Answers and Solutions: 20 – 1

Chapter 20

Hybrid Financing: Preferred Stock, Warrants, and

Convertibles

ANSWERS TO END-OF-CHAPTER QUESTIONS

20-1 a. Preferred stock is a hybrid security, having characteristics of both debt and equity. It

is similar to equity in that it (1) is called “stock” and is included in the equity section

of a firm’s balance sheet, (2) has no maturity date, and (3) has payments which are

considered dividends—thus, they are not legally required and are not tax deductible.

However, it is also similar to debt in that it (1) sets a fixed rate for dividends, (2)

affords its holders no voting rights, and (3) has priority over common shareholders in

the event of bankruptcy.

time. This provision is included to prod owners into exercising their warrants.

e. Convertible securities are bonds or preferred stocks that can be exchanged for

(converted into) common stock, under specific terms, at the option of the holder.

Unlike the exercise of warrants, conversion of a convertible security does not provide

additional capital to the issuer.

Answers and Solutions: 20 – 2

g. A “sweetener” is a feature that makes a security more attractive to some investors,

thereby inducing them to accept a lower current yield. Convertible features and

warrants are examples of sweeteners.

20-2 Preferred stock is best thought of as being somewhere between debt (bonds) and equity

(common stock). Like debt, preferred stock imposes a fixed charge on the firm, affords

20-3 The trend in stock prices subsequent to an issue influences whether or not a convertible

issue will be converted, but conversion itself typically does not provide a firm with

20-4 Either warrants or convertibles could be used by a firm that expects to need additional

financing in the future—warrants, because when they are exercised, additional funds will

20-5 a. The value of a warrant depends primarily on the expected growth of the underlying

stock’s price. This growth, in turn, depends in a major way on the plowback of

earnings; the higher the dividend payout, the lower the retention (or plowback) rate;

hence, the slower the growth rate. Thus, warrant values will be higher, other things

held constant, the smaller the firm’s dividend payout ratio. This effect is more

pronounced for long-term than for short-term warrants.

20-6 The statement is made often. It is not really true, as a convertible’s issue price reflects the

20-7 The convertible bond has an expected return which consists of an interest yield (10

percent) plus an expected capital gain. We know the expected capital gain must be at

least 4 percent, because the total expected return on the convertible must be at least equal

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

20-1 Bonds with warrants: $1,000 par value 15-year 5% coupon bonds with annual payments,

trading for $1,000.

Straight debt: $1,000 par value 15-year bonds with 7% annual coupon, also trading for

$1,000.Value of warrants = ?

20-2 Convertible Bond’s Par value = $1,000; Conversion price, Pc = $50;

CR = ?

c

20-3 a. Exercise value = MAX[Current price – Strike price, 0].

Current Strike Exercise

Price Price Value

$ 20 $25 Max[-$5,0] = 0

Answers and Solutions: 20 – 5

b. VPackage = $1,000 =

warrantsthe

of Value

bond theof Value

debtStraight +

= VB + 50($3)

20-4 a. A 10 percent premium results in a conversion price of $42(1.10) = $46.20, while a 30

percent premium leads to a conversion price of $42(1.30) = $54.60. Investment

20-5 a. The premium of the conversion price over the stock price was 14.1 percent:

$62.75/$55 – 1.0 = 0.141 = 14.1%.

b. The before-tax interest savings is calculated as follows:

$400,000,000(0.0875 – 0.0575) = $12 million per year.

However, the after-tax interest savings would be more relevant to the firm and would

Answers and Solutions: 20 – 6

d. If interest rates had not changed, then the value of the straight bond fifteen years after

issue would have been $699.25, calculated as follows: N = 25, I/YR = 8.75, PV = ?,

PMT = 57.5, FV = 1000. Solving, PV = -699.25.

If the stock price is $32.75, then the value of the bond in conversion is

15.936255($32.75) = $521.91.

