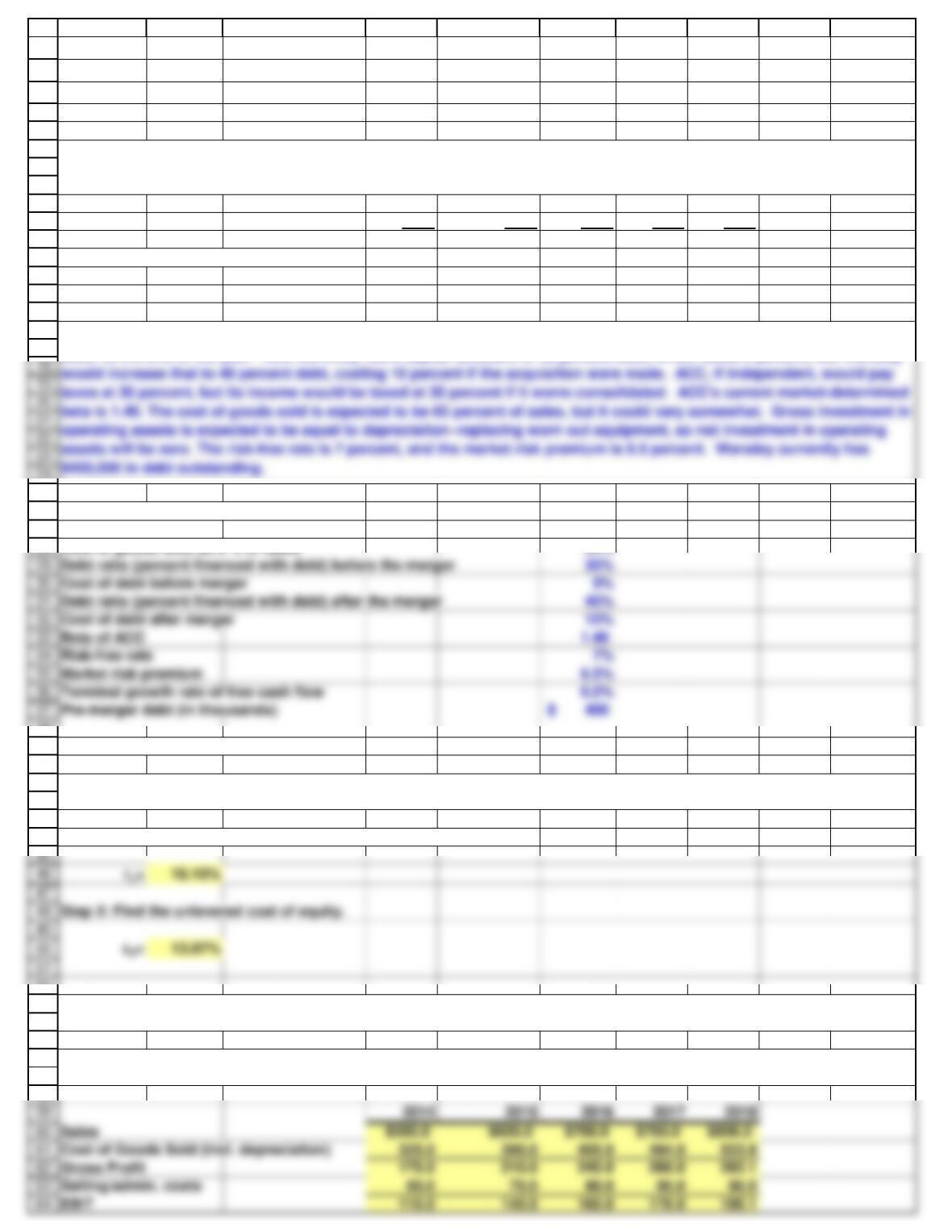

Debt ratio (percent financed with debt) before the merger 30%

Cost of debt before merger 9%

Debt ratio (percent financed with debt) after the merger 40%

Cost of debt after merger 10%

Beta of ACC 1.40

Risk-free rate 7%

Market risk premium 6.5%

Terminal growth rate of free cash flow 6.0%

Pre-merger debt (in thousands) 400$

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

24

25

26

27

28

38

39

40

41

42

43

44

52

53

54

55

56

57

58

Cost of Goods Sold (incl. depreciation) 325.0 390.0 455.0 494.0 523.9

Gross Profit 175.0 210.0 245.0 266.0 282.1

Selling/admin. costs 60.0 70.0 80.0 90.0 96.0

A B C D E F G H I J

Solution 12/8/2012

Chapter: 22

Problem: 7

2014 2015 2016 2017 2018

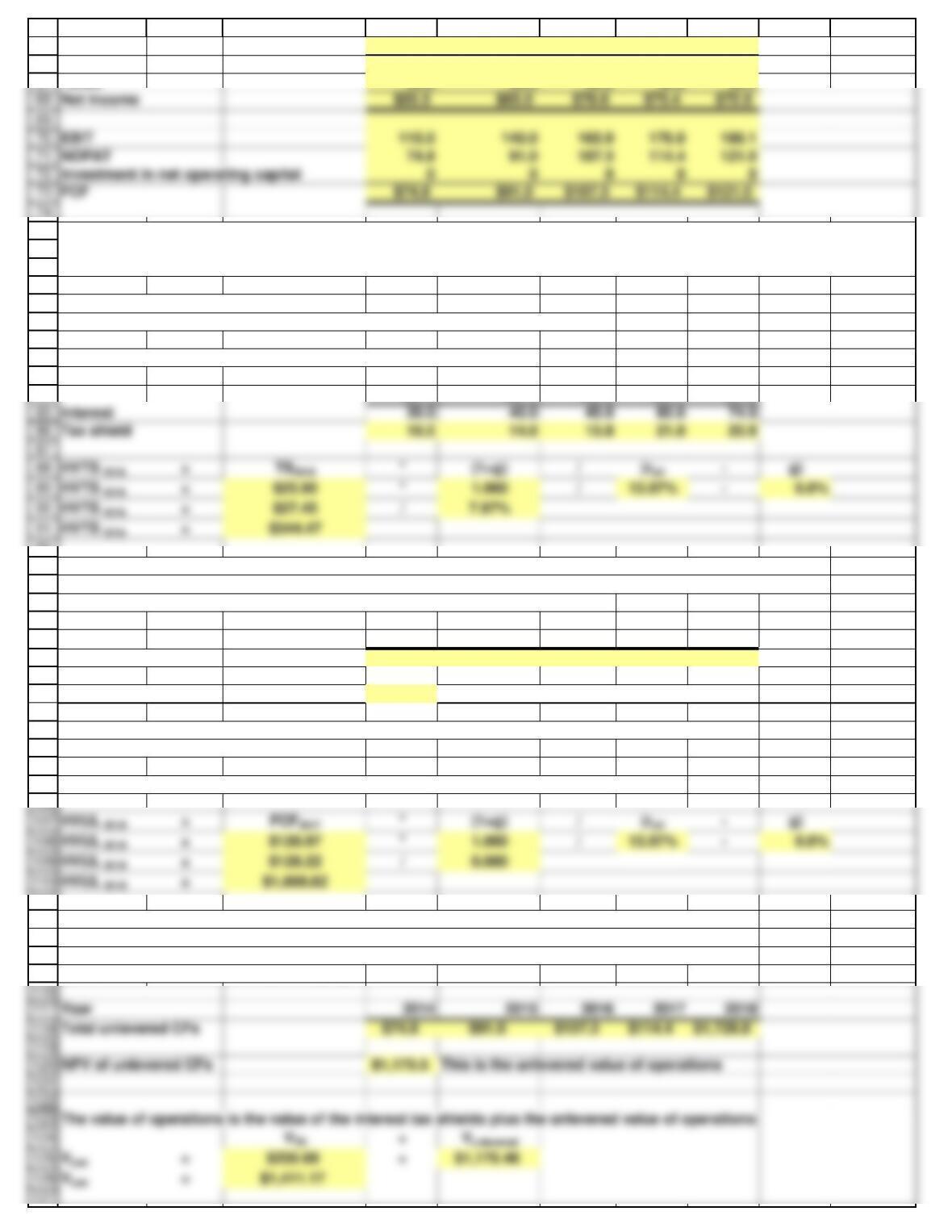

Net sales $500 $600 $700 $760 $806

Selling and administrative expense 60 70 80 90 96

Interest 30 40 45 60 74

Tax rate of ACC before the merger 30%

Tax rate after merger 35%

Cost of goods sold as a % of sales 65%

a. What is the unlevered cost of equity?

Step 1: Find the levered cost of equity at old capital structure.

Before we can proceed with this problem, we must generate pro forma income statements for ACC’s operations after the

proposed merger so we can calculate free cash flow and interest tax shields.

Wansley Portal Inc., a large Internet service provider, is evaluating the possible acquisition of Alabama Connections

