Answers and Solutions: 27 – 1

Chapter 27

Providing and Obtaining Credit

ANSWERS TO END-OF-CHAPTER QUESTIONS

27-1 a. Cash discounts are often used to encourage early payment and to attract customers by

effectively lowering prices. Credit terms are usually stated in the following form:

2/10, net 30. This means a 2 percent discount will apply if the account is paid within

10 days, otherwise the account must be paid within 30 days.

b. Seasonal dating sets the invoice date, or date at which the credit and discount periods

d. The payments pattern approach is a procedure which measures any changes that

might occur in customers’ payment behavior. The advantage of this approach is that

it is not affected by changes in sales levels due to cyclical or seasonal factors. The

uncollected balances schedule, which is an integral part of the payments pattern

approach, helps a firm monitor its receivables better and also forecast future

receivables balances.

27-2 The latest date for paying and taking discounts is May 10. The date by which the

payment must be made is June 9.

27-3 False. An aging schedule will give more detail, especially as to what percentage of

accounts are past due and what percentage of accounts are taking discounts.

Answers and Solutions: 27 – 2

27-5 AR Sales Profit

a. The firm tightens its credit

standards. – – 0

Explanations:

a. When a firm “tightens” its credit standards, it sells on credit more selectively. It will

likely sell less and certainly will make fewer credit sales. Profit may be affected in

either direction.

d. If the credit manager gets tough with past due accounts, sales will decline, as will

accounts receivable.

Answers and Solutions: 27 – 3

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

27-1 $25,000 interest-only loan, 11% nominal rate. Interest calculated as simple interest based

on 365-day year. Interest for 1st month = ?

27-2 $15,000 installment loan, 11% nominal rate.

Effective annual rate, assuming a 365-day year = ?

Add-on interest = 0.11($15,000) = $1,650.

Monthly Payment =

12

650,1$000,15$+

= $1,387.50.

Answers and Solutions: 27 – 4

27-3 a. Effective rate = 12%.

b. 0 1

| |

50,000 -50,000

2.01

−

= $62,500. The effective interest rate will still be 11.25%.

c. 0 1

| |

50,000 -50,000

– 4,375 (discount interest) 7,500

i = ?

i = ?

d. Approximate annual rate =

)/2000,50($

)000,50)($08.0(

=

000,25$

000,4$

= 16%.

Alternative b has the lowest effective interest rate.

27-4 a. The quarterly interest rate is equal to 11.25%/4 = 2.8125%.

Effective annual rate = (1 + 0.028125)4 – 1

= 1.117336 – 1 = 0.117336 = 11.73%.

b. 0 1

Note that, if Gifts Galore actually needs $1,500,000 of funds, it will have to borrow

2.00225.01

000,500,1$

−−

=

7775.0

000,500,1$

= $1,929,260.45. The effective interest rate will still

be 12.088% ≈ 12.09%.

c. Installment loan:

27-5 Analysis of change:

Projected Income Projected Income

Statement Effect of Statement

Under Current Credit Policy Under New

Credit Policy Change Credit Policy

Credit-related costs:

Cost of carrying

receivables* 15,781 + 8,260 24,041

Collection expense 35,000 – 13,000 22,000

Bad debt losses 24,000 + 16,625 40,625

Profit before taxes $ 325,219 -$ 5,635 $ 319,584

Taxes (40%) 130,088 – 2,254 127,834

Net income $ 195,131 -$ 3,381 $ 191,750

27-6 Analysis of change:

Projected Income Projected Income

Statement Effect of Statement

Under Current Credit Policy Under New

Credit Policy Change Credit Policy

Bad debt losses 0 0 0

Profit before taxes $ 275,445 +$ 45,961 $ 321,406

Taxes (40%) 110,178 + 18,384 128,562

Net income $ 165,267 +$ 27,577 $ 192,844

*Cost of carrying receivables:

Answers and Solutions: 27 – 8

27-7 a. Simple interest: 12%.

b. 3-months: (1 + 0.115/4)4 – 1 = 12.0055%, or use the interest conversion feature of

your calculator as follows:

NOM% = 11.5; P/YR = 4; EFF% = ? EFF% = 12.0055%.

Enter N = 12, PV = 100, PMT = -8.8333, FV = 0, and press I to get

I = 0.908032% = rd. This is a monthly periodic rate, so the effective annual rate =

(1.00908032)12 – 1 = 0.1146 = 11.46%.

