Answers and Solutions: 21 – 1

Chapter 21

Dynamic Capital Structures

ANSWERS TO END-OF-CHAPTER QUESTIONS

21-1 a. MM Proposition I states the relationship between leverage and firm value.

Proposition I without taxes is V = EBIT/rsU. Since both EBIT and rsU are constant,

firm value is also constant and capital structure is irrelevant. With corporate taxes,

Proposition I becomes V = Vu + TD. Thus, firm value increases with leverage and the

optimal capital structure is virtually all debt.

c. The Miller model introduces personal taxes. The effect of personal taxes is,

essentially, to reduce the advantage of corporate debt financing.

e. The value of the debt tax shield is the present value of the tax savings from the

interest payments. In the MM model with taxes, this is just interest x tax rate /

discount rate = iDT/r, and since i = r in the MM model, this is just TD. If a firm

grows and the discount rate isn’t r, then the value of this growing tax shield is

rdTDg/(1+rTS) where rd is the interest rate on the debt and rTS is the discount rate for

the tax shield. In the APV model, the tax savings are discounted at the unlevered cost

of equity.

Answers and Solutions: 21 – 2

21-2 Modigliani and Miller show that the value of a leveraged firm must be equal to the

value of an unleveraged firm. If this is not the case, investors in the leveraged firm

will sell their shares (assume they owned 10%). They will then borrow an amount

equal to 10% of the debt of the leveraged firm. Using these proceeds, they will

purchase 10% of the stock of the unlevered firm (which provides the same return as

the leveraged firm) with a surplus left to be invested elsewhere. This arbitrage

process will drive the price of the stock of the leveraged firm down and drive up the

price of the stock of the unlevered firm. This will continue until the value of both

stocks are equal.

The assumptions of the MM model are:

• Stocks and bonds are traded in perfect capital markets. Therefore, (a) there are no

brokerage costs and (b) individuals can borrow at the same rate as corporations.

Brokerage fees and varying interest rates will, in effect, lower the surplus

available for alternative investment.

21-3 MM without taxes would support AT&T, although if AT&T really believed MM,

they should not object to Gordon’s 50 percent debt ratio. MM with taxes would lead

21-4 The value of a growing tax shield is greater than the value of a constant tax shield.

This means that for a given initial level of debt a growing firm will have more value

21-5 If equity is viewed as an option on the total value of the firm with a strike price equal

to the face value of debt then the equity value should be affected by risk in the same

way that an option is affected by risk. An option is worth more if the underlying asset

Answers and Solutions: 21 – 4

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

21-1 VL = VU = $500 million.

21-2 VL = VU + TD= $800 + 0.35($60) = $821 million.

21-4 VL = VU +

−)g

sU

r(

)

c

T)(D(

d

r

= $800 +

−)03.011.0(

)35.0)(60(05.0

= $800 + $13.125

= $813.125 million.

Answers and Solutions: 21 – 5

c. $2 Million Debt: VL = VU + TD = $10 + 0.25($2) = $10.5 million.

rsL = rsU + (rsU − rRF)(1 − T)(D/S)

= 15.625% + (15.625% − 10%)(0.75)($2/$8.5)

= 15.625 + 5.625% (0.75)($2/$8.5) = 16.62%.

d. $6 Million Debt: VL = $8.0 + 0.40($6) = $10.4 million.

rsL = 15.625% + 5.625%(0.60)($6/$4.4) = 20.23%.

21-6 a. VU =

sU

r

EBIT

=

10.0

million 2$

= $20 million.

b. rsU = 10.0%. (Given)

d. WACCU = rsU = 10%.

For Firm L, we know that WACC must equal rsU = 10% according to Proposition I.

e. VL = $22 million is not an equilibrium value according to MM. Here’s why.

Suppose you owned 10 percent of Firm L’s equity, worth 0.10($22 million – $10

million) = $1.2 million. Your cash flow is equal to 10% of the dividends paid by the

levered firm. Because it is a zero-growth firm, its dividends are equal to its net

income: Dividends = Net income = EBIT – rdD = $2,000,000 – 0.05($1,000,000) =

$1,500,000. Your 10% share is 0.10($1,500,000) = $150,000. Therefore, your annual

cash flow is $150,000.

Your cash stream would now be: (a) 10 percent of firm U’s dividends, which is

$200,000: 0.10(EBITU) = 0.10($2 million) = $200,000; plus (b) the return on the

extra $200,000 profit you invested in risk-free debt, which is $10,000: rd(profit) =

0.05($200,000) = $10,000; minus (c) the interest expense on the $1 million you

borrowed, which is $50,000: rd(loan) = 0.05($1 million)] = $50,000. Your net cash

flow from this strategy is $200,000 + $10,000 – $50,000 = $160,000.

