491

LECTURE SUPPLEMENT

20–4 Financial Development and Industrial Structure

Further evidence on the importance of the financial system for economic growth comes from

microeconomic studies of industrial structure. Research has shown that countries with well–developed

financial systems usually have certain types of industries that thrive. In particular, industrial sectors that

rely more heavily on external finance to fund their investment projects should grow faster in countries that

have a more–developed financial system compared with countries that have a less–developed system.1

Young firms and those that don’t generate large cash flow are more likely to use external finance to

fund investment projects than older, established firms and those that generate large cash flow—those firms

ADDITIONAL CASE STUDY

20–5 Unit Banking and Economic Growth

Prior to WWII, federal law allowed a bank to conduct business only in one state, and some state laws

restricted each bank to only one branch location. Supporters of unit banking believed that allowing

multiple branches would lead to banks becoming too large and powerful. But most economists now

believe that unit banking was detrimental to the economy for several reasons: Large banks benefit from

growth before and after the reforms for those states relaxing restrictions and compared this to a control

group of states that were not affected by the reforms.

This study also showed that the main channel through which these reforms influenced economic

growth was the quality of the loans rather than the volume of them. Better loan quality implies better

allocation of funds to productive investments, raising economic growth. The authors interpret this effect

493

LECTURE SUPPLEMENT

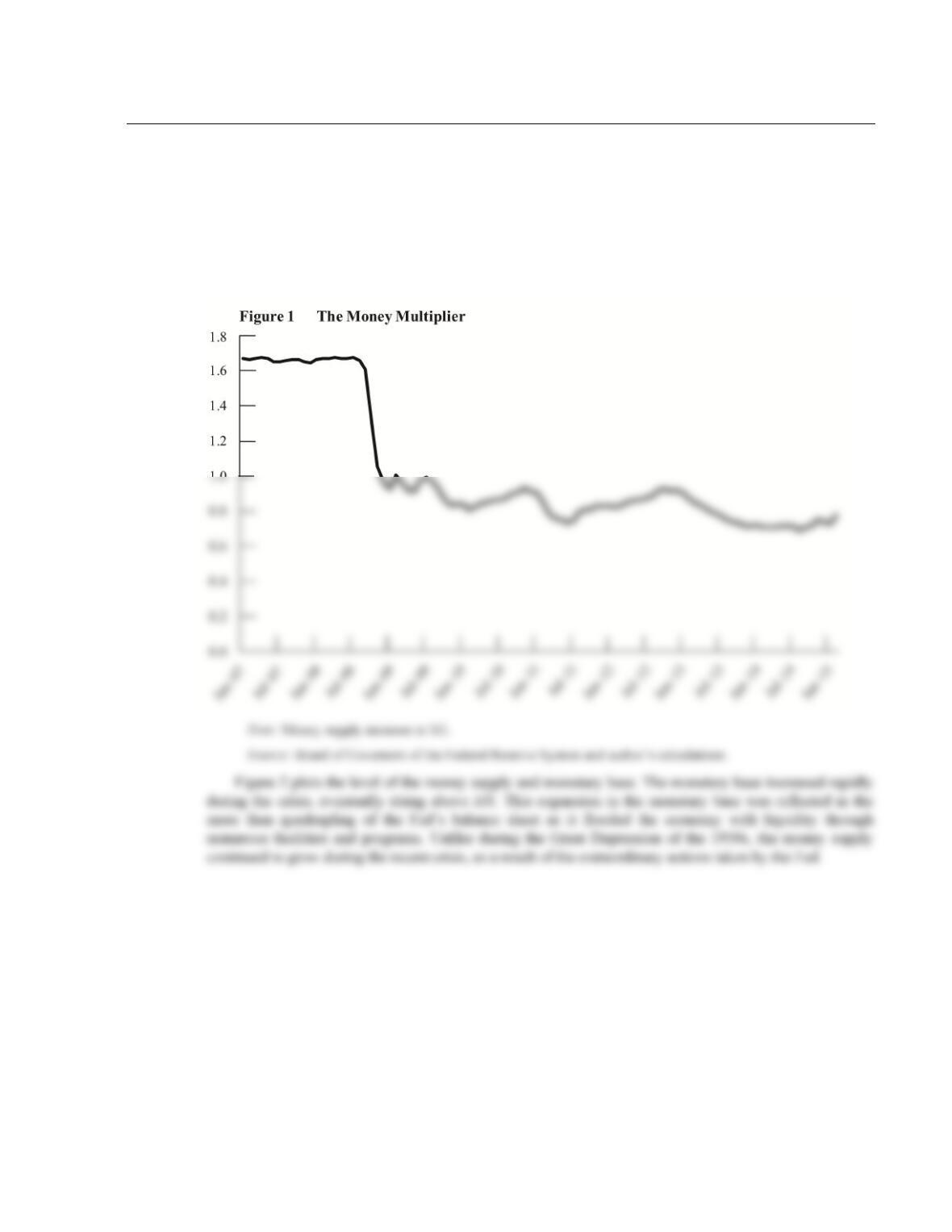

20–6 The Money Multiplier During the Financial Crisis of 2008–2009

As discussed in Chapter 4, the money multiplier measures the ratio of the money supply to the monetary

base. Each dollar of the monetary base gives rise to a multiple expansion in credit as banks make loans

from the funds they receive in deposits.

Figure 1 shows the money multiplier for the money supply measure known as M1. As the financial

crisis intensified during the fall of 2008, the money multiplier declined sharply, as banks became cautious

about lending (see Supplements 20–7 and 20–8). The multiplier fell from a value of about 1.7 before the

crisis to 0.8 by late 2009.

