Basic Econometrics, Gujarati and Porter

17

CHAPTER 3:

TWO-VARIABLE REGRESSION MODEL:

THE PROBLEM OF ESTIMATION

3.1 (1) Y

i

=

1 2

i i

X u

β β

+ +

. Therefore,

E(Y

i

i

X

) = E[(

1

β

+

2

i

X

β

+ u

i

)

i

X

]

i

i

(2) Given cov(u

i

u

j

) = 0 for

∀

for all i,j (i

≠

j), then

cov(Y

i

Y

j

) = E{[Y

i

– E(Y

i

)][Y

j

– E(Y

j

)]}

3.2 Y

i

X

i

y

i

x

i

x

i

y

i

x

i2

4 1 -3 -3 9 9

5 4 -2 0 0 0

3.3

The PRF is: Y

i

=

1 2

i i

X u

β β

+ +

18

3.4

Imposing the first restriction, we obtain:

i

u

∧

∑

=

∑

(Y

i

–

1

β

∧

–

2

β

∧

X

i

) = 0

Simplifying this yields the first normal equation.

i

i

i

3.5

From the Cauchy-Schwarz inequality it follows that:

2

( )

E XY

3.6

Note that:

3.7

Even though

yx

β

∧

.

xy

β

∧

=1, it may still matter (for causality and

3.8

The means of the two-variables are:

1

2

n

Y X

+

= = and the

Basic Econometrics, Gujarati and Porter

19

and similarly,

2

2

( 1)

i

n n

y

−

=

∑

, Then

3.9

(a)

1

β

∧

=

2

Y

β

∧

−

X

i

and

1

α

∧

=

2

Y

β

∧

−

x

−

[Note: x

i

= (X

i

–

X

)]

Basic Econometrics, Gujarati and Porter

20

3.10

Since

0

i i

x y

= =

∑ ∑

, that is, the sum of the deviations from mean

value is always zero,

x

−

=

y

−

= 0 are also zero. Therefore,

3.11

Let Z

i

= aX

i

+ b and W

i

= cYi + d. In deviation form, these become:

3.12

(a) True. Let a and c equal -1 and b and d equal 0 in Question 3.11.

Basic Econometrics, Gujarati and Porter

21

3.13

Let Z = X

1

+ X

2

and W = X

2

and X

3

. In deviation form, we can write

these as z = x

1

+ x

2

and w = x

2

+ x

3

. By definition the correlation

between Z and W is:

3.14 The residuals and fitted values of Y will not change. Let

Y

i

=

1 2

i i

X u

β β

+

+

and Y

i

=

1 2

i i

Z u

α α

+ +

, where Z = 2X

Using the deviation form, we know that

Basic Econometrics, Gujarati and Porter

22

3.15 By definition,

2

ˆ

( )

i i

y y

∑

2

ˆ ˆ ˆ

( )( )

i i i

y u y

+

∑

2

ˆ

i

y

∑

i

i

coefficient will be one and the intercept zero. But a formal proof can

proceed as follows:

3.17

Write the sample regression as:

1

ˆ

ˆ

i i

Y u

β

= +

. By LS principle, we

Basic Econometrics, Gujarati and Porter

23

with the only unknown parameter and set the resulting expression to

zero, to obtain:

Empirical Exercises

3.18

Taking the difference between the two ranks, we obtain:

d

-2 1 -1 3 0 -1 -1 -2 1 2

Therefore, Spearman’s rank correlation coefficient is

3.19

(a) The slope value of 2.250 suggests that over the period 1985-2005,

Basic Econometrics, Gujarati and Porter

24

3.20

(a) The scattergrams are as follows:

Business Sector: Compensation vs Output

140.0

180.0

Basic Econometrics, Gujarati and Porter

25

(b) As both the diagrams show, there is a positive relationship

(c) As the preceding figures show, the relationship between wages is

Business

: Compensation = -102.3662 + 1.9924 Output

Nonfarm Business Sector: Compensation vs Output

140

160

180

Basic Econometrics, Gujarati and Porter

26

3.21

i

Y

∑

i

X

∑

i i

X Y

∑

2

i

X

∑

2

i

Y

∑

3.22 (

a)

(b) If the hypothesis were true, we would expect

2

1

β

≥

.