Answers and Solutions: 27 – 9

27-8 a. March receivables = $120,000(0.8) + $100,000(0.5) = $146,000.

June receivables = $160,000(0.8) + $140,000(0.5) = $198,000.

or ADS = ($3,000 + $4,500)/2 = $3,750.

DSO = $198,000/$3,750 = 52.8 days.

c. Age of Accounts Dollar Value Percent of Total

0 – 30 days $128,000 65%

31 – 60 70,000 35

61 – 90 0 0

$198,000 100%

27-9 a. Malone’s current accounts payable balance represents 60 days purchases. Daily

purchases can be calculated as

60

500$

= $8.33.

Answers and Solutions: 27 – 10

b. Takes Discounts:

If Malone takes discounts its A/P balance would be $83.33. The cash it would need

to be loaned is $500 – $83.33 = $416.67.

Since the loan is a discount loan with compensating balances, Malone would require

more than a $416.67 loan.

c. Nonfree Trade Credit:

Nominal annual cost:

period

Discount

goutstandin is

credit Days

360

% Discount100

%Discount

−

−

=

20

360

99

1

= 18.18%.

0 1

| |

384.62 -384.62

-57.69 Discount interest +76.92

-76.92 Compensating balance -307.70

250.00

0 1

| |

641.03 -641.03

-96.15 Discount interest +128.21

-128.21 Compensating balance -512.82

416.67

Answers and Solutions: 27 – 12

d. Pro Forma Balance Sheet (Thousands of Dollars):

Casha $ 126.9 Accounts payable $ 250.0

Accounts receivable 450.0 Notes payableb 434.6

Answers and Solutions: 27 – 13

e. To reduce the accounts payable by $250,000, which reflects the 1% discount, Malone

must pay the full cost of the payables, which is $250,000/0.99 = $252,525.25. The

lost discount is the difference between the full cost of the payables and the amount

Face amount of loan =

0.65

5$251,515.1

0.200.151

5$251,515.1 =

−−

= $386,946.38.

Pro Forma Balance Sheet (Thousands of Dollars):

Casha $ 127.4 Accounts payable $ 250.0

Accounts receivable 450.0 Notes payableb 436.9

Inventory 750.0 Accruals 50.0

Prepaid interest 58.0

Answers and Solutions: 27 – 14

27-10 a. 1. Line of credit:

Commitment fee = (0.005)($2,000,000)(11/12) = $ 9,167

Interest = (0.11)(1/12)($2,000,000) = 18,333

Total $27,500

2. Trade discount:

a.

rate

Nominal

=

98

2

30

360

= 24.49 ≈ 24.5%.

3. 30-day commercial paper:

Interest = (0.095)($2,000,000)(1/12) = $15,833

Transaction fee = (0.005)($2,000,000) = 10,000

$25,833

4. 60-day commercial paper:

The 30-day commercial paper has the lowest cost.

b. The lowest cost of financing is not necessarily the best. The use of 30-day

commercial paper is the cheapest; however, sometimes the commercial paper market

is tight and funds are not available. This market also is impersonal. A banking

Answers and Solutions: 27 – 15

SOLUTION TO SPREADSHEET PROBLEMS

27-11 The detailed solution for the spreadsheet problem, Ch27 P11 Build a Model Solution.xls,

is available on the textbook’s Web site.

Mini Case: 27- 16

MINI CASE

Rich Jackson, a recent finance graduate, is planning to go into the wholesale building

supply business with his brother, Jim, who majored in building construction. The firm

would sell primarily to general contractors, and it would start operating next January.

Sales would be slow during the cold months, rise during the spring, and then fall off again

in the summer, when new construction in the area slows. Sales estimates for the first 6

months are as follows (in thousands of dollars):

Jan $100

Feb 200

Mar 300

Apr 300

May 200

Jun 100

The terms of sale are net 30, but because of special incentives, the brothers expect 30

percent of the customers (by dollar value) to pay on the 10th day following the sale, 50

percent to pay on the 40th day, and the remaining 20 percent to pay on the 70th day. No

bad debt losses are expected, because Jim, the building construction expert, knows which

contractors are having financial problems.

a. Discuss, in general, what it means for the brothers to set a credit and collections

policy.

