Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

20

21

22

23

24

25

33

34

35

36

37

38

46

47

48

49

50

56

57

58

59

60

61

62

63

64

65

66

71

72

73

74

75

76

A B C D E F G H I J K

12/10/2012

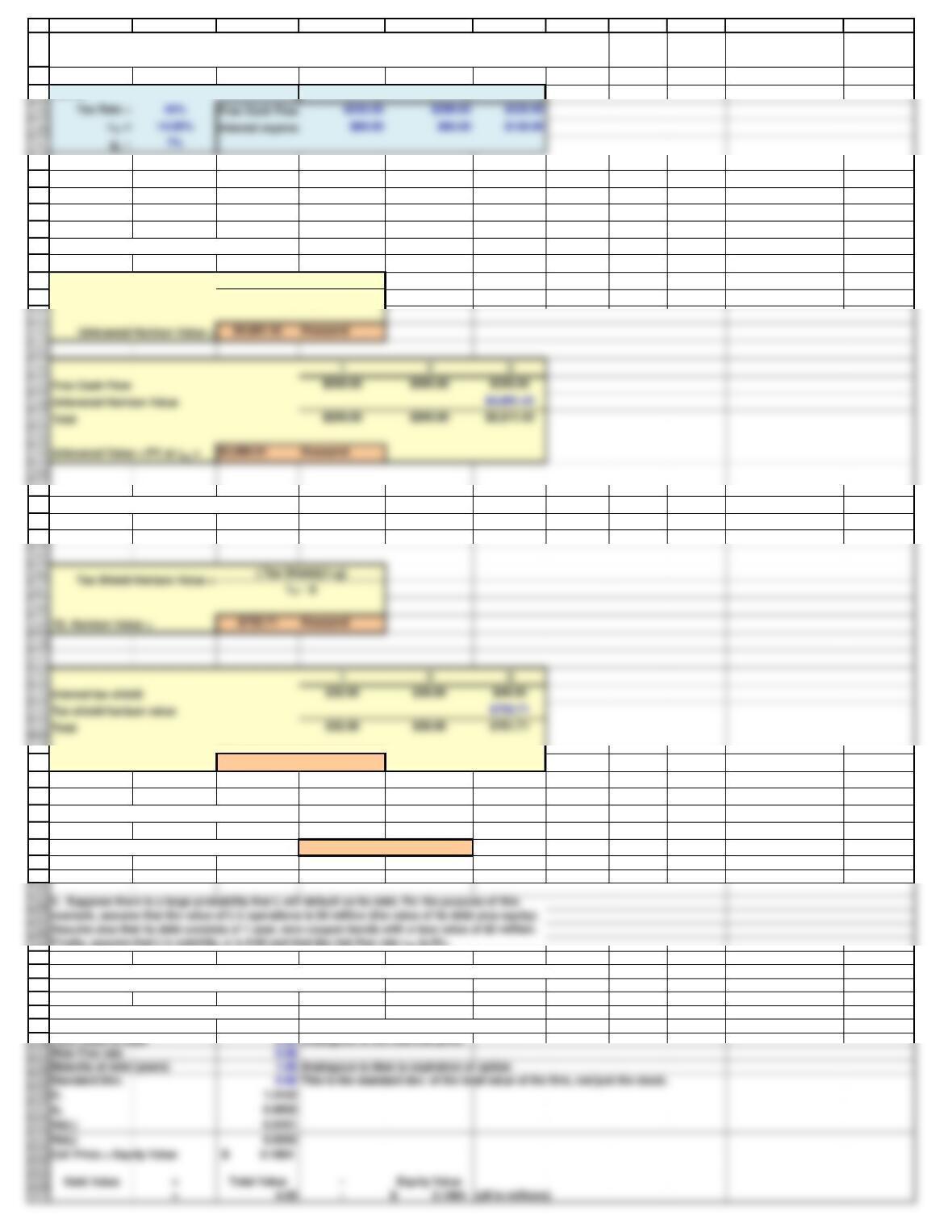

Situation

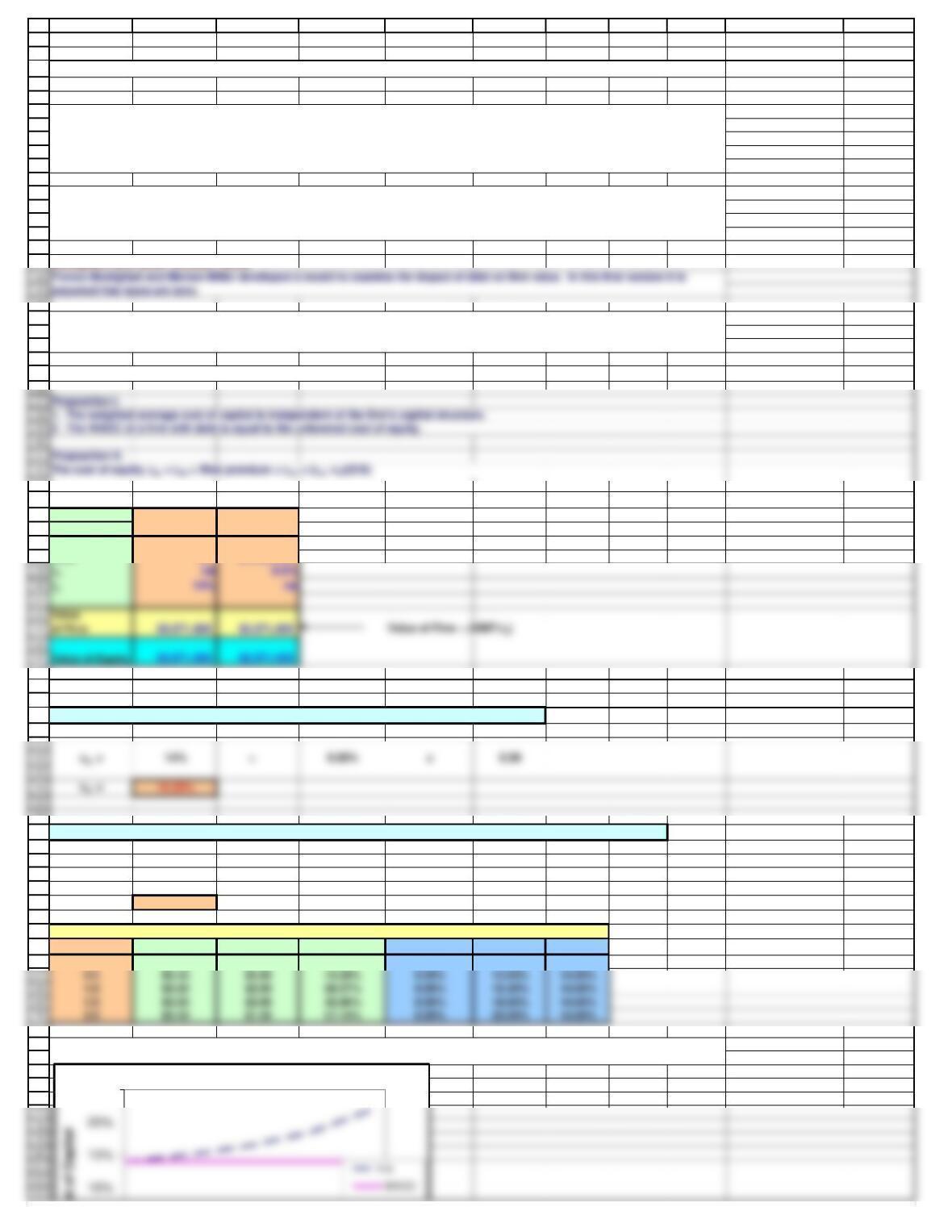

Modigliani and Miller without Taxes

Input Data Firm U Firm L

No Debt Some Debt

EBIT $500,000 $500,000

Debt $0 $1,000,000

rsL = rsU + (rsU-rd)x (D/S)

