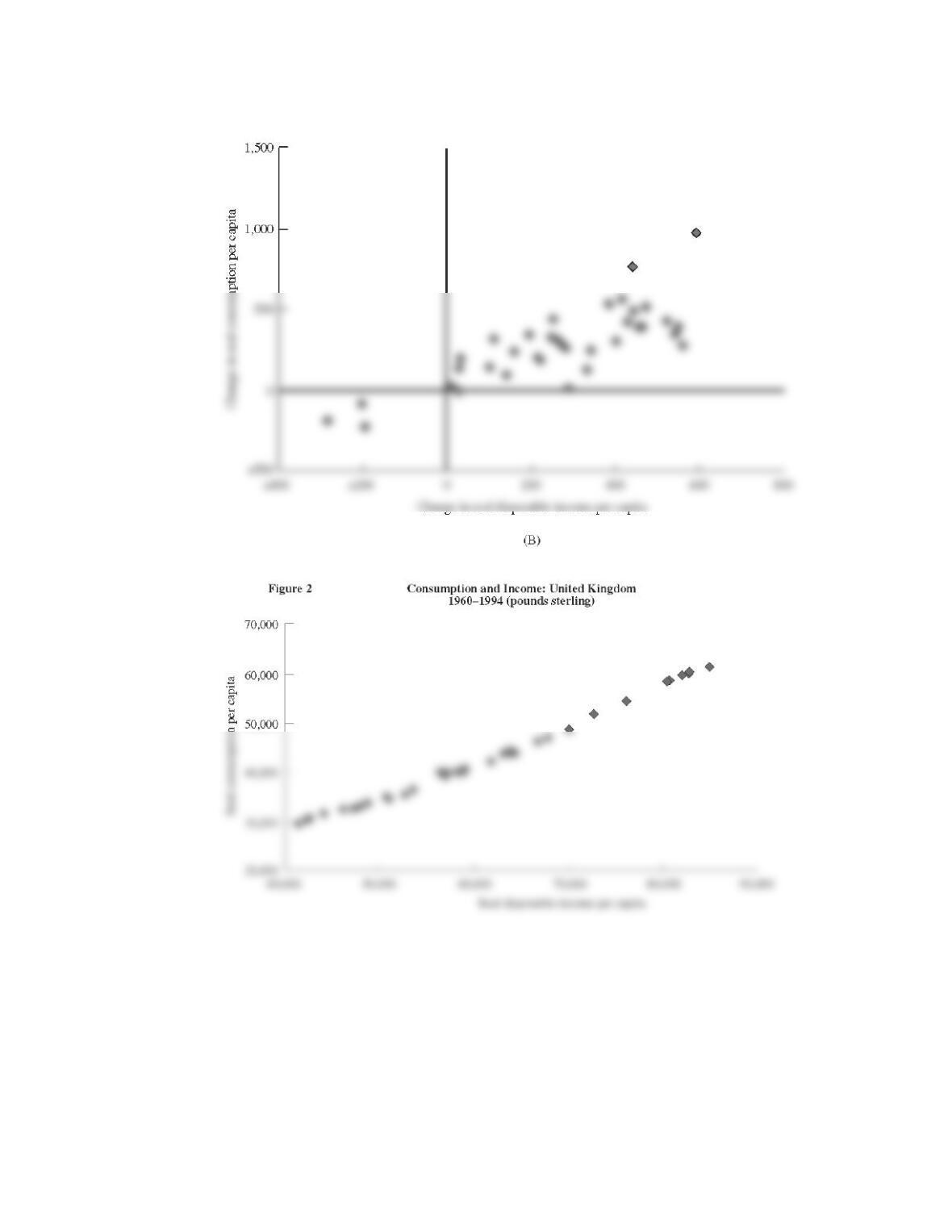

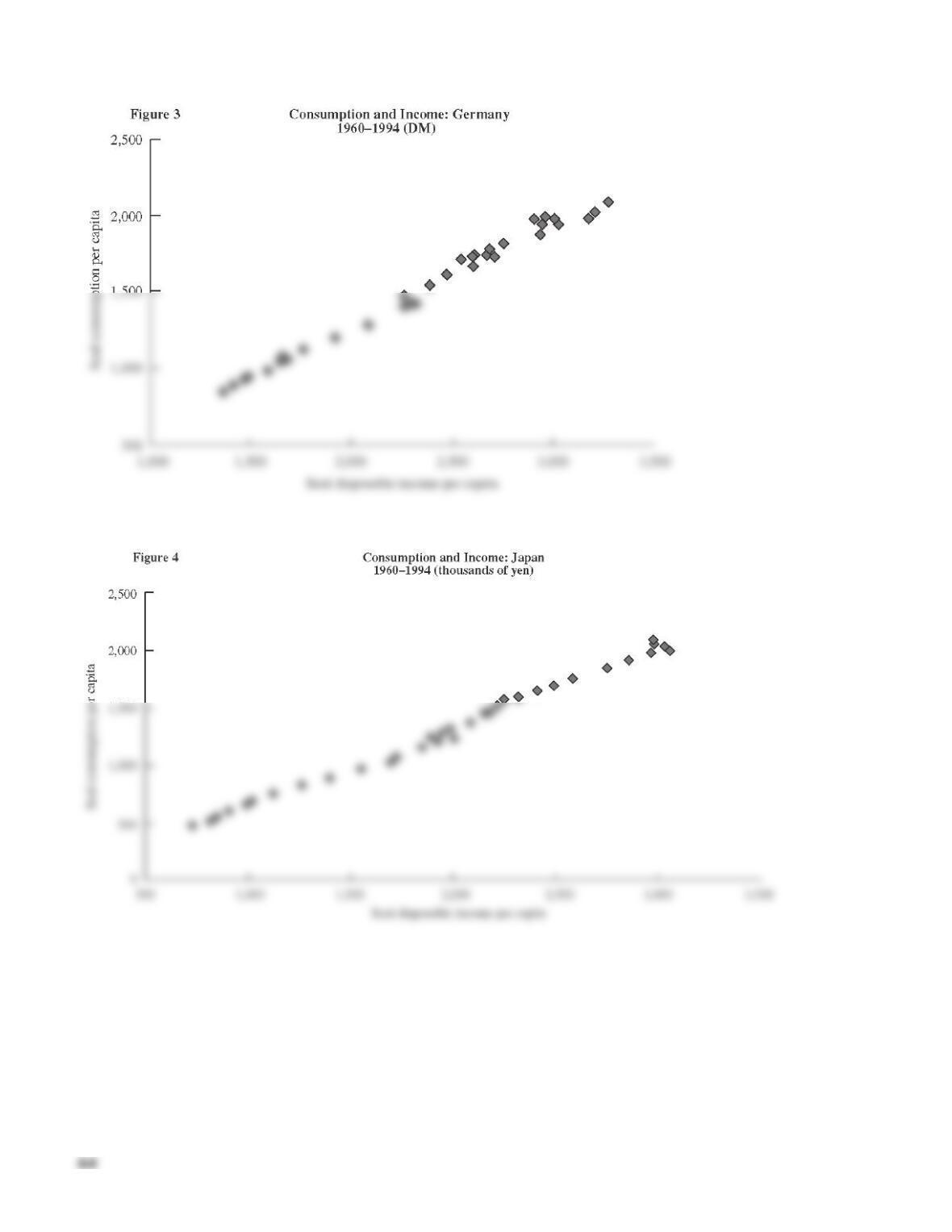

3-4 The Consumption Function

It is easy to find the consumption function in the data. Figures 1A and 1B use annual data from the

national income accounts on consumption per person and disposable income per person to illustrate the

U.S. consumption function in two different ways. Figure 1A, a scatterplot of the level of income and the

level of consumption, emphasizes the long–run relationship between these two variables. As income has

risen over time, so has consumption. Figure 1B, a scatterplot of the year–to–year changes in disposable

Figure 1a

63

Figure 1b Change in Consumption and Income: United States, 1959–1995

(1992 chained dollars)

65

LECTURE SUPPLEMENT

3-5 Economists’ Terminology

Like all sciences, economics has a well–developed terminology, or jargon. Such a language is important

because it allows economists to talk precisely about the economy and to avoid ambiguity. But this

terminology presents pitfalls for the uninitiated, since economists have an annoying habit of taking terms

that are used in everyday speech and giving them a precise meaning that may not exactly match their

everyday meanings. We consider some examples here.

Saving and Investment

In everyday speech, people use the term “investment” to refer to any purchase of an asset, such as stocks

and bonds, works of art, old or new housing, and the like. Macroeconomists usually use the term much

more precisely to refer only to certain purchases of newly produced final goods and services. If a firm

Money and Income

In everyday speech, a rich individual might be described as having a great deal of money. To the

economist, however, money is not a synonym for income or wealth. Money is the name given to a

particular asset or set of assets used for transactions. The detailed definition of money is discussed in

Profit

As discussed in Chapter 3, economists distinguish between economic profit and accounting profit. Euler’s

theorem tells us that a constant–returns–to–scale production function will imply that economic profit is zero

if factors are paid their marginal products. The idea that economists conclude that firms don’t make any

profit may seem baffling. Again, this arises because economists’ use of the term “profit” differs from the

everyday use of the term. What is normally counted as profit by a firm, the economist thinks of as a

payment to a factor of production.