Answers and Solutions: 21 – 7

21-7 a. VU =

sU

r

)T1(EBIT −

=

10.0

)4.01(2$ −

= $12 million.

VL = VU + TD = $12 + (0.4)$10 = $16 million.

c. SL =

sL

d

r

)T1)(DrEBIT( −−

=

15.0

6.0)]10($05.02[$ −

= $6 million.

21-8 a. VU =

)T1(r

)T1)(T1(EBIT

ssU

sC

−

−−

=

)01(10.0

)01)(4.01(2$

−

−−

= $12 million.

Answers and Solutions: 21 – 8

b. VU =

)T1(r

)T1)(T1(EBIT

ssU

sC

−

−−

=

)01(10.0

)01)(01(2$

−

−−

= $20 million.

Gain = VL − VU = $20 − $20 = $0.

c. VU =

)T1(r

)T1)(T1(EBIT

ssU

sC

−

−−

=

)01(10.0

)01)(4.01(2$

−

−−

= $12 million.

Answers and Solutions: 21 – 9

d. VU =

)T1(r

)T1)(T1(EBIT

ssU

sC

−

−−

=

)28.01(10.0

)28.01)(4.01(2$

−

−−

= $12 million.

21-9 a. VU = $500,000/(rsU – g) = $500,000/(0.13 – 0.09) = 12,500,000.

b.

million $16.0

0.09 – 0.13

million 5x 0.40x 0.07

million $12.5VL=

+=

. So since

D = 5, S = 16 – 5 = $11.0 million.

11

5

0.07)(0.130.13 rsL −+=

= 15.7%

21-10 a. VU = SU =

sU

r

EBIT

=

11.0

000,600,1$

= $14,545,455.

VL = VU = $14,545,455.

Answers and Solutions: 21 – 10

b. At D = $0:

rs = 11.0%; WACC = 11.0%

At D = $6 million:

At D = $10 million:

rsL = 11% + 5%

455,545,4$

000,000,10$

= 22.00%.

Answers and Solutions: 21 – 11

d. At D = $0:

WACC = (D/V)rd(1 – T) + (S/V)rs

=($6,000,000/$11,127,273)(6%)(0.6) + ($5,127,273/$11,127,273)(14.51%)

= 8.63%.

At D = $10 million:

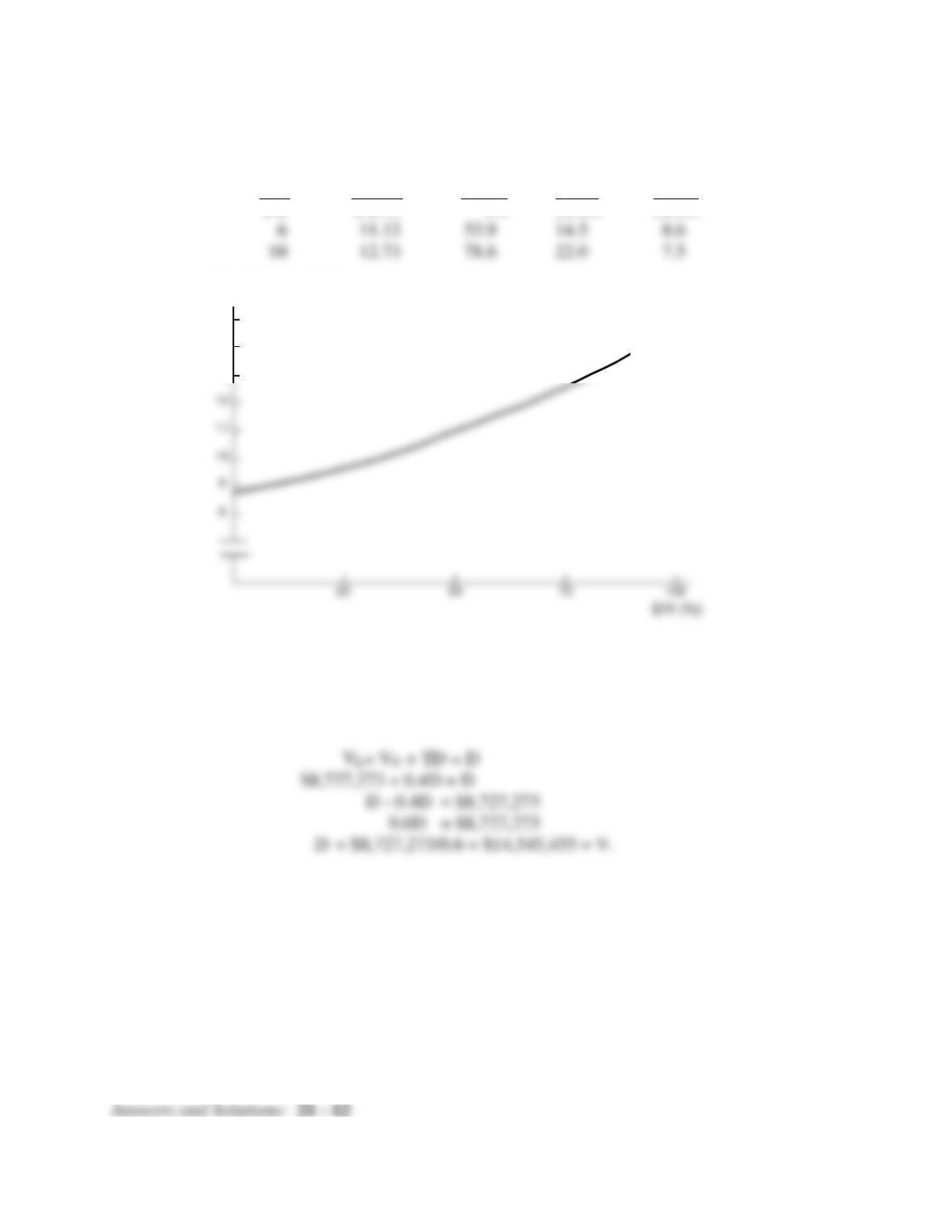

Summary: (in millions)

D V D/V rs WACC

$ 0 $ 8.73 0% 11.0% 11.0%

e. The maximum amount of debt financing is 100 percent. At this level

D = V, and hence

15

14

13

Value (Millions of Dollars)

Answers and Solutions: 21 – 13

Since the bondholders are bearing the same risk as the equity holders of the unlevered