WACC =

wd*rd + wce*rs = (D/V)*rd + (S/V)*rs

WACC = 2.24% + 11.8%

WACC = 14.00%

MM without Taxes

D V S D/V

rdrsWACC

0.0 $3.50 $3.50 0.00% 8.00% 14.00% 14.00%

Chapter 21. Mini Case

David Lyons, the CEO of Lyons Solar Technologies, is concerned about his firm's level of debt financing. The company uses short-

term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar

technology companies average about 30 percent debt, and Mr. Lyons wonders why the difference occurs, and what its effects are

on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant.

a. Business Week recently ran an article on companies' debt policies, and the names Modigliani and Miller (MM) were mentioned

several times as leading researchers on the theory of capital structure. Briefly, who are MM, and what assumptions are embedded

in the MM and Miller models? Answer: See Chapter 21 Mini Case Show

(2.) Graph (a) the relationships between capital costs and leverage as measured by D/V, and (b) the relationship between value

and D.

1. Assume that Firms U and L are in the same risk class, and that both have EBIT = $500,000. Firm U uses no debt financing, and

its cost of equity is rsU = 14%. Firm L has $1 million of debt outstanding at a cost of rd = 8%. There are no taxes. Assume that the

MM assumptions hold, and then:

a. Find V, S, rs, and WACC for Firms U and L.

