(AR) = (DSO)(ADS) =

Accounts Receivable

the higher the dollar cost of carrying receivables.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

29

30

31

32

33

34

38

39

40

46

47

48

49

50

51

52

A B C D E F G H I J

12/10/2012

JAN $100

FEB 200

MAR 300

APR 300

MAY 200

JUN 100

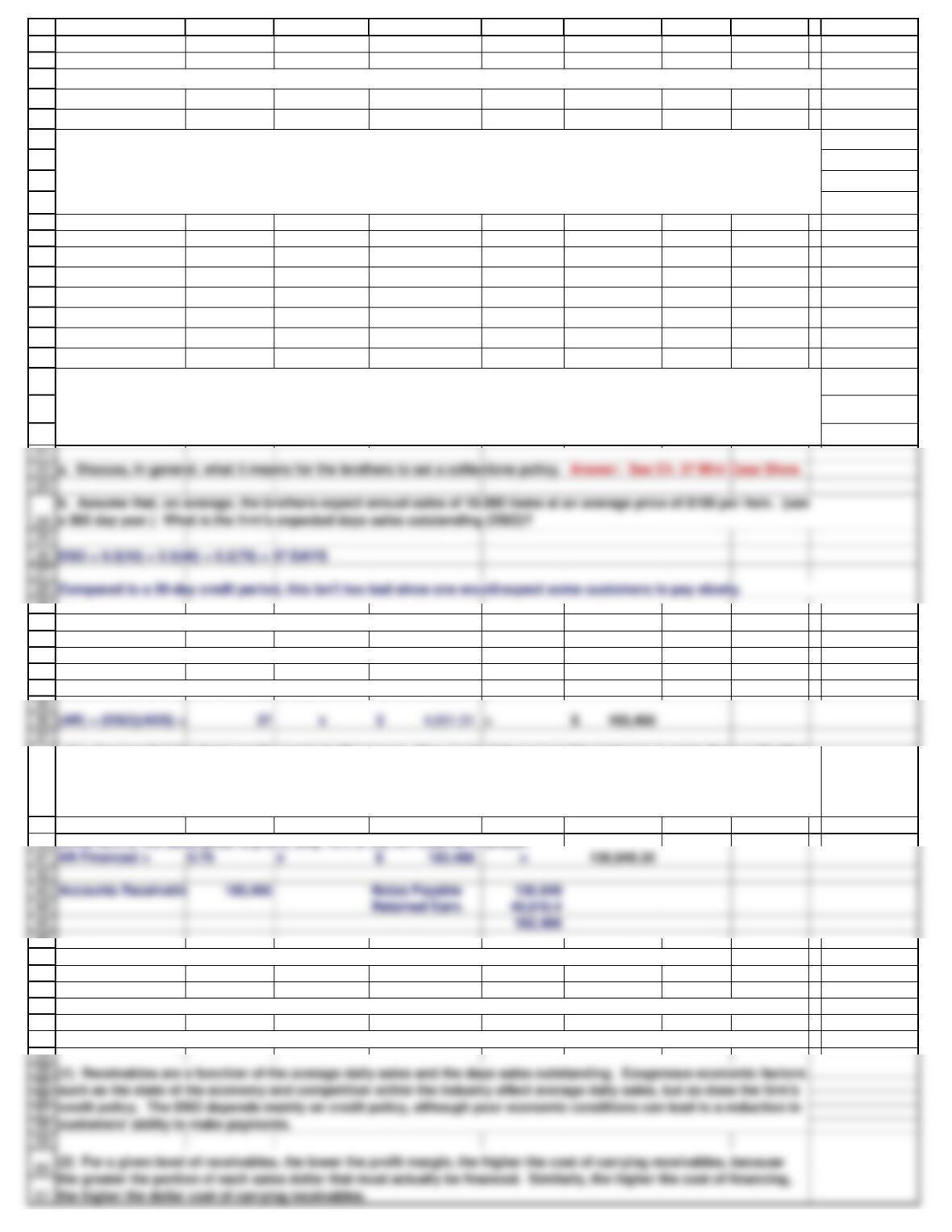

AVERAGE DAILY SALES = ADS = 18,000 (100)/365 = 4,931.51$ per day

cost = 12% x 136,849.32 = 16,421.92

(2.) What is its expected average daily sales (ADS)?

