Chapter 24

ANSWERS TO QUESTIONS

1. What does the Lucas critique state about the limitations of our current understanding of the

way in which the economy works?

The Lucas critique says that policymakers’ priors about the effects of a given policy will

2. “The Lucas critique by itself casts doubt on the ability of discretionary stabilization policy to

be beneficial.” Is this statement true, false, or uncertain? Explain your answer.

3. Suppose an econometric model based on past data predicts a small decrease in domestic

investment when the Federal Reserve increases the federal funds rate. Assume the Federal

Reserve is considering an increase in the federal funds rate target to fight inflation and

promote a low inflation environment that will encourage investment and economic growth.

a. Discuss the implications of the econometric model’s predictions if individuals interpret

the increase in the federal funds rate target as a sign that the Fed will keep inflation at

low levels in the long run.

b. What would be Lucas’s critique of this model?

Lucas’s critique will point out the fact that the model was probably constructed by using

4. If the public expects the Fed to pursue a policy that is likely to raise short-term interest rates

permanently to 5%, but the Fed does not go through with this policy change, what will

happen to long-term interest rates? Explain your answer.

Long-term interest rates will fall. Theories of the term structure suggest that long-term

interest rates are related to the expected average of future short-term interest rates. When the

5. In what sense can greater central bank independence make the time-inconsistency problem

worse?

When central banks are more independent, there is less formal accountability by them to

pursue stable inflation policies. In this sense, it is easier for central banks to give the

6. What are the arguments for and against policy rules?

Advocates of rules argue that they solve the time-inconsistency problem so that policymakers

will achieve good long-run economic outcomes, that they will prevent repeating serious

7. If, in a surprise victory, a new administration that the public believes will pursue inflationary

policy is elected to office, predict what might happen to the level of output and inflation even

before the new administration comes into power.

8. Many economists are worried that a high level of budget deficits may lead to inflationary

monetary policies in the future. Could these budget deficits have an effect on the current rate

of inflation?

Yes, if budget deficits are expected to lead to an inflationary monetary policy and

9. In some countries, the president chooses the head of the central bank. The same president

can fire the head of the central bank and replace him or her with another director at any

time. Explain the implications of such a situation for the conduct of monetary policy. Do you

think the central bank will follow a monetary policy rule, or will it engage in discretionary

policy?

When a president has the authority to nominate or lay off the head of the central bank, it is

quite plausible that the conduct of monetary policy would be discretionary. Adherence to

10. How would an unexpected change in the equilibrium real fed funds rate be an argument

against using a Taylor rule for monetary policy implementation?

One of the criticisms of using rules is that often times, once implemented, structural changes

in the economy necessitate updating the rule regularly to reflect appropriate policy outcomes.

11. How is constrained discretion different from discretion in monetary policy? How are the

outcomes of these policies likely to differ?

Constrained discretion is a more transparent and disciplined type of discretion in which the

general objectives and tactics of the policymaker are committed to in advance. This allows

12. In general, how does credibility (or lack thereof) affect the aggregate supply curve?

In general, when central banks lack credibility, there is little faith by the public that the

13. In Japan, the government and central bank have enacted policies recently to raise inflation

permanently from persistently low levels, however inflation continues to remain near zero.

How, if at all, might credibility of the central bank explain the low inflation persistence?

Normally, expansionary fiscal or monetary policies (especially when implemented together)

should result in higher inflation and consequently raise inflation expectations to permanently

14. As part of its response to the global financial crisis, the Fed lowered the federal funds rate

target to nearly zero by December 2008 and quadrupled the monetary base between 2008

and 2017, a considerable easing of monetary policy. However, survey-based measures of

five- to ten-year inflation expectations remained low throughout most of this period.

Comment on the Fed’s credibility in fighting inflation.

This is a clear sign that the Fed enjoys a high level of credibility. This credibility was

probably earned over the last three decades. Although the Fed never explicitly stated an

15. “The more credible the policymakers who pursue an anti-inflation policy, the more

successful that policy will be.” Is this statement true, false, or uncertain? Explain your

answer.

