Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 254

Chapter 23

ANSWERS TO QUESTIONS

1. What does it mean when we say that the inflation gap is negative?

2. “If autonomous spending falls, the central bank should lower its inflation target in order to

stabilize inflation.” Is this statement true, false, or uncertain? Explain your answer.

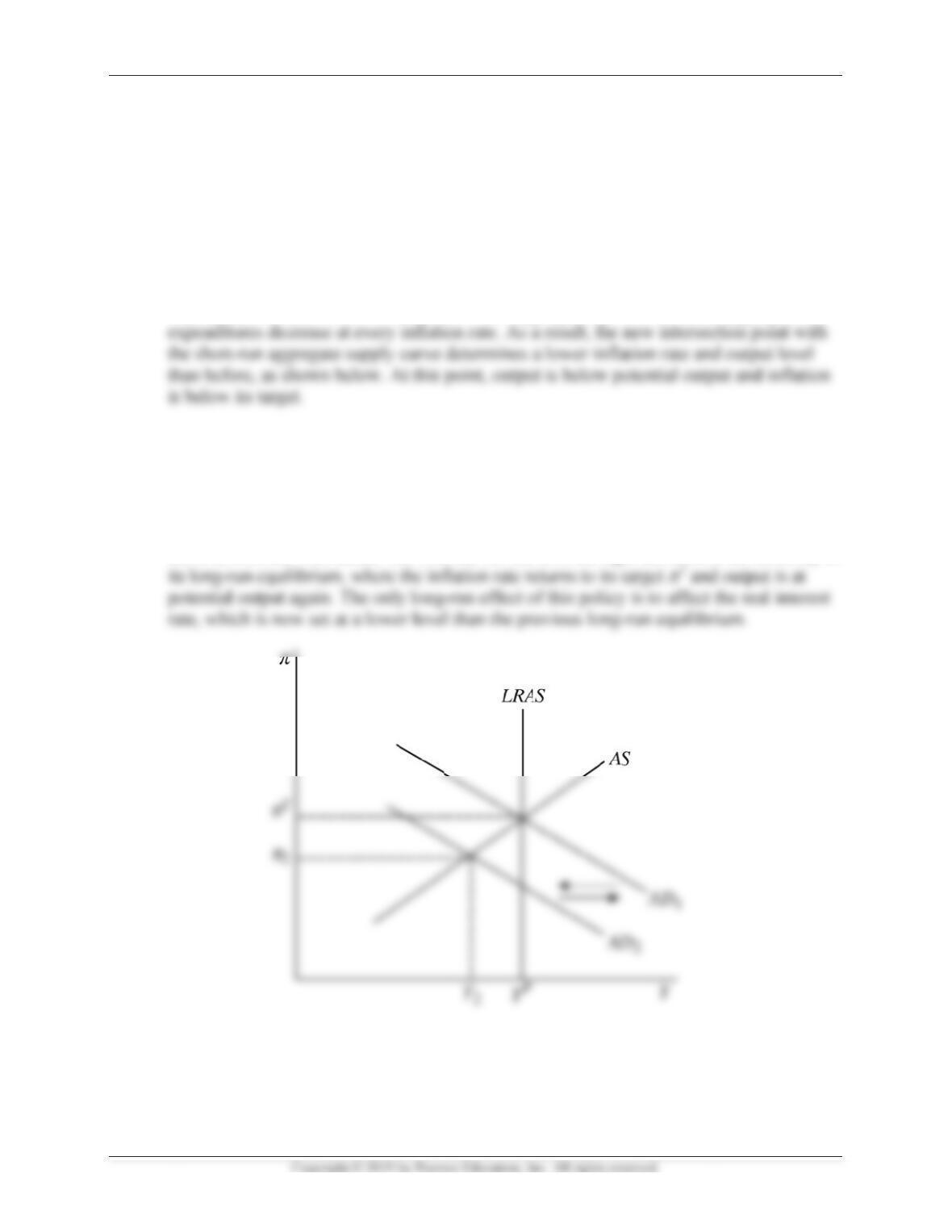

False. If the central bank pursues stabilization policy, it can stabilize both inflation and

output simultaneously by an autonomous easing of policy. If it lowered its inflation target,

3. For each of the following shocks, describe how monetary policymakers would respond (if at

all) to stabilize economic activity. Assume the economy starts at a long-run equilibrium.

a. Consumers reduce autonomous consumption.

A reduction in autonomous consumption reduces aggregate demand, so monetary

policymakers would pursue an autonomous easing of monetary policy to stabilize

economic activity.

b. Financial frictions decrease.

A reduction in financial frictions increases aggregate demand, so monetary

c. Government spending increases.

An increase in government spending increases aggregate demand, so monetary

d. Taxes increase.

An increase in taxes reduces aggregate demand, so monetary policymakers would pursue

an autonomous easing of monetary policy to stabilize economic activity.

e. The domestic currency appreciates.

An appreciation of the domestic currency leads to lower exports and higher imports,

4. During the global financial crisis, how was the Fed able to help offset the sharp increase in

financial frictions without the option of lowering interest rates further? Did the Fed’s plan

work?