(4.) Assume that the firm’s profit margin is 25 percent. How much of the receivables balance must be financed? What

would the firm’s balance sheet figures for accounts receivable, notes payable, and retained earnings be at the end of one

year if notes payable are used to finance the investment in receivables? Assume that the cost of carrying receivables

had been deducted when the 25 percent profit margin was calculated.

(3.) What is its expected average accounts receivable (AR) level?

5. If loans have a cost of 12 percent, what is the annual dollar cost of carrying the receivables?

Since 25% of the sales price is profit, only 75% of the AR must be financed:

c. What are some factors which influence (1) a firm’s receivables level and (2) the dollar cost of carrying receivables?

Also there is the opportunity cost of not having use of the profit component of the receivables.

Chapter 27. Mini Case for Providing and Obtaining Credit

Rich Jackson, a recent finance graduate, is planning to go into the wholesale building supply business with his brother,

Jim, who majored in building construction. The firm would sell primarily to general contractors, and it would start

operating next January. Sales would be slow during the cold months, rise during the spring, and then fall off again in the

summer, when new construction in the area slows. Sales estimates for the first 6 months are as follows (in thousands of

dollars):

The terms of sale are net 30, but because of special incentives, the brothers expect 30 percent of the customers (by

dollar value) to pay on the 10th day following the sale, 50 percent to pay on the 40th day, and the remaining 20 percent to

pay on the 70th day. No bad debt losses are expected, because Jim, the building construction expert, knows which

contractors are having financial problems.

a. Discuss, in general, what it means for the brothers to set a collections policy. Answer: See Ch. 27 Mini Case Show.

DSO = 0.3(10) + 0.5(40) + 0.2(70) = 37 DAYS

Compared to a 30-day credit period, this isn’t too bad since one would expect some customers to pay slowly.

