1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

22

23

24

25

26

27

28

29

30

31

32

33

34

46

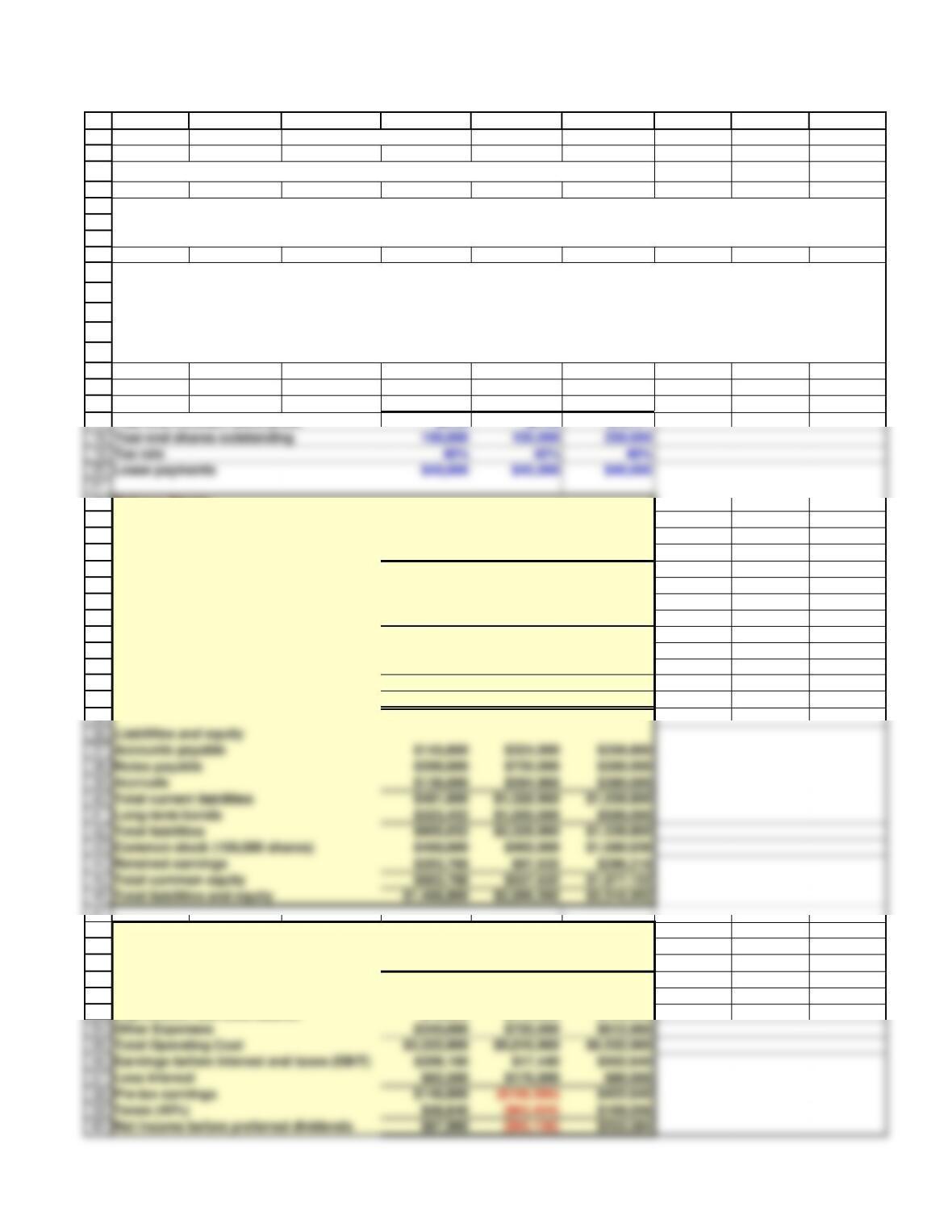

Accounts payable $145,600 $324,000 $359,800

Notes payable $200,000 $720,000 $300,000

Total current liabilities $481,600 $1,328,960 $1,039,800

Long-term bonds $323,432 $1,000,000 $500,000

Total liabilities $805,032 $2,328,960 $1,539,800

Common stock (100,000 shares) $460,000 $460,000 $1,680,936

Retained earnings $203,768 $97,632 $296,216

Total common equity $663,768 $557,632 $1,977,152

Total liabilities and equity $1,468,800 $2,886,592 $3,516,952

47

48

49

50

60

Other Expenses $340,000 $720,000 $612,960

Total Operating Cost $3,222,900 $5,816,960 $6,532,960

Earnings before interest and taxes (EBIT) $209,100 $17,440 $502,640

Less interest $62,500 $176,000 $80,000

Pre-tax earnings $146,600 ($158,560) $422,640

Taxes (40%) $58,640 ($63,424) $169,056

Net Income before preferred dividends $87,960 ($95,136) $253,584

51

52

53

A B C D E F G H I

12/9/2012

Input Data:

2012 2013 2014

Year-end common stock price $8.50 $6.00 $12.17

Balance Sheets

Assets 2012 2013 2014

Cash and equivalents $9,000 $7,282 $14,000

Short-term investments $48,600 $20,000 $71,632

Accounts receivable $351,200 $632,160 $878,000

Inventories $715,200 $1,287,360 $1,716,480

Total current assets $1,124,000 $1,946,802 $2,680,112

Gross Fixed Assets $491,000 $1,202,950 $1,220,000

Less Accumulated Dep. $146,200 $263,160 $383,160

Net Fixed Assets $344,800 $939,790 $836,840

Total Assets $1,468,800 $2,886,592 $3,516,952

Income Statements

2012 2013 2014

Net sales $3,432,000 $5,834,400 $7,035,600

Costs of Goods Sold Except Depr. $2,864,000 $4,980,000 $5,800,000

Depreciation and amortization $18,900 $116,960 $120,000

Jenny Cochran was brought in as assistant to Gary Meissner, Computron’s chairman, who had the task of getting the

company back into a sound financial position. Computron’s 2012 and 2013 balance sheets and income statements, together

with projections for 2014, are shown in the following tables. The tables also show the 2012 and 2013 financial ratios, along

with industry average data. The 2014 projected financial statement data represent Cochran’s and Meissner’s best guess for

2014 results, assuming that some new financing is arranged to get the company “over the hump.”

Chapter 3 Mini Case

The first part of the case, presented in Chapter 3, discussed the situation of Computron Industries after an expansion

program. A large loss occurred in 2013, rather than the expected profit. As a result, its managers, directors, and investors

are concerned about the firm’s survival.

