Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 21: Mergers and Acquisitions

Learning Objectives

569

Chapter 21

Mergers and Acquisitions

Learning Objectives

After reading this chapter, students should be able to:

◆ Identity the different types of mergers and the various rationales for mergers.

◆ Conduct a simple analysis to evaluate the potential value of a target firm and discuss the various

considerations that influence the bid price.

◆ Explain whether the typical merger creates value for the participating shareholders.

◆ Discuss the value of other transactions such as leveraged buyouts (LBOs), corporate alliances, and

divestitures.

570

Lecture Suggestions

Chapter 21: Mergers and Acquisitions

Lecture Suggestions

In this chapter we discuss mergers, LBOs, merger rationales, classifications, merger regulation, and merger

analysis. In addition, we discuss corporate alliances and private equity investments. Finally, we talk about

divestitures and the rationale behind them.

DAYS ON CHAPTER: 2 OF 56 DAYS (50-minute periods)

Chapter 21: Mergers and Acquisitions

Answers and Solutions

571

Answers to End-of-Chapter Questions

21-1 Horizontal and vertical mergers are most likely to result in governmental intervention, but mergers

21-2 A tender offer might be used. Although many tender offers are made by surprise and over the

21-3 An operating merger involves integrating the company’s operations in hopes of obtaining

21-4 Disney’s management could (and did) argue that its stock was worth more than $4.22 per share,

21-5 Academicians have long argued that conglomerate mergers that produce no synergy are not

572

Answers and Solutions

Chapter 21: Mergers and Acquisitions

Solutions to End-of-Chapter Problems

21-1 D1 = $2.00; g = 5%; b = 0.9; rRF = 5%; RPM = 6%; P0 = ?

21-2 D1 = $2.00; g = 7%; b = 1.1; rRF = 5%; RPM = 6%; P0 = ?

b. The value of Vaccaro is $14.93 million:

Chapter 21: Mergers and Acquisitions

Answers and Solutions

573

Value at t4 of CF5 and all subsequent cash flows is:

21-5 0 1 2 3 10

| | | | • • • |

21-6 a. Since the cash flows are equity returns, the appropriate discount rate is that cost of equity

c. Annual cash flows are calculated as follows:

2015

2016

2017

2018

10%

574

Comprehensive/Spreadsheet Problem

Chapter 21: Mergers and Acquisitions

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solutions for parts a, b, and c are provided at the back of the text; however, the solution to

part d is not. Instructors can access the

Excel

file on the textbook’s website.

21-7 See parts a, b, and c on the preceding page.

Chapter 21: Mergers and Acquisitions

Integrated Case

575

Integrated Case

21-8

Smitty’s Home Repair Company

Merger Analysis

Smitty’s Home Repair Company, a regional hardware chain that specializes in do-

576

Integrated Case

Chapter 21: Mergers and Acquisitions

A. Several reasons have been proposed to justify mergers. Among the

more prominent are (1) tax considerations, (2) risk reduction,

(3) control, (4) purchase of assets at below-replacement cost, and

(5) synergy. In general, which of the reasons are economically

justifiable? Which are not? Which fit the situation at hand? Explain.

Answer: [Show S21-1 through S21-3 here.] The economically justifiable

rationales for mergers are synergy and tax consequences. Synergy

Chapter 21: Mergers and Acquisitions

Integrated Case

577

578

Integrated Case

Chapter 21: Mergers and Acquisitions

B. Briefly describe the differences between a hostile merger and a

friendly merger.