True, if expectations about policy affect the wage- and price-setting process. In models in

16. Why did the oil price shocks of the 1970s affect the economy differently than the oil price shocks

of 2007?

As Figure 3 in the chapter demonstrates, the oil price shocks in the 1970s resulted in

significantly higher inflation and unemployment as compared to the shock that affected the

17. Central banks that engage in inflation targeting usually announce the inflation target and

time period for which that target will be relevant. In addition, central bank officials are held

accountable for their actions (e.g., they could be fired if the target is not reached), and their

success or lack thereof is also public information. Explain why transparency is such a

fundamental ingredient of inflation targeting.

Announcements about the inflation targets and potential punishments for central bank

officials are crucial for inflation targeting. It is very important for the public to be able to

check whether the target has been reached or not. When central bank officials know that the

18. In recent years, central banks have dramatically increased the amount of communication

with market participants and the public, and at the same time in many of these countries,

average inflation has declined and become less volatile. Is this coincidence, or is there a

connection? Explain.

19. What are the purposes of inflation targeting, and how does this monetary policy strategy

achieve them?

Inflation targeting has two basic purposes, to keep inflation under control and to increase the

credibility of monetary policymakers’ commitment to price stability. These are achieved by

20. How can the establishment of an exchange-rate target bring credibility to a country with a

poor record of inflation stabilization?

Tying its domestic currency to another country’s currency is an easy way for a country with a

poor inflation record to establish credibility. This is because a formal exchange rate target