The Fed lowered the fed funds rate to zero during the crisis to offset falling aggregate

demand; however, this was insufficient to stabilize aggregate demand and output. As a result,

5. Why does the divine coincidence simplify the job of policymakers?

The divine coincidence exists when policies that are appropriate to achieve price stability also

stabilize economic activity. In this case, policymakers have easier jobs because there is no

tradeoff between policy objectives and they do not have to choose between them. They can,

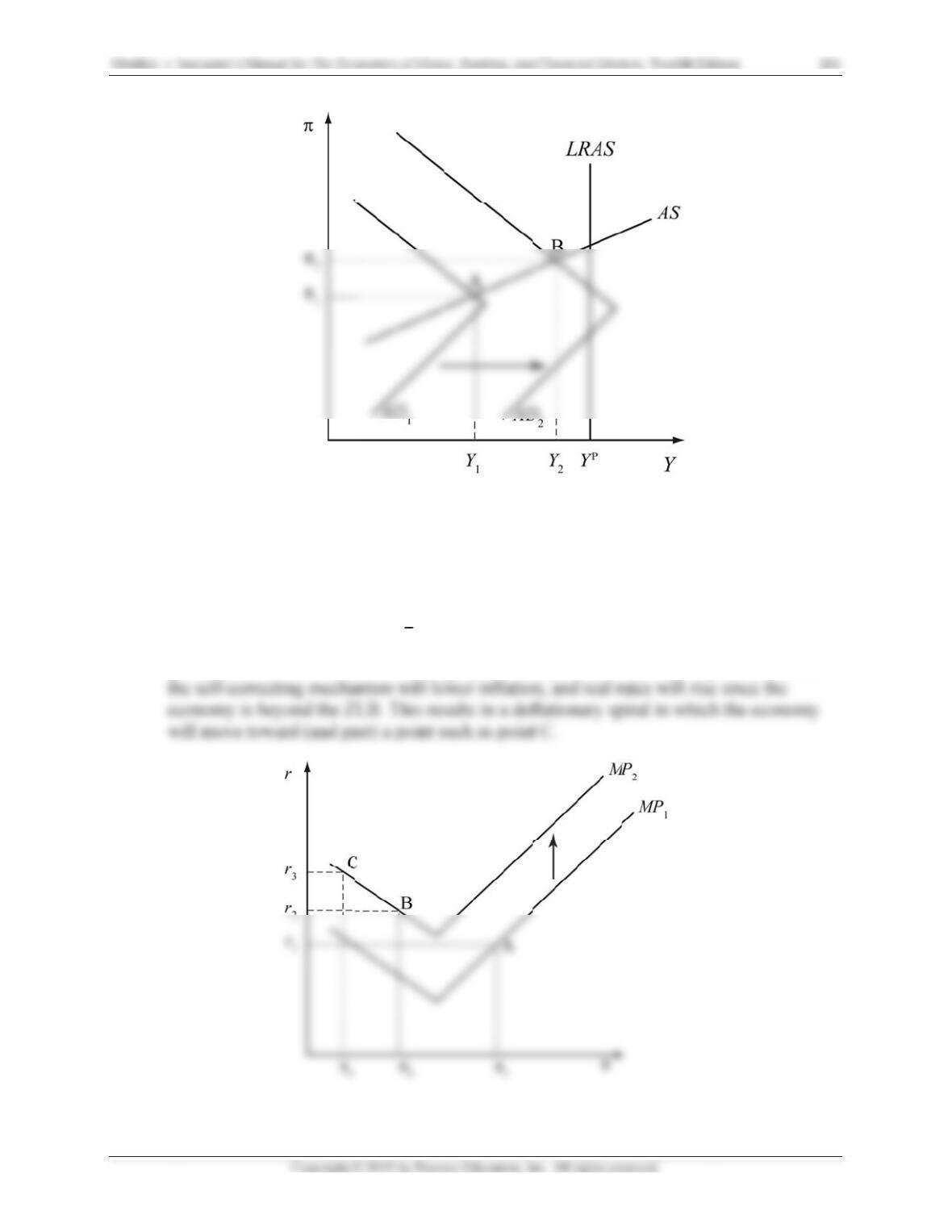

6. Why do temporary negative supply shocks pose a dilemma for policymakers?

With negative supply shocks, both inflation and the unemployment rate increase. In order to

reduce the unemployment rate, an expansionary policy must be pursued, which further

7. In what way is a permanent negative supply shock worse than a temporary negative supply

shock?

In both cases inflation rises and output falls; however, in the case of a permanent negative

supply shock, the long-run effects on these variables are permanent. With a temporary negative

8. Suppose three economies are hit with the same temporary negative supply shock. In country

A, inflation initially rises and output falls; then inflation rises more and output increases. In

country B, inflation initially rises and output falls; then both inflation and output fall. In

country C, inflation initially rises and output falls; then inflation falls and output eventually

increases. What type of stabilization approach did each country take?

9. “Policymakers would never respond by stabilizing output in response to a temporary positive

supply shock.” Is this statement true, false, or uncertain? Explain your answer.

Uncertain. A temporary positive supply shock has the dual benefits of increasing output and

also reducing inflation, so in some sense policymakers get the best of both worlds by not

10. The fact that it takes a long time for firms to get new plants and equipment up and running is

an illustration of what policy problem?

This demonstrates the problem of effectiveness lags in the implementation of monetary

11. In the United States, many observers have commented in recent years on the “political

gridlock in Washington D.C.” and referred to Congress as a ‘Do Nothing Congress”. What

type of policy lag is this describing?

12. Is stabilization policy more likely to be conducted through monetary policy or through fiscal

policy? Why?

Stabilization policy is conducted more frequently using monetary policy rather than fiscal

13. “If the data and recognition lags could be reduced, activist policy probably would be more

beneficial to the economy.” Is this statement true, false, or uncertain? Explain your answer.

14. If the economy’s self-correcting mechanism works slowly, should the government necessarily

pursue discretionary policy to eliminate unemployment? Why or why not?

15. In the early 1970s, an unexpected productivity slowdown lead most economists to believe

that potential output was larger than it actually was. How are policymakers likely to respond

under this situation, and what do you expect to be the outcome?

16. In both the 1960s and the 1970s in the United States, inflation increased significantly.

However, unemployment behaved very differently in the two decades. Why is this?