494

495

LECTURE SUPPLEMENT

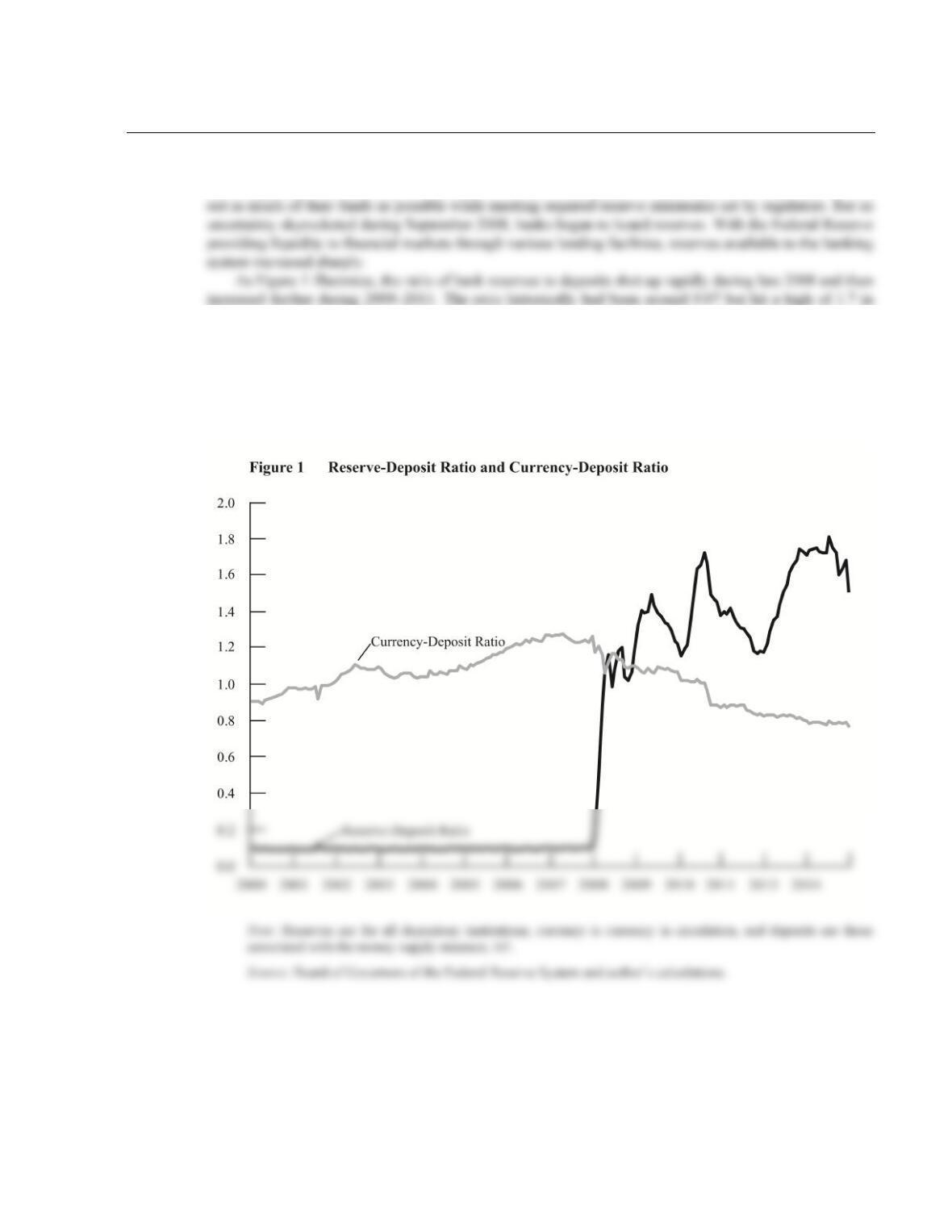

20–7 Banks Hoard Reserves During the Financial Crisis

Banks typically hold relatively low amounts of reserves compared to their deposits, as they seek to lend

2011. As discussed in Chapter 4, during the financial crisis of the early 1930s, the reserve–deposit ratio

also increased when a bank panic caused banks to curtail their lending.

But unlike during the crisis of the early 1930s, the currency–deposit ratio did not rise during the

recent crisis. As shown in Figure 1, it actually declined slightly. Even so, the increase in the reserve–