Answer: When a firm sets its credit and collections policy it determines four things:

1. The credit period, which is the length of time buyers are given to pay for their

purchases

Mini Case: 27 – 17

b. Assume that, on average, the brothers expect annual sales of 18,000 items at an

average price of $100 per item. (use a 365-day year.)

1. What is the firm’s expected days sales outstanding (DSO)?

Answer: Days sales outstanding = DSO = 0.3(10) + 0.5(40) + 0.2(70) = 37 days, vs. 30-day

b. 2. What is its expected average daily sales (ADS)?

b. 3. What is its expected average accounts receivable (AR) level?

Answer: Accounts receivable (AR) = (DSO)(ADS) = 37($4,931) = $182,466. Thus, $182,466

b. 4. Assume that the firm’s profit margin is 25 percent. How much of the receivables

balance must be financed? What would the firm’s balance sheet figures for

accounts receivable, notes payable, and retained earnings be at the end of one

year if notes payable are used to finance the investment in receivables? Assume

that the cost of carrying receivables had been deducted when the 25 percent

profit margin was calculated.

Answer: Although the firm has $182,466 in receivables, the entire amount does not have to be

financed, since 25 percent of the sales price is profit. This means that 75 percent of

Mini Case: 27- 18

b. 5. If bank loans have a cost of 12 percent, what is the annual dollar cost of carrying

the receivables?

Answer: Cost of carrying receivables = 0.12($136,849) = $16,422. In addition, there is an

c. What are some factors that influence (1) a firm’s receivables level

and (2) the dollar cost of carrying receivables?

Answer: 1. As shown in question B.3. Above, receivables are a function of the average daily

sales and the days sales outstanding. Exogenous economic factors such as the

Mini Case: 27 – 19

d. Assuming that the monthly sales forecasts given previously are accurate, and

that customers pay exactly as was predicted, what would the receivables level be

at the end of each month? To reduce calculations, assume that 30 percent of the

firm’s customers pay in the month of sale, 50 percent pay in the month following

the sale, and the remaining 20 percent pay in the second month following the sale.

Note that this is a different assumption than was made earlier. Use the following

format to answer parts c and d:

E.O.M. Quarterly DSO =

Month Sales AR Sales ADS (AR)/(ADS)

Jan $100 $ 70

Feb 200 160

Mar 300 250 $600 $6.59 37.9

Apr 300

May 200

Jun 100

Mini Case: 27- 20

Answer: (Note: from this point on, the solutions are expressed in thousands of dollars. Also,

the table given below is developed in the solutions to parts D and E.)

Mini Case: 27 – 21

e. What is the firm’s forecasted average daily sales for the first 3 months? For the

entire half-year? The days sales outstanding is commonly used to measure

receivables performance. What DSO is expected at the end of March? At the

end of June? What does the DSO indicate about customers’ payments? Is DSO

a good management tool in this situation? If not, why not?

Answer: For the first quarter, sales totaled $100 + $200 + $300 = $600, so ads = $600/91 =

$6.59. Although the sales pattern is different, ads for the second quarter, and hence

for the full half-year, is also $6.59. Note that we can rearrange the formula for

receivables as follows:

Mini Case: 27- 22

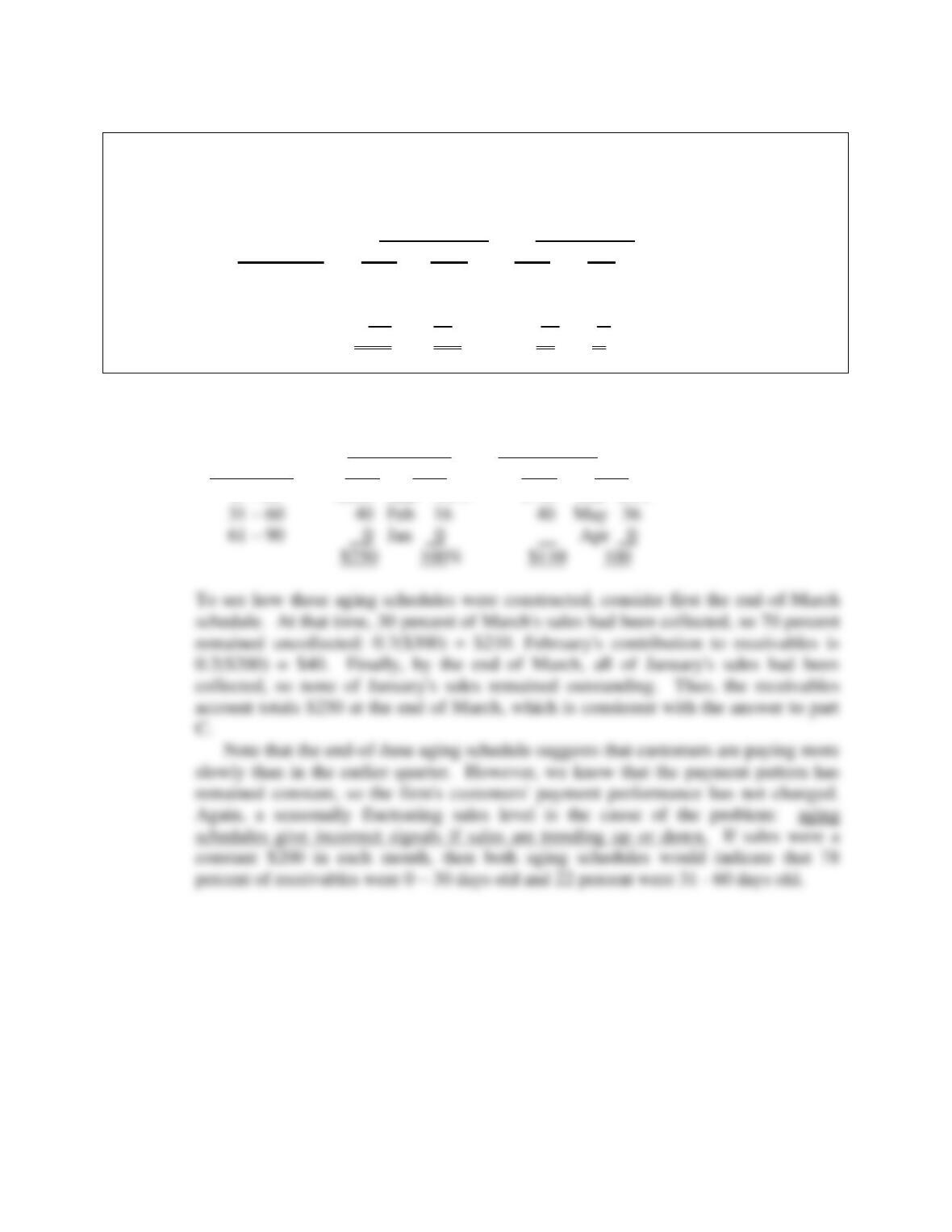

f. Construct aging schedules for the end of March and the end of June (use the

format given below). Do these schedules properly measure customers’ payment

patterns? If not, why not?

Age of account March June

(days) AR % AR %

0 – 30 $210 84%

31 – 60 40 16

61 – 90 0 0

$250 100%

Answer: Aging schedule:

Age of account March June

(days) AR % AR %

0 – 30 $210 Mar 84% $ 70 Jun 64%

Mini Case: 27 – 23

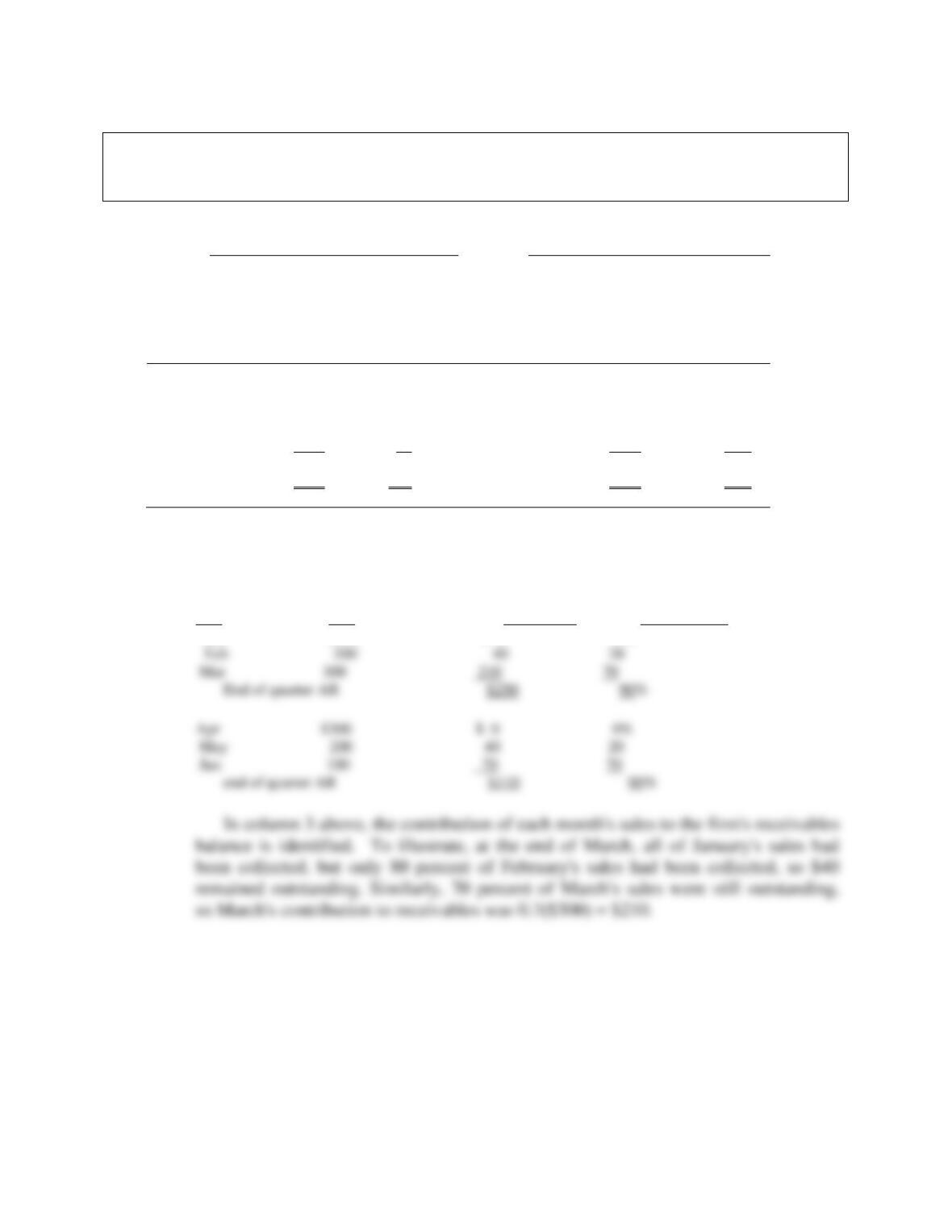

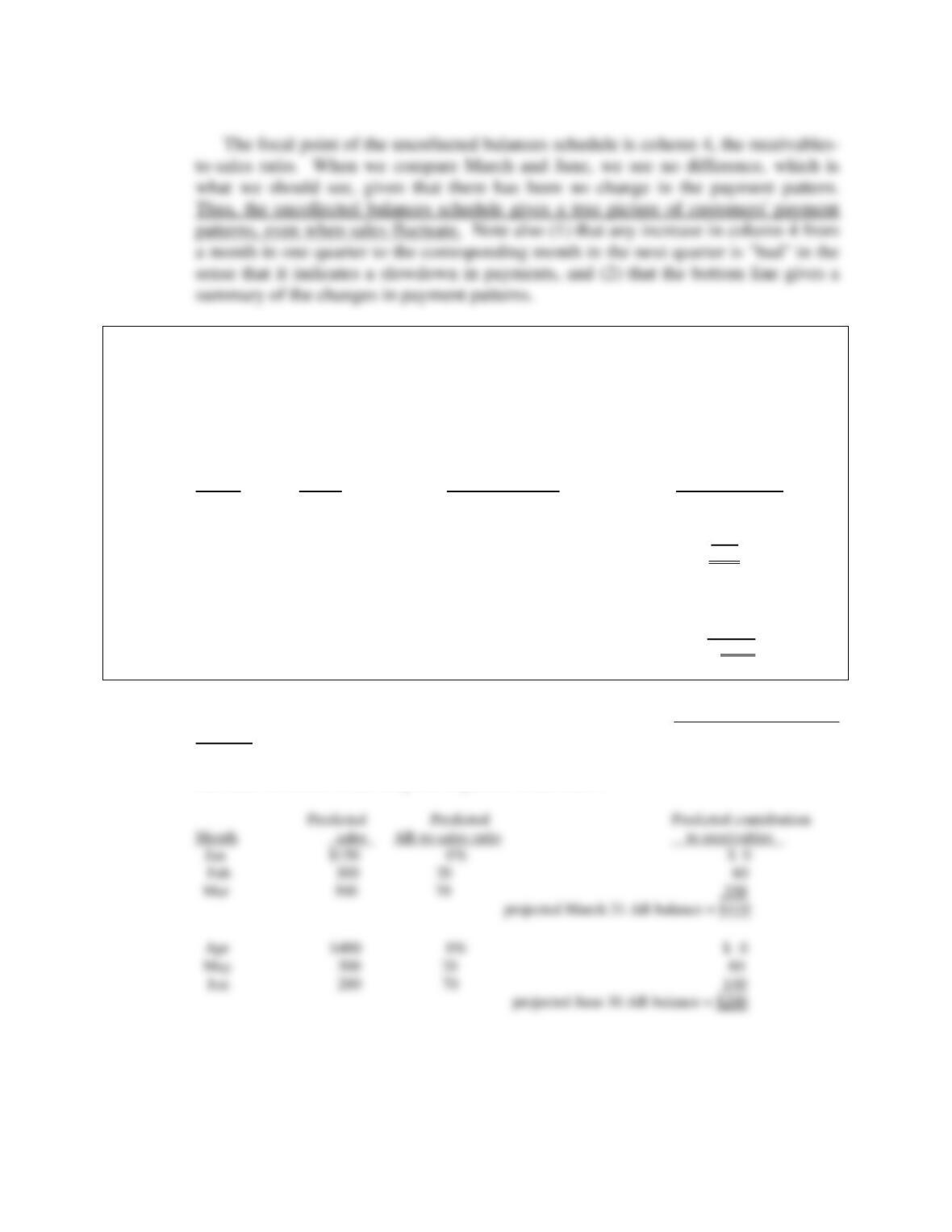

g. Construct the uncollected balances schedules for the end of March and the end

of June. Use the format given below. Do these schedules properly measure

customers’ payment patterns?

March

June

Month

Sales

Contribution

to AR

AR–to–

Sales Ratio

Month

Sales

Contribution

to A/R

AR–to–

Sales

Ratio

January

$100

$ 0

0%

April

February

200

40

20

May

March

300

210

70

June

Answer: Uncollected balances schedules:

Contribution to Ratio of month’s

Month Sales end-of-period AR AR to month’s sales

(1) (2) (3) (4)

Jan $100 $ 0 0%

Mini Case: 27- 24

h. Assume that it is now July of year 1, and the brothers are developing pro forma

financial statements for the following year. Further, assume that sales and

collections in the first half-year matched the predicted levels. Using the year 2

sales forecasts as shown next, what are next year’s pro forma receivables levels

for the end of March and for the end of June?

Predicted Predicted Predicted contribution

Month sales AR–to-sales ratio to receivables

Jan $150 0% $ 0

Feb 300 20 60

Mar 500 70 350

projected March 31 AR balance = $410

Apr $400

May 300

Jun 200

Projected June 30 AR balance =

Answer: The uncollected balances schedule can be used to forecast the pro forma receivables

balance. For forecasting, the historical receivables–to-sales ratios are generally

assumed to be good predictors of future payment patterns, and hence are applied to

the sales forecasts to develop the expected receivables:

Mini Case: 27 – 25