Even though inflation increased significantly in both decades, the sources of the increase

were different, leading to much different effects on unemployment. In the case of the 1960s,

17. Given a relatively steep and a relatively flat short-run aggregate supply curve, which curve

would support the case for nonactivist policy? Why?

When the short-run aggregate supply curve has a steeper slope, wages and prices in general

are more flexible (i.e., changes in output result in larger changes in the inflation rate). This

18. “Because government policymakers do not consider inflation desirable, their policies cannot

be the source of inflation.” Is this statement true, false, or uncertain? Explain your answer.

False. Even though policymakers do not want inflation, if they pursue goals such as high

19. How can monetary authorities target any inflation rate they wish?

20. What will happen if policymakers erroneously believe that the natural rate of unemployment

is 7% when it is actually 5% and therefore pursue stabilization policy?

If policymakers believe that the natural rate of unemployment is 7% when it is actually 5%,

then once the unemployment rate begins to drop below 7%, they are likely to pursue

21. How can demand-pull inflation lead to cost-push inflation?

When inflation increases due to demand-side conditions, this could prompt workers to

demand higher wages (which are greater than the growth in labor productivity) in anticipation

22. How does the policy rate hitting a floor of zero lead to an upward-sloping aggregate demand

curve?

When the zero lower bound is hit, a lower inflation rate leads to a higher real interest rate

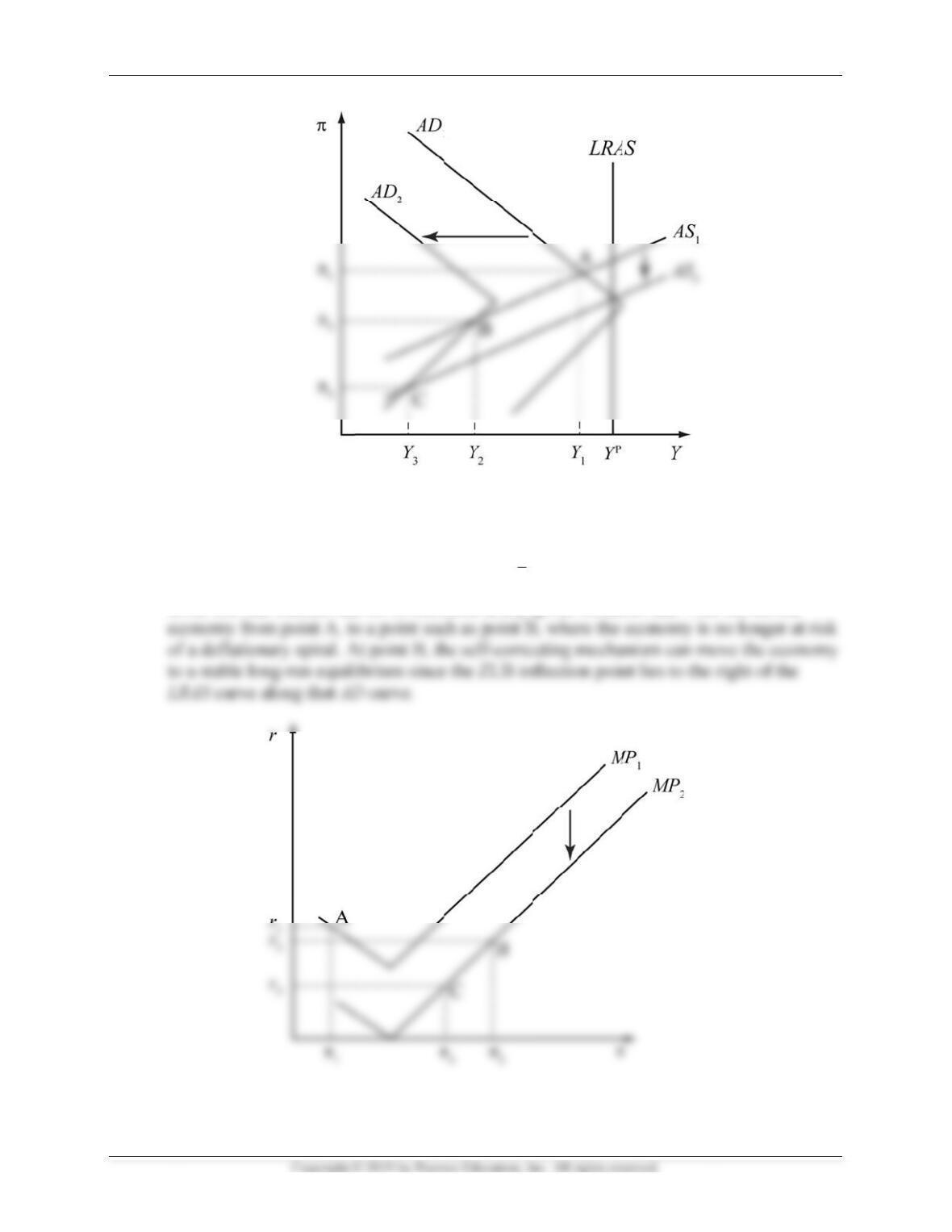

23. Why does the self-correcting mechanism stop working when the policy rate hits the zero

lower bound?

Because a negative output gap, which leads to a fall in the short-run aggregate supply curve,

24. In what ways can nonconventional monetary policy affect the real interest rate for

investments when the economy reaches the zero lower bound? How are credit spreads

affected?

There are a number of ways the central bank can reduce the real interest rate for investments

at the zero lower bound. By providing liquidity to key credit markets, the central bank can

directly reduce financial frictions, which lowers the real interest rate for investments at any

given safe policy interest rate. In this case, credit spreads are reduced directly as financial

Mishkin •

ANSW

E

25.

Supp

of cu

t

a.

U

t

h

A

e

x

b.

