Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Answers and Solutions: 25 - 1

Chapter 25

Portfolio Theory and Asset Pricing Models

ANSWERS TO END-OF-CHAPTER QUESTIONS

25-1 a. A portfolio is made up of a group of individual assets held in combination. An asset

that would be relatively risky if held in isolation may have little, or even no risk if

held in a well-diversified portfolio.

b. An indifference curve is the risk/return trade-off function for a particular investor and

reflects that investor's attitude toward risk. The indifference curve specifies an

investor's required rate of return for a given level of risk. The greater the slope of the

indifference curve, the greater is the investor's risk aversion.

The optimal portfolio for an investor is the point at which the efficient set of

Answers and Solutions: 25 - 2

c. The Capital Asset Pricing Model (CAPM) is a general equilibrium market model

developed to analyze the relationship between risk and required rates of return on

assets when they are held in well-diversified portfolios. The SML is part of the

CAPM.

d. The characteristic line for a particular stock is obtained by regressing the historical

returns on that stock against the historical returns on the general stock market. The

slope of the characteristic line is the stock's beta, which measures the amount by

which the stock's expected return increases for a given increase in the expected return

on the market.

25-2 Security A is less risky if held in a diversified portfolio because of its lower beta and

negative correlation with other stocks. In a single-asset portfolio, Security A would be

more risky because σA > σB and CVA > CVB.

Answers and Solutions: 25 - 3

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

25-1 bi = iM (i / M) = 0.70(0.40/0.20) = 1.4.

25-3 r

^p = wAr

^A + (1 − wA) r

^B

= 0.30(12%) + 0.70(18%) = 16.20%

25-4 a.

.)rr(rb)rr(rr

M

iiM

RFMRFiRFMRFi

−+=−+=

b. CML:

.

rr

rr p

M

RF

M

RF

p

−

+=

SML:

.r

rr

rr iiM

M

RFM

RFi

−

+=

With some arranging, the similarities between the CML and SML are obvious. When

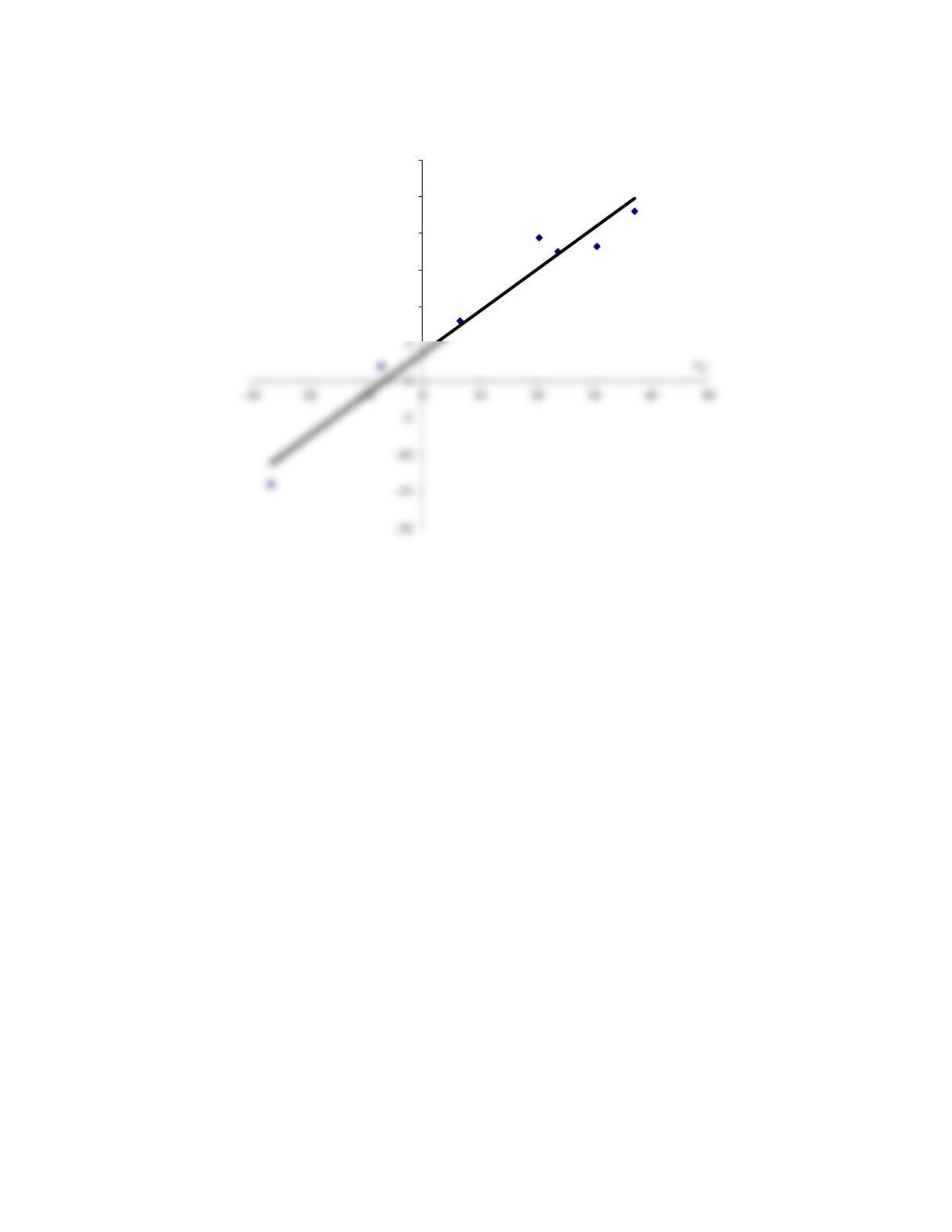

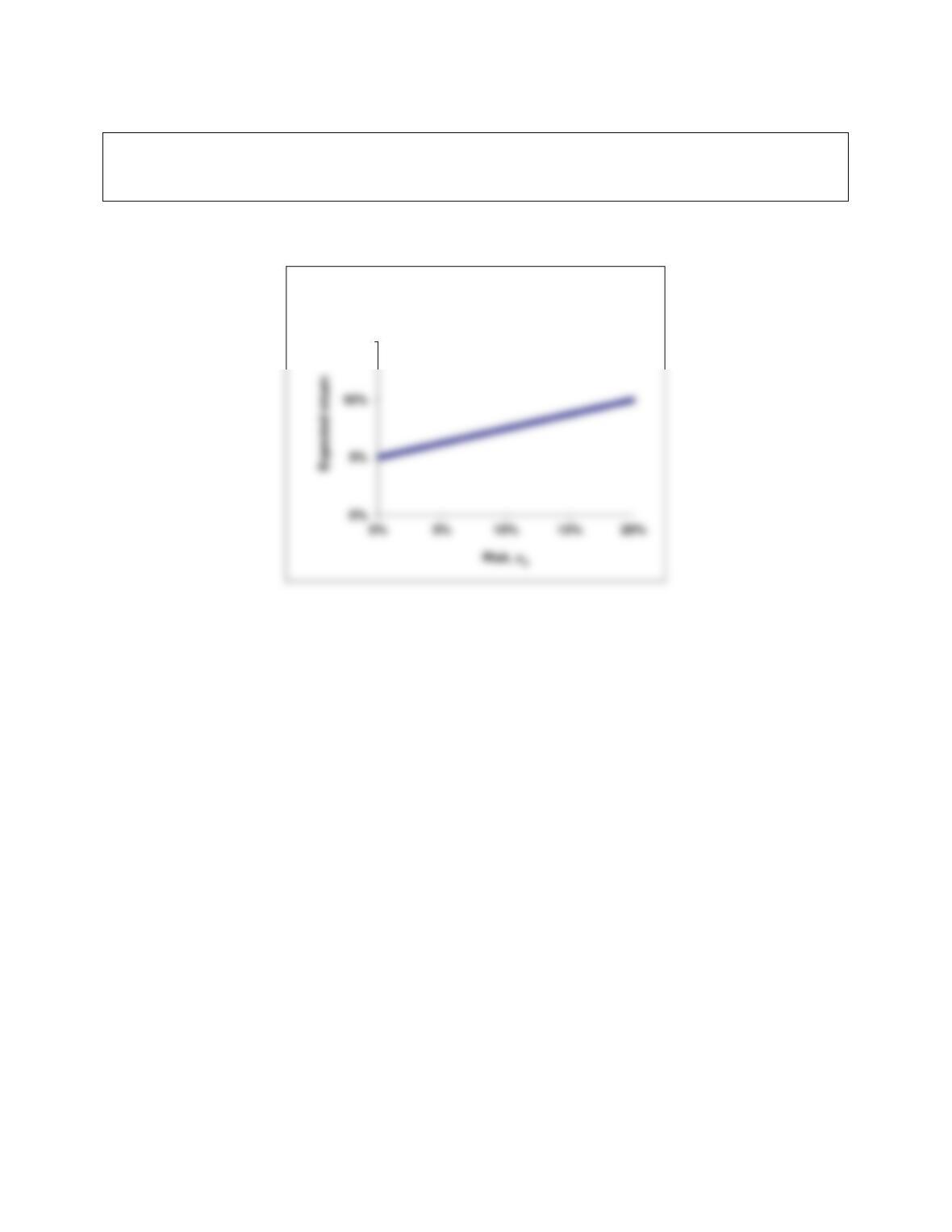

25-5 a. A plot of the approximate regression line is shown in the following figure:

Answers and Solutions: 25 - 4

Using Excel, the regression equation estimates are: Beta = 0.56; Intercept = 0.037; R2

= 0.96.

10

15

20

25

30

r

X

(%)

Answers and Solutions: 25 - 5

b. The arithmetic average return for Stock X is calculated as follows:

%.6.10

7

)2.18...0.230.14(

rAvg =

+++−

=

The standard deviation of returns for the market portfolio is similarly determined to

be 22.6 percent. The results are summarized below:

Stock X Market Portfolio

Average return,

Avg

r

10.6% 12.1%

Standard deviation, σ 13.1 22.6

c. Since Stock X is in equilibrium and plots on the Security Market Line (SML), and

given the further assumption that

XX rr =

and

MM rr =

--and this assumption often

does not hold--then this equation must hold:

Answers and Solutions: 25 - 7

d. The SML is plotted below. Data on the risk-free security (bRF = 0,

rRF = 8.6%) and Security X (bX = 0.56,

X

r

= 10.6%) provide the two points through

which the SML can be drawn. rM provides a third point.

e. In theory, you would be indifferent between the two stocks. Since they have the same

beta, their relevant risks are identical, and in equilibrium they should provide the

same returns. The two stocks would be represented by a single point on the SML.

Stock Y, with the higher standard deviation, has more diversifiable risk, but this risk

k(%)

20

r(%)