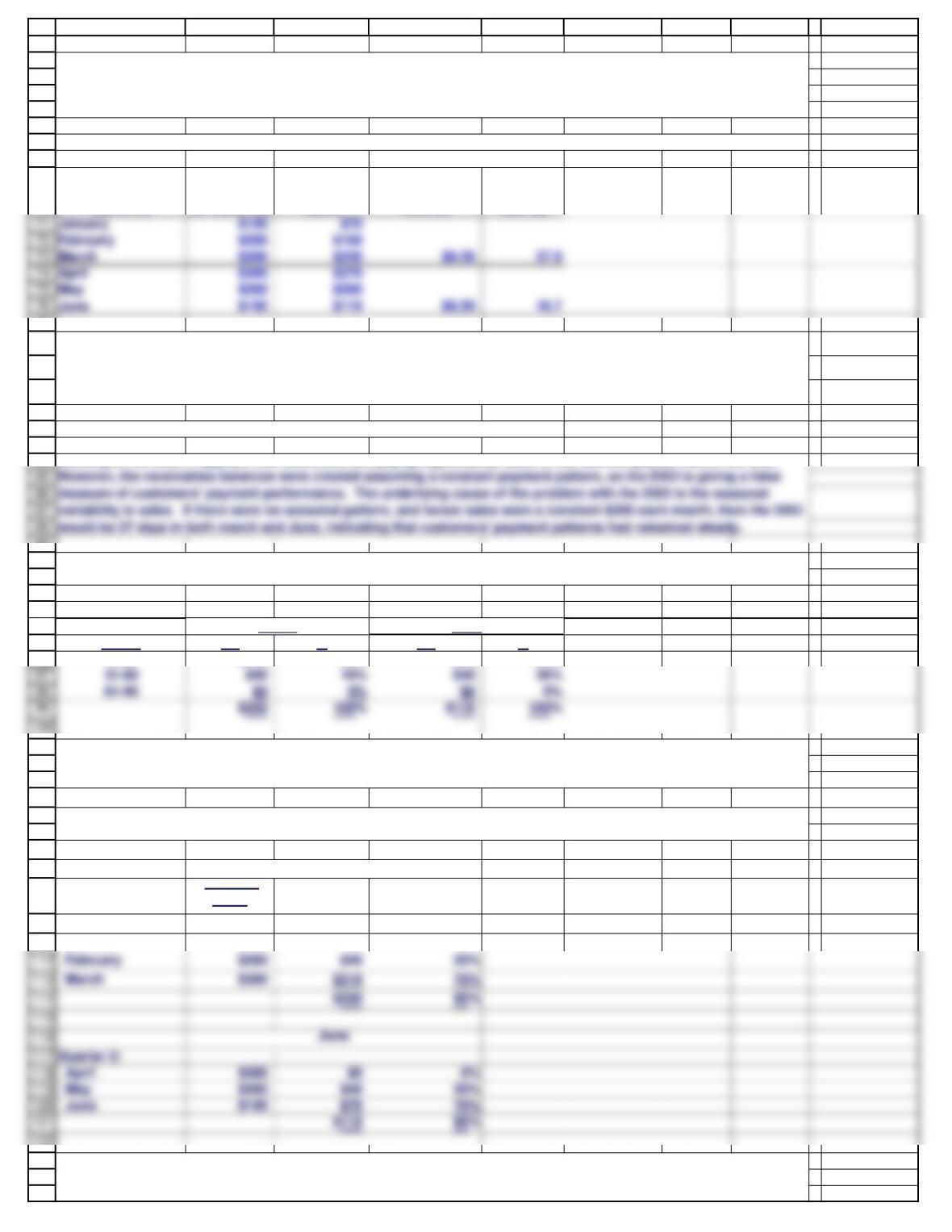

measure of customers’ payment performance. The underlying cause of the problem with the DSO is the seasonal

variability in sales. If there were no seasonal pattern, and hence sales were a constant $200 each month, then the DSO

would be 27 days in both march and June, indicating that customers’ payment patterns had remained steady.

100

62

63

64

65

66

67

68

69

70

77

78

79

80

81

82

83

89

90

91

92

93

94

95

96

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

121

February $200 $40 20%

March $300 $210 70%

Quarter 2:

April $300 $0 0%

May $200 $40 20%

June $100 $70 70%

122

123

124

125

A B C D E F G H I J

Month (1)

Credit Sales

for Month (2)

Receivables

at End of

Month

ADS (4) DSO (5)

Age of Account

(Days) AR %AR %

0-30 $210 84% $70 64%

Monthly

Sales

Contribution

to AR

AR to Sales

Ratio

Quarter 1:

January $100 $0 0%

d. Assuming that the monthly sales forecasts given previously are accurate, and that customers pay exactly as was

predicted, what would the receivables level be at the end of each month? To reduce calculations, assume that 30

percent of the firm’s customers pay in the month of sale, 50 percent pay in the second month following the sale, and

the remaining 20 percent pay in the second month following the sale. Note that this is a different assumption than was

g. Construct the uncollected balances schedules for the end of March and the end of June. Do these schedules

properly measure customers’ payment patterns?

March

June

March

Note that the end of June ageing schedule suggests that customers are paying more slowly than in the earlier quarter.

However we know that the payment pattern has remained constant, so the firm’s customers’ payment performance has

not changed. The apparent change is due to the seasonal fluctuations.

h. Assume that it is now July of Year 1, and the brothers are developing pro forma financial statements for the

following year. Further, assume that sales and collections in the first half-year matched the predicted levels. Using

the year 2 sales forecasts as shown next, what are next year’s pro forma receivables levels for the end of march and for

f. Construct aging schedules for the end of March and the end of June. Do these schedules properly measure

customers‘ payment patterns? If not, why not?

AR = 0.7(SALES IN THAT MONTH) + 0.2(SALES IN PREVIOUS MONTH).

Quarterly Statement

e. What is the firm’s forecasted average daily sales for the first 3 months? For the entire half-year? The days sales

outstanding is commonly used to measure receivables performance. What DSO is expected at the end of March? At

the end of June? What does the DSO indicate about customers’ payments? Is DSO a good management tool in this

situation? If not, why not?

Looking at the DSO, it appears that customers are paying significantly faster in the second quarter than in the first.

See above in question (D) for average daily sales and DSO at the end of the quarter.