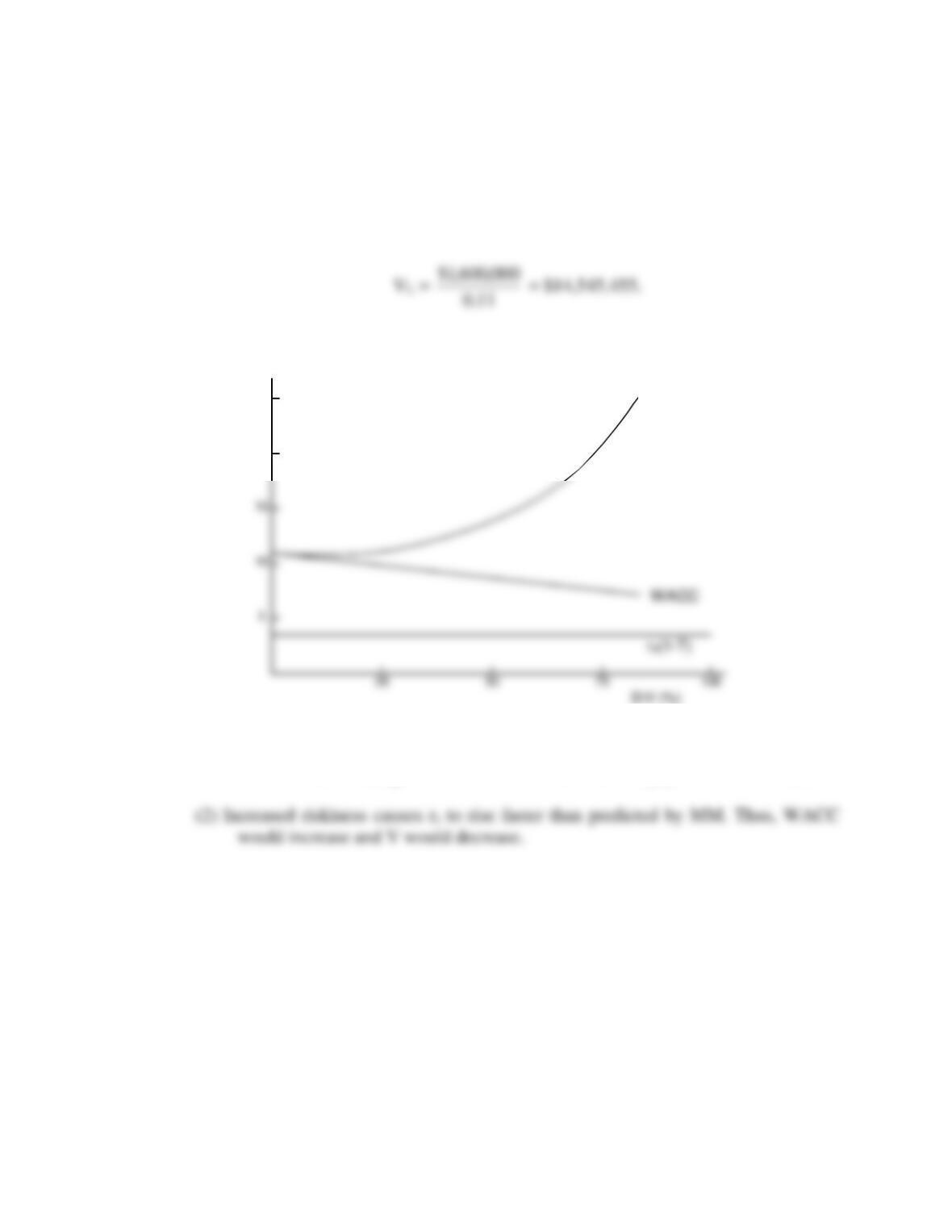

firm, rd is now 11 percent. Now, the total interest payment is $14,545,455(0.11) =

$1.6 million, and the entire $1.6 million of EBIT would be paid out as interest. Thus,

the investors (bondholders) would get $1.6 million per year, and it would be

capitalized at 11 percent:

f. (1) Rising interest rates would cause rd and hence rd(1 – T) to increase, pulling up

WACC. These changes would cause V to rise less steeply, or even to decline.

25

20

Cost of Capital (%)

kS

rs

Answers and Solutions: 21 – 14

21-11 a. The inputs to the Black and Scholes option pricing model are P = 5, X = 2, rRF = 6%,

= 50%, and t = 2 years. Given these inputs, the value of a call option is calculated

as:

t

t]2/r[)X/Pln(

d2

RF

1

++

=

=

8191.1

25.0

2]2/5.006.0[)2/5ln( 2=

++

.

b. The debt must therefore be worth 5-3.29 = $1.71 million. Its yield is

%1.881.0171.1/0.2 ==−

.

c. At a volatility of 30% d1 = 2.6547 and N(d1) = 0.9960. d2 = 2.2304 and N(d2) =

0.9871. This gives an option value of $3.23 million. The debt value is then 5.0 –

Answers and Solutions: 21 – 15

21-12 a. HVU,3 =

07.013.0

)07.1( 40$

−

= $713.33.

c. TS = (Interest expense)(T)

TS1 = $8(0.4) = $3.2

TS2 = $9(0.4) = $3.6

TS3 = $10(0.4) = $4.0

HVU,3 =

07.013.0

)07.1( 0.4$

−

= $71.33.

Answers and Solutions: 21 – 16

SOLUTION TO SPREADSHEET PROBLEM

21-13 The detailed solution for the problem is available in the file FM14 Ch21 P13 Build a

Model Solution.xls on the textbook’s Web site.

Mini Case: 21 – 17

MINI CASE

David Lyons, CEO of Lyons Solar Technologies, is concerned about his firm’s level of debt

financing. The company uses short-term debt to finance its temporary working capital

needs, but it does not use any permanent (long-term) debt. Other solar technology

companies average about 30 percent debt, and Mr. Lyons wonders why they use so much

more debt, and what its effects are on stock prices. To gain some insights into the matter,

he poses the following questions to you, his recently hired assistant:

a. Who were Modigliani and Miller (MM), and what assumptions are embedded in

the MM and Miller models?

Answer: Modigliani and Miller (MM) published their first paper on capital structure (which

assumed zero taxes) in 1958, and they added corporate taxes in their 1963 paper.

Modigliani won the Nobel Prize in economics in part because of this work, and most

subsequent work on capital structure theory stems from MM. Here are their

assumptions:

• Firms’ business risk can be measured by σEBIT, and firms with the same degree of

risk can be grouped into homogeneous business risk classes.

Mini Case: 21 – 18

b. Assume that firms U and L are in the same risk class, and that both have EBIT =

$500,000. Firm U uses no debt financing, and its cost of equity is rsU = 14%.

Firm L has $1 million of debt outstanding at a cost of rd = 8%. There are no

taxes. Assume that the MM assumptions hold, and then:

1. Find v, s, rs, and WACC for firms U and L.

Answer: First, we find Vu and VL:

VU =

sU

r

EBIT

=

14.0

000,500$

= $3,571,429.

