Solution 12/8/2012

Chapter: 21

Problem: 13

a. Using the Black-Scholes Option Pricing Model, how much is the equity worth?

Black-Scholes Option Pricing Model

Total Value of Firm 200.00 this is the current value of operations

b. How much is the debt worth today? What is its yield?

Debt value = Total Value – Equity Value = 79.15$ million

Debt yield = 8.107%

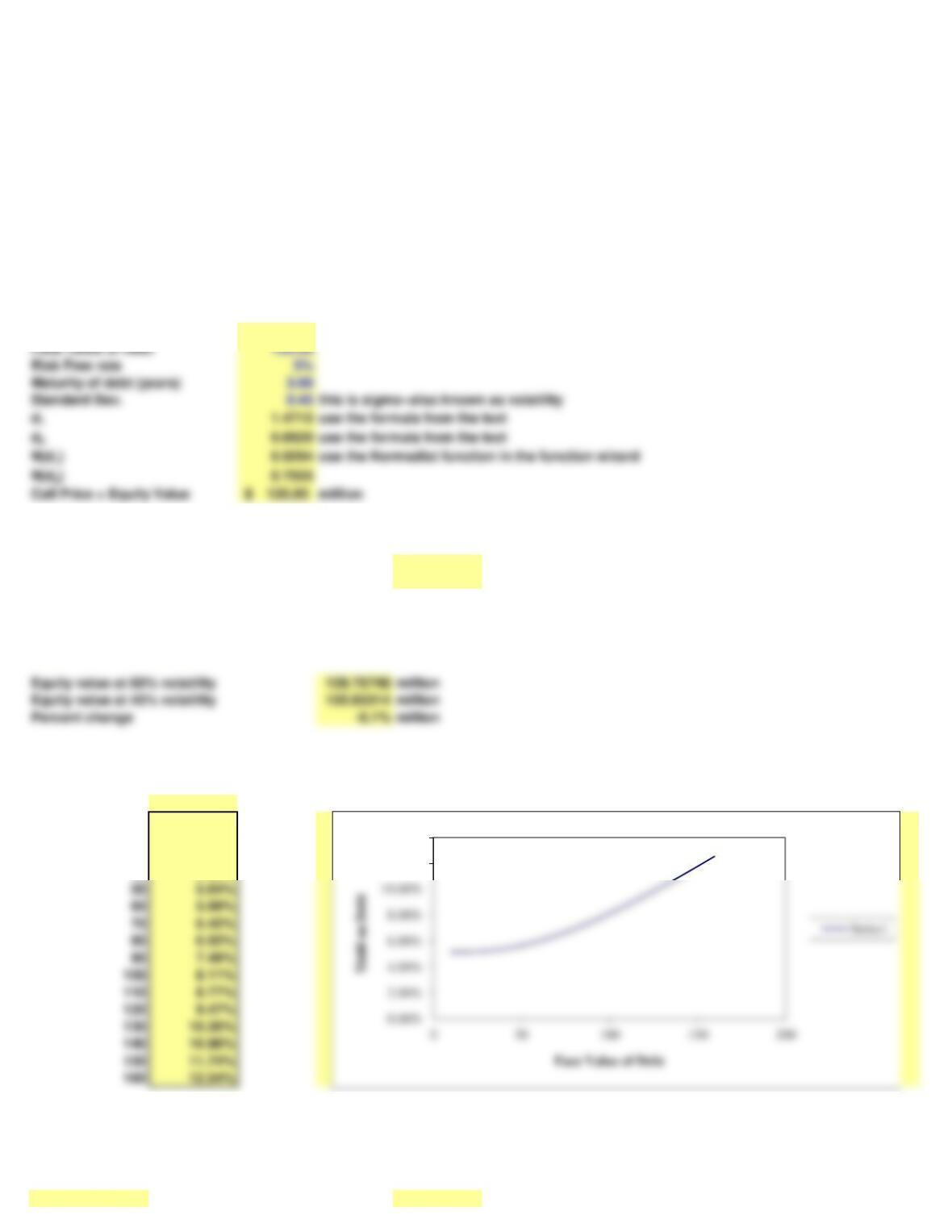

Equity value at 60% volatility 128.76748 million

Equity value at 45% volatility 120.85314 million

Percent change -6.1% million

d. Graph the cost of debt versus the face value of debt for values of the face value from $0.5 to $8 million.

Cost of Debt

Face Value of Debt

8.107% hint: use a data table

10 5.13%

20 5.15%

30 5.22%

40 5.38%

50 5.64%

60 5.99%

70 6.42%

80 6.92%

90 7.49%

b. Graph the values of debt and equity for volatilities from 0.10 to 0.90 when the face value of the debt is $2 million.

Value of Debt Value of Equity

Volatility Face Value of Debt Volatility Face Value of Debt

79.15$ 100.00 120.85$ 100.00

Higgs Bassoon Corporation is a custom manufacturer of bassoons and other wind

instruments. Its current value of operations, which is also its value of debt plus equity, is

estimated to be $200 million. Higgs has $110 million face value, zero coupon debt that is

due in 3 years. The risk-free rate is 5%, and the standard deviation of returns for similar

companies is 60%. The owners of Higgs Bassoon view their equity investment as an

option and would like to know the value of their investment.

c. How much would the equity value and the yield on the debt change if Fethe’s

management were able to use risk management techniques to reduce its volatility to 45

percent? Can you explain this?

12.00%

14.00%

1 of 2

Face Value of Debt 100.00

Risk Free rate 5%

Maturity of debt (years) 3.00

Standard Dev. 0.45 this is sigma–also known as volatility

Call Price = Equity Value 120.85$ million

0.1 86.0708 0.1 113.9292

0.2 85.9606 0.2 114.0394

120.0000

140.0000

160.0000

Equity and Debt Values

2 of 2

0.3 84.6060 0.3 115.3940

0.4 81.3418 0.4 118.6582

0.5 76.6861 0.5 123.3139

0.6 71.2325 0.6 128.7675

0.7 65.3983 0.7 134.6017

0.8 59.4584 0.8 140.5416

0.9 53.5949 0.9 146.4051