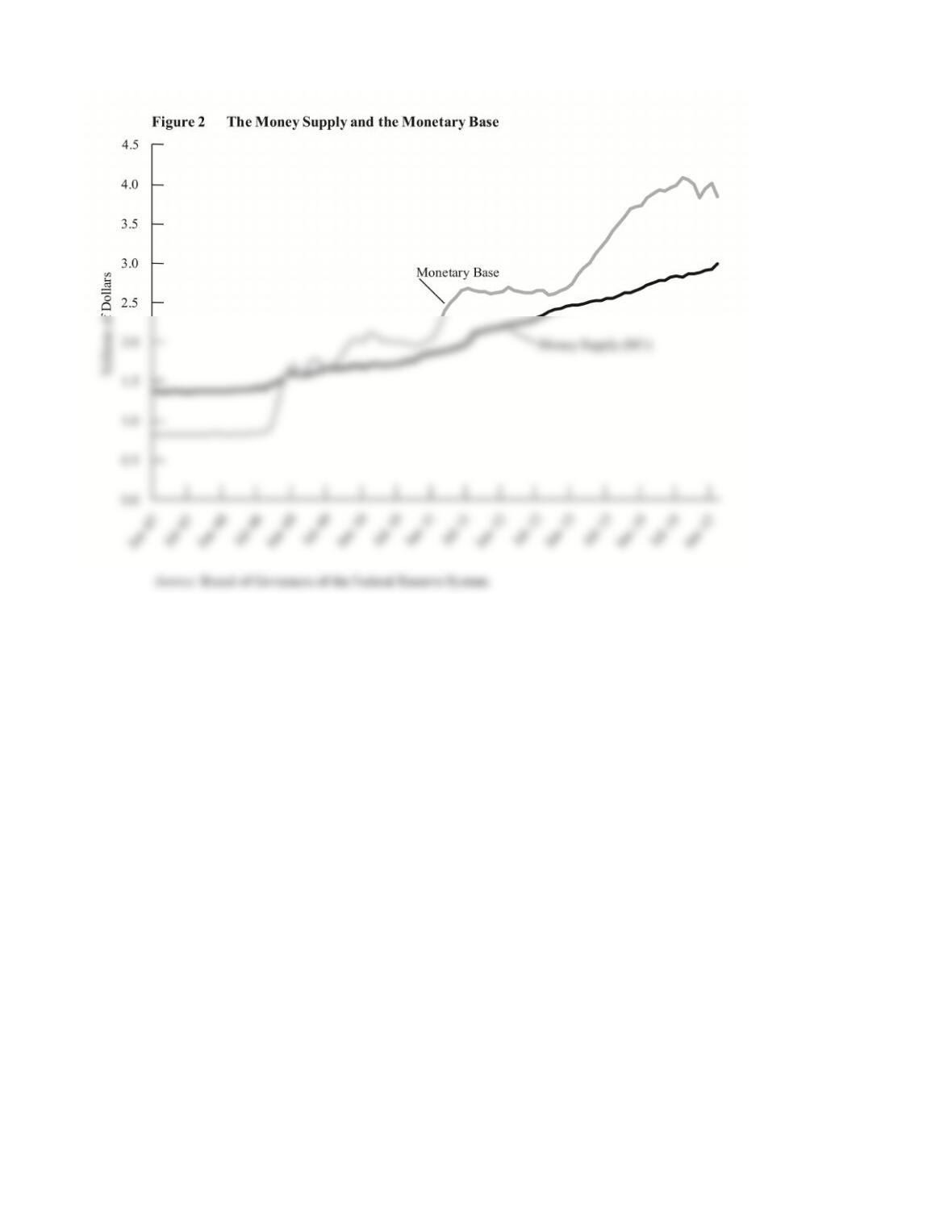

deposit ratio caused the money multiplier to drop sharply (see Supplement 20–6). But because the Fed had

tripled the monetary base, the money supply continued to expand, in contrast to the 1930s, when the Fed

did not increase reserves sufficiently to keep the money supply from plummeting.