Mini Case: 21 – 19

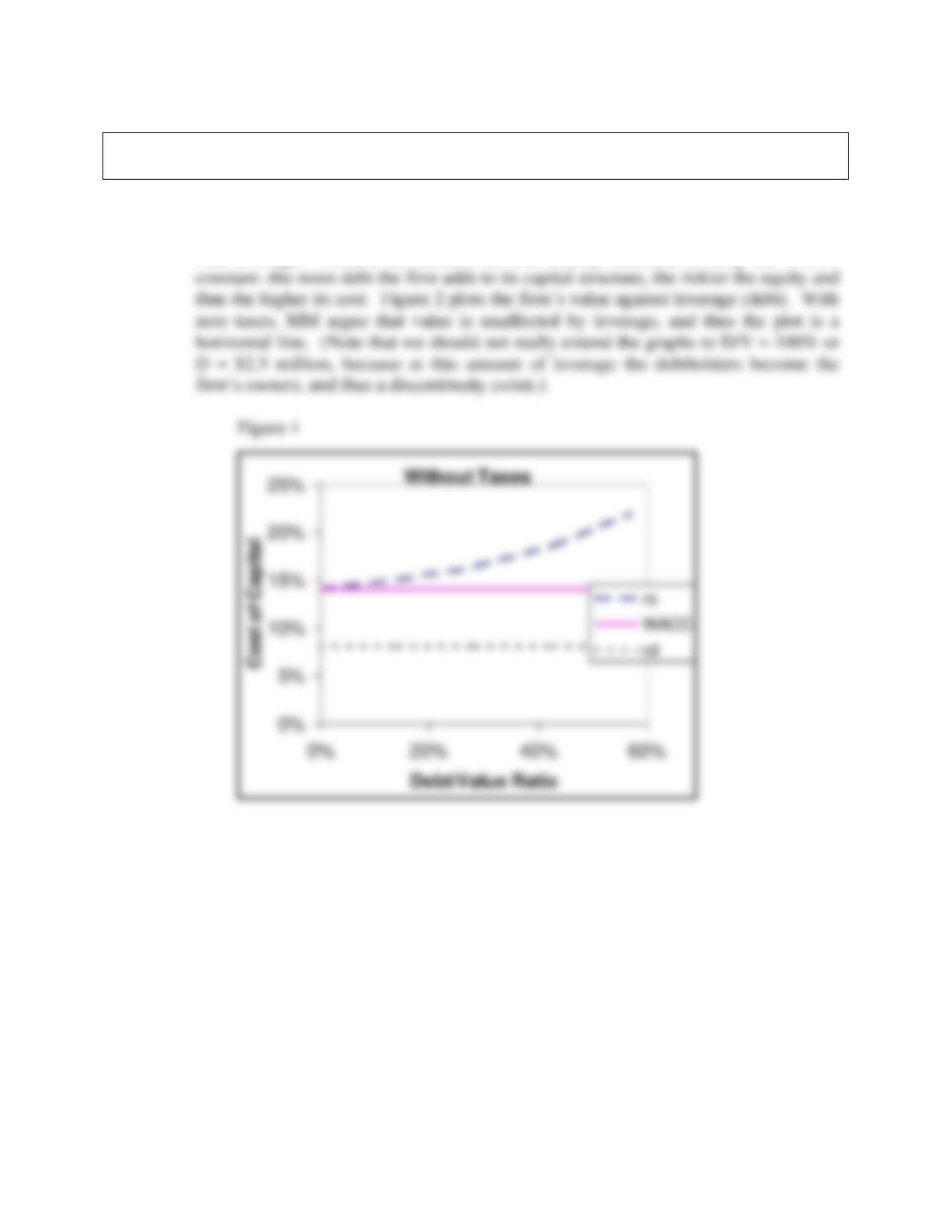

b. 2. Graph (a) the relationships between capital costs and leverage as measured by

D/V, and (b) the relationship between value and D.

Answer: Figure 1 plots capital costs against leverage as measured by the debt/value ratio.

Note that, under the MM no-tax assumption, rd is a constant 8 percent, but rs increases

with leverage. Further, the increase in rs is exactly sufficient to keep the WACC

Mini Case: 21 – 20

c. Using the data given in part B, but now assuming that firms L and U are both

subject to a 40 percent corporate tax rate, repeat the analysis called for in B(1)

and B(2) under the MM with-tax model.