25%

Cost of Capital

Without Taxes

rd

84

85

91

92

93

94

95

96

97

98

106

107

108

109

110

118

119

120

121

122

123

124

125

126

127

128

129

137

138

139

140

141

142

143

144

155

156

157

158

159

A B C D E F G H I J K

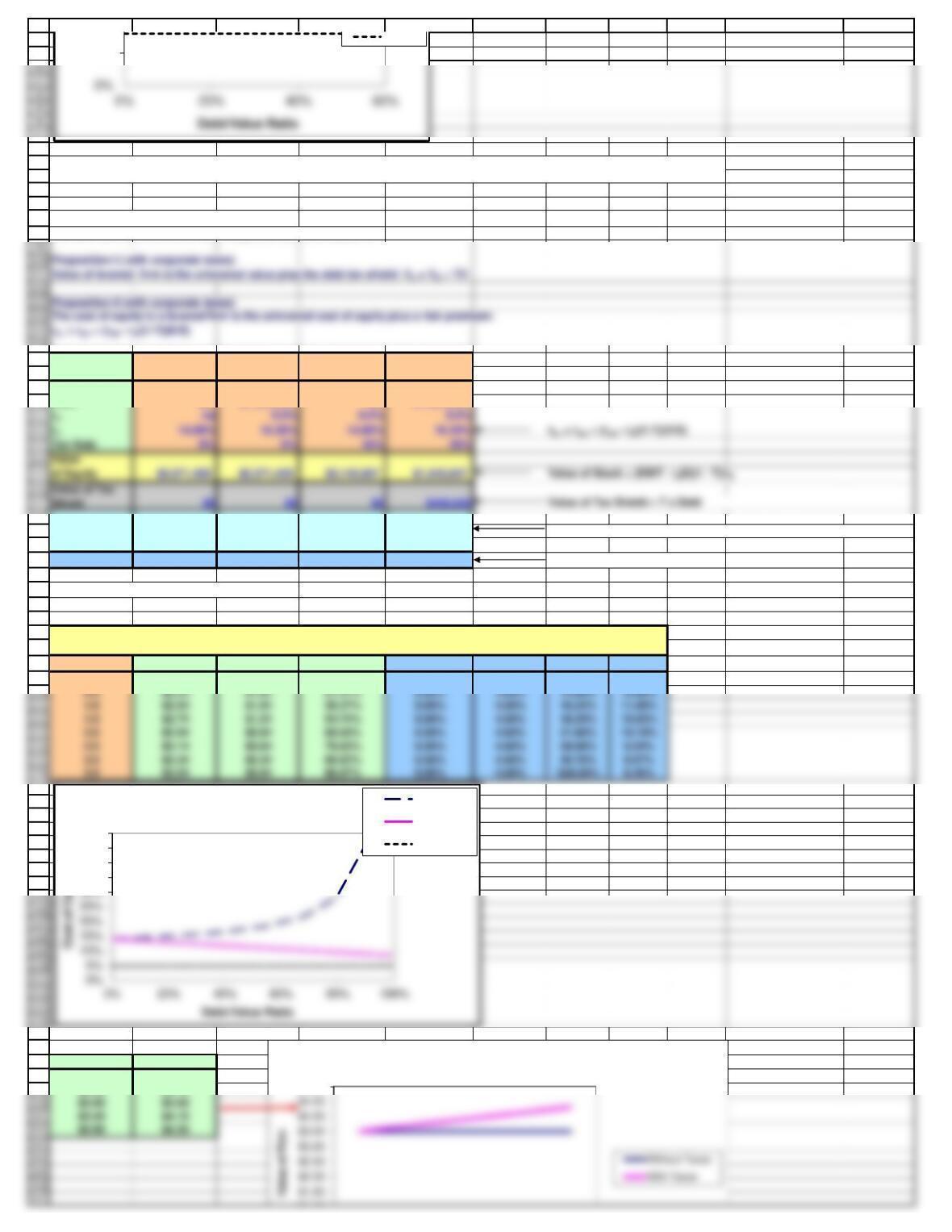

Modigliani and Miller with CorporateTaxes

The MM results are different once corporate taxes are added in.

Firm U Firm L 40% Tax Rate 40% Tax Rate

Input Data No Debt Some Debt No Debt Some Debt

EBIT $500,000 $500,000 $500,000 $500,000

Debt $0 $1,000,000 $0 $1,000,000

WACC 14.00% 14.00% 14.00% 11.80%

Effects of Leverage: MM Models

MM with Corporate Taxes

Tc = 40.00%

DV S D/V

rdrd x (1-T) rsWACC

0.0 $2.14 $2.14 0.00% 8.00% 4.80% 14.00% 14.00%

V-No Taxes V-Taxes

$3.50 $3.50

$3.50 $3.70

c. Using the data given in Part b, but now assuming that Firms L and U are both subject to a 40 percent corporate tax rate, repeat

the analysis called for in b(1) and b(2) under the MM with-tax model.

WACC = (D/V)rd(1-T) + (S/V)rs

$3,571,429

Value of Firm = Value of Unlevered Firm +T x Debt

$2,142,857

$2,542,857

Total Market

Value of Firm

$3,571,429

5%

10%

Cost of Capital

rd

35%

40%

45%

50%

With Taxes rs

WACC

rd x (1-T)