Answer: [Show S21-4 here.] In a friendly merger, the management of one

firm (the acquirer) agrees to buy another firm (the target). In most

Chapter 21: Mergers and Acquisitions

Integrated Case

579

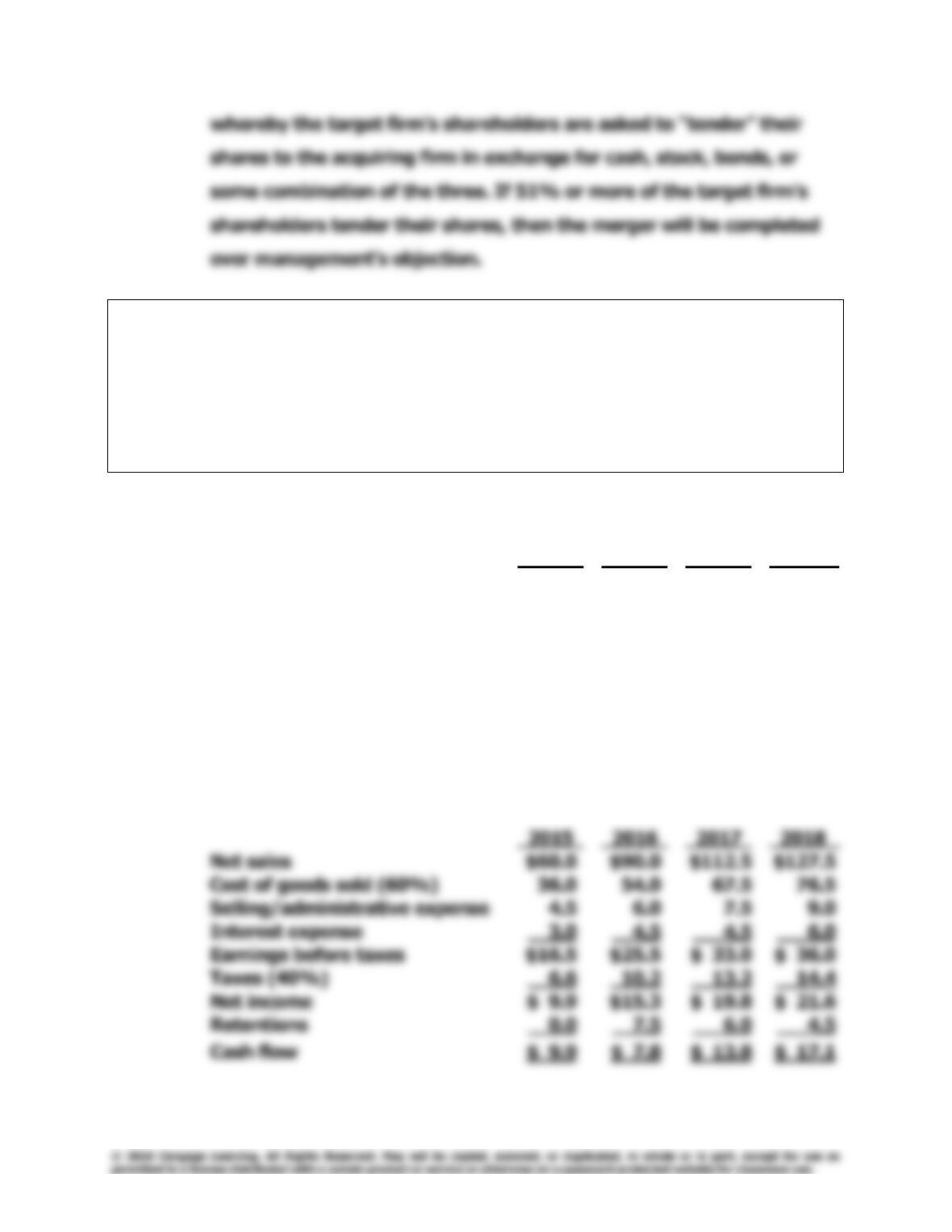

C. Use the data developed in Table IC 21.1 to construct the H division’s

cash flow statements for 2015 through 2018. Why is interest expense

deducted in merger cash flow statements, whereas it is not normally

deducted in a capital budgeting cash flow analysis? Why are earnings

retentions deducted in the cash flow statement?

Table IC 21.1 Estimates of Hill’s Hardware Data for Merger Analysis

2015 2016 2017 2018

Net sales $60.0 $90.0 $112.5 $127.5

Cost of goods sold (60%) 36.0 54.0 67.5 76.5

Selling/administrative expense 4.5 6.0 7.5 9.0

Interest expense 3.0 4.5 4.5 6.0

Necessary retained earnings 0.0 7.5 6.0 4.5

Answer: [Show S21-5 through S21-7 here.] The easiest approach here is to

create cash flow statements for the H division, assuming that the

acquisition is made (in millions of dollars).

580

Integrated Case

Chapter 21: Mergers and Acquisitions

D. Conceptually, what is the appropriate discount rate to apply to the

cash flows developed in Part C? What is your actual estimate of this

discount rate?

Answer: [Show S21-8 and S21-9 here.] As discussed above, the cash flows are

residuals, and they belong to the acquiring firm’s shareholders. Since

Chapter 21: Mergers and Acquisitions

Integrated Case

581

E. What is the estimated continuing value of the acquisition; that is,

what is the estimated value of the H division’s cash flows beyond

2018? What is Hill’s value to Smitty’s? Suppose another firm were

evaluating Hill’s as an acquisition candidate. Would it obtain the same

value? Explain.

Answer: [Show S21-10 through S21-12 here.] The 2018 cash flow is $17.1

million, and it is expected to grow at a 6% constant growth rate in

2019 and beyond. With a constant growth rate, the Gordon model

= $221.0 million.

582

Integrated Case

Chapter 21: Mergers and Acquisitions

F. Assume that Hill’s has 10 million shares outstanding. These shares are

traded relatively infrequently; but the last trade, made several weeks

ago, was at a price of $9 per share. Should Smitty’s make an offer for

Hill’s? If so, how much should it offer per share?

Answer: [Show S21-13 through S21-18 here.] With a current price of $9 per

Chapter 21: Mergers and Acquisitions

Integrated Case

583

G. What merger-related activities are undertaken by investment

bankers?

Answer: [Show S21-19 here.] The investment banking community is involved