Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 280

Chapter 25

ANSWERS TO QUESTIONS

1. From 2008 to 2017, auto loan rates in the United States declined from around 8% to near

historic lows of around 4.5%. At the same time, auto sales increased to near historic high

levels by 2017. How, if at all, does this relate to the monetary transmission mechanism?

Assuming that monetary policy was relatively accommodative during that period of time that

2. “Considering that consumption accounts for nearly two-thirds of total GDP, this means that the

interest rate, wealth, and household liquidity channels are the most important monetary policy

channels in the U.S.” Is this statement true, false, or uncertain? Explain your answer.

Uncertain. Although consumption is the largest part of overall U.S. GDP, and there is no doubt

that these channels can be important to monetary policy effectiveness, some may disagree

with this statement. For instance, even though investment is closer to 15% of U.S. GDP,

3. How can the interest rate channel still function when short-term nominal interest rates are at

the zero lower bound?

If the central bank commits to a higher inflation policy while maintaining low nominal

interest rates, this will raise inflation expectations and therefore lower real interest rates, even

4. Lars Svensson, a former Princeton professor and deputy governor of the Swedish central

bank, proclaimed that when an economy is at risk of falling into deflation, central bankers

should be “responsibly irresponsible” with monetary expansion policies. What does this

mean, and how does it relate to the monetary transmission mechanism?

Part of the problem with deflation is that lower (negative) inflation raises the real interest

rate, which raises the cost of capital and lowers investment and consumption through the

5. Describe an advantage and a disadvantage of the fact that monetary policy has so many

different channels through which it can operate.

An advantage to monetary policy having so many channels through which it can impact the

economy is that if policy is rendered ineffective through any one particular channel, it

6. “If countries fix their exchange rate, the exchange rate channel of monetary policy does not

exist.” Is this statement true, false, or uncertain? Explain your answer.

True. When countries fix their exchange rate, they must use monetary policy to affect the

7. During the 2007–2009 recession, the value of common stocks in real terms fell by more than

50%. How might this decline in the stock market have affected aggregate demand and thus

contributed to the severity of the recession? Be specific about the mechanisms through which

the stock market decline affected the economy.

There are four main mechanisms through which the decline in stock prices could have

reduced aggregate demand and contributed to the severity of the recession. First, the decline

8. “The costs of financing investment are related only to interest rates; therefore, the only way

that monetary policy can affect investment spending is through its effects on interest rates.” Is

this statement true, false, or uncertain? Explain your answer.

9. From early 2009 to fall 2017, the S&P 500 stock index increased by a cumulative 260%, or

approximately 30% per year. Over the same period, one index of consumer confidence

increased from 56 to just below 100 (or a cumulative increase of about 80%). Explain how

this relates to the monetary transmission mechanism.

Assuming that monetary policy was relatively accommodative during that period of time, this

10. From mid-2008 to early 2009, the Dow Jones Industrial Average declined by more than

50%, while real interest rates were low or falling. What does this scenario suggest should

have happened to investment?

The lower real interest rates would stimulate investment spending because the cost of

11. Nobel Prize winner Franco Modigliani found that the most important transmission

mechanisms of monetary policy involve consumer expenditure. Describe how at least two of

these mechanisms work.

There are three mechanisms involving consumer expenditure. First, an expansionary

monetary policy lowers interest rates and reduces the cost of financing purchases of

12. In the late 1990s, the stock market was rising rapidly, the economy was growing, and the

Federal Reserve kept interest rates relatively low. Comment on how this policy stance would

affect the economy as it relates to the Tobin q transmission mechanisms.

This situation is consistent with Tobin’s q and the wealth effects of expansionary monetary

13. During and after the global financial crisis, the Fed reduced the fed funds rate to nearly

zero. At the same time, the stock market fell dramatically and housing market values declined

sharply. Comment on the effectiveness of monetary policy during this period with regard to

the wealth channel.

The wealth channel suggests that this type of monetary policy would raise stock prices and

14. From August 2014 to August 2017, the Fed continued to reiterate that monetary policy was

‘accommodative’. And during this time, excess reserves by banks decreased from around

$2.67 trillion to around $2 trillion, a decline of about 25%. What does this say about the

bank lending channel?

With accommodative monetary policy and plenty of reserves in the banking system, the

15. Why does the credit view imply that monetary policy has a greater effect on small businesses

than on large firms?

16. Why might the bank lending channel be less effective today than it once was?

There are a couple reasons why this might be true. First, bank regulations in the United States

have eased, making it easier for banks to raise funds through various sources that were

17. If adverse selection and moral hazard increase, how does this affect the ability of monetary

policy to address economic downturns?