$5.00

Relationship Between Value and Debt

168

169

170

171

172

173

174

175

176

177

178

179

187

188

189

190

191

192

193

194

195

196

213

214

215

216

217

218

219

220

221

222

223

236

237

238

239

240

241

242

243

244

245

246

A B C D E F G H I J K

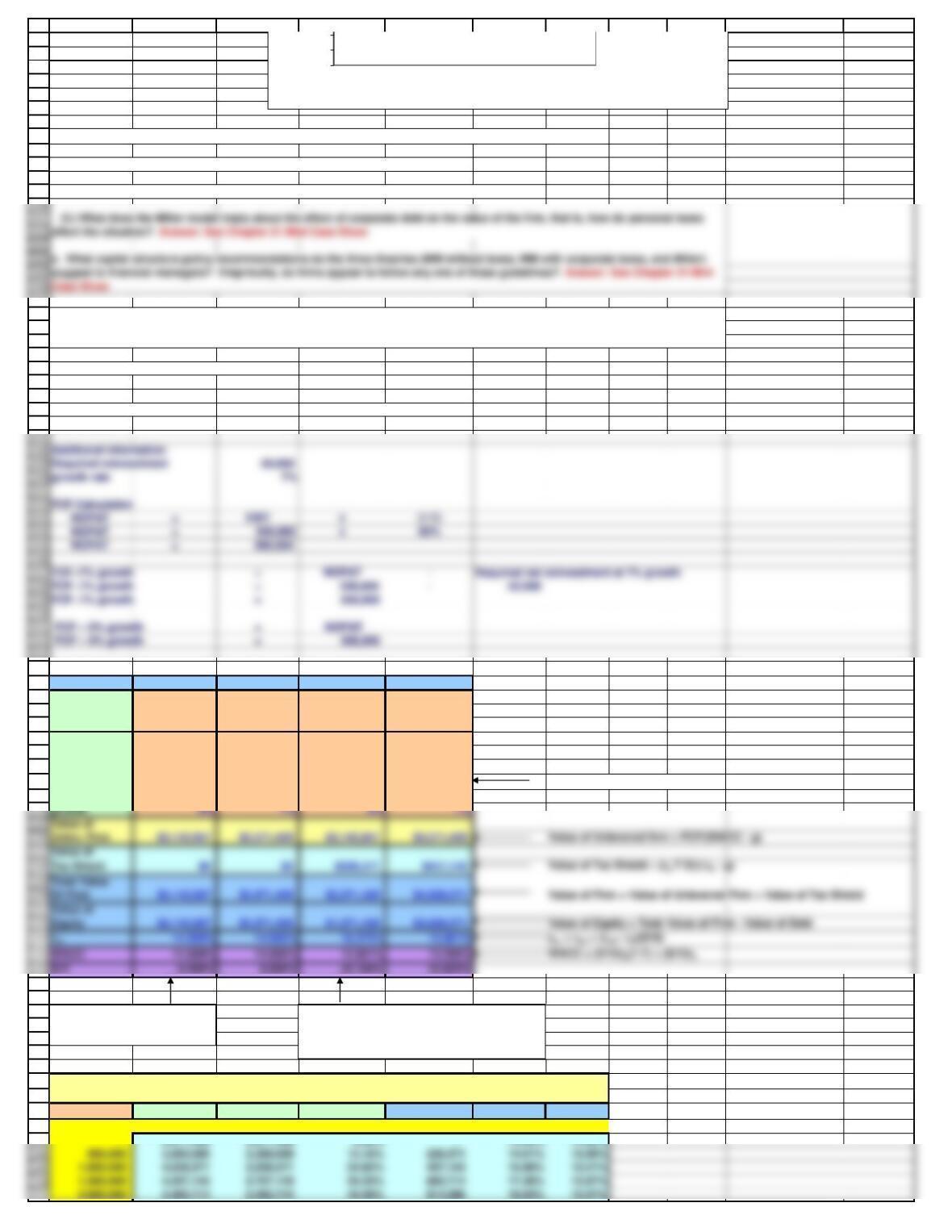

Relevant information from part c.

EBIT

500,000

Tax rate

40%

Unlevered cost of equity

14% = WACC if there is no debt

Cost of debt

8%

Firm U Firm U Firm L Firm L

Data for 40% Tax Rate 40% Tax Rate 40% Tax Rate 40% Tax Rate

Lyons zero Debt zero Debt some Debt some Debt

and no growth and 7% growth and no growth and 7% growth

exp. FCF 300,000$ 250,000$ 300,000$ 250,000$

Debt -$ -$ 1,000,000$ 1,000,000$

rd8.0% 8.0% 8.0% 8.0%

rsU 14.00% 14.00% 14.00% 14.00%

WACC = rsU if the firm is unlevered

Tax Rate 40% 40% 40% 40%

APV with growth: rTS = rsU.growth = 7.00%

T = 40.00%

DV S D/V Tax shield

rsL WACC

$4,028,571 $3,028,571 24.823% $457,143 15.981% 13.206%

This column will NOT be the same as the "40%

tax rate, some debt" column from part c

because we are discounting the tax shield at

rsU instead of rd.

This column is the same as the

"40% tax rate no debt" column

from part c.

f. Suppose that Firms U and L are growing at a constant rate of 7% and that the investment in net operating assets required to

support this growth is 10% of EBIT. Use the compressed adjusted present value (APV) model to estimate the value of U and L. Also

estimate the levered cost of equity and the weighted average cost of capital.

d. Now suppose investors are subject to the following tax rates: Td = 30% and Ts = 12%.

(1.) What is the gain from leverage according to the Miller model?

(2.) How does this gain compare to the gain in the MM model with corporate taxes?