Company (ACC), a regional Internet service provider. Wansley‘s analysts project the following post merger data for ACC

(in thousands of dollars):

If the acquisition is made, it will occur on January 1, 2014. All cash flows shown in the income statements are assumed to

occur at the end of the year. ACC currently has a capital structure of 30 percent debt, which costs 9 percent, but Wansley

The unlevered cost of equity should be used to discount the FCFs, tax shields and horizon value.

b. What is the horizon value of the tax shields and the unlevered operations? What is the value of ACC’s operations and

the value of ACC’s equity to Wansley’s shareholders?

65

66

67

75

76

77

78

79

80

81

82

83

84

Interest 30.0 40.0 45.0 60.0 74.0

Tax shield 10.5 14.0 15.8 21.0 25.9

92

93

94

95

96

97

Total unlevered CFs $74.8 $91.0 $107.3 $114.4 $1,729.8

NPV of unlevered CFs $1,175.5 This is the unlevered value of operations

The value of operations is the value of the interest tax shields plus the unlevered value of operations

98

99

100

101

102

103

104

105

106

111

112

113

114

115

A B C D E F G H I J

Interest 30.0 40.0 45.0 60.0 74.0

EBT 85.0 100.0 120.0 116.0 112.1

Taxes 29.8 35.0 42.0 40.6 39.2

We must determine the tax shields.

From this point, we can derive horizon value from the basic DCF framework.

The tax shield is the interest multiplied by the post-merger tax rate.

2014 2015 2016 2017 2018

To calculate the value of the tax shields add the horizon value of the tax shields to the 2018 tax shield