18. How does the Great Depression demonstrate the unanticipated price level channel?

19. How are the wealth effect and the household liquidity effect similar? How are they different?

The two channels are similar in that increases in real interest rates lead to lower asset prices,

which lead to lower spending on consumption and housing. The difference is in how changes

20. Following the global financial crisis, mortgage rates reached record-low levels in 2011.

a. What effect should this have had on the economy, according to the household liquidity

effect channel?

Lower mortgage rates should lead to higher housing prices and raise the value of housing

b. During the same time, most banks raised their credit standards significantly, making it

much more difficult to qualify for home loans and to refinance existing loans. How does

this information alter your answer to part (a)?

21. “If the fed funds rate is at zero, the Fed can no longer implement effective accommodative

policy.” Is this statement true, false, or uncertain? Explain.

False. Even though conventional monetary policy tools may be ineffective, the Fed can

22. In December 2015, the Fed raised the fed funds rate for the first time in nearly a decade, and

gradually increased interest rates over a prolonged period of time after that. However, the

Fed continued to reiterate in its policy statements during this time that “the stance of

monetary policy remains accommodative.” Explain this seeming contradiction.

Even though the Fed was raising its conventional policy interest rate, the fact that inflation

was higher than the fed funds rate indicates that real policy rates were still negative, and

23. In general, if stock prices are rising, consumption growth is strong, house price appreciation

is high, and unemployment is low, would you classify monetary policy as too tight, too loose,

or just right?

24. How does the experience of Japan during the “two lost decades” lend support to the four

lessons for monetary policy outlined in this chapter?

The experience of Japan directly supports the four lessons of monetary policy discussed in

the chapter. First, short-term interest rates in Japan were near zero; however, due to deflation,

real interest rates remained elevated, suggesting a contractionary monetary policy stance.

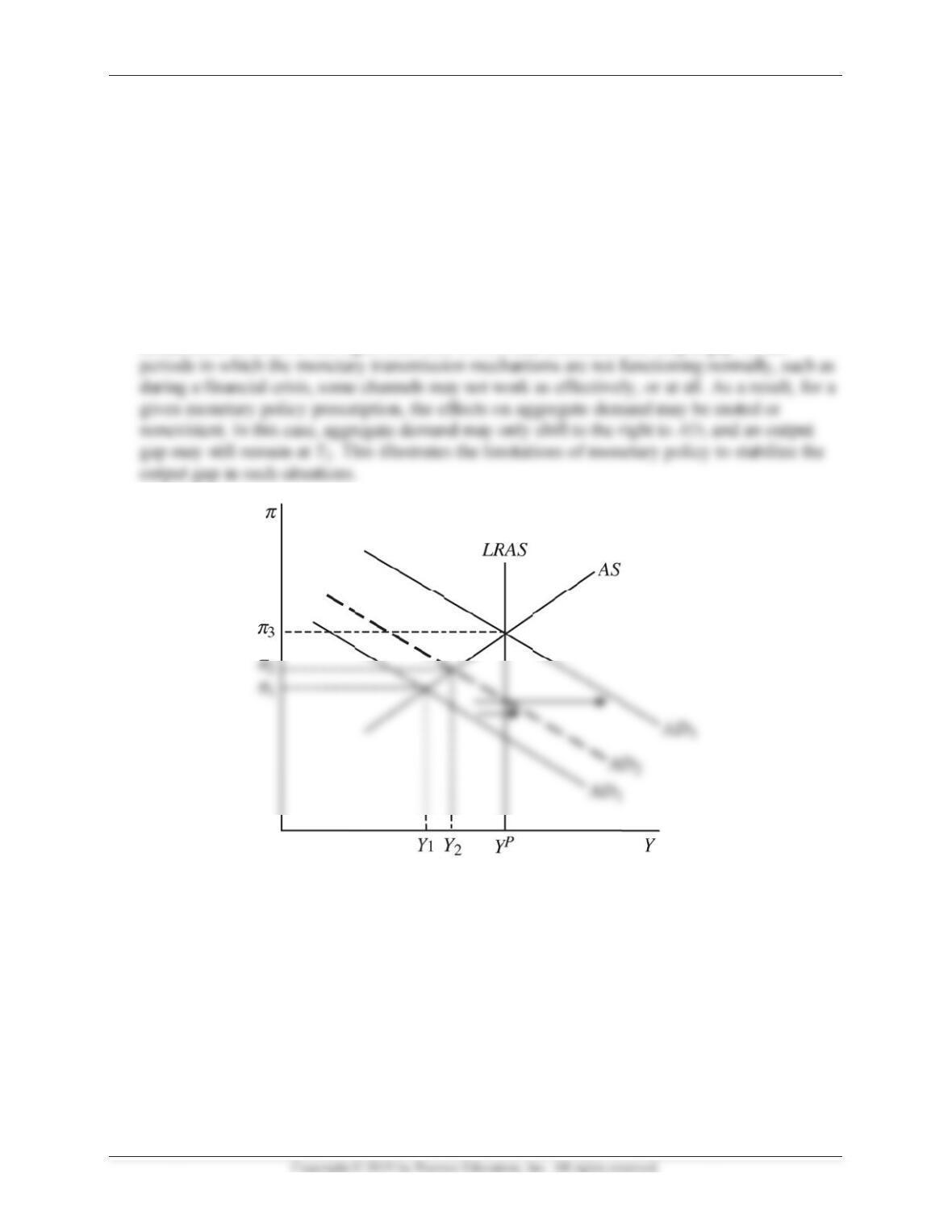

Mishkin •

ANSW

E

25.

