Answers and Solutions: 29 – 1

Chapter 29

Pension Plan Management

ANSWERS TO END-OF-CHAPTER QUESTIONS

29-1 a. Under a defined benefit plan, the employer agrees to give retirees a specifically

defined benefits package. The payments could be set in final form as of the

retirement date, or they could be indexed to increase with the cost of living.

d. The cash balance plan is a new type of retirement plan developed in the late 1990s. It

is like a defined benefit plan in some respects and like a defined contribution plan in

others. Cash balance plans work like this: An account is created for each employee.

The company promises to put a specified percentage of the employee’s monthly

salary into the plan, and to pay a specified return on the plan’s assets, often the T-bill

rate.

e. An employee’s pension rights are said to be vested if they provide a claim on pension

fund assets, even if the employee leaves the company prior to retirement.

j. The Pension Benefit Guarantee Corporation (PBGC) is a government run insurance

system created by the ERISA to ensure that employees of companies which go

bankrupt before their plans are fully funded will receive benefits.

l. Funding strategy for a pension fund involves two decisions: (1) how fast should any

unfunded liability be reduced, and (2) what rate of return should be assumed in the

actuarial calculations?

m. The investment strategy for a pension plan deals with the question: Given the

assumed actuarial rate of return, how should the portfolio be structured?

p. Tapping fund assets refers to usage of pension fund assets for a corporation’s own

benefit. Given that corporate sponsors administer defined benefit plans which have

assets running into the hundreds of billions of dollars, to what extent should a

corporation be able to tap its pension fund? Should companies be able to use funds to

fight off takeovers? There are no easy answers to these questions.

Answers and Solutions: 29 – 3

29-2 Ideally, the employee will choose the plan that provides the incremental cash flows (both

costs and benefits) that maximize the employee’s expected utility of consumption.

29-3 From an employer’s standpoint, the defined benefit plan’s major advantage is promotion

of low employee turnover. The economic consequences of job-changing are not

desirable under a defined benefit plan, since benefits are frozen at the time of separation,

instead of adjusted for inflation over time. Thus, defined benefit plans provide incentive

to stay with the firm for a long period.

However, there are several disadvantages associated with defined benefit plans. First,

the plan puts greater risk on employers, since it guarantees to pay employees a fixed

retirement benefit regardless of the firm’s ability to fully fund the plan. Second, the

employer’s future cash contributions to the plan are uncertain, thus hampering financial

Answers and Solutions: 29 – 4

29-4 If the returns on these assets are less than perfectly positively correlated with the fund’s

other assets, then the addition of such investments as foreign stocks and precious metals

29-5 a. Defined benefit plans carry with them economic incentive to discriminate against

older workers in hiring, while defined contribution plans and cash balance plans are

neutral in this regard.

b. There is an economic incentive for employers to discriminate against women in their

hiring practices if they use defined benefit plans, since women tend to live longer

than men.

c. Defined benefit plans contribute to lower employee turnover that would reduce

training costs.

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

29-1 a. His wage in the final year of working is $179,700:

$20,000(1.05)45 = $20,000(8.9850) = $179,700.

Thus, his annual retirement benefit is $80,865:

$179,700(0.01)(45) = $80,865.

c. Final year wage = $20,000(1.05)20 = $53,066.

Annual retirement benefit = $53,066(0.01)(20) = $10,613.

Lump sum required = $10,613(PVIFA10%,15) = $80,723.

Annual contribution = $1,409:

$80,723 = PMT(FVIFA10%,20)

PMT = $1,409.

Answers and Solutions: 29 – 6

29-2 a. Required return = r = rRF + (rM – rRF)b = 10% + (6%)1.2 = 17.2%.

Realized return =

r

= 18.0%.

Alpha =

r

– r = 18.0% – 17.2% = 0.8 percentage points.

b. If the portfolio return was net of all transactions costs and management fees, then the

portfolio manager “outperformed the market” on a risk-adjusted basis. This may be

due to his extraordinary ability to identify undervalued stocks or, more commonly,

sheer luck.

Answers and Solutions: 29 – 7

29-3 a. Find the present value (today’s value) of the firm’s obligations.

