Answers and Solutions: 26 – 1

Chapter 26

Real Options

ANSWERS TO END-OF-CHAPTER QUESTIONS

26-1 a. Real options occur when managers can influence the size and risk of a project’s cash

flows by taking different actions during the project’s life. They are referred to as real

options because they deal with real as opposed to financial assets. They are also

called managerial options because they give opportunities to managers to respond to

changing market conditions. Sometimes they are called strategic options because

they often deal with strategic issues. Finally, they are also called embedded options

because they are a part of another project.

c. Decision trees are a form of scenario analysis in which different actions are taken in

different scenarios.

26-2 Postponing the project means that cash flows come later rather than sooner; however,

waiting may allow you to take advantage of changing conditions. It might make sense,

however, to proceed today if there are important advantages to being the first competitor

to enter a market.

Answers and Solutions: 26 – 2

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

26-1 a. 0 1 2 20

├─────┼─────┼────── • • • ────┤

-20 3 3 3

NPV = $1.074 million.

b. Wait 1 year:

Note though, that if the tax is imposed, the NPV of the project is negative and therefore

would not be undertaken. The value of this option of waiting one year is evaluated as

0.5($0) + (0.5)($ 5.920) = $2.96 million.

Since the NPV of waiting one year is greater than going ahead and proceeding with the

project today, it makes sense to wait.

Answers and Solutions: 26 – 3

26-2 a. 0 1 2 3 4

├─────┼─────┼─────┼─────┤

-8 4 4 4 4

NPV = $4.6795 million.

b. Wait 2 years:

10%

Answers and Solutions: 26 – 4

26-3 a. 0 1 2 20

├─────┼─────┼────── • • • ────┤

-300 40 40 40

NPV = –$19.0099 million. Don’t purchase.

b. Wait 1 year:

NPV @

0 1 2 3 4 21 Yr. 0

| | | | | • • • |

50% Prob. 0 –300 30 30 + 280 0 0 -$27.1468

| | | | | • • • |

50% Prob. 0 –300 50 50 50 50 45.3430

13%

r = 13%

Answers and Solutions: 26 – 5

26-4 a. 0 1 14 15

| | • • • | |

-6,200,000 600,000 600,000 600,000

c. If they proceed with the project today, the project’s expected NPV = (0.5 –

$2,113,481.31) + (0.5 $1,973,037.39) = −$70,221.96. So, Hart Enterprises would not

do it.

d. Since the project’s NPV with the tax is negative, if the tax were imposed the firm

would abandon the project. Thus, the decision tree looks like this:

12%

12%

Answers and Solutions: 26 – 6

e. NPV @

0 1 Yr. 0

50% Prob. | |

Taxes NPV = ? -1,500,000 $ 0.00

+300,000 = NPV @ t = 1

r = 12%

wouldn’t do

Answers and Solutions: 26 – 7

26-5

a.

b. 0 1 2 3 4

40% Prob. | | | | |

Good –20,000 25,000 25,000 25,000 25,000

-20,000 (r = 6%)

Bad | | | | |

60% Prob. –20,000 5,000 5,000 0 0

r = 10%

r = 10%

Answers and Solutions: 26 – 8

26-6 P = PV of all expected future cash flows if project is delayed. From Problem 14-1 we

know that PV @ Year 1 of Tax Imposed scenario is $15.45 and PV @ Year 1 of Tax Not

Imposed Scenario is $26.69. So the PV is:

P = [0.5(15.45)+ 0.5(26.690] / 1.13 = $18.646.

X = $20.

V = P[N(d1)] –

trRF

Xe−

[N(d2)]

Answers and Solutions: 26 – 9

26-7 P = PV of all expected future cash flows if project is delayed. From Problem 14-1 we

know that PV @ Year 2 of Low CF Scenario is $6.974 and PV @ Year 2 of High CF

Scenario is $13.313. So the PV is:

P = [0.1(6.974)+ 0.9(13.313] / 1.102 = $10.479.