W

t

h

I

f

e

f

c

u

t

q

w

f

f

e

e

t

d

d

I

nstructor’s Ma

n

E

RS TO AP

P

o

se the curr

t

ting the exi

s

U

sing a grap

h

e economy

A

ccording to

x

penditures

W

hat will be

h

e Federal

R

f

the Federa

l

f

fectively d

e

u

rve down

w

n

ual for The Ec

o

P

LIED PR

O

ent adminis

t

s

ting gover

n

h

of aggreg

a

in the short

aggregate

d

results in a

s

the effect o

n

R

eserve deci

d

l

Reserve de

e

crease the r

e

w

ard. This ac

t

o

nomics of Mon

e

O

BLEMS

t

ration deci

d

n

ment budge

a

te demand

a

run. Descri

b

d

emand and

s

s

hift to the l

e

n

the real in

t

d

es to stabil

cides to use

e

al interest

r

t

ion will shi

f

e

y, Banking, an

d

d

es to decre

a

t deficit.

a

nd supply,

b

e the effect

s

s

upply anal

y

e

ft in the ag

g

t

erest rate, t

h

i

ze the infla

t

its monetar

y

r

ate at every

f

t the AD cu

r

d

Financial Mar

k

a

se govern

m

show the ef

f

s

on inflatio

n

y

sis, the dec

r

g

regate de

m

h

e inflation

r

t

ion rate?

y

policy too

l

inflation ra

t

r

ve to the ri

g

k

ets, Twelfth E

d

m

ent expendi

t

ff

ects of such

n

and outpu

t

r

ease in gov

m

and curve,

a

r

ate, and th

e

l

s to stabiliz

e

t

e, thereby s

h

g

ht and resto

r

d

ition

tures as a

m

a decision

o

t

.

ernment

a

s aggregate

e

output lev

e

e inflation,

i

h

ifting the

M

r

e the econo

m

260

m

eans

o

n

e

l if

i

t will

MP

m

y to

x

x

h

u

e

i

i

a

a

c

c

26.

Use

a

resul

t

Supp

stabi

l

may

d

the e

c

c

c

n

k

s

a

k

e

a

p

x

p

x

g

27.

As

m

the a

g

the a

g

temp

o

dem

a

As s

e

give

n

e

e

t

o

g

c

g

e

a

e

a

c

,

e

c

e

m

m

n

n

a

graph of a

g

t

in undesir

a

ose the eco

n

l

ize output.

G

d

evise a pol

i

c

onomy. H

o

m

onetary pol

i

g

gregate de

m

g

gregate de

m

o

rary negat

i

a

nd and sup

p

e

en in the gr

a

n

negative a

g

g

gregate de

m

a

ble fluctuati

o

n

omy is curr

e

G

iven curre

n

i

cy that the

y

o

wever, bec

a

i

cymakers b

e

m

and curve

m

and curve

i

ve supply s

h

p

ly to demo

n

a

ph below,

w

g

gregate sup

p

m

and and su

p

o

ns in outpu

t

e

ntly in rece

s

n

t assumptio

y

anticipate

w

a

use of lags

i

e

come more

becomes fl

a

help stabili

z

h

ock? How

d

n

strate.

w

hen the ag

g

p

ly shock th

i

p

ply to demo

t

and inflati

o

sion at poin

t

ns about th

e

w

ill shift ag

g

i

n the polic

y

concerned

w

a

tter. How d

o

z

e inflation

w

d

oes this aff

e

g

regate dem

i

s implies th

a

o

nstrate how

o

n.

t

A in the gr

a

e

state of the

g

regate dem

a

y

process (w

h

w

ith inflatio

o

es the resu

l

w

hen the ec

o

fe

ct output?

U

m

and curve b

e

a

t the increa

s

lags in the

p

a

ph, and poli

economy,

p

a

nd out to A

h

ich were p

r

n stabilizati

o

l

ting chang

e

o

nomy is hit

U

se a graph

e

comes flat

t

se in inflati

o

p

olicy proce

s

cymakers w

i

p

olicymaker

s

D

A

and stab

i

r

esumably

o

n, the slop

e

e

in the slop

e

with a

of aggrega

t

t

er, then for

a

o

n is smaller

,

s

s can

i

sh to

s

i

lize

e

of

e

of

t

e

a

,

and

28.