21

Year-end shares outstanding 100,000 100,000 250,000

Tax rate 40% 40% 40%

Lease payments $40,000 $40,000 $40,000

61

62

63

64

65

66

67

68

69

88

Industry

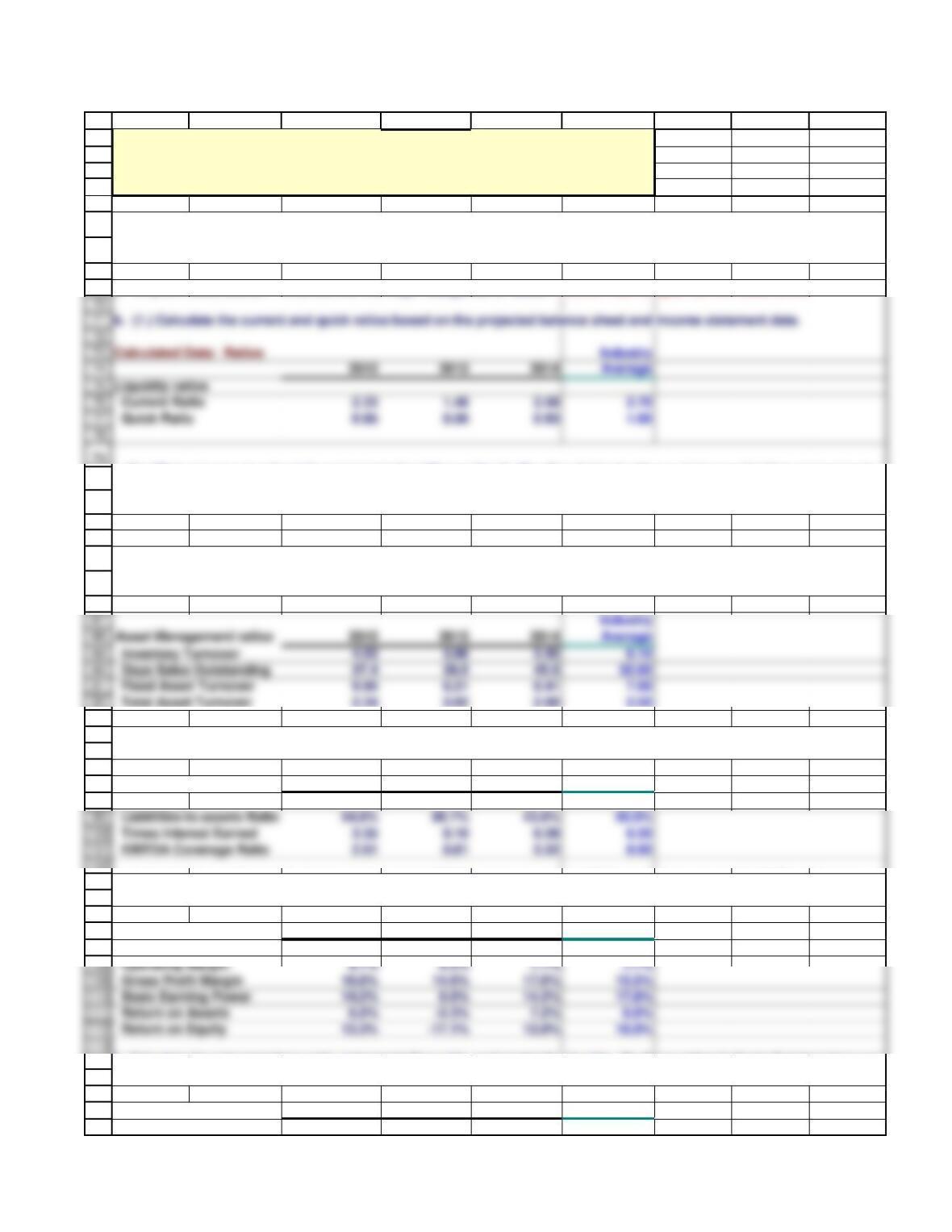

Asset Management ratios 2012 2013 2014 Average

Inventory Turnover 4.03 3.96 3.45 6.10

Days Sales Outstanding 37.4 39.5 45.5 32.00

Fixed Asset Turnover 9.95 6.21 8.41 7.00

Total Asset Turnover 2.34 2.02 2.00 2.50

80

81

82

83

84

85

86

93

94

95

96

97

Liabilities-to-assets Ratio

Times Interest Earned 3.35 0.10 6.28 6.20

EBITDA Coverage Ratio 2.61 0.81 5.52 8.00

98

102

103

104

105

106

Operating Margin 6.1% 0.3% 7.1% 7.1%

Gross Profit Margin 16.6% 14.6% 17.6% 15.5%

Basic Earning Power 14.2% 0.6% 14.3% 17.8%

Return on Assets 6.0% -3.3% 7.2% 9.0%

Return on Equity 13.3% -17.1% 12.8% 18.0%

107

114

115

116

117

118

A B C D E F G H I

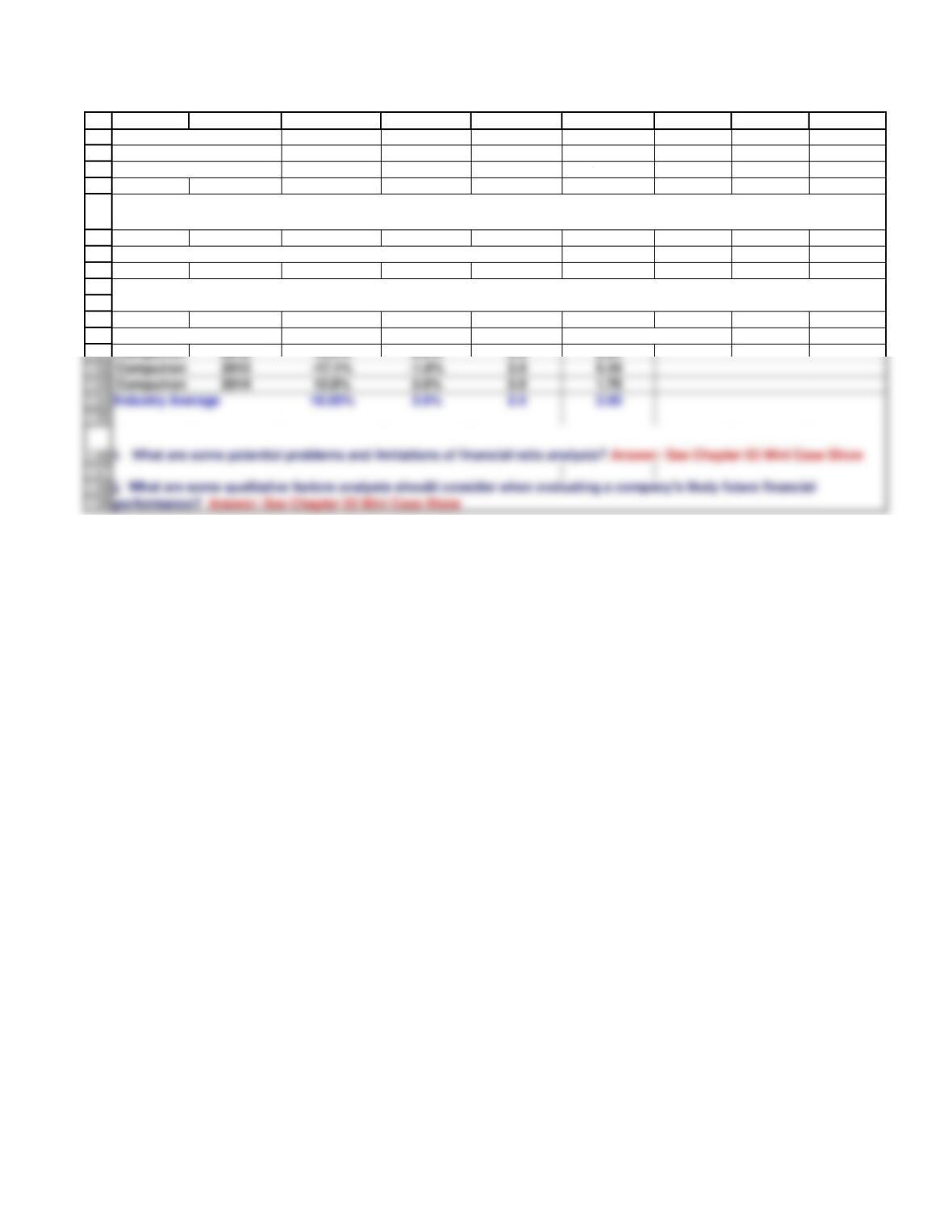

EPS $0.880 ($0.951) $1.014

DPS $0.220 $0.110 $0.220

Book Value Per Share $6.638 $5.576 $7.909

Industry

Debt Management ratios 2012 2013 2014 Average

Debt Ratio 35.6% 59.6% 22.7% 32.0%

Industry

Profitability ratios 2012 2013 2014 Average

Net Profit Margin 2.6% -1.6% 3.6% 3.6%

Industry

Market Value ratios 2012 2013 2014 Average

Price-to Earnings Ratio 9.66 -6.31 12.00 14.20

d. Calculate the debt ratio, liabilities-to-assets ratio, times-interest-earned, and EBITDA coverage ratios. How does

Computron compare with the industry with respect to financial leverage? What can you conclude from these ratios?

e. Calculate the profit margin, basic earning power (BEP), return on assets (ROA), and return on equity (ROE). What can

you say about these ratios?

a. Why are ratios useful? What are the five major categories of ratios? Answer: See Chapter 03 Mini Case Show