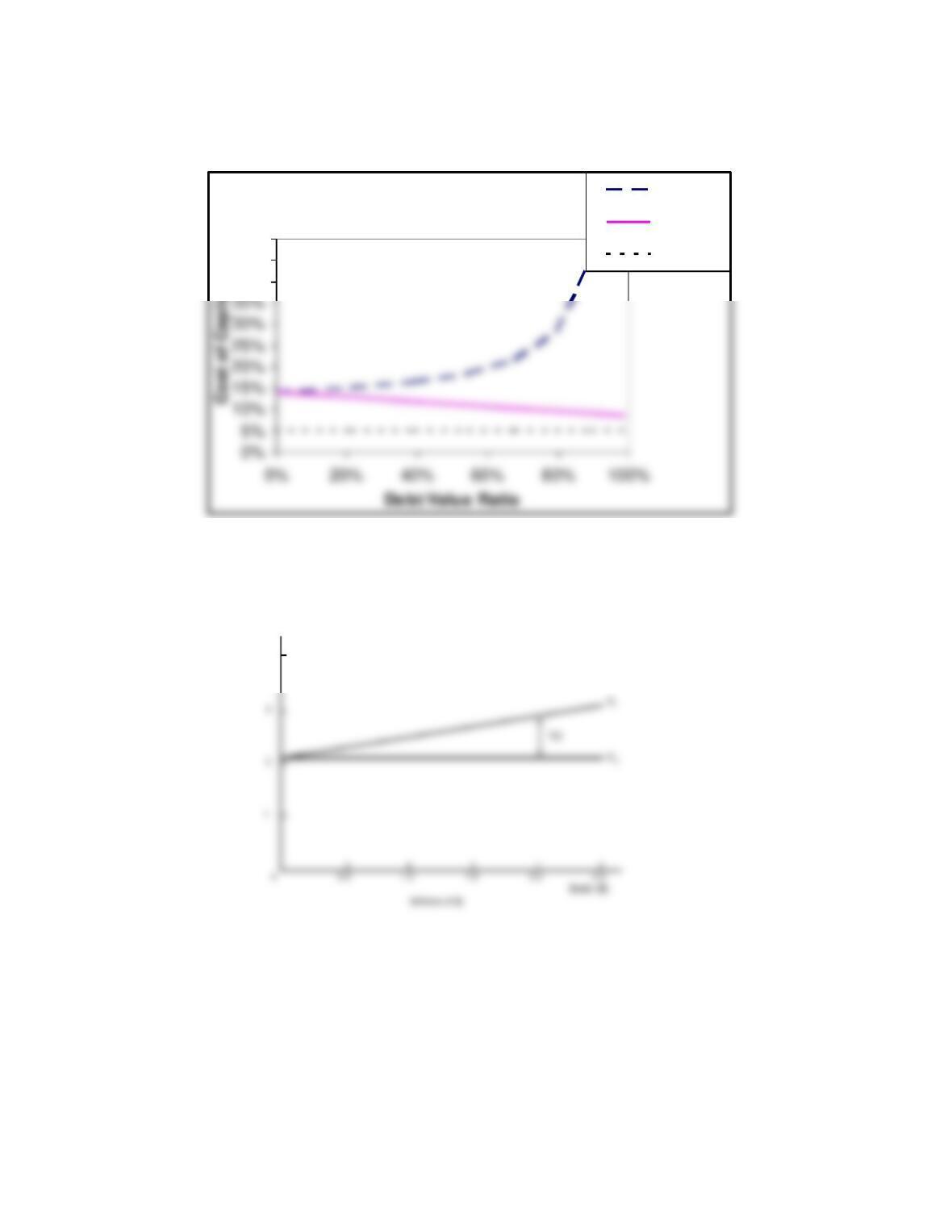

Answer: With corporate taxes added, the MM propositions become:

Proposition I: VL = VU + TD.

Proposition II: rsL = rsU + (rsU – rd)(1 – T)(D/S).

4

Value of Firm, V

VUVL

($)

Figure 2

Thus, the use of $1,000,000 of debt financing increases firm value by T(D) =

$400,000 over its leverage-free value.

To find rsL, it is first necessary to find the market value of the equity:

D + SL = VL

$1,000,000 + SL = $2,542,857

SL = $1,542,857.

now,

The WACC is lower for the levered firm than for the unlevered firm when corporate

taxes are considered.

Figure 3 below plots capital costs at different D/V ratios under the MM model

Mini Case: 21 – 22

Figure 3

4

Value of Firm, V

($)

Figure 4

With Taxes

40%

45%

50%

rs

WACC

rd x (1-T)

Mini Case: 21 – 23

d. Now suppose investors are subject to the following tax rates:

TD = 30% and TS = 12%.