M

an

y

thes

e

grap

h

Graf

t

that

g

t

r

n

e

e

a

u

a

u

m

i

o

i

o

a

y

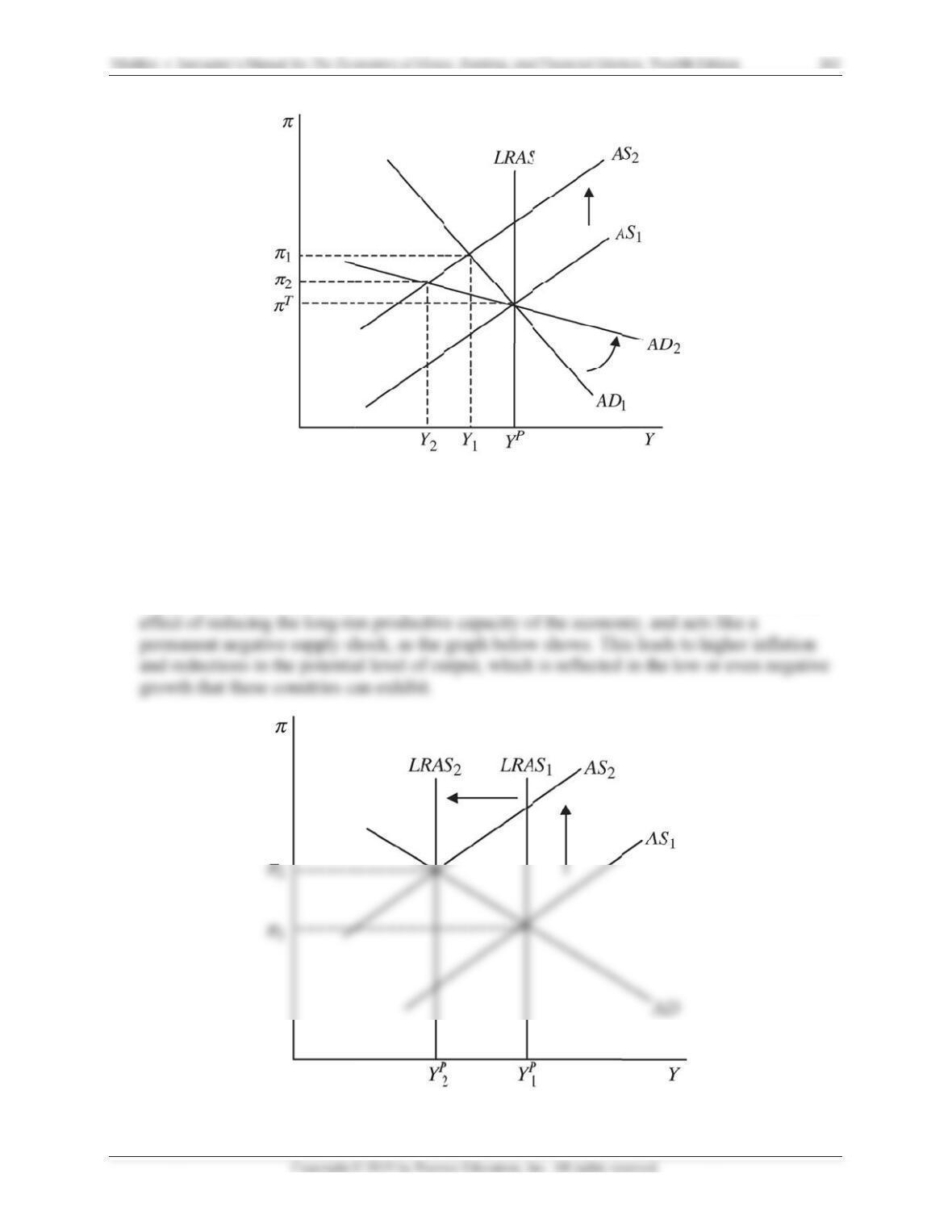

develo

p

in

g

e

countries’

e

h

of aggreg

a

t

and corrup

t

g

oods and s

e

g

countries s

u

e

conomies t

y

a

te demand

a

t

ion result i

n

e

rvices are p

r

u

ffer from e

n

y

pically hav

e

a

nd supply t

o

n

significant

r

ovided to c

o

n

demic cor

r

e

high inflat

i

o

demonstr

a

inefficienci

e

o

nsumers a

n

r

uption. Ho

w

ion and eco

n

a

te.

e

s in marke

t

n

d other fir

m

w

does this h

n

omic stagn

t

s, and parti

c

m

s. As a res

u

elp explain

w

ation? Use

a

c

ularly in th

e

u

lt, this has t

h

w

hy

a

e

way

h

e

29.

I

n 2

0

bega

n

defla

2002

addi

t

p

eri

o

p

ote

n

a.

H

a

P

s

p

b

a

v

v

o

c

e

.

e

b.

