12/10/2012

d. Describe the eight components of the COSO ERM framework.

g. What are forward contracts? How can they be used to manage foreign exchange risk?

5,000,000

7%

20 years

So if Tennessee Sunshine waits and interest rates increase by 1%, they could lose almost half a million dollars through higher

interest costs. They can hedge this cost with T-Bond futures.

rate of 6% (payable semi-annually).

Size of futures contract (dollars per contract) = $100,000

Settle price on futures contract as quoted = 111 and 25 32nds

Settle price on futures contract (% of par, decimal) = 111.781%

Settle price on futures contract (dollars) = $111,781

Size of planned debt offering = $5,000,000

Value of futures contract (dollars per contract) = $111,781.0

i. It is January and Tennessee Sunshine is considering issuing $5 million in bonds in June to raise capital for an expansion, and is concerned

that interest rates will rise during the interim. Currently, TS can issue 20-year bonds at 7%, but interest rates are on the rise and Stooksbury

is concerned that long-term interest rates might rise by as much as 1% before June. You looked online and found that June T-Bond futures

are trading at 111-25. What are the risks of not hedging and how might TS hedge this exposure? In your analysis, consider what would

happen if interest rates all increased by 1%.

Size of bond issue

Chapter 23. Mini Case for Enterprise Risk Management

Assume you have just been hired as a financial analyst by Tennessee Sunshine Inc., a mid-sized Tennessee company that specializes in

creating exotic sauces from imported fruits and vegetables. The firm’s CEO, Bill Stooksbury, recently returned from an industry corporate

executive conference in San Francisco, and one of the sessions he attended was on the pressing need for companies to institute enterprise

risk management programs. Since no one at Tennessee Sunshine is familiar with the basics of enterprise risk management, Stooksbury has

asked you to prepare a brief report that the firm’s executives could use to gain at least a cursory understanding of the topics.

To begin, you gathered some outside materials on derivatives and risk management and used these materials to draft a list of pertinent

questions that need to be answered. In fact, one possible approach to the paper is to use a question-and-answer format. Now that the

questions have been drafted, you have to develop the answers.

f. What are some actions that companies can take to minimize or reduce risk exposures? Answer: See Chapter 23 Mini Case Show

h. Describe how commodity futures markets can be used to reduce input price risk. Answer: See Chapter 23 Mini Case Show

a. Why might stockholders be indifferent whether or not a firm reduces the volatility of its cash flows? Answer: See Chapter 23

c. What is COSO? How does COSO define enterprise risk management?

e. Describe the following major categories of risk: (1) strategy and reputation, (2) control and compliance, (3) hazards, (4) human resources,

(5) operations, (6) technology, and (7) financial management.

Current interest rate

Maturity of debt issue

If interest rates increased from 7% to 8%, then the value of the bonds would decrease from $5,000,000 to:

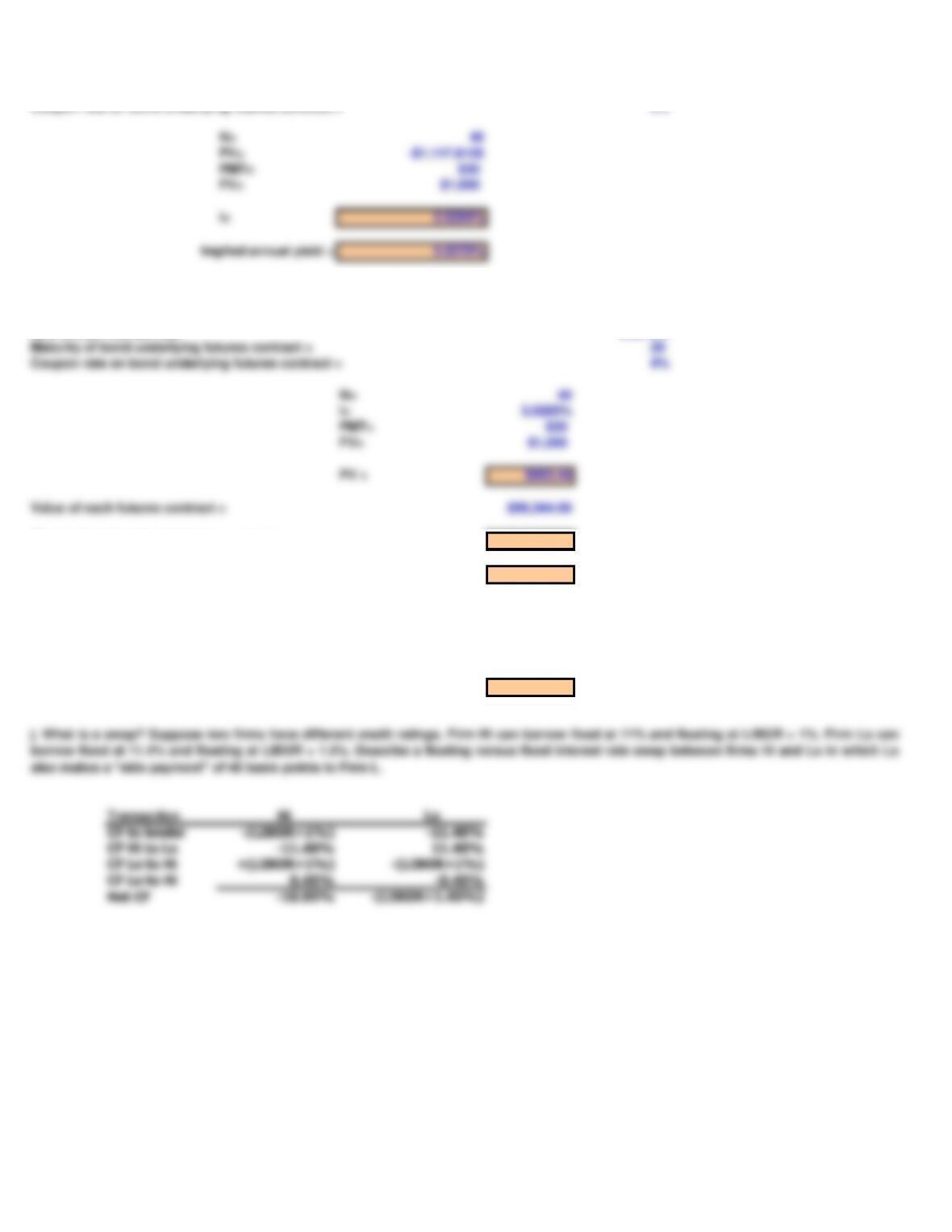

Tennessee Sunshine will use a short hedge, which means it agrees to deliver the contract in June (actually, it will not deliver bonds, but will

settle up). How many contracts must TS sell short?

Settle price on futures contract (% of par, decimal) = 111.78125%

Maturity of bond underlying futures contract = 20

Coupon rate on bond underlying futures contract = 6%

Suppose interest rates increase. What happens to the price of the futures contract?

Interest rate increase: 1%

New annual interest rate: 6.0570%

Maturity of bond underlying futures contract = 20

Coupon rate on bond underlying futures contract = 6%

Value of each futures contract = $99,344.00

Change in value of each futures contract = -$12,437.00

Total of change in value of all contracts = -$559,665.00

Profit or loss from issuing bonds at new rate= -$494,819.0

Profit or loss from futures contract = -$559,665.0

Net profit or loss from hedge = -$1,054,484.0

What is the net impact on TS?

The implied yield is based on the quoted price and the hypothetical bond’s coupon of 6% and maturity of 20 years. Note that the price is

quoted as a percent of par, and it is quoted in percentage points and 32nd of percentage points.