126

127

128

129

130

142

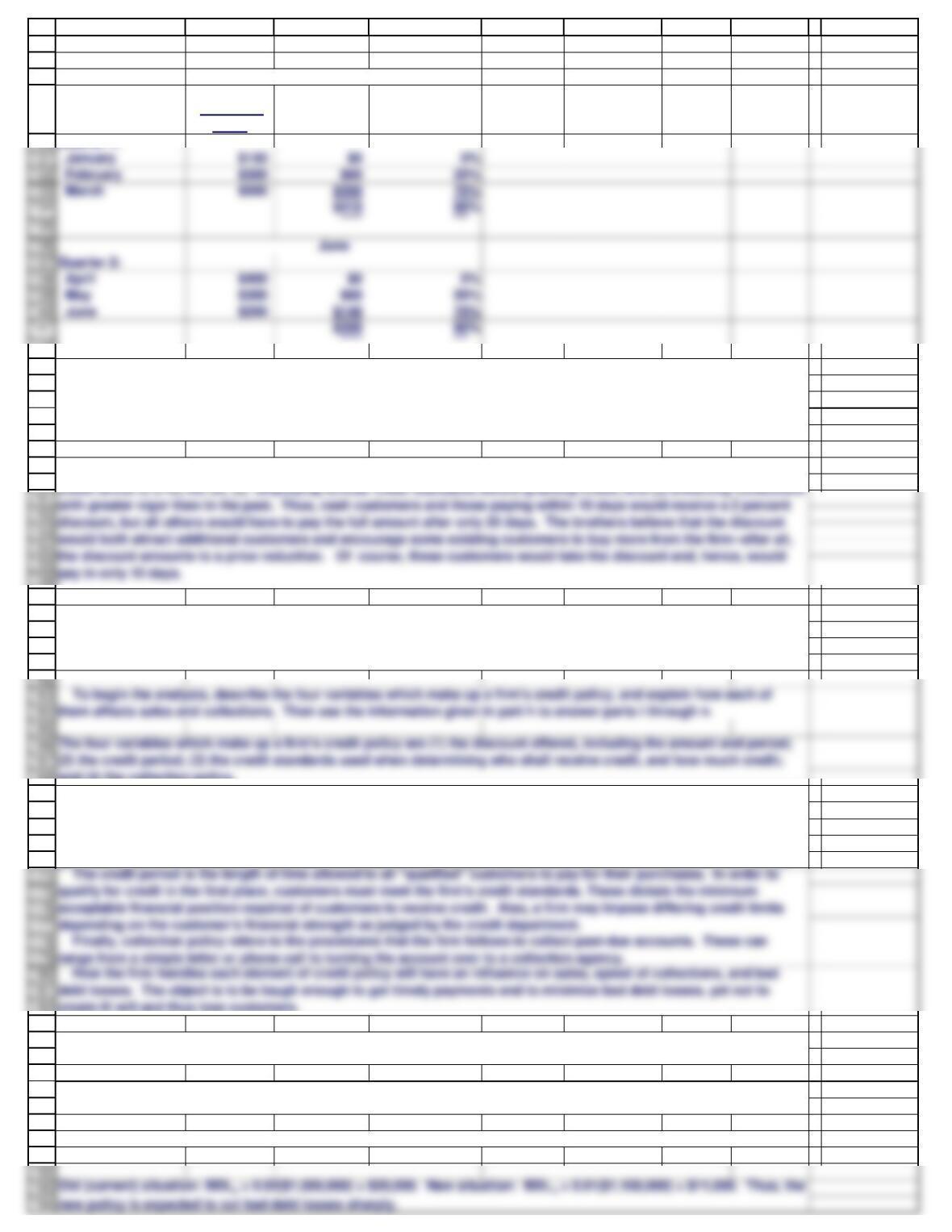

The four variables which make up a firm’s credit policy are (1) the discount offered, including the amount and period;

(2) the credit period; (3) the credit standards used when determining who shall receive credit, and how much credit;

To begin the analysis, describe the four variables which make up a firm’s credit policy, and explain how each of

them affects sales and collections. Then use the information given in part h to answer parts i through n.

depending on the customer’s financial strength as judged by the credit department.

Finally, collection policy refers to the procedures that the firm follows to collect past-due accounts. These can

range from a simple letter or phone call to turning the account over to a collection agency.

How the firm handles each element of credit policy will have an influence on sales, speed of collections, and bad

debt losses. The object is to be tough enough to get timely payments and to minimize bad debt losses, yet not to

new policy is expected to cut bad debt losses sharply.

143

144

145

146

147

148

149

150

157

158

159

160

161

168

169

170

171

172

173

182

183

184

185

186

187

188

189

190

191

A B C D E F G H I J

Predicted

Sales

Predicted

Contribution

to AR

Predicted AR to

Sales Ratio

Quarter 1:

k. What is the dollar amount of the firm’s current bad debt losses? What losses would be expected under the new

March

i. Assume now that it is several years later. The brothers are concerned about the firm’s current credit terms, which

are now net 30, which means that contractors buying building products from the firm are not offered a discount, and

they are supposed to pay the full amount in 30 days. Gross sales are now running $1,000,000 a year, and 80 percent

(by dollar volume) of the firms paying customers generally pay the full amount on day 30, while the other 20 percent

pay, on average, on day 40. Two percent of the firm’s gross sales end up as bad debt losses.