S

t

h

W

i

0

03, as the

U

n

to worry

a

tion. As a r

e

to 1% by m

t

ion, the Fe

d

o

d of time. T

h

n

tially inflat

i

H

ow might f

e

c

tually in a

r

olicymaker

s

p

iral, in whi

c

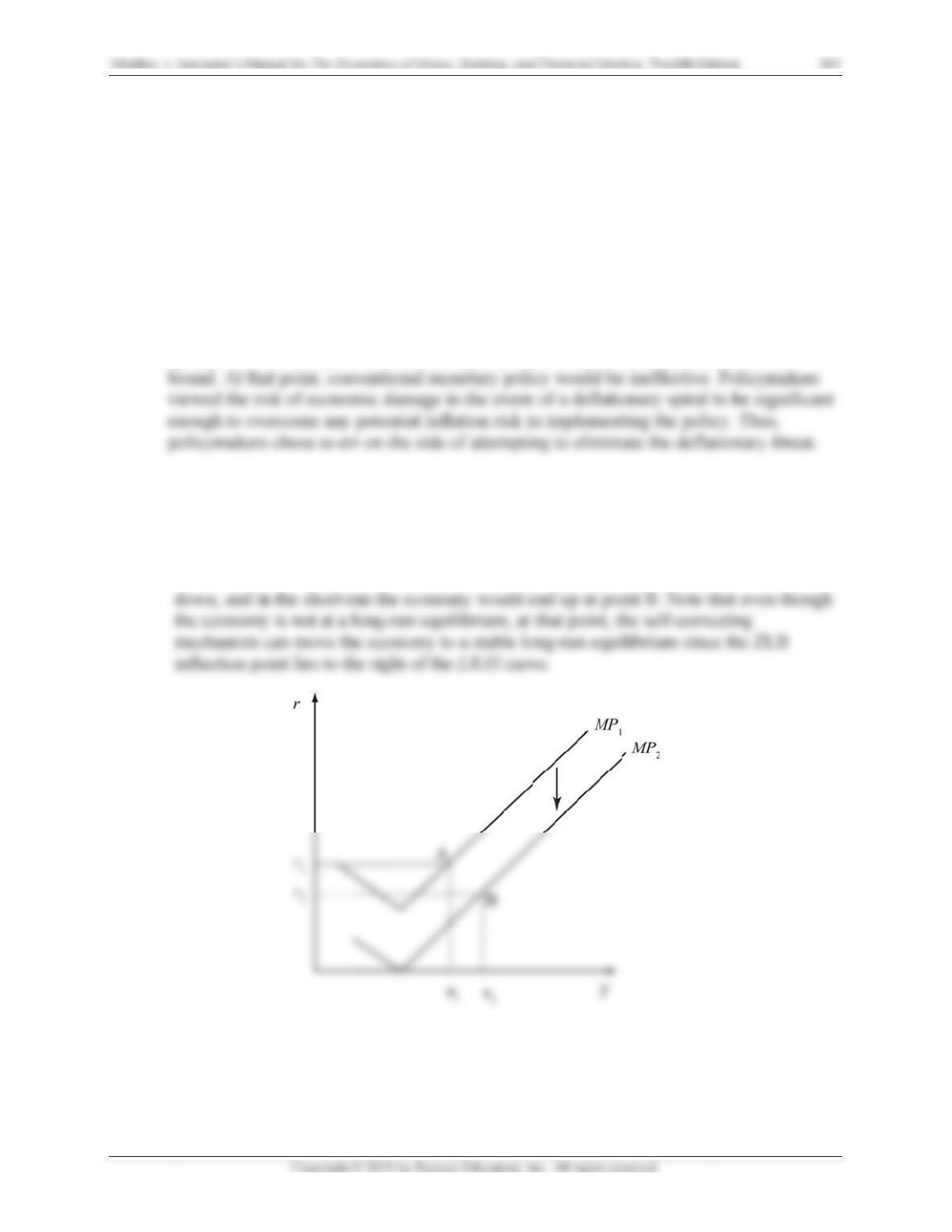

Sh

ow the im

p

h

e initial co

n

W

ith the ec

o

i

nto a desta

b

U

.S. econom

y

a

bout a “sof

t

e

sult, the Fe

d

id-2003, th

e

d

committed

h

is policy w

a

i

onary and

u

e

ars of a zer

o

r

ecession?

s

were worri

c

h the short

–

p

act of these

n

ditions in 2

o

nomy starti

n

b

ilizing defl

a

y

finally see

m

t

patch” in t

h

d

proactivel

y

e

lowest fede

t

o keeping t

h

a

s consider

e

u

nnecessary.