Answers and Solutions: 25 - 8

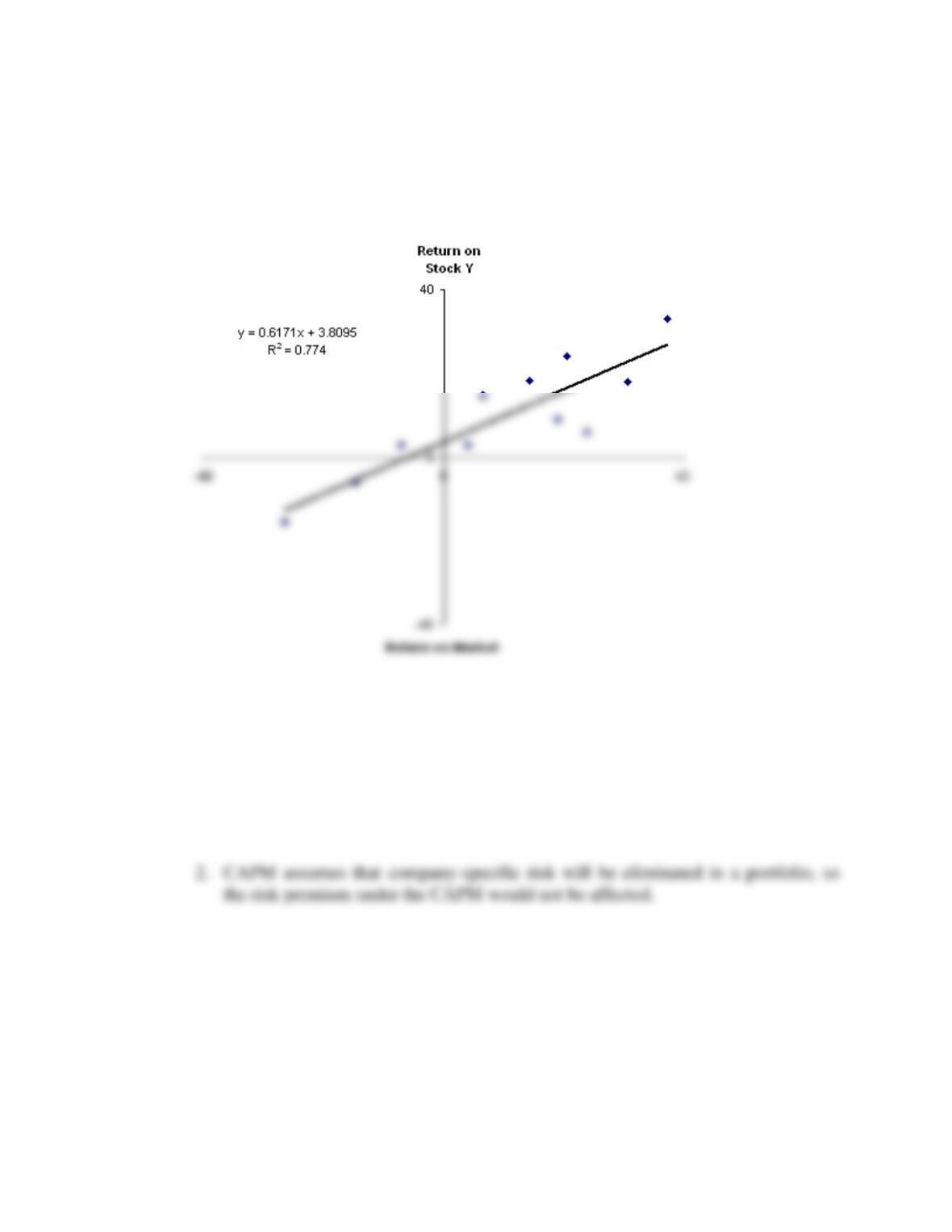

25-6

a. The regression graph is shown below. Using a spreadsheet, we find b = 0.62.

b. Because b = 0.62, Stock Y is about 62 percent as volatile as the market; thus, its

relative risk is about 62 percent of that of an average firm.

c. 1. Total risk

)( 2

Y

would be greater because the second term of the firm's risk

equation,

2

eY

2

M

2

Y

2

Yb+=

, would be greater.

Answers and Solutions: 25 - 9

d. 1. The stock's variance would not change, but the risk of the stock to an investor

holding a diversified portfolio would be greatly reduced.

Answers and Solutions: 25 - 10

SOLUTION TO SPREADSHEET PROBLEM

Mini Case: 25 - 11

MINI CASE

Answer the following questions.