66

Real and Nominal Variables

One of the most important distinctions in macroeconomics, and one that recurs throughout the textbook, is

that between real and nominal variables. The distinction is actually very simple; acquiring the habit of

Stocks Versus Flows

Economists distinguish between variables know as “stocks” and variables known as “flows.” Stocks are

measured at a point in time, whereas flows are measured over time. In the loanable funds model, saving is

67

ADDITIONAL CASE STUDY

3-6 Public and Private Saving

The classical model of Chapter 3 discusses equilibrium in terms of the equality of investment and national

saving. In interpreting this model, it is crucial to remember that national saving includes both private

saving and the saving of the government. Private saving can in turn be subdivided into personal saving—

the saving of individuals—and business saving, or saving by corporations. Public or government saving

make it consistent with the manner in which private investment is calculated. Business expenditures on

equipment and structures are considered investment. Prior to the 1996 revision these expenditures, if

undertaken by the government, were considered government consumption expenditures. Thus, a new

office building purchased by the private sector would increase investment, whereas the same building if

purchased by the government would not increase investment. Now, expenditures on equipment and

68

69

ADDITIONAL CASE STUDY

3-7 Wars and Interest Rates

Wars provide a good illustration of our theory, since government expenditures usually increase greatly in

wartime. Also, wars are occasions when we can be reasonably confident that changes in government

spending are really exogenous. Often, governments’ fiscal policies may actually be responses to the state

of the economy. Between the mid–eighteenth century and the early twentieth century, the United Kingdom

was involved in a number of wars, during each of which military spending rose. As predicted by the

model, interest rates were also high at those times.

Are there other explanations for the observed correlation (in British data) between government

spending in wartime and interest rates? Robert Barro discusses two issues in his Journal of Monetary