21. What traits characterize a “conservative” central banker?

ANSWERS TO APPLIED PROBLEMS

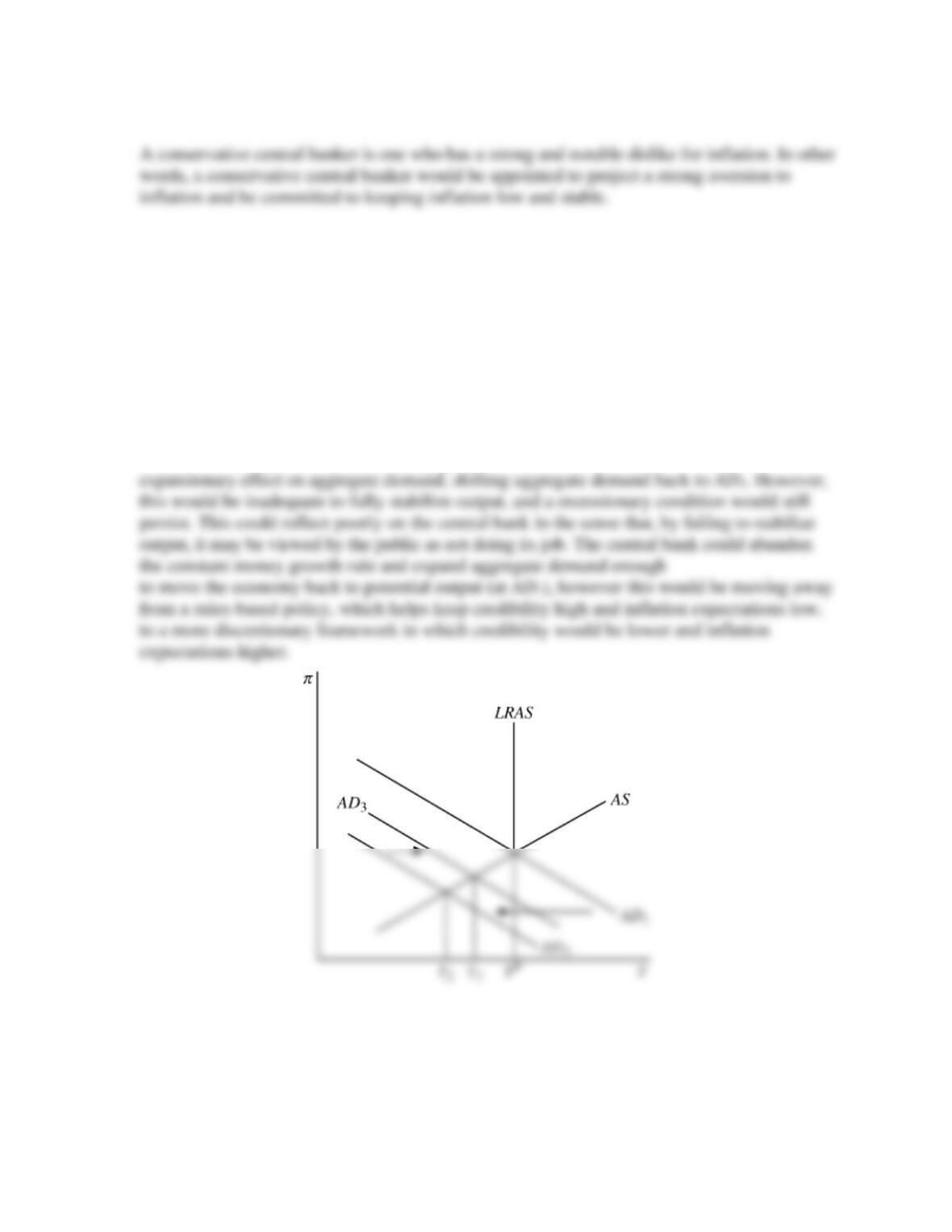

22. Suppose the central bank is following a constant-money-growth-rate rule and the economy is hit

with a severe economic downturn. Use an aggregate supply and demand graph to show the

possible effects on the economy. How does this situation reflect on the credibility of the central

bank if it maintains the money growth rule? How does it reflect on the central bank’s credibility

if it abandons the money growth rule to respond to the downturn?

A severe downturn would result in the aggregate demand curve shifting sharply to the left to

AD2 below. With a strict constant money growth rule, this would result in a limited