496

ADDITIONAL CASE STUDY

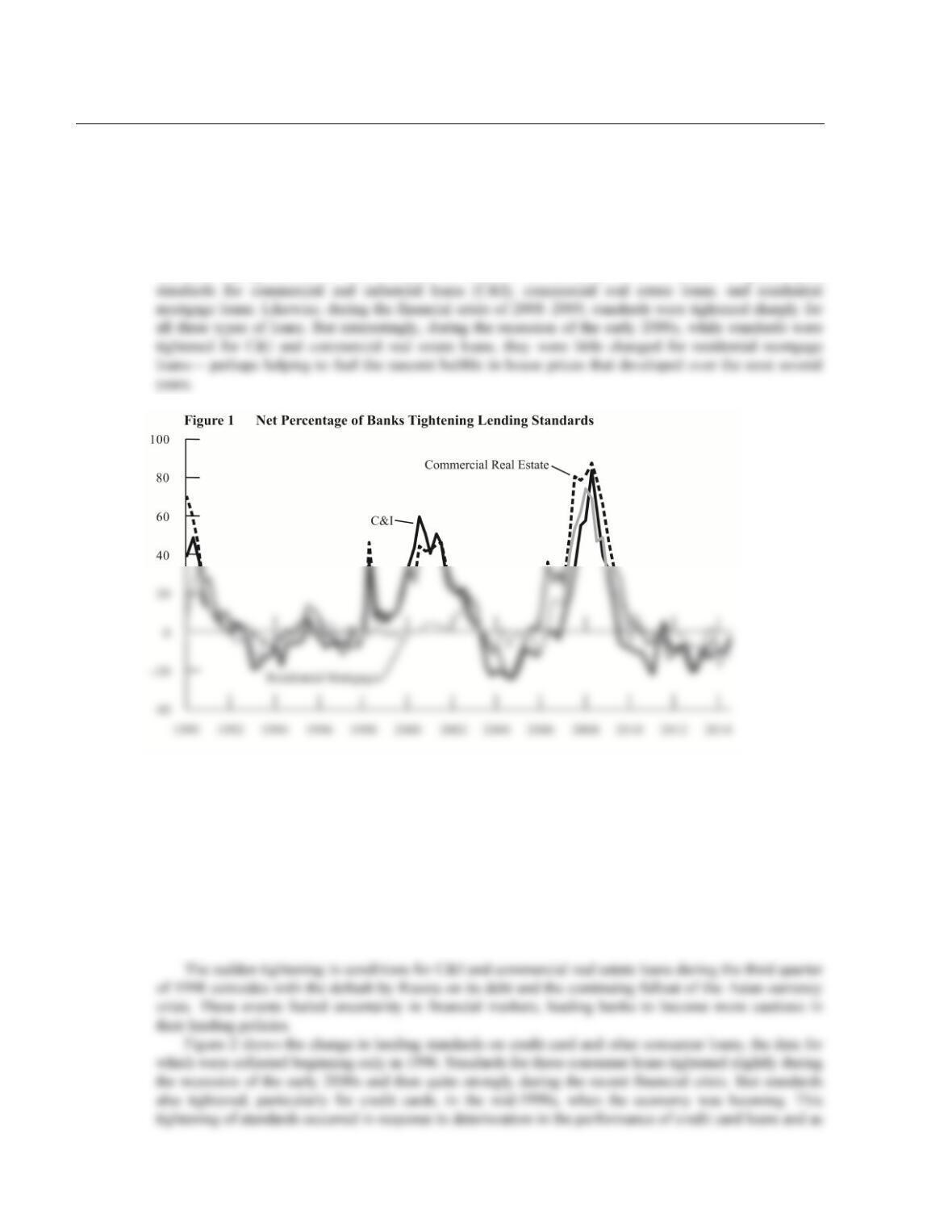

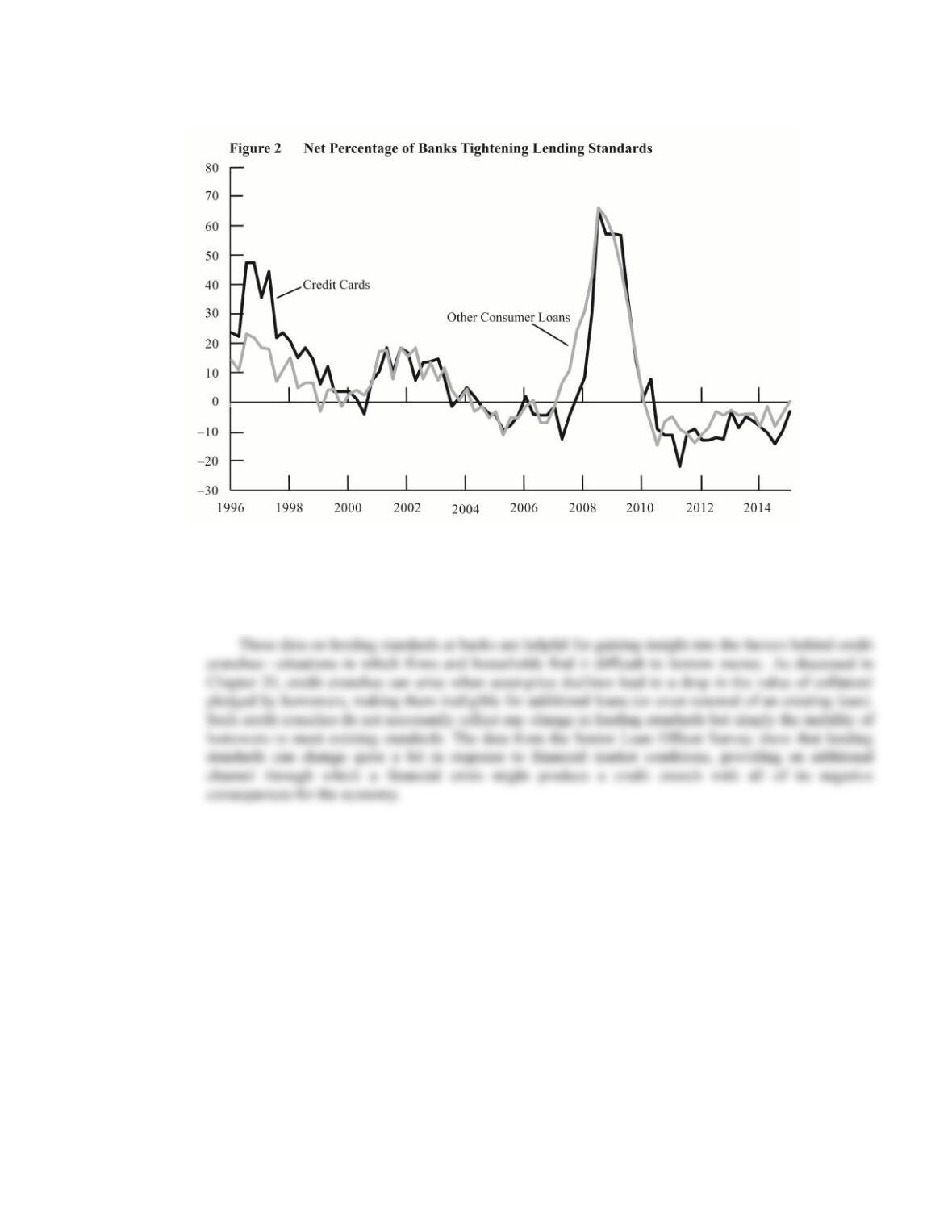

20–8 The Fed’s Senior Loan Officer Survey

To gain insight into how lending conditions may be changing in the economy, the Federal Reserve carries

out a quarterly Senior Loan Officer Survey at commercial banks. The survey asks detailed questions about

whether the respondent’s institution is tightening or easing credit to potential borrowers. In addition, it

asks about demand for loans and changes in the terms of loans.

As illustrated in Figure 1, banks generally tighten lending standards during recessions and ease

standards during recoveries. For example, the recession of the early 1990s witnessed a tightening of

Note: Data show the difference between the percentage of banks that reported tightening standards minus the

percentage of banks that reported easing standards. C&I loans are those made to commercial and industrial

enterprises that are not secured by real estate. Data for C&I loans in the figure are for loans to large and middle–

market firms. Data for commercial real estate loans starting in 2013 Q4 are for loans with construction and land

development purposes. Prior to the second quarter of 2007 data for residential mortgage loans are for all such

loans, while from the second quarter of 2007 data are for residential mortgage loans available only to prime