1. What is the gain from leverage according to the miller model?

Answer: To begin, note that Miller’s Proposition I is stated as follows:

VL = VU +

−

−−

−)T1(

)T1)(T1(

1D

SC

D.

Mini Case: 21 – 24

d. 2. How does this gain compare to the gain in the MM model with corporate taxes?

Answer: If only corporate taxes were considered, then

VL = VU + TCD = VU + 0.40D.

The net effect depends on the relative effective tax rates on income from stocks and

bonds, and on corporate tax rates. The tax rate on stock income is reduced vis-à-vis

d. 3. What does the Miller model imply about the effect of corporate debt on the value

of the firm, that is, how do personal taxes affect the situation?

Answer: The addition of personal taxes lowers the value of debt financing to the firm. The

underlying rationale can be explained as follows: the U.S. corporate tax laws favor

debt financing over equity financing, because interest expense is tax deductible while

Mini Case: 21 – 25

e. What capital structure policy recommendations do the three theories (MM

without taxes, MM with corporate taxes, and Miller) suggest to financial

managers? Empirically, do firms appear to follow any one of these guidelines?

Answer: In a zero tax world, MM theory says that capital structure is irrelevant—it has no

impact on firm value. Thus, one capital structure is as good as another. With

f. Suppose that Firms U and L are growing at a constant rate of 7% and that the

investment in net operating assets required to support this growth is 10% of

EBIT. Use the compressed adjusted present value (APV) model to estimate the

value of U and L. Also estimate the levered cost of equity and the weighted

average cost of capital.

Answer: If a firm is growing, the assumptions that MM made are violated. The extension to

the MM model shows how growth affects the value of the debt tax shield and the cost

of capital. The first difference in this situation is that the appropriate discount rate for

the debt tax shield is the unlevered cost of equity, not the cost of debt. The second

difference is that a growing debt tax shield is more valuable than a constant debt tax

shield.

Mini Case: 21 – 26

= 250,000/(0.14 – 0.07) = $3,571,429

Which is greater than in part C because the firm is growing.

In this case the increase in the firm’s value due to the debt tax shield as a percent of

its zero debt value is $457,143/$3,571,429 = 12.80%

This is less than the increase in the non–growing firm’s value as calculated using the

MM model: $400,000/$2,142,857 = 18.7%.

g. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to

grow unevenly over the next 3 years: FCF2 = $290,000 and FCF3 = $320,000,

after which it will grow at a constant rate of 7%. The expected interest expense

at Year 1 is $80,000, but it is expected to grow over the next couple of years

before the capital structure becomes constant: Interest expense at Year 2 will be

$95,000, at Year 3 it will be $120,000 and it will grow at 7% thereafter. What is

the estimated horizon unlevered value of operations (i.e., the value at Year 3

immediately after the FCF at Year 3)? What is the current unlevered value of

operations? What is the horizon value of the tax shield at Year 3? What is the

current value of the tax shield? What is the current total value? The tax rate and

unlevered cost of equity remain at 40% and 14%, respectively.

Answer: The unlevered horizon value of operations can be found by applying the constant

growth formula:

Mini Case: 21 – 27

HVU,3 = [FCF3(1+gL)]/(rsU – gL) = [$320(1.07)]/(0.14 – 0.07) = $4,891.43.

The horizon value of the tax shield can be found by applying the constant growth

formula:

HVTS,3 = [TS3(1+gL)]/(rsU – gL) = [$48(1.07)]/(0.14 – 0.07) = $733.71.

h. Suppose there is a large probability that L will default on its debt. For the

purpose of this example, assume that the value of L’s operations is $4 million

(the value of its debt plus equity). Assume also that its debt consists of 1-year,

zero coupon bonds with a face value of $2 million. Finally, assume that L’s

volatility, σ is 0.60 and that the risk-free rate rRF is 6%.

Answer: L’s equity can be considered as a call option on the total value of l with an exercise

price of $2 million, and an expiration date in one year. If the value of L’s operations

Mini Case: 21 – 28

than $2 million in one year, then management will repay the debt and the

stockholders will keep the company.

in this case, P = $4

X = $2

= 0.60

T = 1.0

R = 0.06

Mini Case: 21 – 29

i. What is the value of L’s stock for volatilities between 0.20 and 0.95? What

incentives might the manager of L have if she understands this relationship?

What might debtholders do in response?