Cash discounts generally produce two benefits: (1) they attract both new customers and expanded sales from

current customers, because people view discounts as a price reduction, and (2) discounts cause a reduction in the

days sales outstanding, since both new customers and some established customers will pay more promptly in order to

get the discount. Of course, these benefits are offset to some degree by the dollar cost of the discounts themselves.

and (4) the collection policy.

create ill will and thus lose customers.

j. Under the current credit policy, what is the firm’s days sales outstanding (DSO)? What would the expected DSO be

if the credit policy change were made?

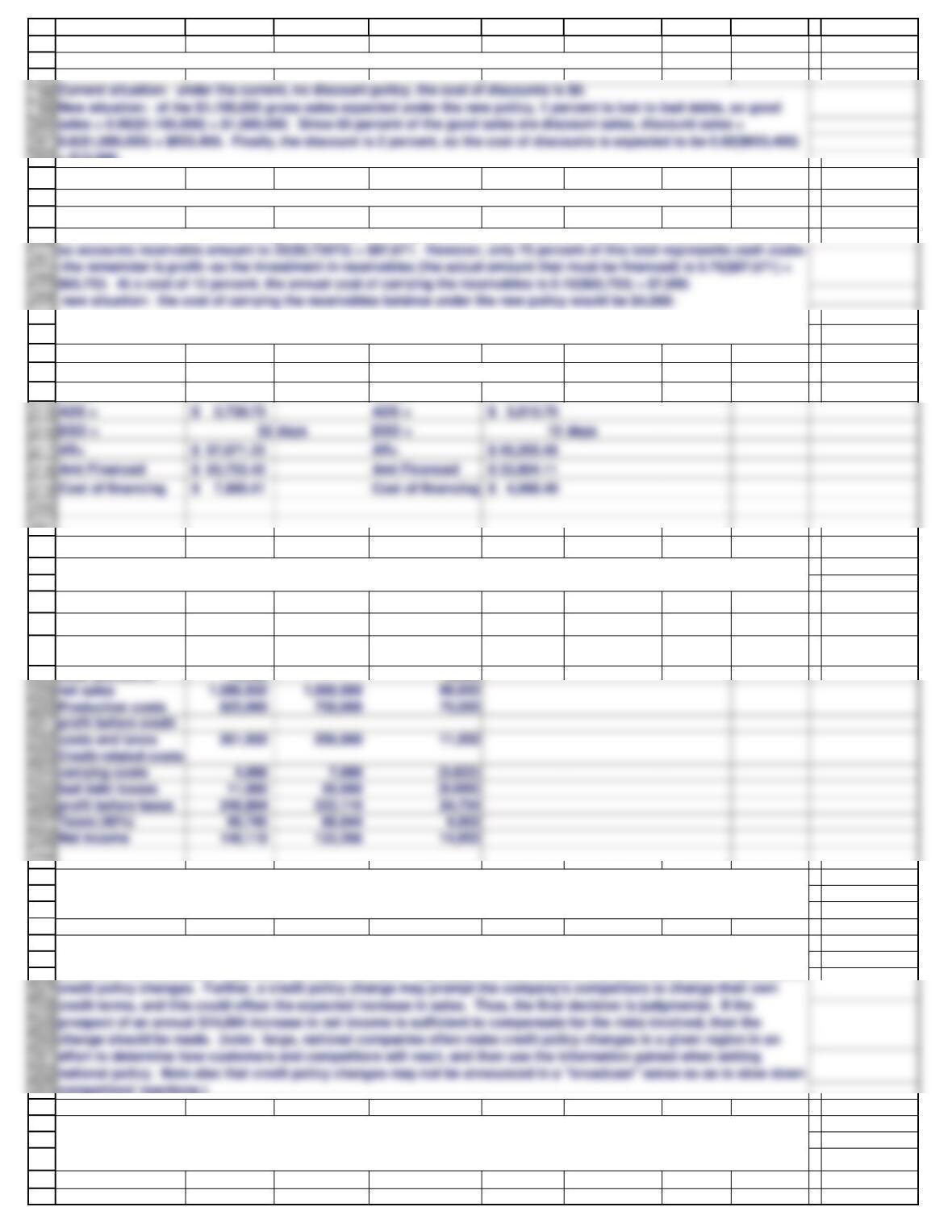

Old (current) situation: DSO0 = 0.8(30) + 0.2(40) = 32 days. New situation: DSOn = 0.6(10) + 0.3(20) + 0.1(30) = 15 days.