To simplify calculations, find the value of each 5-year period’s payment as of the

beginning of the period. For example, the value at Time 10 of the payments for Years

11-15 is:

10 11 12 13 14 15

| | | | | |

2,500,000 2,500,000 2,500,000 2,500,000 2,500,000

Mini Case: 29 – 8

MINI CASE

Southeast Tile Distributors Inc. is a building tile wholesaler that originated in Atlanta but

is now considering expansion throughout the region to take advantage of continued strong

population growth. The company has been a “mom and pop” operation supplemented by

part-time workers, so it currently has no corporate retirement plan. However, the firm’s

owner, Andy Johnson, believes that it will be necessary to start a corporate pension plan to

attract the quality employees needed to make the expansion succeed. Andy has asked you,

a recent business school graduate who has just joined the firm, to learn all that you can

about pension funds, and then prepare a briefing paper on the subject. To help you get

started, he sketched out the following questions:

a. How important are pension funds to the U. S. Economy?

b. Define the following pension fund terms:

1. Defined benefit plan

2. Defined contribution plan

3. Profit sharing plan

4. Cash balance plan

5. Vesting

6. Portability

7. Fully funded; overfunded; underfunded

8. Actuarial rate of return

9. Employee Retirement Income Security Act (ERISA)

10. Pension Benefit Guarantee Corporation (PBGC)

Answer: 1. Under a defined benefit plan, the employer agrees to give retirees a specific

defined benefit, such as $500 per month, 80 percent of his or her average salary

Mini Case: 29 – 9

5. An employee is vested if he or she has the right to receive pension benefits even

if they leave the company prior to retirement. If the employee loses his or her

pension rights upon leaving the company prior to retirement, the rights are said

to be nonvested. Most plans today have deferred vesting, in which pension rights

are nonvested for the first few years, say 5, and then become fully vested at that

point.

6. A portable pension plan is one that an employee can carry from one employer to

another. Portability is especially important in industries where job changes are

frequent—as in trucking and construction—and union-administered plans are

typically used to make portability possible.

7. If the present value of expected retirement benefits is equal to plan assets on

10. The Pension Benefit Guarantee Corporation (PBGC) is a government-run

insurance company created by the ERISA to ensure that employees of companies

which go bankrupt before their plans are fully funded will receive benefits.

Mini Case: 29 – 10

c. What two organizations provide guidelines for reporting pension fund activities

to stockholders? Describe briefly how pension fund data are reported in a firm’s

financial statements. (hint: consider both defined contribution and defined

benefit plans.)

Answer: The Financial Accounting Standards Board (FASB), together with the SEC,

establishes the rules under which a firm reports its financial results, including its

d. Assume that an employee joins the firm at age 25, works for 40 years to age 65,

and then retires. The employee lives another 15 years, to age 80, and during

retirement draws a pension of $20,000 at the end of each year. How much must

the firm contribute annually (at year-end) over the employee’s working life to

fully fund the plan by retirement age if the plan’s actuarial expected rate of

return is 10% and its assumed interest rate for discounting pension benefits also