X = $9.

d2 = 1.9010 – (.0111)0.5 (2)0.5 = 1.7520

From Excel function NORMSDIST, or approximated from the table in Appendix A:

N(d1) = 0.9713

N(d2) = 0.9601

26-8 P = PV as of time zero of all expected future cash flows if the project is repeated starting

in year 2. Note it includes both the good cash flows and the bad cash flows since as of

now, we don’t know which outcome will result, and P excludes the $20,000 investment

in the franchise.

0 1 2 3 4

40% Prob. | | | | |

Good 25,000 25,000

r = 10%

Answers and Solutions: 26 – 10

The time to expiration is the time you decide whether or not to extend the franchise, and

is at the end of year 2.

Although the problem stated to assume the variance of the project’s rate of return was

0.2025, we’ll also calculate it using the direct method. First calculate the rates of return

using the decision tree. To do this, calculate the present values of the two branches as of

the exercise date, year 2, and the rates of return assuming the initial value of the

investment was P = $18,646.

0 1 2 3 4

The expected value of these two returns is 52.54(0.40) – 31.78(0.60) = 1.95% [Note: this

isn’t 10% as you might hope! The 2-year returns are 43,388/18,646 – 1 = 132.69% in

the good state and 8,678/18,646 – 1 = -53.46% in the bad state. The expected value of

these is 132.69% (0.40) – 53.46% (0.60) = 21.0%, which is exactly 10% compounded

twice: 0.21 = (1.10)2 – 1.]

Answers and Solutions: 26 – 11

To calculate the variance of the project’s returns using the indirect method, first calculate

the standard deviation of the value at year 2. The value is either 43,388 (probability

40%) or 8,678 (probability 60%).

P = $18,646

X = $20,000

t = 2.

rRF = 0.06.

σ2 = 0.2025

d1 = ln[18.646/20] + [0.06 + .5(0.2025)](2) = 0.3966

(0.2025)0.5 (2)0.5

Answers and Solutions: 26 – 12

SOLUTION TO SPREADSHEET PROBLEMS

Mini Case: 26 – 13

MINI CASE

Assume that you have just been hired as a financial analyst by Tropical Sweets Inc., a mid–

sized California company that specializes in creating exotic candies from tropical fruits

such as mangoes, papayas, and dates. The firm’s CEO, George Yamaguchi, recently

returned from an industry corporate executive conference in San Francisco, and one of the

sessions he attended was on real options. Since no one at Tropical Sweets is familiar with

the basics of real options, Yamaguchi has asked you to prepare a brief report that the

firm’s executives could use to gain at least a cursory understanding of the topics.

To begin, you gathered some outside materials the subject and used these materials to

draft a list of pertinent questions that need to be answered. In fact, one possible approach

to the paper is to use a question-and-answer format. Now that the questions have been

drafted, you have to develop the answers.

a. What are some types of real options?

Answer: 1. Investment timing options

2. Growth options

a. Expansion of existing product line

b. What are five possible procedures for analyzing a real option?

Answer: 1. DCF analysis of expected cash flows, ignoring option.

Mini Case: 26 – 14

c. Tropical Sweets is considering a project that will cost $70 million and will

generate expected cash flows of $30 per year for three years. The cost of capital

for this type of project is 10 percent and the risk-free rate is 6 percent. After

discussions with the marketing department, you learn that there is a 30 percent

chance of high demand, with future cash flows of $45 million per year. There is

a 40 percent chance of average demand, with cash flows of $30 million per year.

If demand is low (a 30 percent chance), cash flows will be only $15 million per

year. What is the expected NPV?