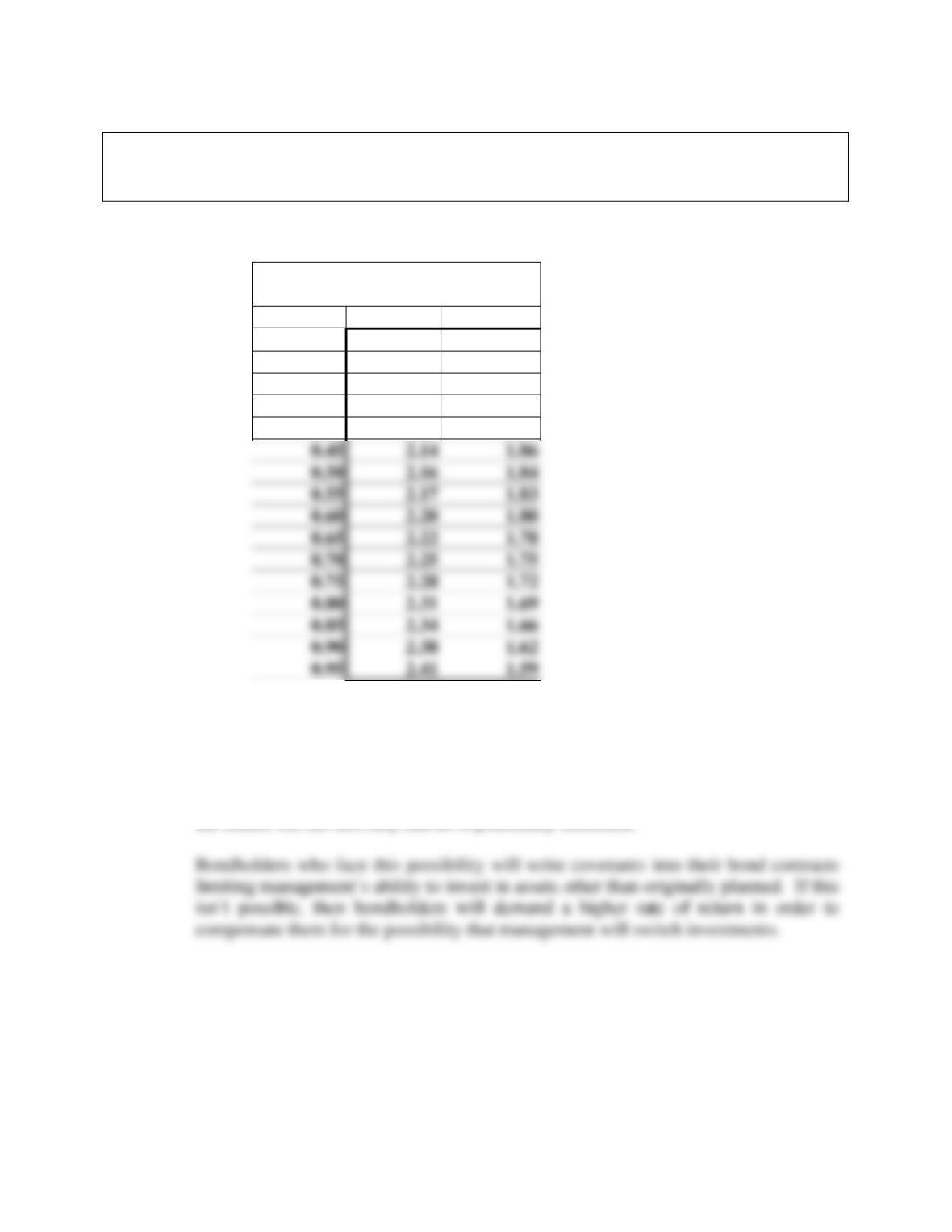

Answer: The mini case model shows the calculations for the table below.

Value of Stock and Debt

for Different Volatilities

Volatility

Equity

Debt

0.20

2.12

1.88

0.25

2.12

1.88

0.30

2.12

1.88

0.35

2.12

1.88

0.40

2.13

1.87

The value of the equity increases as the volatility increases—and the value of the debt

decreases as well. A manager who knows this may choose to invest the proceeds

from borrowing in assets that are riskier than usual. This is called “bait and switch.”

This action decreases the value of the debt, because now its claim is riskier. It

increases the value of equity because the worse the stockholders can do is default on

the bonds, but the best they can do is potentially unlimited.

0.45

2.14

1.86

0.50

2.16

1.84

0.55

2.17

1.83

0.60

2.20

1.80

0.65

2.22

1.78

0.70

2.25

1.75

0.75

2.28

1.72

0.80

2.31

1.69

0.85

2.34

1.66

0.90

2.38

1.62

0.95

2.41

1.59