o

lower bou

n

ed that a sh

o

–

term nomi

n

policies on

003 and the

n

g out at po

i

a

tion. An au

t

m

ed poised

t

h

e economy,

y

lowered th

ral funds ra

t

h

e federal f

u

e

d highly ex

p

n

d justify su

c

o

ck could p

u

n

al policy ra

t

the MP cur

v

impact of t

h

i

nt A, an ad

v

t

onomous e

a

t

o exit its on

g

,

in particul

a

e federal fu

n

te on recor

d

u

nds rate at

t

p

ansionary

a

c

h a policy,

u

sh the econ

o

t

e would be

b

v

e and the A

D

h

e policy on

v

erse shock

a

sing of poli

g

oing reces

s

a

r the possi

b

n

ds rate fro

m

d

up to that

p

t

his level fo

r

a

nd was see

n

even if the

e

o

my into a

d

b

ound at th

e

D

/AS graph

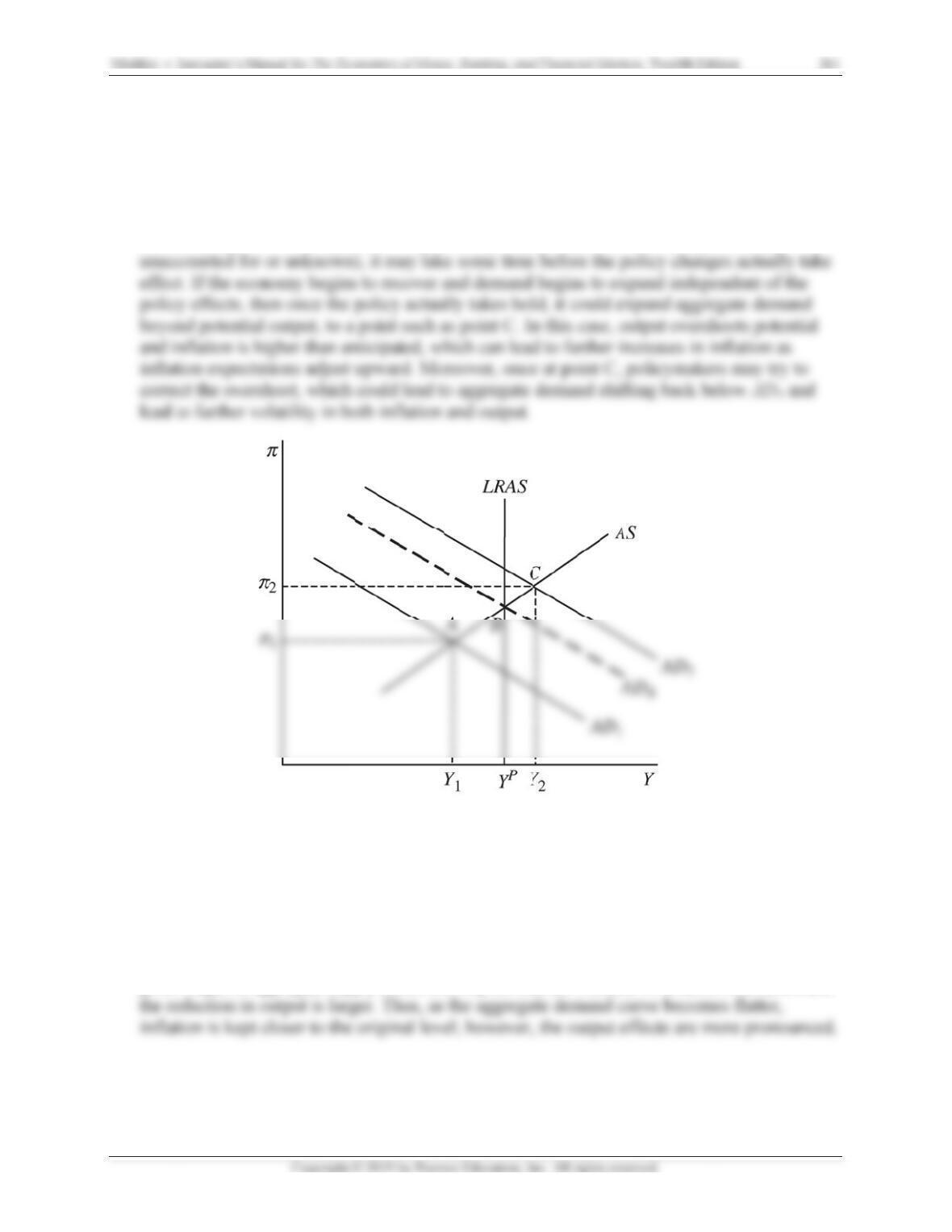

.

the deflatio

n

would push

cy would s

h

s

ion, the Fe

d

b

ility of a

m

1.75% in

l

p

oint in time

r

a consider

a

n

by some a

s

e

conomy wa

s

d

eflationary

e

zero lower

.

Be sure to

s

n

threat.

the econo

m

h

ift the MP

c

d

l

ate

. In

a

ble

s

s

not

s

how

m

y

c

urve

30.

Supp

a.

U

c

a

s

p

A

g

h

a

a

n

r

r

e

e

o

se that f is

U

sing an M

P

a

n pull the

e

p

iral.

A

financial p

a

i

ven inflati

o

determined

P

curve and

a

e

conomy bel

o

a

nic will in

c

o

n rate. A su

f

by two fact

o

a

n AS/AD g

r

o

w the zero

c

rease

f

, th

u

f

ficiently la

r

o

rs: financia

r

aph, show

h

lower boun

d

u

s raising th

e

r

ge panic wi

l

l panic and

h

ow a suffici

d

and into a

e

real intere

s

l

l push the

e

asset purch

a

ently large

f

destabilizin

g

s

t rate on in

v

e

conomy to

p

a

ses.

f

inancial pa

n

g

deflationa

v

estments a

t

p

oint B, wh

e

n

ic

ry

t

any

e

re

Mishkin •

b.

U

p

A

l

o

I

nstructor’s Ma

n

U

sing an M

P

u

rchases ca

n

A

sufficient

e

o

wer the rea

l

n

ual for The Ec

o

P

curve and

a

n

reverse th

e

e

nough asse

t

l

interest rat

e

o

nomics of Mon

e

a

n AS/AD g

r

e

effects of t

h

t

purchase

w

e

on invest

m

e

y, Banking, an

d

r

aph, show

h

h

e financial

w

ill lower

f

,

m

ents at any

d

Financial Mar

k

h

ow a suffici

panic depi

c

,

reversing t

h

given inflat

i

k

ets, Twelfth E

d

ent amount

o

c

ted in part

(

h

e effects o

f

i

on rate. Th

i

d

ition

o

f asset

(

a).

f

the panic,

a

i

s moves the

265

a

nd

Mishkin •

ANSW

E

1. On J

a

goal

s

infla

t

cons

u

statu

t

nor

m

of un

data

b

the u

n

p

rod

u

setti

n

f

req

u

a.

F

u

s

i

n

b.

F

u

s

e

a

e

o

e

o

t

n

t

l

t

a

l

a

a

a

I

nstructor’s Ma

n

E

RS TO D

A

a

nuary 19,

2

s

and monet

a

t

ion at the r

a

u

mption exp

e

t

ory manda

t

m

al rate of u

n

employmen

t

b

ase, and fi

n

n

employme

n

u

ct (GDPP

O

n

g to “Perc

e

u

ency settin

g

F

or the most

s

ing the 2%

n

flation gap

s

F

or the most

s

ing the G

D

n

ual for The Ec

o

A

TA ANAL

Y

2

017, the Fe

d

a

ry policy s

t

a

te of 2%, a

s

e

nditures, i

s

t

e.” and tha

t

n

employmen

t

is believed

n

d data on t

h

n

t rate (UN

R

O

T), an esti

m

e

nt Change

F

g

to ‘Quarte

r

recent four

q

target refer

s

over the fo

recent fou

r

q

D

P measure

a

o

nomics of Mon

e

Y

SIS PRO

B

d

eral Reser

v

t

rategy. It s

t

s

measured

b

s

most consi

s

t

“the media

t was 4.8%.

to be 4.8%.

h

e personal

c

R

ATE), real

G

m

ate of pote

n

F

rom Year

A

r

ly’. Downl

o

q

uarters of

d

enced by th

e

ur quarters.

q

uarters of

d

a

nd the pote

n

e

y, Banking, an

d

B

LEMS

v

e released

i

t

ated: “The

C

b

y the annu

a

s

tent over th

n of FOMC

p

” Assume th

Go to the S

t

c

onsumptio

n

G

DP (GDP

C

n

tial GDP.