i. Assume now that it is several years later. The brothers are concerned about the

firm’s current credit terms, which are now net 30, which means that contractors

buying building products from the firm are not offered a discount, and they are

supposed to pay the full amount in 30 days. Gross sales are now running

$1,000,000 a year, and 80 percent (by dollar volume) of the firm‘s paying

customers generally pay the full amount on day 30, while the other 20 percent

pay, on average, on day 40. Two percent of the firm‘s gross sales end up as bad

debt losses.

The brothers are now considering a change in the firm’s credit policy. The

change would entail (1) changing the credit terms to 2/10, net 20, (2) employing

stricter credit standards before granting credit, and (3) enforcing collections

with greater vigor than in the past. Thus, cash customers and those paying

within 10 days would receive a 2 percent discount, but all others would have to

pay the full amount after only 20 days. The brothers believe that the discount

would both attract additional customers and encourage some existing customers

to purchase more from the firm—after all, the discount amounts to a price

reduction. Of course, these customers would take the discount and, hence,

would pay in only 10 days.

The net expected result is for sales to increase to $1,100,000; for 60 percent of

the paying customers to take the discount and pay on the 10th day; for 30

percent to pay the full amount on day 20; for 10 percent to pay late on day 30;

and for bad debt losses to fall from 2 percent to 1 percent of gross sales. The

firm’s operating cost ratio will remain unchanged at 75 percent, and its cost of

carrying receivables will remain unchanged at 12 percent.