borrowers.

Source: Senior Loan Officer Opinion Survey on Bank Lending Practices, Board of Governors of the Federal

Reserve System.

497

a result of banks’ desire to encourage households to substitute secured, home–equity lines for unsecured

credit card balances and other consumer loans.

Note: Data show the difference between the percentage of banks that reported tightening standards minus the

percentage of banks that reported easing standards. From the second quarter of 2011, data for other consumer

loans exclude auto loans.

Source: Senior Loan Officer Opinion Survey on Bank Lending Practices, Board of Governors of the Federal

Reserve System.

LECTURE SUPPLEMENT

20–9 The Tax Treatment of Housing

Tax laws in the United States subsidize homeownership and may well have contributed to the frenzy in the

housing market during the house–price bubble of the mid–2000s. While it is true that the huge expansion in

subprime mortgage lending provided access to credit for many households that previously could not

qualify to buy a home, the tax breaks available under the personal income tax code made these loans seem

LECTURE SUPPLEMENT

20–10 More on the Fed’s Rescue Programs

In a speech given in April 2009, Federal Reserve Chairman Ben Bernanke outlined a framework for

to 0.25 percent, close to its lower bound. These new tools were intended, according to Bernanke, “to

further improve the functioning of credit markets and provide additional support to the economy.” The

actions taken by the Fed in using these new tools had significant effects on both the size and composition

of its balance sheet. Most importantly, the balance sheet more than doubled, from roughly $870 billion

before the crisis to over $2 trillion in 2010.

as to prevent panic caused by insufficient access to funds.

To improve the functioning of credit markets, the Fed established programs to lend directly to market

participants. These included the Commercial Paper Funding Facility (CPFF) and the Term Asset–Backed

Loan Facility (TALF). The goal of these programs was to bolster demand for commercial paper and asset–

backed securities, so as to meet funding needs of investors and borrowers in these markets and help restart

prevent the default of AIG. He argues that these loans were very different from the Fed’s other liquidity

programs but were necessary to prevent major disruptions in financial markets. And he points out that this

lending represented only about 5 percent of the Fed’s asset holdings. He said that he would work with the

Obama administration and Congress toward developing a formal resolution authority for such systemically

important nonbank financial institutions.

