CHAPTER 26

Scarcity and Choice

Neoclassical View

LEARNING OBJECTIVES

Explain the concept of scarcity and how people make choices according to neoclassical

analysis.

Describe how the production possibilities curve captures production choices in a society.

OUTLINE OF CHAPTER

I. Neoclassical View of Scarcity and Choice

Choice, Scarcity and the Production Possibilities Curve

KEY TERMS

choice

which goods he or she wants to consu

me

institutions

sets of customs, laws, and norms that influence, enable, or constrain human behavior

and time

individuals

ANSWERS TO END OF CHAPTER REVIEW QUESTIONS

Explain the concept of scarcity and how people make choices according to neoclassical

analysis.

1. List the underlying assumptions that neoclassical economist make about people.

(1) Human beings make rational choices by weighing the costs and benefits of a decision.

2. Explain the foundation of neoclassical analysis. What are two key assumptions made

about people and how they make decisions?

The foundation of neoclassical analysis is the isolated individual.

3. What creates scarcity, according to neoclassical analysis? Explain the difference between

what people need and what people want and desire and how this difference creates scarcity.

Scarcity is created by the fact that there is never enough production to satisfy the wants

Describe how the production possibilities curve captures production choices in a society.

4. Explain what the production possibilities curve (PPC) demonstrates. What assumptions

are made when creating a PPC?

5. What does it mean if a society is producing on the frontier or directly on the PPC?

6. If a society is producing on the frontier, what happens if society decides it wants more of

one of the goods being produced?

In order to produce more of one good, society must produce less of the other good.

7. Is it always impossible to produce more of one good without giving up some of the other

good? Why or why not?

Society could produce more of one good without giving up some of the other good if there

Describe what progressive economists see as the primary shortcomings of the neoclassical

scarcity perspective.

8. What is the progressive criticism of the analysis of the economy, starting with isolated

individuals? What is the critique of the assumptions about individuals and how

individuals make decisions? What is the progressive alternative?

The assumption of isolated individuals does not describe life in a highly complex society

9. Why is the context in which individuals make decisions important? How do social and

cultural norms play into how individuals make decisions? Give an example of how a

social norm may influence an economic decision.

Few decisions are made in isolation. People often make decisions based on reasons

10. What is the progressive criticism of the neoclassical notion of scarcity? Give a specific

example. What is the progressive alternative?

Under capitalist economic institutions in peacetime, there is no problem of scarcity. The

11. A progressive economist would claim we should not assume a market economy is always

producing on the PPC. Explain. What does this mean about the decision to produce

additional amounts of one good? Both goods?

Capitalist economies often produce at less than full employment of all resources, i.e. the

12. Progressive economists claim the types of choices different people make are very

different from the simple choices presented in the overview of neoclassical choice.

Explain.

Progressive economists reject the neoclassical focus on scarcity and isolated individuals,

APPENDIX 26.1

More on the Production Possibility Curve

LEARNING OBJECTIVES FOR APPENDIX 26.1

List the assumptions behind the PPC

Use the PPC to illustrate scarcity, choice, constant opportunity costs, and the law of

OUTLINE OF APPENDIX

I. The Simplest, Linear PPC for Individuals

II. Linear Opportunity Costs

KEY TERMS

attainable region

production points on the frontier or inside the frontier of the PPC.

comparative Advantage

producing a good or service at the lowest opportunity cost

constant marginal opportunity costs

eventually rise.

the value of what is given up when a choice is made to do something else

production possibilities curve (PPC)

a curve showing the production combinations available to an economy given finite inputs and

techn

ology

resources/inputs

the assets needed in production and development of an economy, including land, labor, capital,

and time

technology

the existing level of knowledge, techniques, and types of tools available for the production of

goods and services

to get one additional thing, something else must be given up

ANSWERS TO APPENDIX 26.1 REVIEW QUESTIONS

List the assumptions behind the PPC

1. What do we assume about inputs, institutions, and technology in building the PPC?

2. What does the PPC represent?

The PPC shows the production combinations available to an economy given finite inputs

and technology.

3. What is an opportunity cost? Give an example of an opportunity cost involved in a

decision you made today.

4. What does marginal cost mean? Create an example of a marginal cost.

The additional cost of producing an additional item.

5.

Use the PPC to illustrate scarcity, choice, constant opportunity costs, and the law of

increasing marginal opportunity cost.