To begin the analysis, describe the four variables that make up a firm’s

credit policy, and explain how each of them affects sales and collections. Then

use the information given in part H to answer parts I through N.

Answer: The four variables which make up a firm’s credit policy are (1) the discount offered,

including the amount and period; (2) the credit period; (3) the credit standards used

when determining who shall receive credit, and how much credit; and (4) the

collection policy.

Mini Case: 27- 26

j. Under the current credit policy, what is the firm’s days sales outstanding (DSO)?

What would the expected DSO be if the credit policy change were made?

Answer: Old (current) situation: DSO0 = 0.8(30) + 0.2(40) = 32 days. New situation: DSOn =

k. What is the dollar amount of the firm’s current bad debt losses? What losses

would be expected under the new policy?

Answer: Old (current) situation: BDLo = 0.02($1,000,000) = $20,000. New situation: BDLn

l. What would be the firm’s expected dollar cost of granting discounts under the

new policy?

Answer: Current situation: under the current, no discount policy, the cost of discounts is $0.

Mini Case: 27 – 27

m. What is the firm’s current dollar cost of carrying receivables? What would it be

after the proposed change?

Answer: Current situation: the firm’s average daily sales currently amount to $1,000,000/365

= $2,739.73. The DSO is 32 days, so accounts receivable amount to 32($2,739.73) =