$699.25 fifteen years later, as calculated above, due to the fact that the bonds are

closer to maturity (because a bond’s value approaches its par value as it gets closer to

maturity). However, the value of the conversion feature would have fallen sharply,

for two reasons. First, the stock price fell from $55 to $32.75, and a decrease in stock

price hurts the value of an option. Second, the time until maturity for the conversion

fell from 40 years to 25 years, and a reduction in the remaining time to exercise an

option hurts its value. Therefore, the bonds probably would have fallen below the

$1,000 issue price.

f. Had the rate of interest fallen to 5.75 percent, which is the coupon rate on the bonds,

Answers and Solutions: 20 – 7

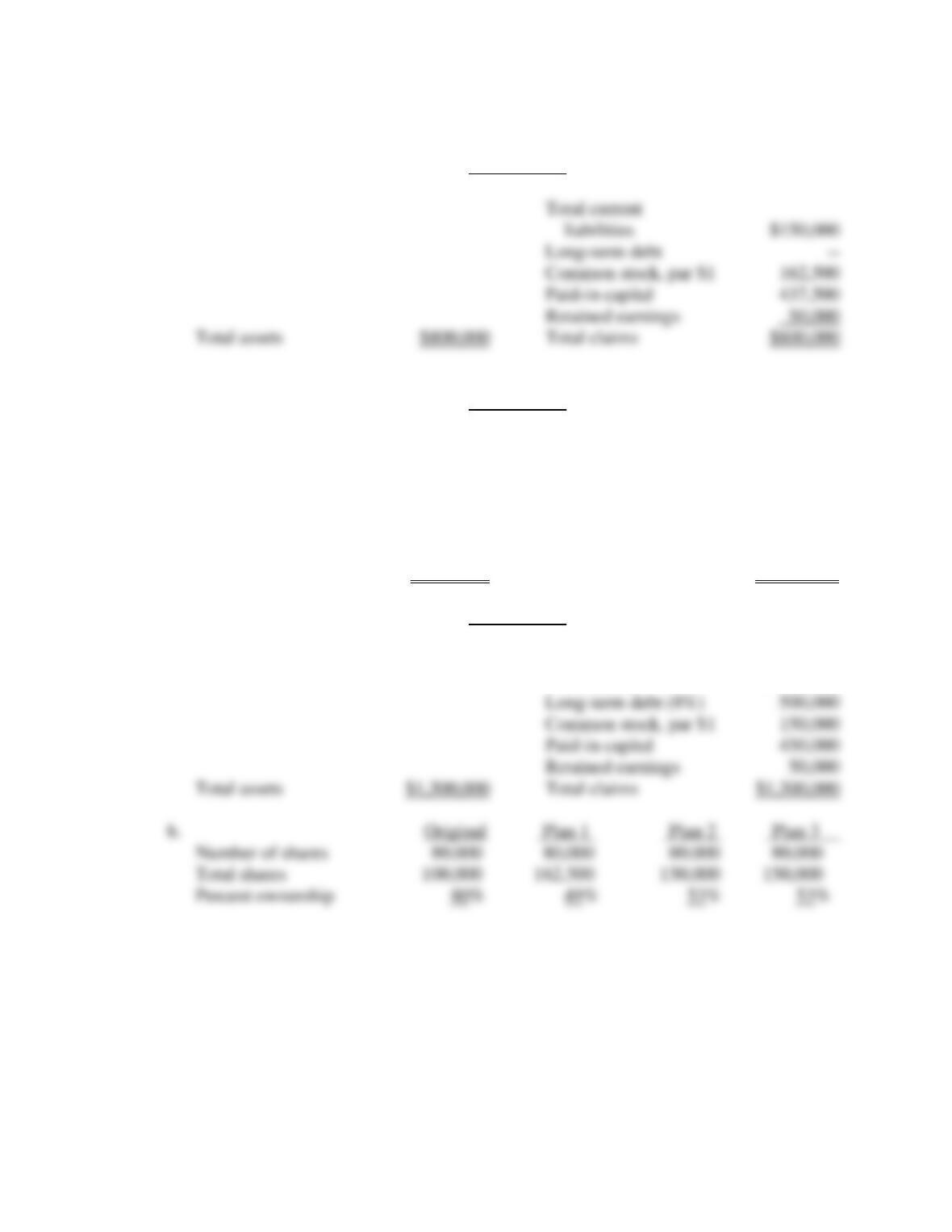

20-6 a. Balance Sheet

Alternative 1

Alternative 2

Total current

liabilities $ 150,000

Long-term debt —

Common stock, par $1 150,000

Paid-in capital 450,000

Retained earnings 50,000

Total assets $ 800,000 Total claims $ 800,000

Alternative 3

Total current

liabilities $ 150,000

Answers and Solutions: 20 – 8

c. Original Plan 1 Plan 2 Plan 3

Total assets $ 550,000 $800,000 $800,000 $1,300,000

EBIT $ 110,000 $160,000 $160,000 $ 260,000

Interest 20,000 0 0 40,000

e. Alternative 1 results in loss of control (to 49 percent) for the firm. Under it, he loses

his majority of shares outstanding. Indicated earnings per share increase, and the debt

ratio is reduced considerably (by 54 percentage points).