Thus, the new credit policy is expected to cut the DSO in half.

The brothers are now considering a change in the firm’s credit policy. The change would entail (1) changing the

The net expected result is for sales to increase to $1,100,000; for 60 percent of the paying customers to take the

discount and pay on the 10th day; for 30 percent to pay the full amount on day 20; for 10 percent to pay late on day 30;

and for bad debt losses to fall from 2 percent to 1 percent of gross sales. The firm’s operating cost ratio will remain

unchanged at 75 percent, and its cost of carrying receivables will remain unchanged at 12 percent.

134

135

141

January $150 $0 0%

February $300 $60 20%

March $500 $350 70%

Quarter 2:

April $400 $0 0%

May $300 $60 20%

June $200 $140 70%

net sales 1,086,932 1,000,000 86,932

Production costs 825,000 750,000 75,000

costs and taxes 261,932 250,000 11,932

carrying costs 4,068 7,890 (3,822)

bad debt losses 11,000 20,000 (9,000)

profit before taxes 246,864 222,110 24,754

Taxes (40%) 98,745 88,844 9,902

Net income 148,118 133,266 14,852

195

196

202

203

204

205

210

211

212

213

214

221

222

223

224

225

226

227

228

239

240

241

242

243

244

245

253

254

255

256

257

258

259

A B C D E F G H I J

Current situation Proposed situation

Sales 1,000,000$ Sales

$ 1,100,000

New

Old Difference

Gross sales 1,100,000 1,000,000

100,000

Less discounts 13,068 – 13,068

New

However, the new policy is not riskless. If the firm’s customers do not react as predicted, then the firm’s profits could

actually decrease as a result of the change. The amount of risk involved in the decision depends on the uncertainty

inherent in the estimates, especially the sales estimate. Typically, it is very difficult to predict customers‘ responses to

competitors’ reactions.)

n. What is the incremental after-tax profit associated with the change in credit terms? Should the company make the

change? (assume a tax rate of 40 percent.)

o. Suppose the firm makes the change, but its competitors react by making similar changes to their own credit terms,

with the net result being that gross sales remain at the current $1,000,000 level. What would the impact be on the

firm’s post-tax profitability?