Mini Case: 27- 28

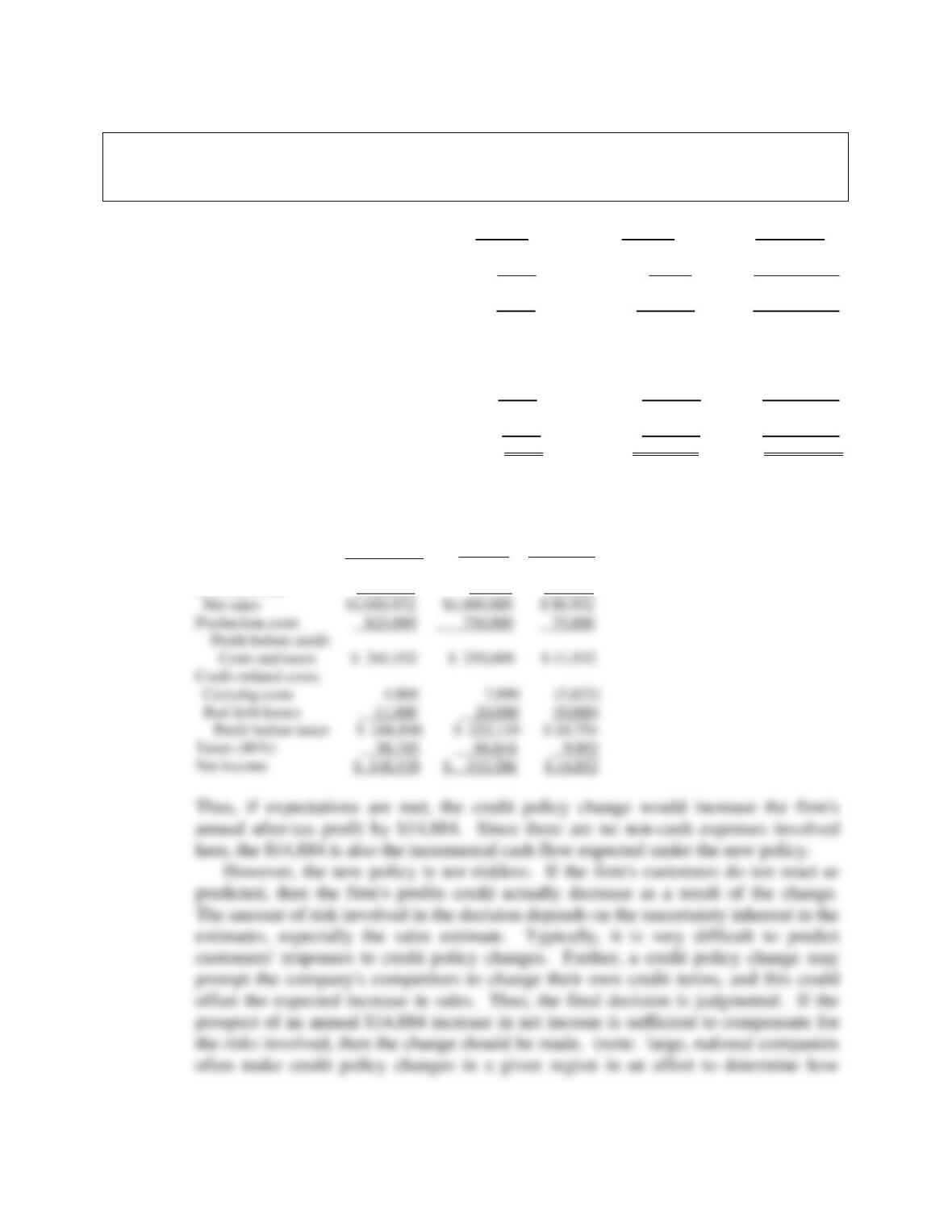

n. What is the incremental after-tax profit associated with the change in credit

terms? Should the company make the change? (assume a tax rate of 40

percent.)

New Old Difference

Gross sales $1,000,000

Less discounts 0

Net sales $1,000,000

Production costs 750,000

Profit before credit

Costs and taxes $ 250,000

Credit-related costs:

Carrying costs 7,890

Bad debt losses 20,000

Profit before taxes $ 222,110

Taxes (40%) 88,844

Net income $ 133,266

Answer: The income statements and differentials under the two credit policies are shown

below:

New Old Difference

Gross sales $1,100,000 $1,000,000 $100,000

Less discounts 13,068 0 13,068

Mini Case: 27 – 29

o. Suppose the firm makes the change, but its competitors react by making similar

changes to their own credit terms, with the net result being that gross sales

remain at the current $1,000,000 level. What would the impact be on the firm‘s

post-tax profitability?

Answer: If sales remain at $1,000,000 after the change is made, then the following situation

would exist:

Gross sales $1,000,000

Less discounts 11,880

Mini Case: 27- 30

p. The brothers need $100,000 and are considering a 1-year bank loan with a

quoted annual rate of 8%. The bank is offering the following alternatives: (1)

simple interest, (2) discount interest, (3) discount interest with a 10%

compensating balance, and (4) add-on interest on a 12-month installment loan.

What is the effective annual cost rate for each alternative? For the first three of

these assumptions, what is the effective rate if the loan is for 90 days, but

renewable? How large must the face value of the loan amount actually be in each

of the 4 alternatives to provide $100,000 in usable funds at the time the loan is

originated?

Answer: 1. With a simple interest loan, they gets the full use of the $100,000 for a year, and

then pay 0.08($100,000) = $8,000 in interest at the end of the term, along with the

$100,000 principal repayment. For a 1-year simple interest loan, the nominal rate,

8 percent, is also the effective annual rate.

Mini Case: 27 – 31

Note that a timeline can also be used to calculate the effective annual rate of the

1-year discount loan:

0 1

| |

100,000 -100,000

-8,000 (discount interest)

92,000

With a financial calculator, enter N = 1, PV = 92000, PMT = 0, and FV = -100000

to solve for I/YR = 8.6957% ≈ 8.7%.

If the loan were for 90 days:

i = ?

Mini Case: 27- 32

3. If the loan is a discount loan, and a compensating balance is also required, then

the effective rate is calculated as follows:

Amount borrowed =

1.008.01

000,100$

−−

= $121,951.22.

The face value (the amount of the loan required to get the desired level

of usable funds) of the loan is calculated as:

Face value =

CB–RATE NOMINAL1

REQUIRED FUNDS

−

=

10.008.01

000,100$

−−

= $121,951.22.

4. In an installment (add-on) loan, the interest is calculated and added on to the

required cash amount, and then this sum is the face amount of loan, and it is

amortized by equal payments over the stated life. Thus, the interest would be

$100,000 0.08 = $8,000, the face amount would be $108,000, and each monthly

payment would be $9,000: $108,000/12 = $9,000.

Enter in N = 12, PV = 100000, and PMT = -9000 in a financial calculator, we find

the monthly rate to be 1.2043%, which converts to an effective annual rate of

15.45 percent:

(1.012043)12 – 1.0 = 0.1545 = 15.45%

The face value (the amount of the loan required to get the desired level of usable

funds) of the loan is $100,000. Note that the borrower would only have full use