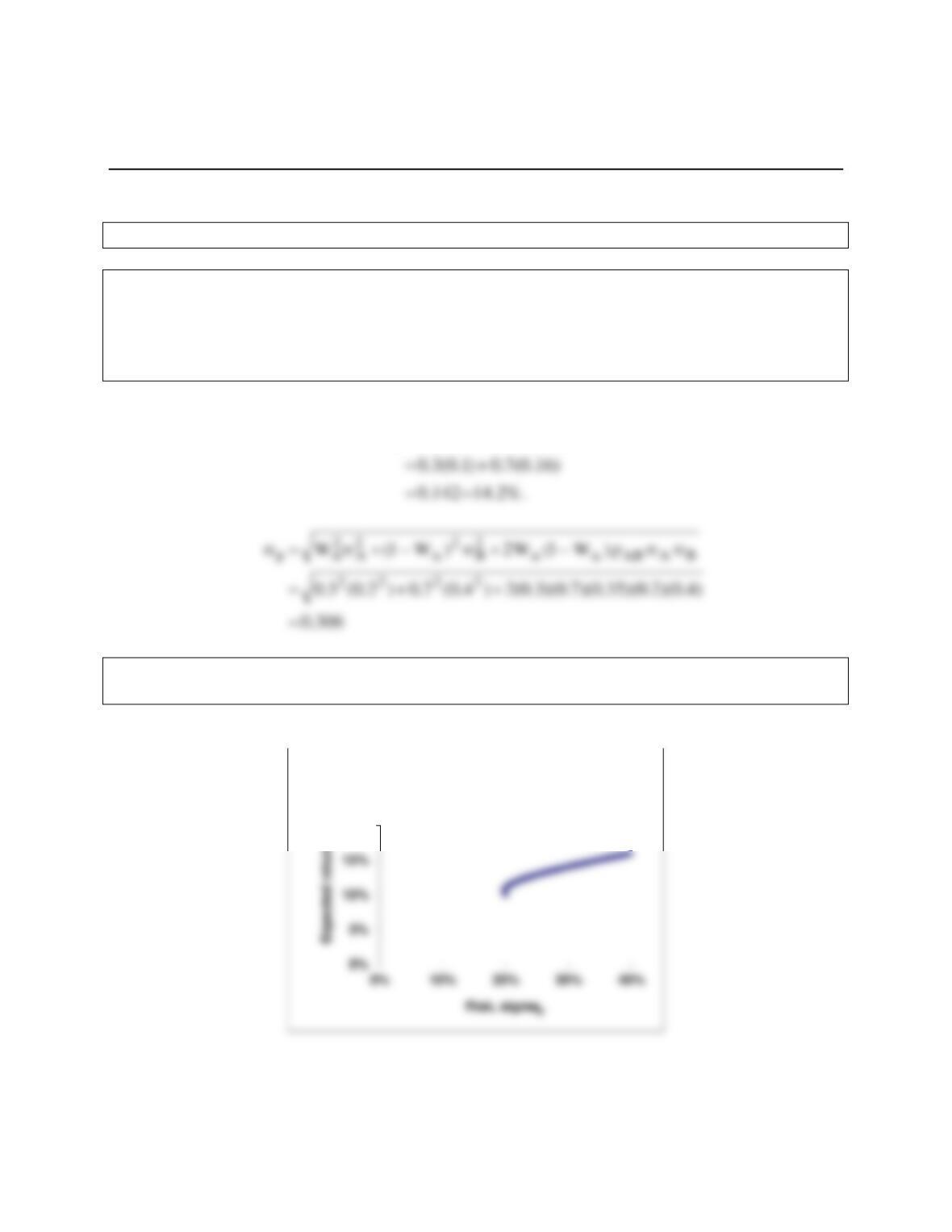

a. Suppose asset A has an expected return of 10 percent and a standard deviation

of 20 percent. Asset B has an expected return of 16 percent and a standard

deviation of 40 percent. If the correlation between A and B is 0.35, what are the

expected return and standard deviation for a portfolio comprised of 30 percent

asset A and 70 percent asset B?

Answer:

r

ˆ

)w1(r

ˆ

wr

ˆBAAAP

−+=

b. Plot the attainable portfolios for a correlation of 0.35. Now plot the attainable

portfolios for correlations of +1.0 and -1.0.