Answer: Initial Cost = $70 Million

Expected Cash Flows = $30 Million Per Year For Three Years

Cost Of Capital = 10%

PV Of Expected CFs = $74.61 Million

Expected NPV = $74.61 – $70

= $4.61 Million

Mini Case: 26 – 15

d. Now suppose this project has an investment timing option, since it can be

delayed for a year. The cost will still be $70 million at the end of the year, and

the cash flows for the scenarios will still last three years. However, Tropical

Sweets will know the level of demand, and will implement the project only if it

adds value to the company. Perform a qualitative assessment of the investment

timing option’s value.

Answer: If we immediately proceed with the project, its expected NPV is $4.61 million.

However, the project is very risky. If demand is high, NPV will be $41.91

Mini Case: 26 – 16

e. Use decision tree analysis to calculate the NPV of the project with the investment

timing option.

Answer: The project will be implemented only if demand is average or high.

Here is the time line:

0 1 2 3 4

f. Use a financial option pricing model to estimate the value of the investment

timing option.

Answer: The option to wait resembles a financial call option— we get to “buy” the project for

$70 million in one year if value of project in one year is greater than $70 million.

Mini Case: 26 – 17

Step 1: Find the value of all cash flows beyond the exercise date discounted back to

the exercise date. Here is the time line. The exercise date is year 1, so we discount

all future cash flows back to year 1.

0 1 2 3 4

High $45 $45 $45

Average $30 $30 $30

Low $15 $15 $15

Mini Case: 26 – 18

Following is an explanation of each approach.

Subjective estimate:

The typical stock has σ2 of about 12%. Most projects will be somewhat riskier than

the firm, since the risk of the firm reflects the diversification that comes from having

many projects. Subjectively scale the variance of the company’s stock return up or

down to reflect the risk of the project. The company in our example has a stock with

a variance of 10%, so we might expect the project to have a variance in the range of

12% to 19%.

Expected Return = 0.3(0.65) + 0.4(0.10) + 0.3(-0.45)

= 10%.

2 = 0.3(0.65-0.10)2 + 0.4(0.10-0.10)2 + 0.3(-0.45-0.10)2

= 0.182 = 18.2%.

Mini Case: 26 – 19

The indirect approach:

Given a current stock price and an anticipated range of possible stock prices at some

We previously calculated the value of the project at the time the option expires, and

we can use this to calculate the expected value and the standard deviation.