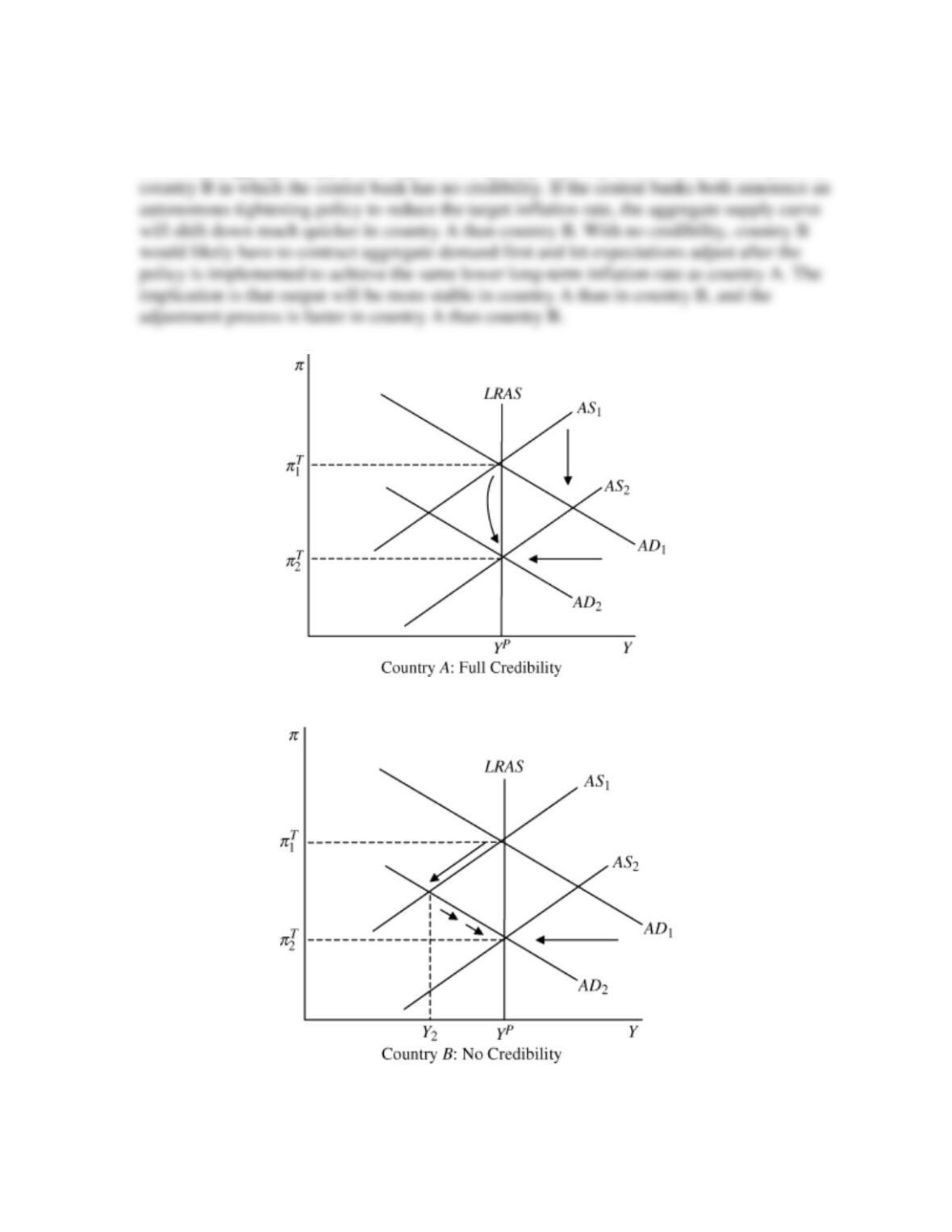

23. Suppose country A has a central bank with full credibility, and country B has a central bank

with no credibility. How does the credibility of each country’s central bank affect the speed

of adjustment of the aggregate supply curve to policy announcements? How does this result

affect output stability? Use an aggregate supply and demand diagram to demonstrate.

In country A, the public is more likely to believe announcements about future policy

changes, and therefore adjust inflation expectations in anticipation of changes in future policy.

As a result, aggregate supply will adjust more quickly to policy announcements compared to

24. Suppose two countries have identical aggregate demand curves and potential levels of

output, and

is the same in both countries. Assume that in 2016, both countries are hit with

the same negative supply shock. Given the table of values below for inflation in each country,

what can you say, if anything, about the credibility of each country’s central bank? Explain

your answer.

Country A

Country B

%

%

2016

3.8

%

%

2017

3.5

5.0

5.5

%

%

2018

3.2

%

%

4.3

Since the aggregate demand curve, potential output, the parameter

, and the price shock are

identical in both countries, the only factor that can explain the difference in inflation between