Answer:

20%

pAB = +0.35: Attainable Set of

Risk/Return Combinations

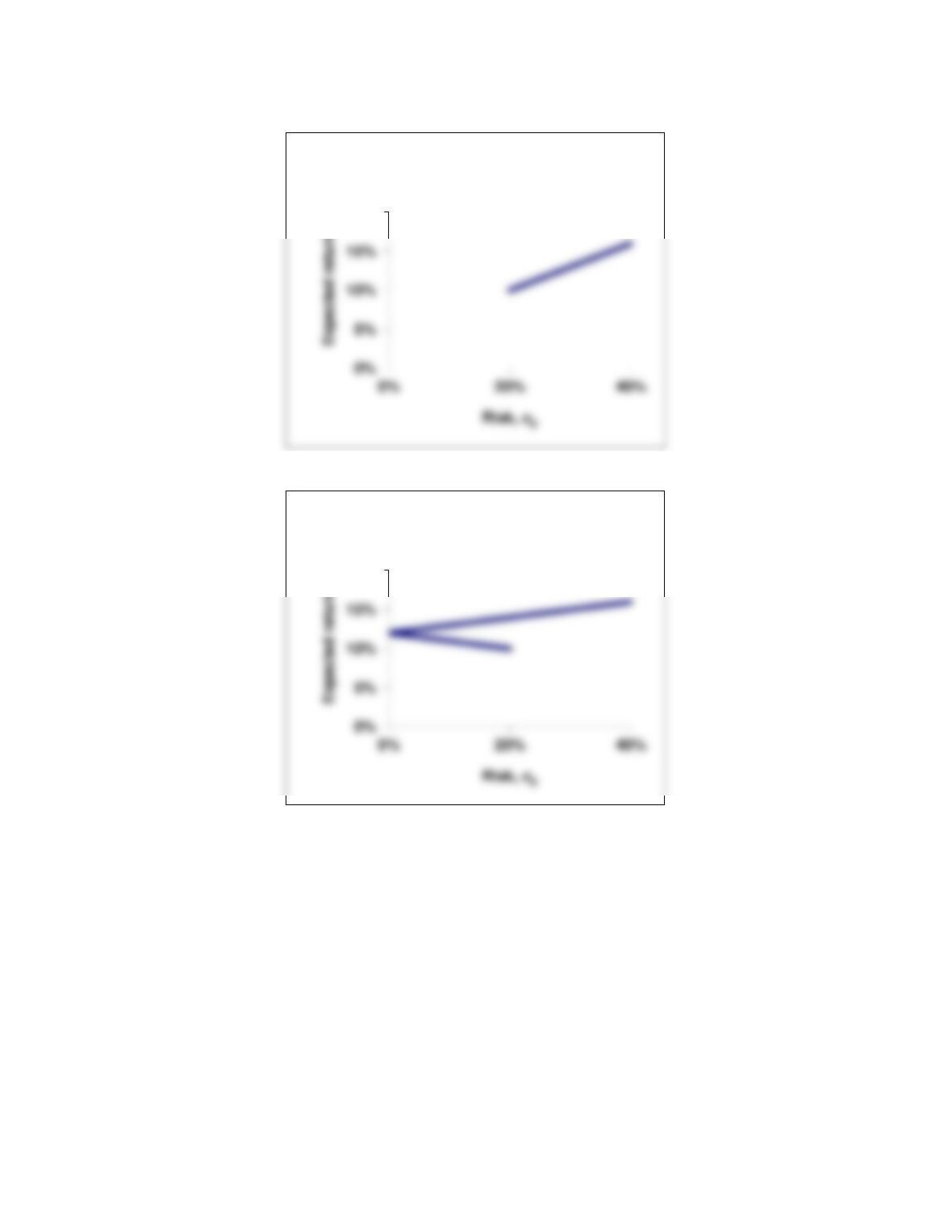

Mini Case: 25 - 12

20%

AB = +1.0: Attainable Set of Risk/Return

Combinations

20%

AB = -1.0: Attainable Set of Risk/Return

Combinations

Mini Case: 25 - 13

c. Suppose a risk-free asset has an expected return of 5 percent. By definition, its

standard deviation is zero, and its correlation with any other asset is also zero. Using

only asset A and the risk-free asset, plot the attainable portfolios.