to get the total tax shield cash flow in 2018. In the other years the total TS cash flow is just the annual TS

Then find the NPV of this stream of tax shields at the unlevered cost of equity.

2014 2015 2016 2017 2018

Total TS Cash Flows 10.5 14.0 15.8 21.0 $370.37

NPV of TS Cash Flows $235.69 This is the value of all of the tax shields.

To calculate the unlevered value of operations you need the unlevered horizon value and the

the annual free cash flows.

To calculate the unlevered horizon value, we just need the free cash flow for 2014

To calculate the unlevered value of operations, add the unlevered horizon value to the free cash flow

in 2018 to get the total unlevered cash flow in 2018. In the other years the unlevered cash flow is

just the annual free cash flow. The unlevered value of operations is the NPV of the unlevered

cash flows at the unlevered cost of equity.

* In this scenario, we state that investment in net operating capital is zero. This arises from the fact that the only needed

investments are those needed to replace worn out capital, and that they equal depreciation.

68

73

EBIT 115.0 140.0 165.0 176.0 186.1

NOPAT 74.8 91.0 107.3 114.4 121.0

Investment in net operating capital 0 0 0 0 0

128

129

130

131

A B C D E F G H I J

To find the value of ACC to Wansley’s shareholders take the value of operations, add in any non-operating

assets (there are non for ACC) and subtract off the debt.