F

A

go.” For th

e

o

ad the data

d

ata availa

b

e

Fed. Calc

u

d

ata availa

b

n

tial GDP e

s

d

Financial Mar

k

i

ts amended

C

ommittee

r

a

l change in

e longer ru

n

participant

s

h

is statemen

t

t

. Louis Fed

e

n

expenditur

e

C

1), and

r

e

a

F

or the pric

e

e

unemploy

m

into a s

p

re

a

b

le, calculat

e

u

late this va

l

b

le, calculat

e

e

stimate. Ca

l

k

ets, Twelfth E

d

statement o

r

eaffirms its

j

the price in

d

n

with the F

e

s

’ estimates

t

implies tha

e

ral Reserv

e

e price inde

x

a

l potential

g

e

index, adj

u

m

ent rate, a

d

a

dsheet.

e

the avera

g

l

ue as the a

v

e

the avera

g

l

culate the

g

d

ition

n longe

r

-ru

n

j

udgment t

h

d

e

x

for pers

e

deral Rese

r

of the longe

r

t the natura

l

e

FRED

x

(PCECTP

I

g

ross domes

t

u

st the units

d

just the

g

e inflation

g

v

erage of th

e

g

e output ga

p

g

ap as the

266

n

h

at

onal

r

ve’s

r

-run

l

rate

I

),

t

ic

g

ap

e

p

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 267

a. From 2016:Q2: 2017:Q1, the average inflation gap was –0.5%.

b. From 2016:Q2: 2017:Q1, the average output gap was –0.76%

c. From 2016:Q2: 2017:Q1, the average unemployment gap was 0.0%. Yes, the divine

coincidence applies based on the current data. Expansionary policy would close a

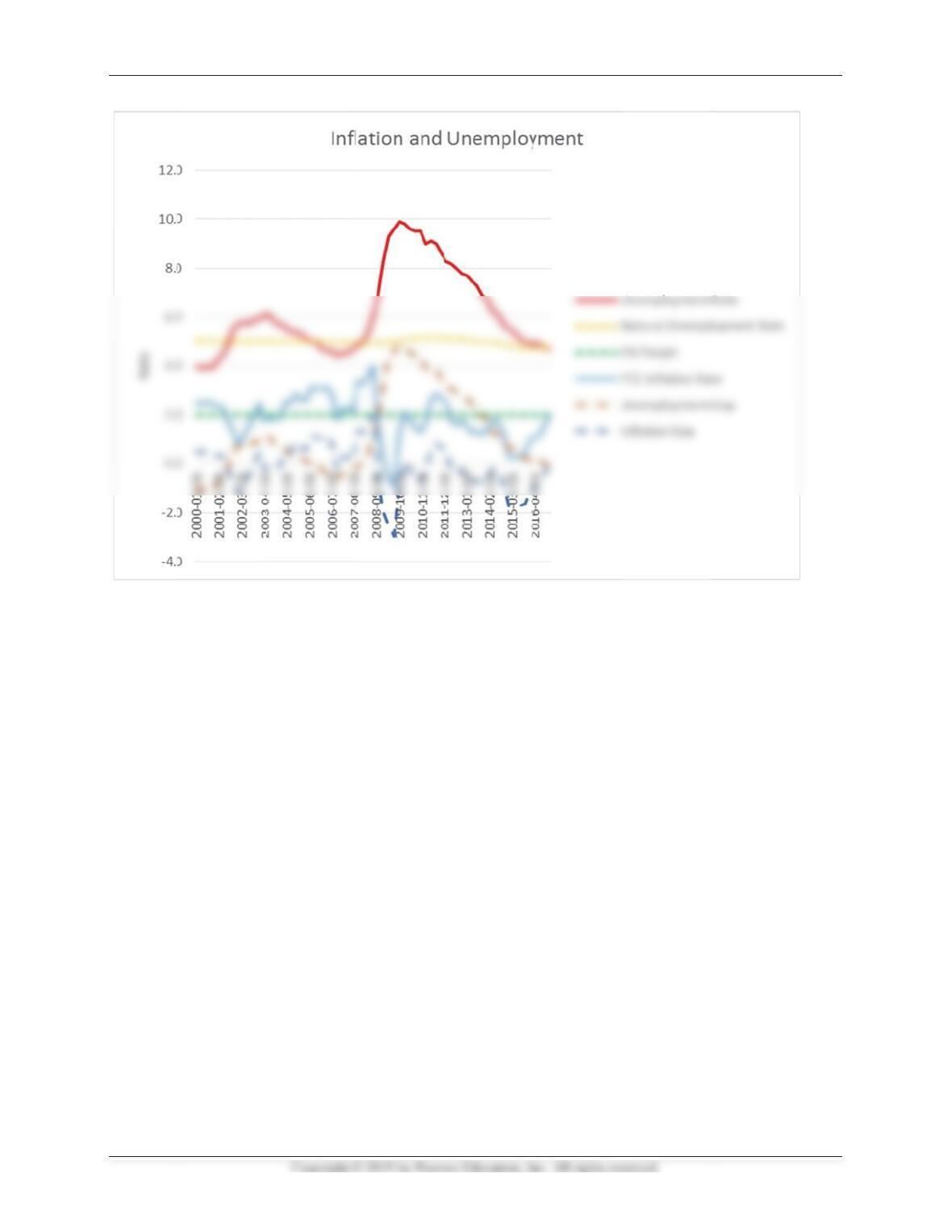

2. Go to the St. Louis Federal Reserve FRED database and find data on the personal

consumption expenditure price index (PCECTPI), the unemployment rate (UNRATE), and an

estimate of the natural rate of unemployment (NROU). For the price index, adjust the units

setting to “Percent Change From Year Ago.” For the unemployment rate, adjust the

frequency setting to ‘Quarterly’. Select the data from 2000 through the most current data

available, download the data, and plot all three variables on the same graph. Using your

graph, identify periods of demand-pull or cost-push movements in the inflation rate. Briefly

explain your reasoning.

See graph below. The period from around early 2001 to around the end of 2003 appears to be

influenced by demand-pull inflation conditions, since inflation is a bit lower than what

appears to be normal at the time (2.5%), and the unemployment rate rises and remains above

Mishkin •

I

nstructor’s Ma

n

n

ual for The Ec

o

o

nomics of Mon

e

f

e

y, Banking, an

d

d

Financial Mar

k

k

ets, Twelfth E

d

d

ition 268

f