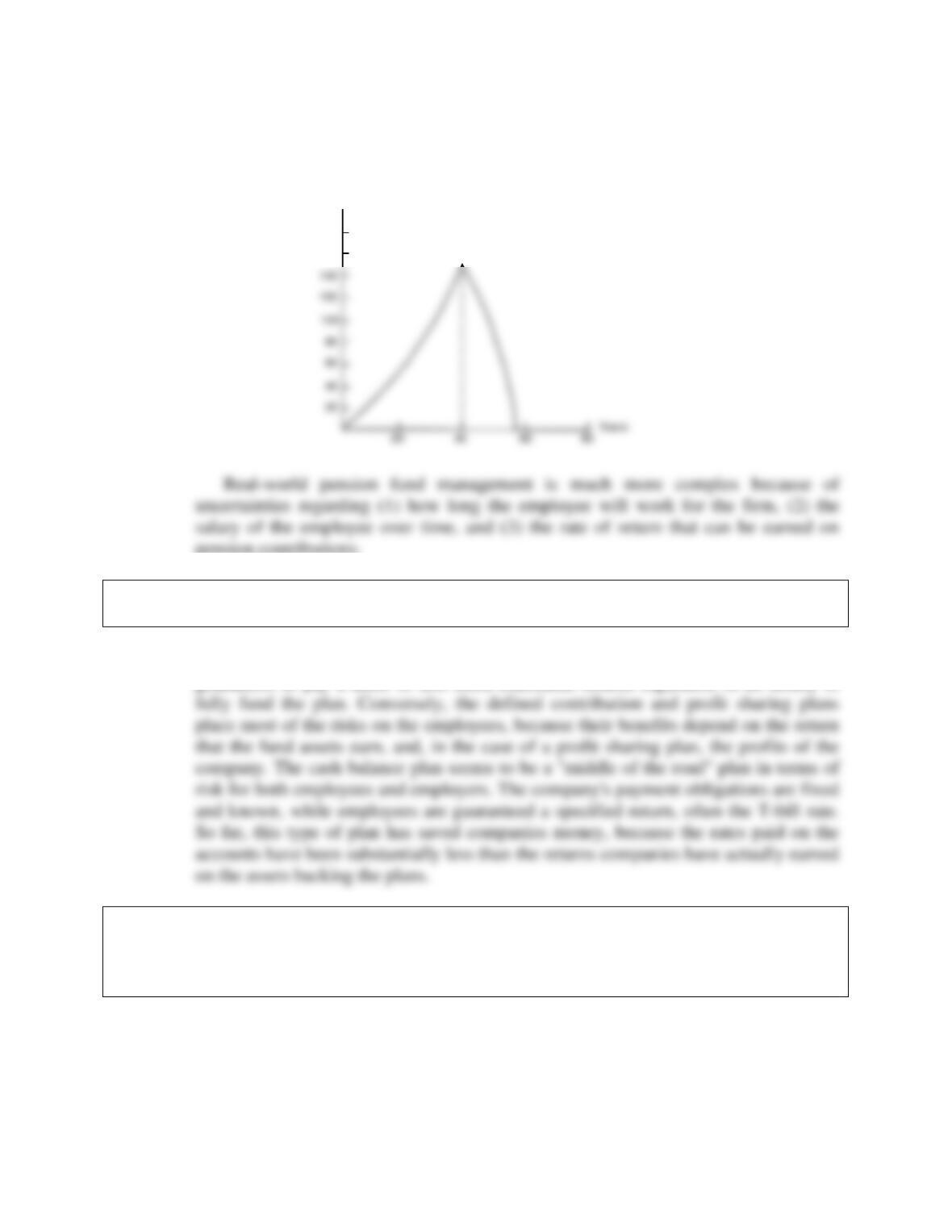

is 10%? Draw a graph which shows the value of the employee’s pension fund

over time. Why is real-world pension fund management much more complex

than indicated in this illustration?

Answer: The employee will draw an annual pension (an annuity) of $20,000 for 15 years.

Thus, the firm must accumulate $152,121.59 in the pension plan by the time the

employee retires to fully fund the retirement:

Mini Case: 29 – 11

A graph of the employee’s pension fund assets looks like this:

pension contributions.

e. Discuss the risks to both the plan sponsor and plan beneficiaries under the four

types of pension plans.

Answer: The defined benefit plan places most of the risks on the company, because it

guarantees to pay a more or less fixed retirement benefit regardless of its ability to

f. How does the type of pension plan influence decisions in each of the following

areas:

1. The possibility of age discrimination in hiring?

of Dollars

Thousands

160

180

of Dollars

Thousands

160

180

Mini Case: 29 – 12

Answer: Defined benefit plans are more costly to firms when older workers are hired as

f. 2. The possibility of sex discrimination in hiring?

Answer: Since women live longer than men, female employees are more costly than male

f. 3. Employee training costs?

Answer: To the extent that defined benefit plans encourage employees to stay with a single

f. 4. The militancy of unions when a company faces financial adversity?

Answer: Since defined benefit plan benefits are usually tied to the number of years worked and

ensure its survival if it has a defined benefit plan.

g. What are the two components of a plan’s funding strategy? What is the primary

goal of a plan’s investment strategy?

Answer: The two components of a plan’s funding strategy are:

h. How can a corporate financial manager judge the performance of pension plan

managers?

Answer: Pension plan managers can be judged in several ways. One way is to compare the

Mini Case: 29 – 13

i. What is meant by “tapping” pension fund assets? Why is this action so

controversial?

Answer: Pension fund assets are tapped when a company terminates an overfunded defined

j. What has happened to the cost of retiree health benefits over the last decade?

How are retiree health benefits reported to shareholders?

Answer: Because of the increased number of retirees, and the dramatic escalation in health

care costs over the past 10 years, many companies are facing situations where retiree