c. Calculate the inventory turnover, days sales outstanding (DSO), fixed assets turnover, operating capital requirement, and

total assets turnover. How does Computron’s utilization of assets stack up against other firms in its industry?

Cochran must prepare an analysis of where the company is now, what it must do to regain its financial health, and what

actions should be taken. Your assignment is to help her answer the following questions. Provide clear explanations, not

yes or no answers.

(2.) What can you say about the company’s liquidity position? We often think of ratios as being useful (1) to managers to

help run the business, (2) to bankers for credit analysis, and (3) to stockholders for stock valuation. Would these different

types of analysts have an equal interest in the liquidity ratios? Answer: See Chapter 03 Mini Case Show

f. Calculate the price/earnings ratio, price/cash flow ratio, and market/book ratio. Do these ratios indicate that investors are

expected to have a high or low opinion of the company?

74

Current Ratio 2.33 1.46 2.58 2.70

Quick Ratio 0.85 0.50 0.93 1.00

119

120

121

122

123

124

125

126

127

128

129

130

A B C D E F G H I

Price-to-Cash Flow Ratio 7.95 27.49 8.14 7.60

Market-to-Book Ratio 1.28 1.08 1.54 2.90

Book Value Per Share 6.64 5.58 7.91 na

See the worksheet with the TAB “Common Size and % Change”

DuPont Analysis ROE =

P.M. X

T.A.T.O. X

Equity Multiplier

h. Use the extended DuPont equation to provide a summary and overview of Computron’s projected financial condition.

What are the firm’s major strengths and weaknesses?

g. Perform a common size analysis and percent change analysis. What do these analyses tell you about Computron?

i. What are some potential problems and limitations of financial ratio analysis? Answer: See Chapter 03 Mini Case Show