$0.00

$0.50

$1.00

Debt

255

256

257

258

259

260

261

262

263

264

273

274

275

276

277

278

279

280

288

289

290

291

292

293

298

299

300

301

302

310

311

312

313

314

315

316

317

329

330

331

332

333

334

335

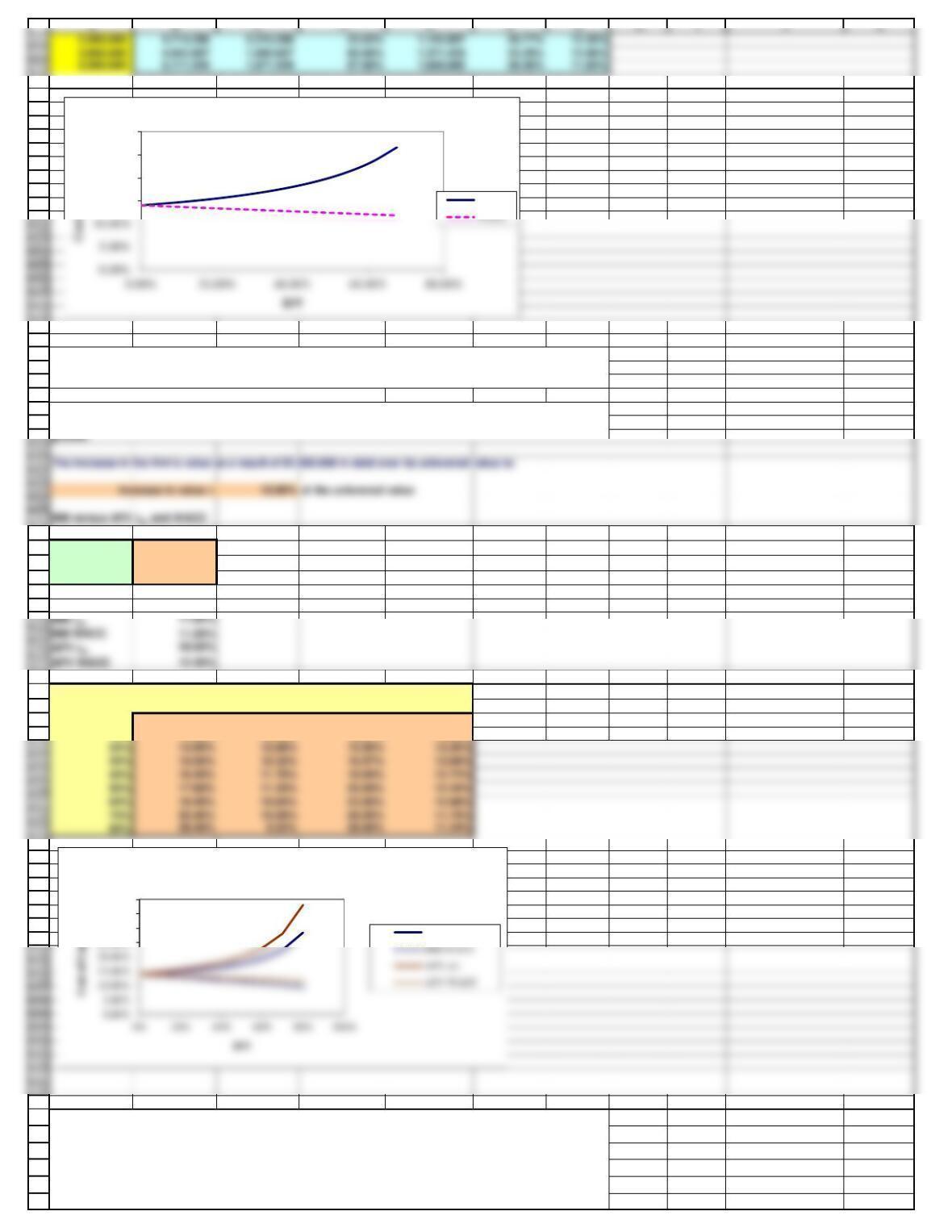

Things to note:

2. The gain from debt is larger with growth than without growth.

rd8.0%

rsU 14.00%

Tax Rate 40%

D/V

50%

D/S 1

MM rsL MM WACC APV rsL APV WACC

D/V 17.60% 11.20% 20.00% 12.40%

0%

14.00% 14.00% 14.00% 14.00%

10%

14.40% 13.44% 14.67% 13.68%

1. The gain from the tax shield will be lower using the APV model than under MM because the APV model

discounts the interest tax shield at the unlevered cost of equity, which is larger than the cost of debt. The

MM model discounts the tax shield at the cost of debt.