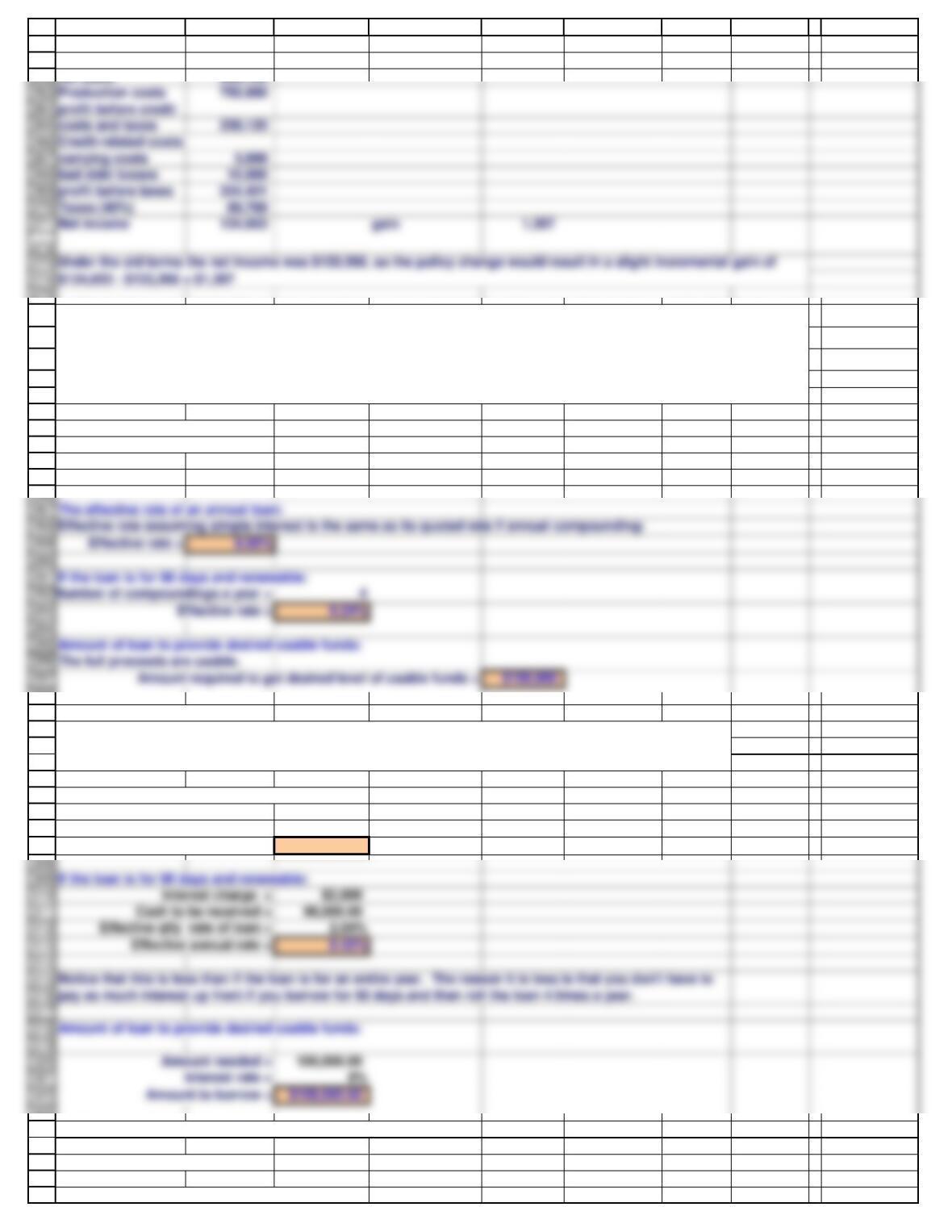

Thus, if expectations are met, the credit policy change would increase the firm’s annual after-tax profit by $14,852.

Since there are no non-cash expenses involved here, the $14,852 is also the incremental cash flow expected under the

new policy.

Current situation: the firm’s average daily sales currently amount to $1,000,000/365 = $2,739.73. The DSO is 32 days,

($1,100,000/365)(15)(0.75)(0.12) = $4,068.

m. What is the firm’s current dollar cost of carrying receivables? What would it be after the proposed change?

= $13,068.

l. What would be the firm’s expected dollar cost of granting discounts under the new policy?

288

289

292

293

296

297

The effective rate of an annual loan:

If the loan is for 90 days and renewable:

Amount of loan to provide desired usable funds:

260

261

262

275

276

277

278

279

280

281

282

283

284

285

298

299

300

301

302

303

304

305

306

307

312

313

321

322

If the loan is for 90 days and renewable:

Amount of loan to provide desired usable funds:

323

324

325

326

327

328

A B C D E F G H I J

Gross sales 1,000,000

Less discounts 11,880

net sales 988,120

Desired loan amount = $100,000

Quoted interest rate = 8%

(1) Simple interest:

(2) Discount interest:

The effective rate of an annual loan:

Interest charge = $8,000

Cash to be received = 92,000.00

Effective rate of loan = 8.70%

(3) discount interest with a 10 percent compensating balance.

compensating bal. % = 10%

The effective rate of an annual loan:

In a discount interest loan, the bank deducts the interest in advance. Therefore, the borrower receives

less than the face value of the loan. From this, we can determine the actual cash received by the interest

charge, the borrower and the effective rate of such a loan.

p. The brothers need $100,000 and are considering a 1-year bank loan with a quoted annual rate of 8%. The bank is

offering the following alternatives: (1) simple interest, (2) discount interest, (3) discount interest with a 10%

compensating balance, and (4) add-on interest on a 12-month installment loan. What is the effective annual cost rate

for each alternative? For the first three of these assumptions, what is the effective rate if the loan is for 90 days, but

renewable? How large must the face value of the loan amount actually be in each of the 4 alternatives to provide

$100,000 in usable funds at the time the loan is originated?