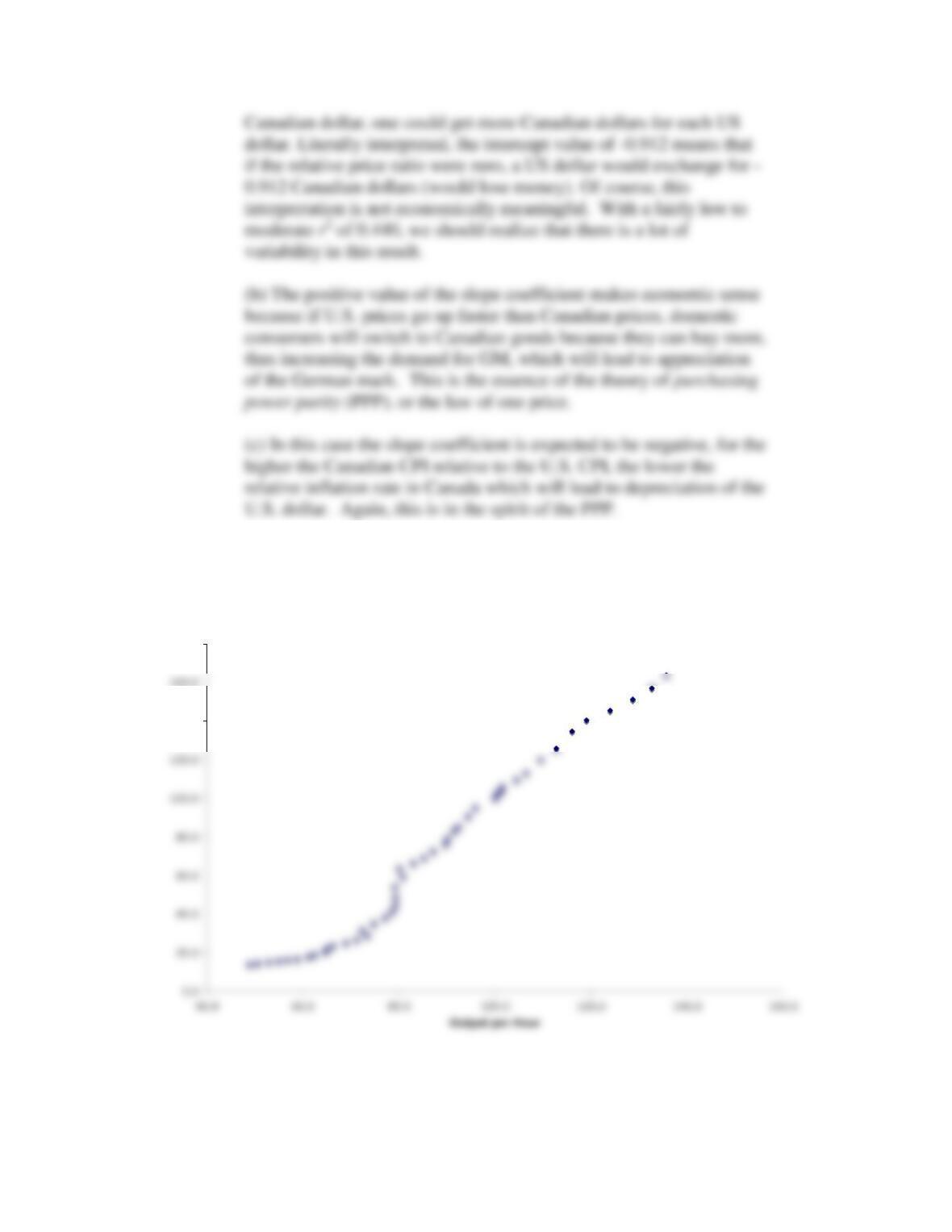

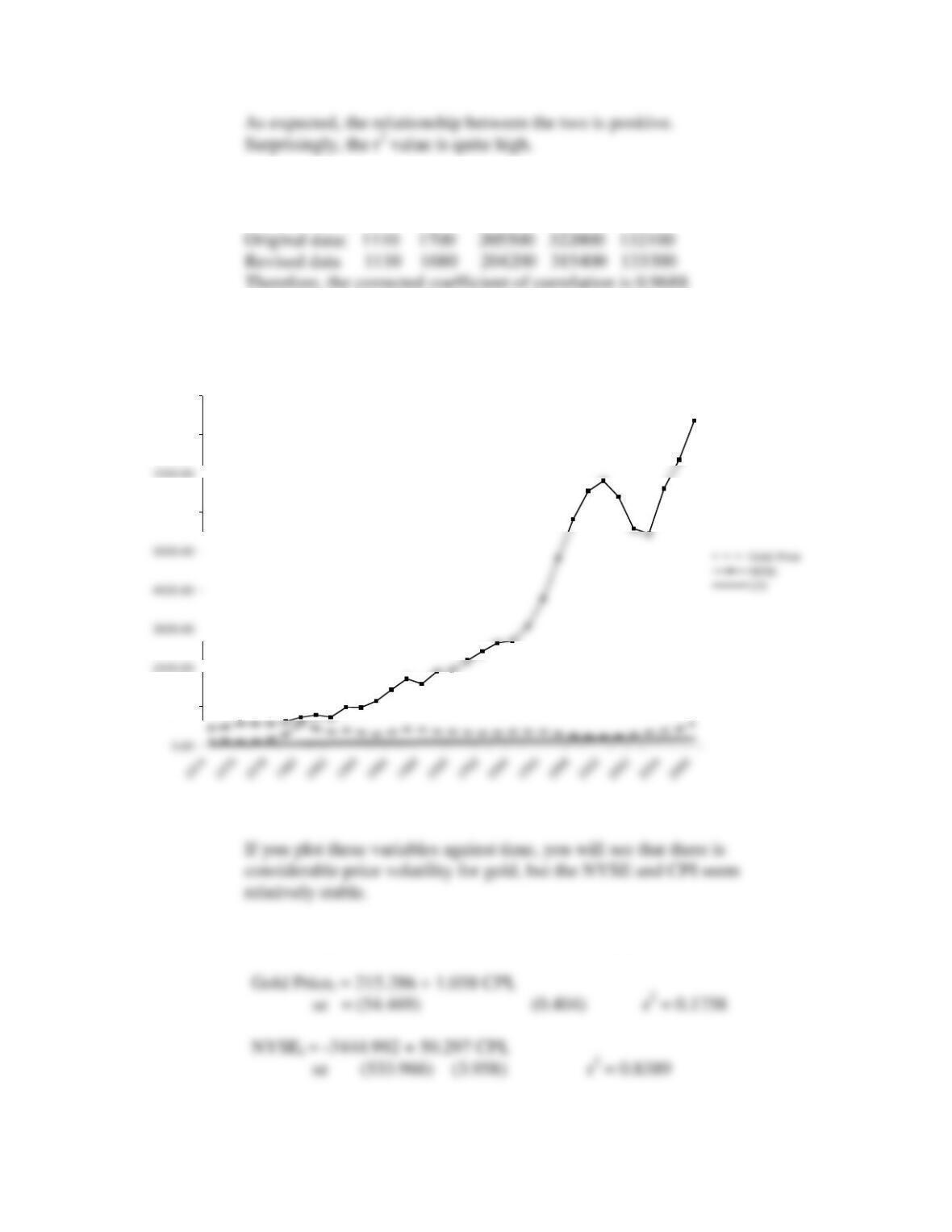

Gold Prices, CPI, and the NYSE Index Over Time

1000.00

6000.00

8000.00

9000.00

27

3.23

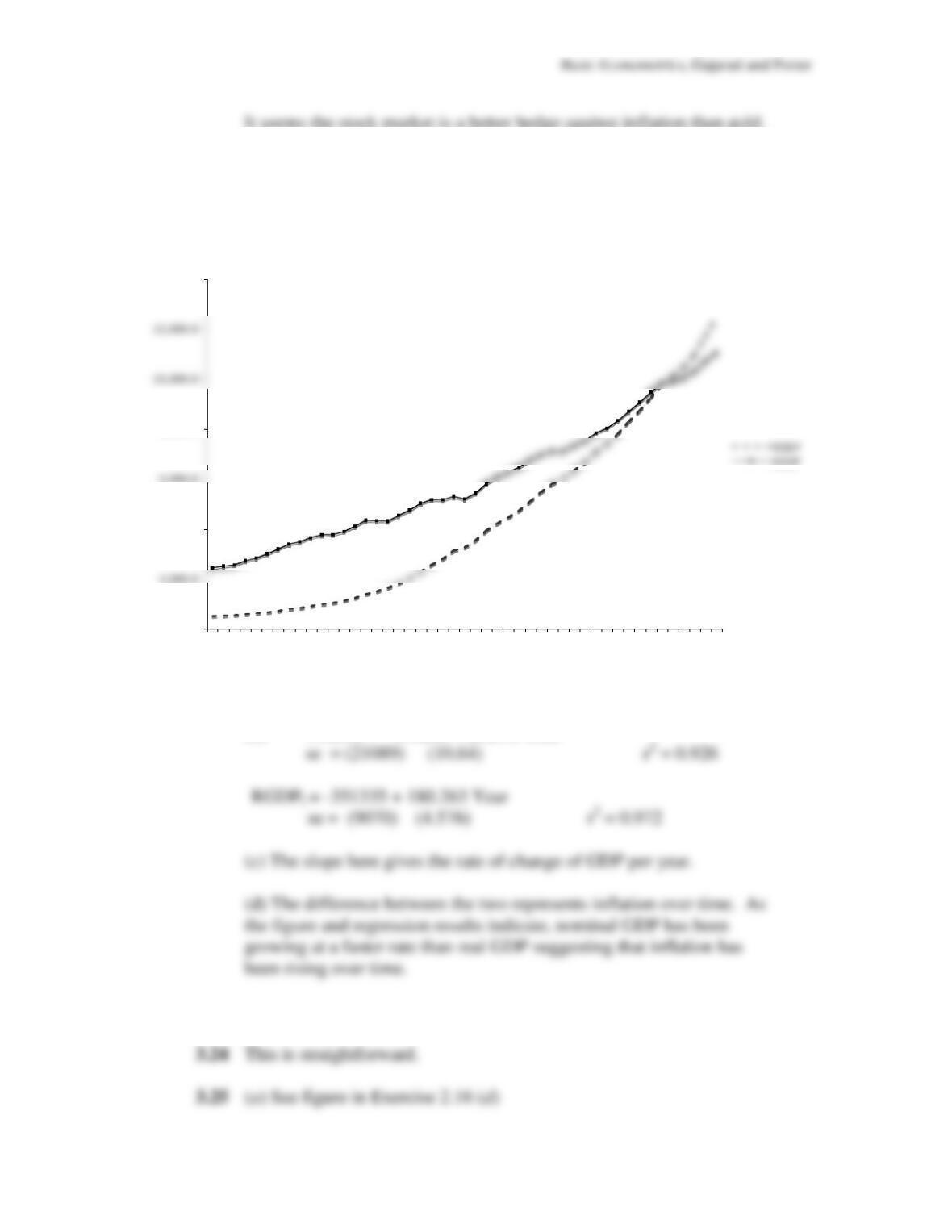

(a) The plot is as follows, where NGDP and RGDP are nominal and real

GDP.

(b) NGDP

t

= – 496268 + 252.58 Year

NGDP and RGDP Over Time

0.0

4,000.0

8,000.0

14,000.0

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Basic Econometrics, Gujarati and Porter

(

b

) The regression results are:

(

c

) As pointed out in the text, a statistical relationship, however

3.26

The regression results are:

ö

Y

= −

257.02

+

1.416

X

3.28

Cell Phone Subscribers vs PC Ownership

100

120