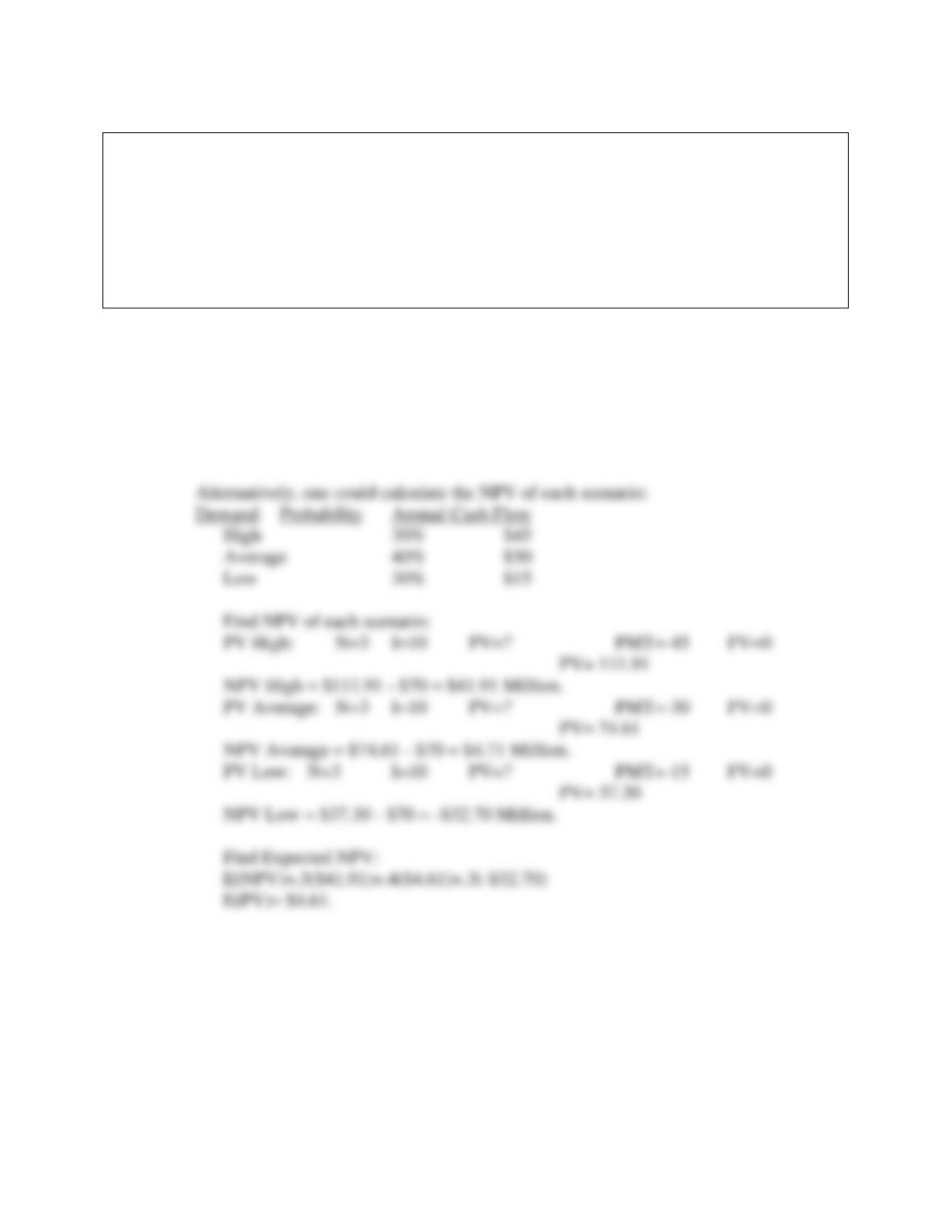

Value At Expiration

Year 1

High $111.91

Average $74.61

Low $37.30

Mini Case: 26 – 20

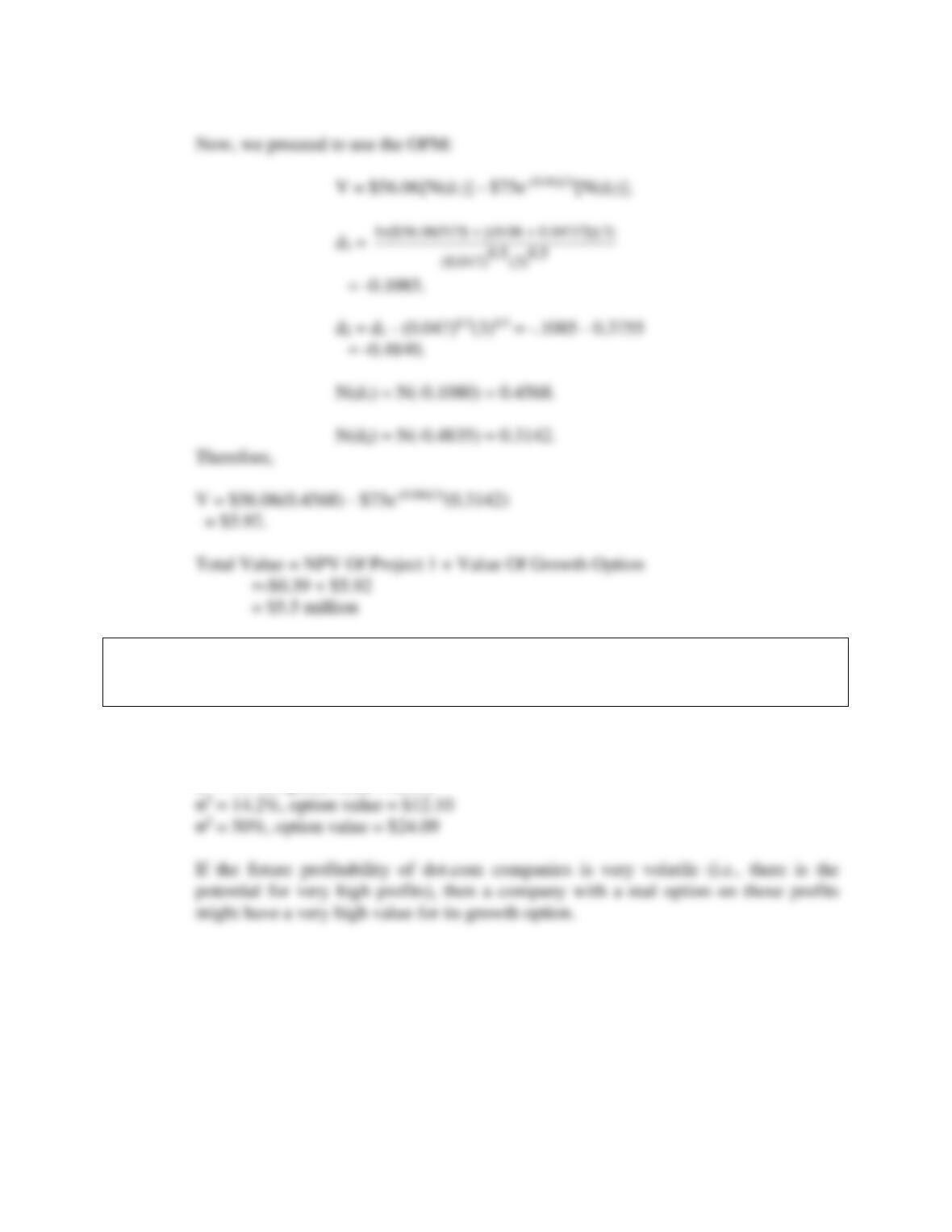

Now, we proceed to use the OPM:

= $10.98.

g. Now suppose the cost of the project is $75 million and the project cannot be

delayed. But if Tropical Sweets implements the project, then Tropical Sweets

will have a growth option. It will have the opportunity to replicate the original

project at the end of its life. What is the total expected NPV of the two projects

if both are implemented?

Answer: Suppose the cost of the project is $75 million instead of $70 million, and there is no

option to wait.

NPV = PV of future cash flows – cost

Mini Case: 26 – 21

h. Tropical Sweets will replicate the original project only if demand is high. Using

decision tree analysis, estimate the value of the project with the growth option.

Answer: The future cash flows of the optimal decisions are shown below. The cash flow in

year 3 for the high demand scenario is the cash flow from the original project and the

cost of the replication project.

Mini Case: 26 – 22

i. Use a financial option model to estimate the value of the growth option.

Answer: X = Strike Price = Cost Of Implement Project = $75 million.

RRF = Risk-Free Rate = 6%.

T = Time To Maturity = 3 years.

P = Current Price Of Stock = Current Value Of The Project’s Future Cash Flows.

σ2 = Variance Of Stock Return = Variance Of Project’s Rate Of Return.

Direct approach for estimating σ2:

From our previous analysis, we know the current value of the project and the value

for each scenario at the time the option expires (year 3). Here is the time line:

Mini Case: 26 – 24

The indirect approach:

First, find the coefficient of variation for the value of the project at the time the option

expires (year 3).

We previously calculated the value of the project at the time the option expires, and

we can use this to calculate the expected value and the standard deviation.

Mini Case: 26 – 25

j. What happens to the value of the growth option if the variance of the project’s

return is 14.2 percent? What if it is 50 percent? How might this explain the

high valuations of many dot.com companies?

Answer: If risk, defined by σ2, goes up, then value of growth option goes up (see the file Ch26

mini case.xls for calculations):

σ2 = 4.7%, option value = $5.92