Supp

an e

ff

dem

o

f

unc

t

deep

Whe

n

polic

y

dem

a

I

nstructor’s Ma

n

E

RS TO AP

P

o

se the eco

n

ff

ort to stabi

l

o

nstrate the

e

ioning nor

m

downturn o

r

n

the trans

m

y

makers ca

n

a

nd curve sh

n

ual for The Ec

o

P

LIED PR

O

n

omy is in r

e

l

ize the eco

n

e

ffects of a

m

m

ally and wh

r

when sign

if

m

ission mech

n

ease mone

t

i

fts to the ri

g

o

nomics of Mon

e

O

BLEMS

e

cession an

d

n

omy. Use a

n

m

onetary ea

s

en the trans

m

if

icant finan

c

anisms are

f

t

ary policy

w

g

ht from A

D

e

y, Banking, an

d

d

the moneta

r

n

aggregate

s

ing when t

h

m

ission me

c

c

ial friction

s

f

unctioning

n

w

ith reasona

b

D

1

to AD

3

an

d

d

Financial Mar

k

r

y policyma

k

supply and

d

h

e transmiss

c

hanisms ar

e

s

are presen

n

ormally (a

n

a

ble precisio

n

d

eliminates

k

ets, Twelfth E

d

k

ers lower i

n

d

emand dia

g

ion mechan

i

e

weak, suc

h

t.

n

d predictab

l

n

, so that th

e

the output

g

d

ition

n

terest rate

s

g

ram to

i

sms are

h

as during

a

l

y),

e

aggregate

g

ap. Under

286

s

in

a

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 287

ANSWERS TO DATA ANALYSIS PROBLEMS

1. A “rate cycle” is a period of monetary policy during which the federal funds rate moves from

its low point toward its high point, or vice versa, in response to business cycle conditions. Go

to the St. Louis Federal Reserve FRED database and find data on the federal funds rate

(FEDFUNDS), real business fixed investment (PNFIC96), real residential investment

(PRFIC96), and consumer durable expenditures (PCDGCC96). Use the frequency setting to

convert the federal funds rate data to “quarterly,” and download the data.

a. When did the last rate cycle begin and end? (Note: If a rate cycle is currently in progress,

use the current period as the end.) Is this rate cycle a contractionary or an expansionary

rate cycle?

The last rate cycle, as of July 2017, was the period from 2015:Q4 to 2017:Q1 (the most

b. Calculate the percentage change in business fixed investment, residential (housing)

investment, and consumer durable expenditures over this rate cycle.

c. Based on your answers to parts (a) and (b), how effective was the traditional interest rate

channel of monetary policy over this rate cycle?

Based on the contractionary nature of the rate cycle, and the modest increases in all three

components of the traditional interest rate channel, this transmission mechanism was not

2. As defined in Exercise 1, a “rate cycle” is a period of monetary policy during which the

federal funds rate moves from its low point toward its high point, or vice versa, in response

to business cycle conditions. Go to the St. Louis Federal Reserve FRED database and find

data on the federal funds rate (FEDFUNDS), bank reserves (TOTRESNS), bank deposits

(TCDSL), commercial and industrial loans (BUSLOANS), real estate loans (REALLN), real

business fixed investment (PNFIC96), and real residential investment (PRFIC96). Use the

frequency setting to convert the federal funds rate, bank reserves, bank deposits, commercial

and industrial loans, and real estate loans data to “quarterly,” and download the data.

a. When did the last rate cycle begin and end? (Note: if a rate cycle is currently in progress,

use the current period as the end.) Is this rate cycle a contractionary or an expansionary

rate cycle?

0.16% to 0.70%, a contractionary policy.

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 288

b. Calculate the percentage change in bank deposits, bank lending, real business fixed

investment, and real residential (housing) investment over this rate cycle.

Over this period, bank reserves decreased by 12.9%, bank deposits increased by 13.8%.

c. Based on your answers to parts (a) and (b), how effective was the bank lending channel

of monetary policy over this rate cycle?

The results are somewhat mixed with the data. Based on the contractionary nature of the

rate cycle, we would expect all of these variables to decrease when the policy rate

increases, according to the bank lending transmission mechanism. However, with the