LECTURE SUPPLEMENT

20–11 Exit Strategies for the Fed

As mentioned in Supplement 20–10, the Fed’s balance sheet more than doubled during the financial crisis

of 2008–2009 as a result of various programs to provide support to the economy. By early 2010, with the

economy recovering and the financial crisis contained, discussion turned to the question of when and how

the Fed should begin to shrink the outstanding sums of money it had put into the economy. Some

and agrees to buy them back at a later date for a slightly higher price. During the interim, the level of

reserves is lowered, and if done on a rolling basis, a sustained decline in reserves can be achieved.

Second, Bernanke discusses introducing term deposits for banks at the Fed—similar to a certificate of

deposit—on which the bank would receive interest but would be restricted from cashing the deposit for a

period of time. This would serve to lower the amount of reserves available for lending during the term of

ADDITIONAL CASE STUDY

20–12 Greenspan Warns About Government Budget Surpluses

Chapter 20 discusses the use of equity injections into financial institutions by the Treasury. This was done

under authority granted by the Troubled Asset Relief Program (TARP) passed by Congress in October

2008 during the financial crisis. These equity injections are controversial in part because they may worsen

the moral hazard problem in banking, but also because they represent the government taking an ownership

continuing to run budget surpluses would require the government to start investing in the private sector. In

testimony before a congressional committee in January 2001, Greenspan argued that reducing the budget

deficit and debt to zero was desirable:

But continuing to run surpluses beyond the point at which we reach zero or near–zero federal

debt brings to center stage the critical longer–term fiscal policy issue of whether the federal

historically have been done through purchase and sale of short–term Treasury securities, paying off most

or all of the debt would mean that the market for Treasury securities would become thin and possibly go

out of existence. As Greenspan noted in testimony during February 2001:

The prospective decline in Treasury debt outstanding implied by projected federal budget

surpluses does pose a challenge to the implementation of monetary policy. The Federal

U.S. state and foreign governments, something allowed under the Federal Reserve Act. And he raised the

question of whether it might be necessary to expand the use of the discount window or to request authority

from Congress for acquiring a broader variety of assets via open market operations.

1 Testimony of Chairman Alan Greenspan, “Outlook for the Federal Budget and Implications for Fiscal Policy,” Before the Committee on the

LECTURE SUPPLEMENT

20–13 The Squam Lake Report

The Squam Lake Report: Fixing the Financial System was published in the summer of 2010 and provides

guidelines for reform of financial markets.1 The report was the work of a group of 15 academic economists

who had first come together at Squam Lake in New Hampshire in the fall of 2008 during the financial

crisis.

systemically important financial institutions, and capital standards would be more closely linked

to an institution’s risk.

Improving Resolution Options for Systemically Important Financial Institutions, so that the

government can resolve failing institutions in an orderly process and avoid potentially

destabilizing effects of an institution’s collapse.

504

LECTURE SUPPLEMENT

20–14 Additional Readings

The Journal of Economic Perspectives published a collection of papers from a symposium on the “Early

No. 4) and a symposium on “Financial Regulation after the Crisis” in the Winter 2011 issue (Vol. 25, No.

1).

The Squam Lake Group’s Web site provides a number of working papers that focus on various

aspects of regulatory reform (www.squamlakegroup.org). These papers served as the background to the

Squam Lake Report discussed in Supplement 20–13.

For details of the Federal Reserve’s various crisis lending programs and how they affected its balance

sheet, see www.federalreserve.gov/monetarypolicy. See also the series of four lectures on the Fed and the

financial crisis presented by Chairman Ben Bernanke, available on the Federal Reserve Web site at

www.federalreserve.gov/newsevents/lectures/about.htm. Reports and information on the Treasury

Department’s TARP and other elements of the government’s rescue programs are available at

www.financialstability.gov.

A number of books on the financial crisis written for a general audience have been published. These

include Too Big to Fail, by Andrew Sorkin (Viking Penguin, 2009), and In Fed We Trust: Ben Bernanke’s