Production costs 750,000

profit before credit

Credit-related costs:

carrying costs 3,699

bad debt losses 10,000

profit before taxes 224,421

Taxes (40%) 89,769

334

335

336

337

338

339

340

341

342

352

353

343

344

345

346

354

355

356

357

358

359

360

361

366

367

370

371

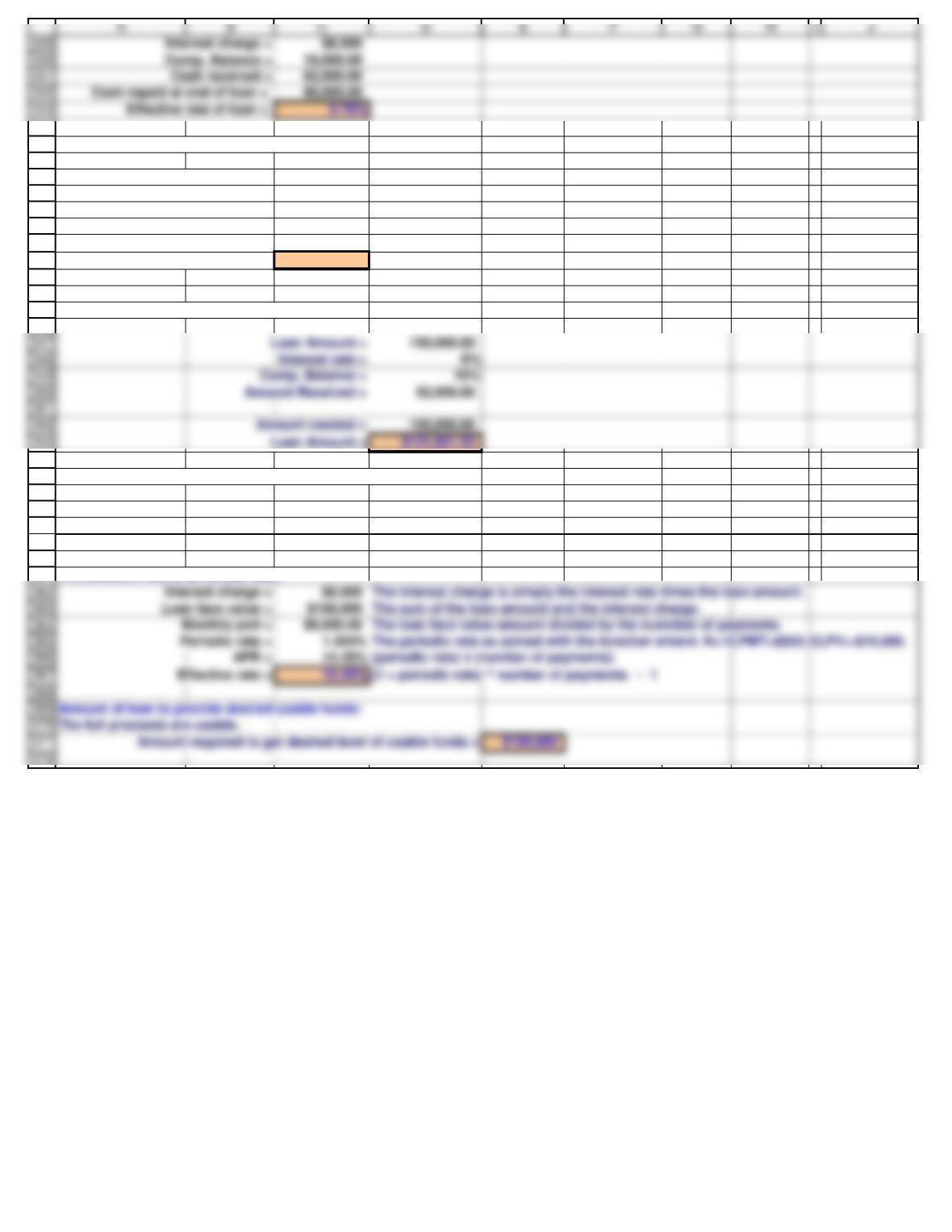

Interest charge = $8,000 The interest charge is simply the interest rate times the loan amount.

Amount of loan to provide desired usable funds:

If the loan is for 90 days and renewable:

Interest charge = $2,000

Comp. Balance = 10,000.00

Cash received = 88,000.00

Cash repaid at end of loan = 90,000.00

Effective qtly rate of loan = 2.2727%

Effective annual rate = 9.41%

Amount of loan to provide desired usable funds:

(4) Add-on interest on a 12-month installment loan.

Loan amount $100,000

Payments 12

Interest rate 8%

The effective rate of an annual loan:

332

333

Interest charge = $8,000

Comp. Balance = 10,000.00

Cash received = 82,000.00