70

LECTURE SUPPLEMENT

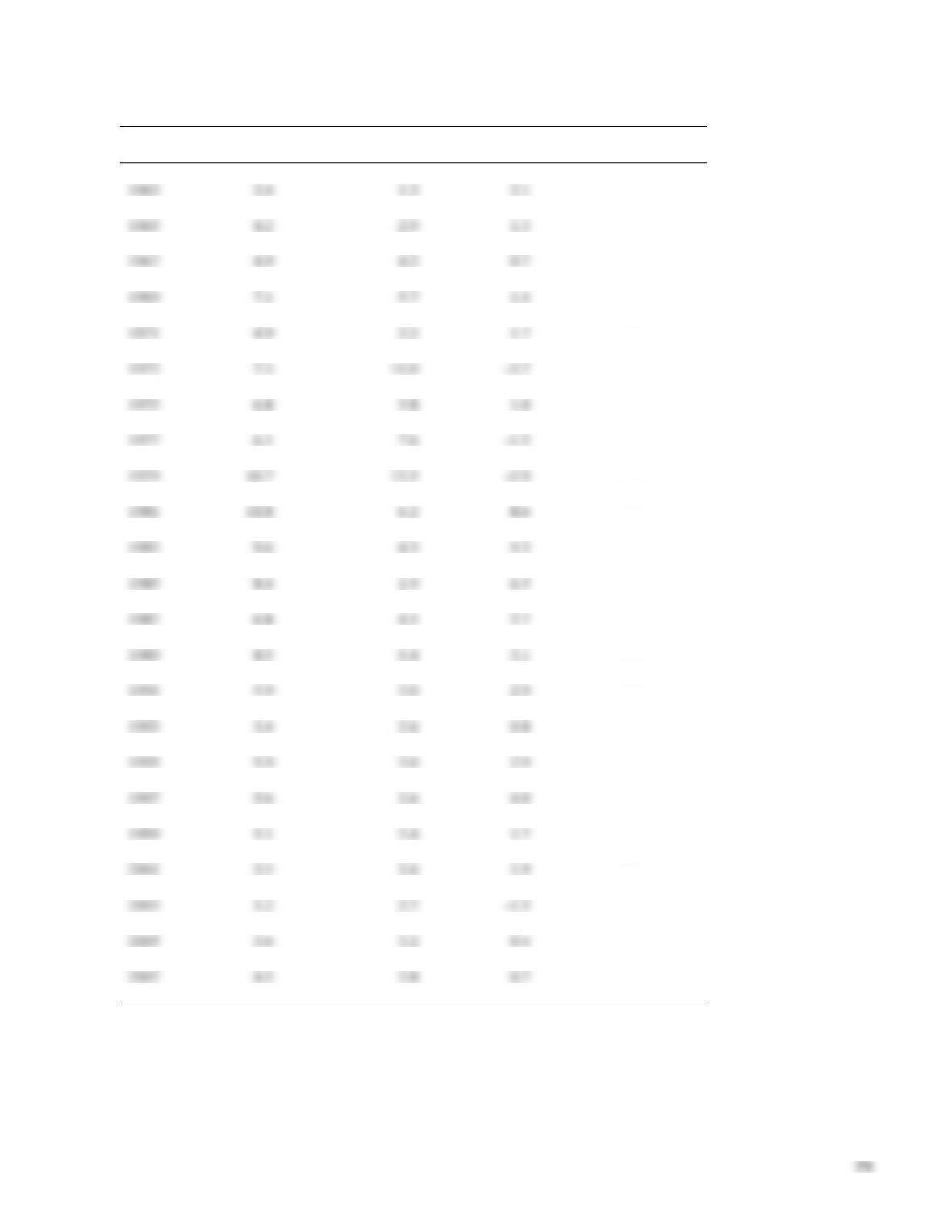

3-8 A First Look at Nominal and Real Interest Rates

The text describes how investment depends on the real interest rate—the rate adjusted for inflation—and

simply states that it represents the true cost of borrowing, putting aside for now the question of exactly

how real interest rates are measured. As we will see in Chapter 17, the appropriate real interest rate for

investment decisions is the ex ante or expected real interest rate, which is equal to the nominal rate minus

Some observers point to this pattern of higher ex post real interest rates in the 1980s as evidence that

the shift toward large budget deficits fireduction in government saving) during the Reagan administration

had the effect of raising the real interest rate. Such a rise is what the simple classical model described in

this chapter predicts following a decline in government saving. Others, however, argue that the ex ante

real interest rate did not follow the pattern of the ex post real interest rate because people expected the high

recovery that followed. Although inflation fell somewhat during these years, it remained above zero.

With the nominal interest rate close to zero and inflation positive, the real interest dropped below zero

from 2009 through 2013.

Table 1 Nominal and Real Interest Rates, 1962–2013 (percent)

Year

One–Year

Treasury Rate

Annual Rate

of Inflation

Real Interest

Rate

Decadal

Average

1962

3.1

1.3

1.8

1963

3.4

1.3

2.1

1964

3.9

1.6

2.3

1965

4.2

2.9

1.3

1966

5.2

3.1

2.1

1967

4.9

4.2

0.7

1968

5.7

5.5

0.2

1969

7.1

5.7

1.4

1970

6.9

4.4

2.5

1.6

1971

4.9

3.2

1.7

1972

5.0

6.2

–1.3

1973

7.3

11.0

–3.7

1974

8.2

9.1

–0.9

1975

6.8

5.8

1.0

1976

5.9

6.5

–0.6

1977

6.1

7.6

–1.5

1978

8.3

11.3

–3.0

1979

10.7

13.5

–2.9

1980

12.0

10.3

1.7

–0.9

1981

14.8

6.2

8.6

1982

12.3

3.2

9.1

1983

9.6

4.3

5.3

1984

10.9

3.6

7.3

1985

8.4

1.9

6.5

1986

6.5

3.6

2.9

1987

6.8

4.1

2.7

1988

7.7

4.8

2.9

1989

8.5

5.4

3.1

1990

7.9

4.2

3.7

5.2

1991

5.9

3.0

2.9

1992

3.9

3.0

0.9

1993

3.4

2.6

0.8

1994

5.3

2.8

2.5

1995

5.9

3.0

2.9

1996

5.5

2.3

3.2

1997

5.6

1.6

4.0

1998

5.1

2.2

2.9

1999

5.1

3.4

1.7

2000

6.1

2.8

3.3

2.5

2001

3.5

1.6

1.9

2002

2.0

2.3

–0.3

2003

1.2

2.7

–1.5

2004

1.9

3.4

–1.5

2005

3.6

3.2

0.4

2006

4.9

2.8

2.1

2007

4.5

3.8

0.7

2008

1.8

–0.4

2.2

(Continued on next page)

Table 1 Nominal and Real Interest Rates, 1962–2013 (percent) (Continued)

Year

One–Year

Treasury Rate

Annual Rate

of Inflation

Real Interest

Rate

Decadal

Average

2009

0.5

1.6

–1.1

2010

0.3

3.2

–2.9

2011

0.2

2.1

–1.9

2012

0.2

1.5

–1.3

2013

0.1

1.6

–1.5

–1.6

Note: The interest rate is the one–year constant maturity Treasury yield. Inflation is annual percent change in the consumer price