Basic Econometrics, Gujarati and Porter

227

CHAPTER 22:

TIME SERIES ECONOMETRICS: FORECASTING

22.1 As discussed in Sec. 22.1, broadly speaking there are five

22.2 Simultaneous-equation (SE) economic forecasting is based on a

system of equations (composed of at least two variables but usually

many more) that explain some economic phenomena on the basis of

22.4 Since the B-J method explicitly assumes that the underlying time

22.5 The B-J approach to forecasting is based on analyzing the

probabilistic properties of a single time series without relying on

22.6 It is a-theoretic because it uses less prior information than a SE

22.7 As we discussed in Exercise 22.1, there are five methods of

22.8 We want lags long enough to fully capture the dynamics of the

system being modeled. On the other hand, the longer the lags, the

228

22.9 See the answers to Exercises 22.2 and 22.6.

22.10 Operationally, the two procedures are similar. The difference comes

in the purpose of research. In Granger causality our objective is to

Empirical Exercises

22.11 The steps involved are as follows:

(1) Examine the series for stationarity. We have already seen that

(2) Examine the autocorrelation function (ACF) and the partial

(3) Having chosen an appropriate ARMA model, the next task is to

estimate it and examine the residuals of the estimated model. If

The regression results for the AR(4) model were as follows:

ln DPI

*

=0.0098 −0.1412 ln DPI

*

Basic Econometrics, Gujarati and Porter

229

22.12

Follow Exercise 22.11 and try the models MA(2), MA(6), AR(2)

22.13

Follow Exercise 22.11 and try the models MA(1) and AR(1), again

22.15

According to the Schwarz criterion, choose the model

that has the lowest value of Schwarz statistic. The same also

22.16

On the basis of the Schwarz criterion, it was determined that a

VAR model with 3 lags of log DPI and log PCE might suffice.

The regression results are as follows:

Dependent variable

→

log PCE log DPI

Explanatory Variables

↓

Intercept 0.0042 0.0319

(0.52

) (3.24)

Basic Econometrics, Gujarati and Porter

230

Based on this model, the actual and forecast values of the two

variables for 2007:1 to 2007:4 are as follows:

Q Actual log PCE Fcst log PCE Actual log DPI Fcst log DPI

2007:1 9.0138 9.0117 9.0623 9.0569

22.20

Although the model did not specifically test for causality, we can

get some idea about it from the reported F statistic. For the variable

22.21

For the application of the VAR methodology all the variables

entering into the model must be (jointly stationary). Perhaps in the

22.22

In the level form, M1 is nonstationary on the basis of the DF test

in its various forms. The same is true about R.

231

22.23

The regression results are as follows:

Variable Coefficient Std. Error t-Statistic

C -7.8618 1.2807 -6.1385

(b) To see if the ARCH effect is present, we obtained residuals (

ˆ

t

u

)

from the regression given in (a) and obtained the following

ARCH (1) regression:

22.24

The model given here is the restricted version of the model

232

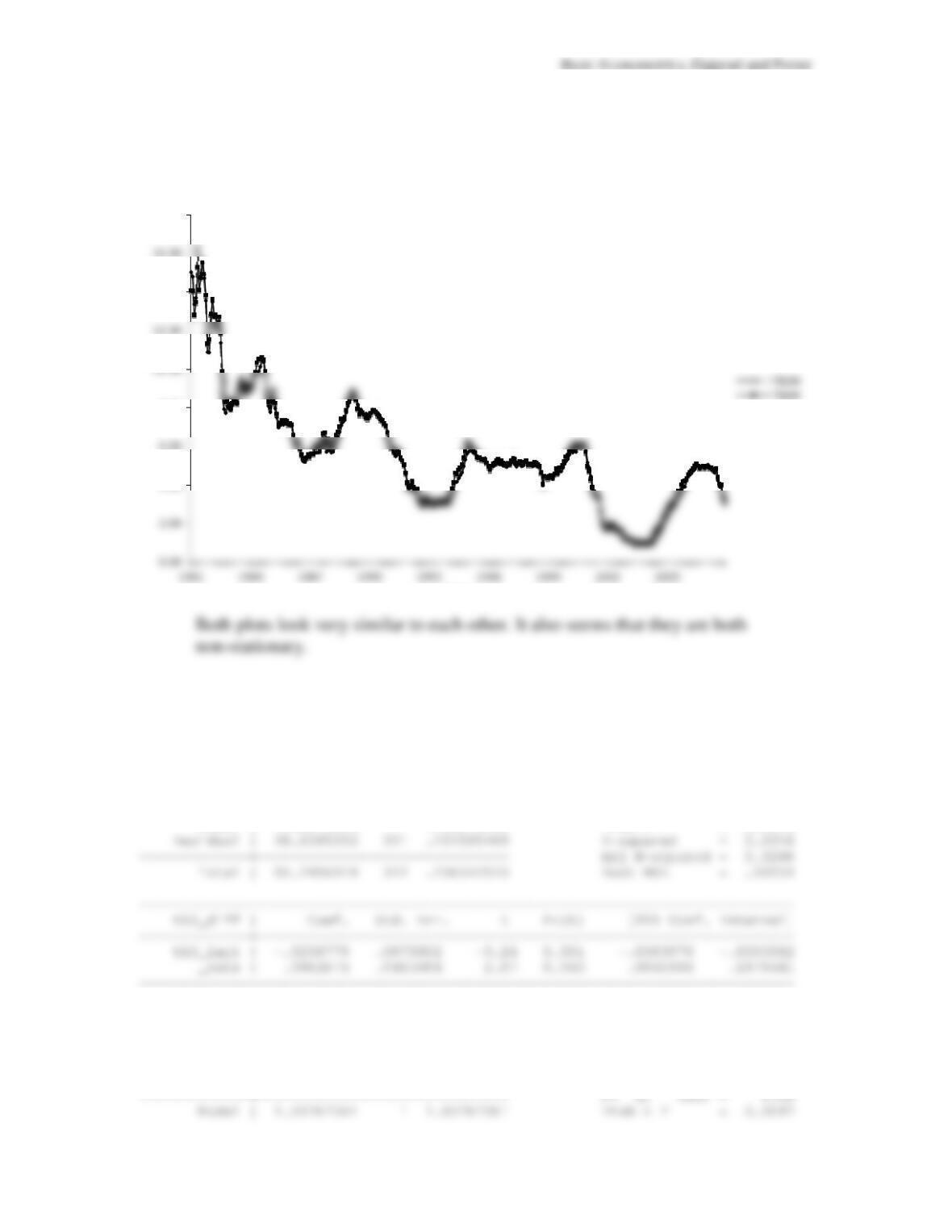

22.25

(a) Time series plot for the two series is:

(b) To perform the unit root test, we regressed the first differences

on the lagged series with the following results:

3-month Treasury Bills:

Source | SS df MS Number of obs = 323

————-+—————————— F( 1, 321) = 10.47

Model | 1.58675694 1 1.58675694 Prob > F = 0.0013

6-month Treasury Bills:

Source | SS df MS Number of obs = 323

3 and 6 Month Treasury Bills

4.00

8.00

14.00

18.00

Year

Basic Econometrics, Gujarati and Porter

Residual | 41.1815604 321 .128291465 R-squared = 0.0246

The tau statistic cutoffs for the 5% and 1% levels are around -2.88 and –

(c) To test if the two series are cointegrated, we will use the Engle-

Granger Test. First we estimate the residuals of the regression of 3-month

bills on 6-month bills:

Source | SS df MS Number of obs = 324

————-+—————————— F( 1, 322) =62428.06

Model | 2775.41205 1 2775.41205 Prob > F = 0.0000

and we saved the residuals from this regression. Now the regression of the

differenced residuals on the lagged residuals is as follows:

Source | SS df MS Number of obs = 323

————-+—————————— F( 1, 321) = 45.56

Model | .607086075 1 .607086075 Prob > F = 0.0000

The t statistic for the slope from this regression is -6.75, which is certainly

in the rejection region. Therefore, the residuals from this regression are

234

22.26

This is a class exercise.

22.27

This is a class exercise.