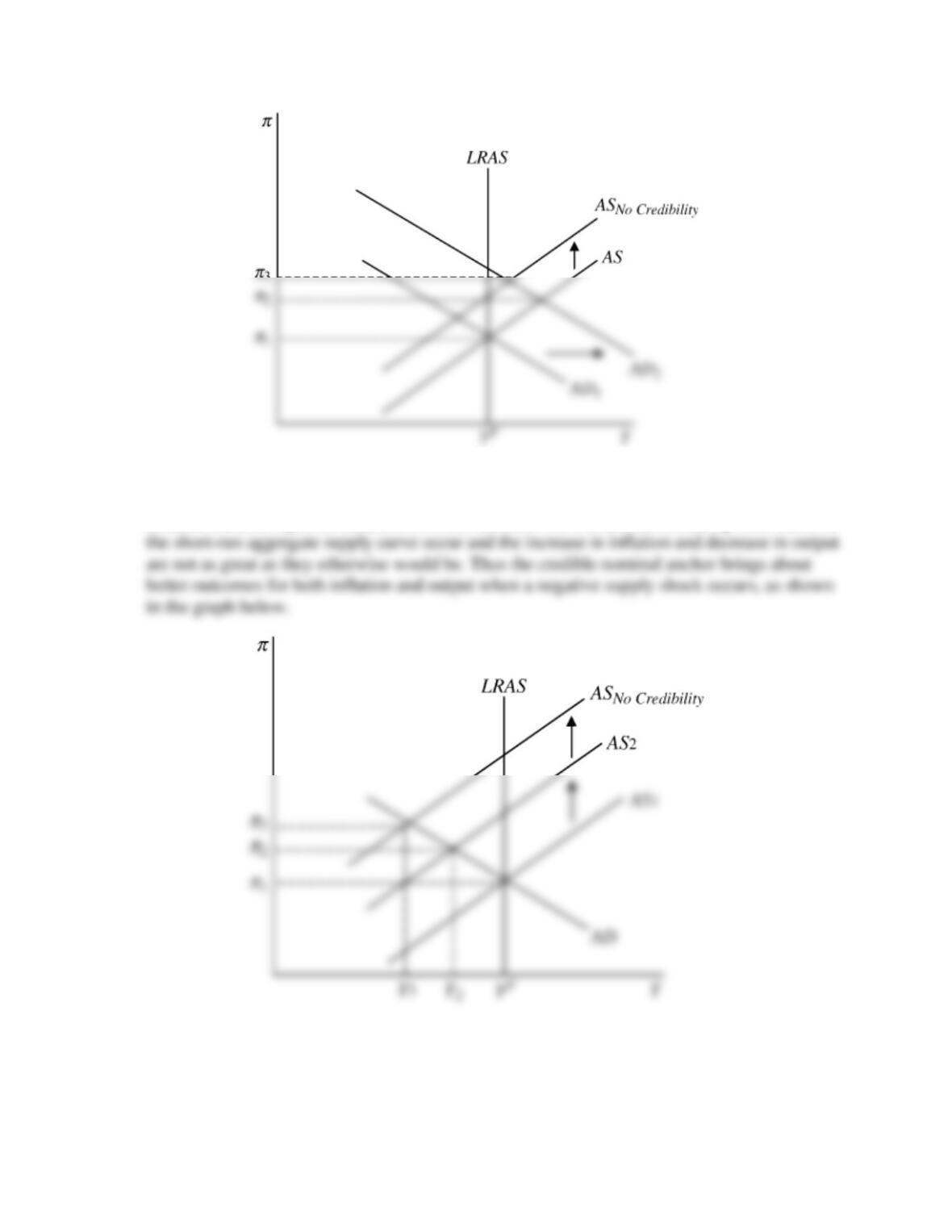

25. How does a credible nominal anchor help improve the economic outcomes that result from a

positive aggregate demand shock? How does a credible nominal anchor help if a negative

aggregate supply shock occurs? Use graphs of aggregate supply and demand to

demonstrate.

Positive aggregate demand shocks shift the aggregate demand curve to the right, causing both

inflation and output to rise. Without a credible nominal anchor, the increase in inflation

The outcome is similar when a negative aggregate supply shock occurs. Inflation increases

and output falls as the short-run aggregate supply curve shifts upward, but with a credible

nominal anchor, expected inflation does not increase. As a result, no further upward shifts of

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database and find data on the personal

consumption expenditure price index (PCECTPI). Convert the units setting to “Percent

Change from Year Ago,” and download the data. Beginning in January 2012, the Fed

formally announced a 2% inflation goal over the “longer-term.”

a. Calculate the average inflation rate over the last four and the last eight quarters of data

available. How does it compare to the 2% inflation goal?

b. What, if anything, does your answer to part (a) imply about Federal Reserve credibility?

Over both the one year and two year horizons the Fed missed its target by a meaningful

2. Go to the St. Louis Federal Reserve FRED database and find data on the core PCE price

index (PCEPILFE) and the spot price of a barrel of oil (WTISPLC). For both variables,

convert the units setting to “Percent Change from Year Ago,” and download the data from

1960 to the most recent available data.