3. The value of the firm, whether levered or not, will be larger with growth, provided ROIC is greater than

WACC. Although we don't show it here, ROIC is greater than WACC, so the value of the firm increases with

g. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to grow faster than 7%

during the next 3 years: FCF2 = $290,000 and FCF3 = $320,000, after which it will grow at a constant rate of

7%. The expected interest expense at Year 1 is $80,000, but it is expected to grow over the next couple of

years before the capital structure becomes constant: Interest expense at Year 2 will be $95,000, at Year 3 it

will be $120,000 and it will grow at 7% thereafter. What is the estimated horizon unlevered value of

operations (i.e., the value at Year 3 immediately after the FCF at Year 3)? What is the current unlevered value

of operations? What is the horizon value of the tax shield at Year 3? What is the current value of the tax

shield? What is the current total value? The tax rate and unlevered cost of equity remain at 40% and 14%,

respectively.

15.00%

20.00%

25.00%

30.00%

Cost of Capital with growth

rsL

25.00%

30.00%

35.00%

40.00%

Costs of capital for MM and APV

MM rsL

336

337

338

342

343

344

345

346

347

348

349

350

361

362

363

364

376

377

378

379

380

381

382

383

384

389

390

391

392

393

394

395

A B C D E F G H I J K

Inputs: 1 2 3

Estimate the unlevered value of operations

Estimate the value of the tax shield

Tax Shield Value = PV at rsU = $584.94 thousand

Estimate the total value of operations

Vops = Tax shield value + Unlevered value = $4,544.95 thousand

If L's debt is risky, then its equity is like a call option and can be valued with the Black-Scholes Option

Pricing Model (OPM). See Chapter 2 for details of the OPM.

Black-Scholes Option Pricing Model

Total Value of Firm 4.00 Analogous to the stock price from the BSOPM

Finally, assume that L’s volatility, σ is 0.60 and that the risk-free rate rRF is 6%.

Unlevered Horizon Value =

rsU - g

g. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to grow faster than 7%

during the next 3 years: FCF2 = $290,000 and FCF3 = $320,000, after which it will grow at a constant rate of

7%. The expected interest expense at Year 1 is $80,000, but it is expected to grow over the next couple of

years before the capital structure becomes constant: Interest expense at Year 2 will be $95,000, at Year 3 it

will be $120,000 and it will grow at 7% thereafter. What is the estimated horizon unlevered value of

operations (i.e., the value at Year 3 immediately after the FCF at Year 3)? What is the current unlevered value

of operations? What is the horizon value of the tax shield at Year 3? What is the current value of the tax

shield? What is the current total value? The tax rate and unlevered cost of equity remain at 40% and 14%,

respectively.

(Free Cash Flow)(1+g)

412

413

414

415

416

417

418

419

420

421

422

423

424

425

439

440

441

442

443

444

445

446

A B C D E F G H I J K

The value of L's equity must be $2.20 million. The value of its debt must be what is left over: $1.80 million.

This gives a yield of 10.88% for the debt.

Value of Stock and Debt for Different Volatilities

Equity Debt Debt yield

Volatility $ 2.20 $ 1.80 10.888%

0.20

2.12 1.88 6.18%

0.25

2.12 1.88 6.20%

0.30

2.12 1.88 6.27%

i. What is the value of L's stock for volatilities between 0.20 and 0.95? What incentives might

the manager of L have if she understands this relationship? What might debtholders do in

response? Answer: See below and the Chapter 21 Mini Case Show.

2.00

2.50

3.00

Values of Debt and Equity for Different Volatilities