Answer:

15%

Attainable Set of Risk/Return

Combinations with Risk-Free Asset

Mini Case: 25 - 14

d. Construct a reasonable, but hypothetical, graph which shows risk, as measured

by portfolio standard deviation, on the x axis and expected rate of return on the

y axis. Now add an illustrative feasible (or attainable) set of portfolios, and show

what portion of the feasible set is efficient. What makes a particular portfolio

efficient? Don't worry about specific values when constructing the graph—

merely illustrate how things look with "reasonable" data.

Answer:

Expected Portfolio

B

C

Return, kp

Efficient Set

(A,B)

^

Expected Portfolio

Return

^

rP

Mini Case: 25 - 15

e. Now add a set of indifference curves to the graph created for part B. What do

these curves represent? What is the optimal portfolio for this investor? Finally,

add a second set of indifference curves which leads to the selection of a different

optimal portfolio. Why do the two investors choose different portfolios?

Answer:

The figure above shows the indifference curves for two hypothetical investors, A and

B. To determine the optimal portfolio for a particular investor, we must know the

Expected Portfolio

Risk,

p

A

B

C

D

E

IA3

IA2

IA1

IB2

IB1

Optimal

Portfolio

Investor B

Optimal

Portfolio

Investor A

Return, kp

^

Expected Portfolio

Return,

^

rp

risk, P

Mini Case: 25 - 16

f. What is the capital asset pricing model (CAPM)? What are the assumptions

that underlie the model?

Answer: The Capital Asset Pricing Model (CAPM) is an equilibrium model which specifies

the relationship between risk and required rates of return on assets when they are held

in well-diversified portfolios. The CAPM requires an extensive set of assumptions:

• All investors are single-period expected utility of terminal wealth maximizers,

who choose among alternative portfolios on the basis of each portfolio's expected

return and standard deviation.

Mini Case: 25 - 17

g. Now add the risk-free asset. What impact does this have on the efficient

frontier?

Answer: The risk-free asset by definition has zero risk, and hence σ = 0%, so it is plotted on

the vertical axis. Now, given the possibility of investing in the risk-free asset,

investors can create new portfolios that combine the risk-free asset with a portfolio of

Expected Portfolio

Risk,

p

A

B

Z

M

kRF

Return, kp

^

Expected Portfolio

Return,

^

rp

rR

F

σp

Mini Case: 25 - 18

h. Write out the equation for the capital market line (CML) and draw it on the

graph. Interpret the CML. Now add a set of indifference curves, and illustrate

how an investor's optimal portfolio is some combination of the risky portfolio

and the risk-free asset. What is the composition of the risky portfolio?

Answer: The line rRFmz in the figure above is called the capital market line (CML). It has an

intercept of rRF and a slope of

MRF

M/)rr( −

. Therefore the equation for the capital

market line may be expressed as follows:

Mini Case: 25 - 19

i. What is a characteristic line? How is this line used to estimate a stock’s beta

coefficient? Write out and explain the formula that relates total risk, market

risk, and diversifiable risk.

Answer: Betas are calculated as the slope of the characteristic line, which is the regression line

formed by plotting returns on a given stock on the y axis against returns on the

general stock market on the x axis. In practice, 5 years of monthly data, with 60

observations, would be used, and a computer would be used to obtain a least squares

Mini Case: 25 - 20

j. What are two potential tests that can be conducted to verify the CAPM? What

are the results of such tests? What is roll’s critique of CAPM tests?

Answer: Since the CAPM was developed on the basis of a set of unrealistic assumptions,

empirical tests should be used to verify the CAPM. The first test looks for stability in

historical betas. If betas have been stable in the past for a particular stock, then its

historical beta would probably be a good proxy for its ex-ante, or expected beta.

Mini Case: 25 - 21

k. Briefly explain the difference between the CAPM and the arbitrage pricing

theory (APT).

Answer: The CAPM is a single-factor model, while the Arbitrage Pricing Theory (APT) can

include any number of risk factors. It is likely that the required return is dependent