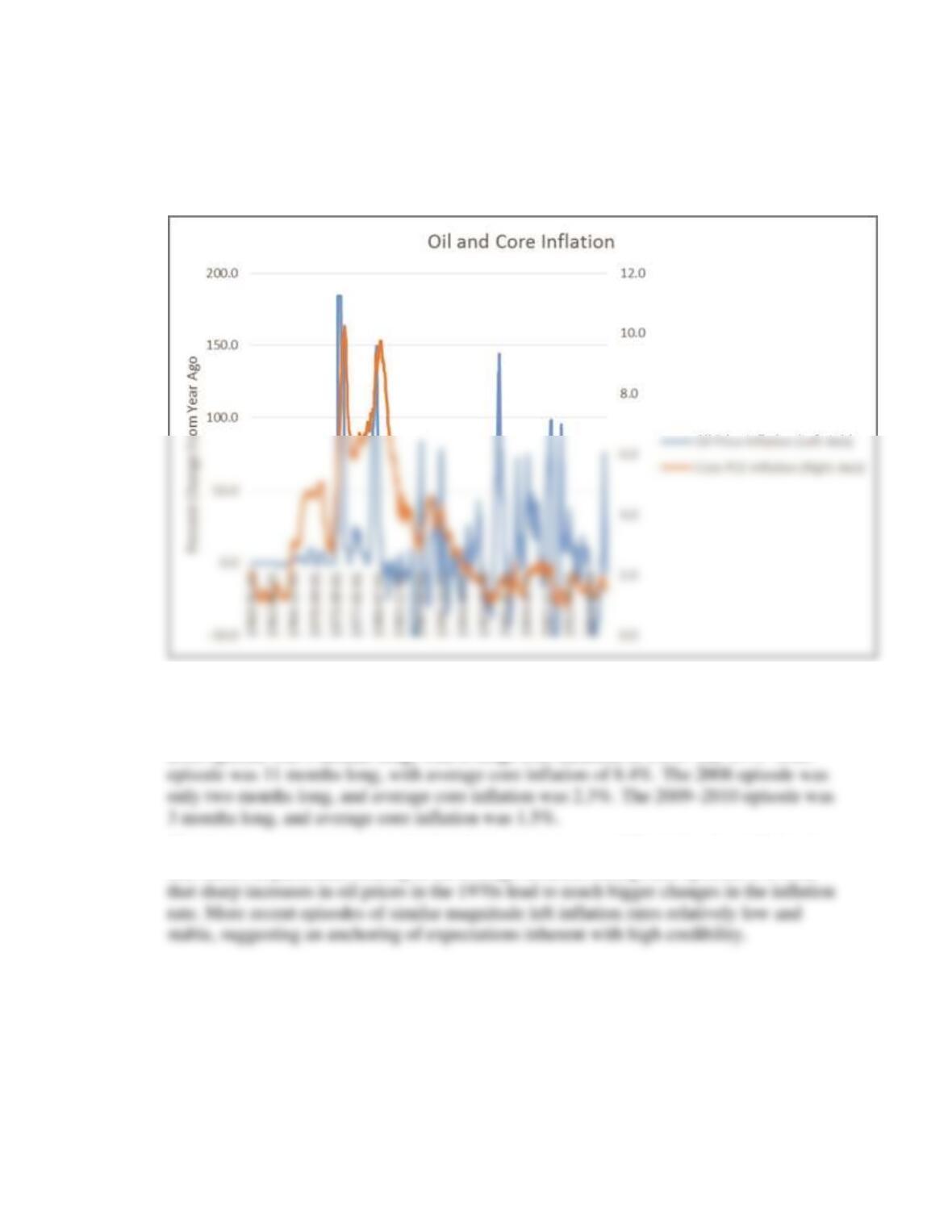

a. Identify periods in which oil price inflation is 80% or higher.

a. See graph below. Oil price inflation was 80% or higher during the periods of January

1974–December 1974; September 1979–July 1980; July 1987; November 1999–March

2000; May 2008–June 2008; and December 2009–February 2010

b. For the 1974 episode, it lasted 12 months, and average inflation during that time was

7.9%. The 1979–1980 episode was 11 months long, with average core inflation of 8.4%.

The 1987 episode was only 1 month long, with average core inflation of 3.2%. The 1999–

2000 episode was 5 months long, with average core inflation of 1.6%. The 1979–1980

c. Clearly, the recent monetary policy has been much more credible in keeping inflation low

and stable. In particular, looking at the average inflation during each episode, it is clear