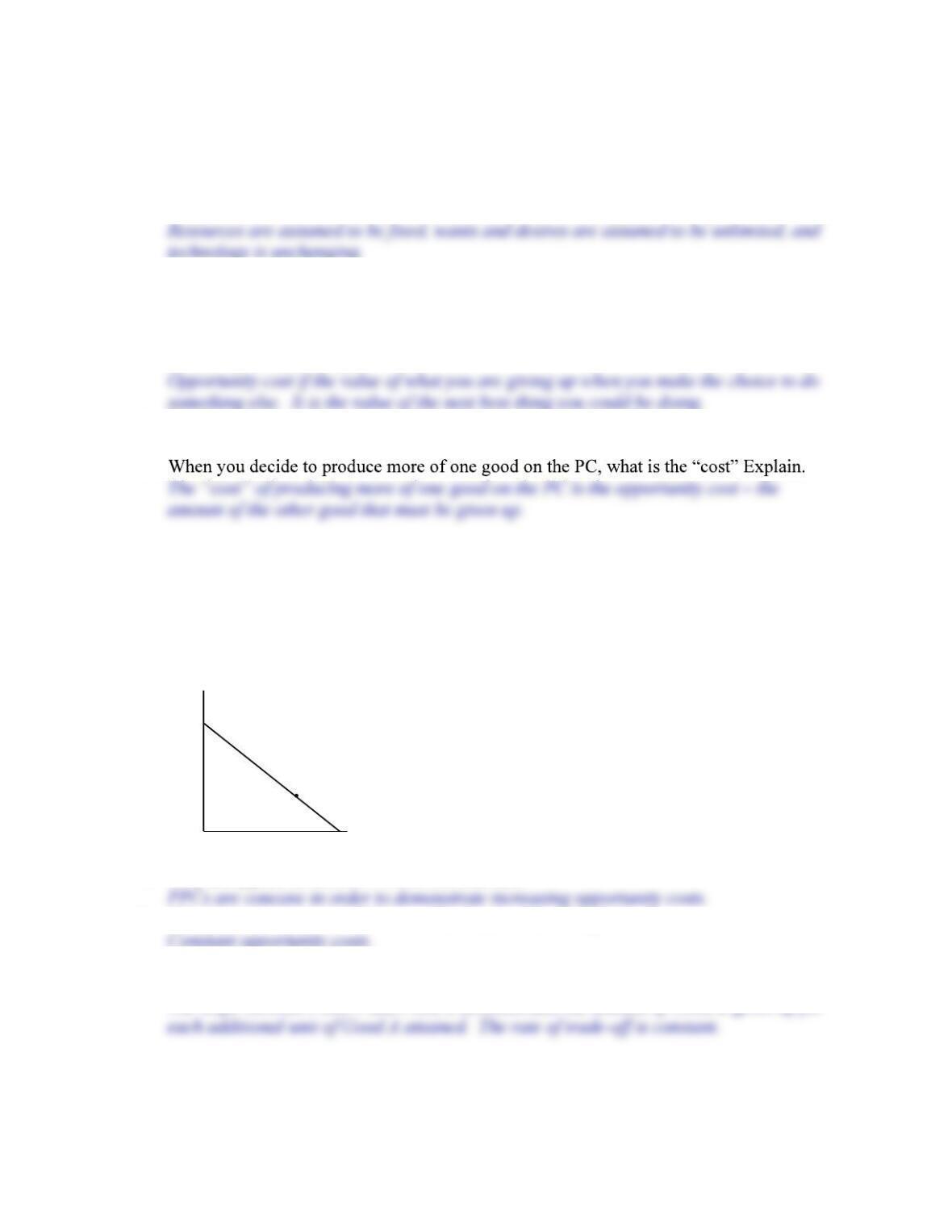

6. Draw a PPC diagram and illustrate the attainable region and unattainable region. Label a

combination of goods representing efficient production.

7. Why are typical textbook PPCs bowed outward?

8. What does it mean when PPCs are illustrated with a straight line?

9. Draw a linear PPC. Label two points on this diagram and explain how these points are

consistent with the idea of constant marginal opportunity costs.

The slope between Point 1 and Point 2 demonstrates the amount of Good B given up for

Unattainable

region

Attainable

region

Good A

Good B

Efficient combination of

Good A and Good B

10. Draw a concave PPC. Label two points on this diagram and how these points are

consistent with the law of increasing opportunity costs.

The amount of Good B that must be given up for each additional unit of Good A

11. Draw a linear PPC like that illustrating the work of Student Painters. On the vertical axis,

label large houses, and on the horizontal axis, put small houses. Assume that the

company begins using a special kind of scaffolding for painting big houses. However,

setting it up tak

PPC be affected by this new resource?

The PPC will show an increase in the maximum possible number of large houses that can

12. In the 1980s, rates of growth in Japan were higher than in the United States. One

argument given for the stronger growth in Japan was higher level s of investment. Draw

a PPC for both the United States and Japan. On the axes, label the goods as investment

goods and consumption goods. Use these two diagrams to explain why Japan

experienced faster growth than did the United States.

If the U.S. produced at Point 1, it would produce relatively more consumption goods and

Explain why and how changes in technology, resources, and institutions influence the PPC.

13. What would cause a parallel shift in a PPC? What would cause a change in its slope?

A parallel shift in a PPC reflects an equal increase in resources used in the production of

14. Give an example of how a change in technology might have an effect on the production

of one good and not the other, and illustrate this situation with a PPC. What changed in

the graph?

The change in the slope reflects a change in technology that improves the production

15. What kind of institutional changes could cause an increase in production even though no

other inputs increased and no technology changed?

16. Assume a hurricane devastated an island economy that produced only coconuts and

There would be an inward shift of the PPC.