Alternative 2 results in maintaining control (53 percent) for the firm. Earnings per

share increase, while a reduction in the debt ratio like that in Alternative 1 occurs.

Under Alternative 3 there is also maintenance of control (53 percent) for the firm.

between 2 and 3.

The differences between these two alternatives, which are illustrated in Parts c

and d, are that the increase in earnings per share is substantially greater under

Alternative 3, but so is the debt ratio. With its low debt ratio (19 percent), the firm is

in a good position for future growth under Alternative 2. However, the 50 percent

ratio under 3 is not prohibitive and is a great improvement over the original situation.

The combination of increased earnings per share and reduced debt ratios indicates

favorable stock price movements in both cases, particularly under Alternative 3.

There is the remote chance that the firm could lose its commercial bank financing

Answers and Solutions: 20 – 9

20-7 a.

Stock data and stock required return:

rd = 9%.

P0 = $23.

Dividend yield = 7%.g = 6%.

rs = Dividend yield + g = 7% + 6% = 13%.

Convertible bond data:

We need to find the number of years that it takes $805 to grow to $1,200 at a 6% interest

rate. Using a financial calculator, I/YR = 6, PV = 805, PMT = 0, FV = -1200; solving, N

= 6.852. So the call will be at the first year end after this, or at Year 7.

We could also calculate this as:

(CR)(P0)(1 + g)N = $1,200

Straight-debt value of the convertible at t = 0:

(Assumes annual payment of coupon)

Answers and Solutions: 20 – 10

Repeating, we can find the straight bond value for different values of N:

V at t = 5 (N = 15): $919.39.

Conversion value:

The stock price should grow at the 6%. The conversion value at Year t is equal to the

expected stock price multiplied by the conversion ratio:

CVt = P0(1.06)N(35).

Repeating for different values of N:

For the expected time of conversion (N = 7), the conversion value is:

CV7 = $23(1.06)7(35) = $1,210.422.

The cash flow at the time of conversion (N = 7), is equal to the conversion value plus the

coupon payment:

Answers and Solutions: 20 – 11

SOLUTION TO SPREADSHEET PROBLEM

Mini Case: 20 – 12

MINI CASE

Paul Duncan, financial manager of Edusoft Inc., is facing a dilemma. The firm was

founded five years ago to provide educational software for the rapidly expanding primary

and secondary school markets. Although Edusoft has done well, the firm’s founder

believes that an industry shakeout is imminent. To survive, Edusoft must grab market

share now, and this will require a large infusion of new capital.

Because he expects earnings to continue rising sharply and looks for the stock price to

follow suit, Mr. Duncan does not think it would be wise to issue new common stock at this

time. On the other hand, interest rates are currently high by historical standards, and with

the firm’s B rating, the interest payments on a new debt issue would be prohibitive. Thus,

he has narrowed his choice of financing alternatives to: (1) preferred stock; (2) bonds with

warrants; or (3) convertible bonds.

As Duncan’s assistant, you have been asked to help in the decision process by answering

the following questions:

a. How does preferred stock differ from both common equity and debt? Is

preferred stock more risky than common stock? What is floating rate preferred

stock?

Answer: Preferred stock is a hybrid—it contains some features that are similar to debt and some

features that are similar to common equity. Like debt, preferred payments to

Mini Case: 20 – 13

b. What is a call option? How can knowledge of call options help a financial

manager to better understand warrants and convertibles?

Answer: A call option is a contract which gives the holder the right, but not the obligation, to

c. Mr. Duncan has decided to eliminate preferred stock as one of the alternatives

and focus on the others. EduSoft’s investment banker estimates that EduSoft

could issue a bond-with-warrants package consisting of a 20-year bond and 27

warrants. Each warrant would have a strike price of $25 and 10 years until

expiration. It is estimated that each warrant, when detached and traded

separately, would have a value of $5. The coupon on a similar bond but without

warrants would be 10%.

1. What coupon rate should be set on the bond with warrants if the total package is

to sell for $1,000?

Answer: If the entire package is to sell for $1,000, then

Mini Case: 20 – 14

c. 2. When would you expect the warrants to be exercised? What is a stepped–up–

exercise price?

Answer: Generally, a warrant will sell in the open market at a premium above its expiration

value, which is the value of the warrant if exercised. Thus, prior to expiration, an

investor who wanted cash would sell his or her warrants in the marketplace rather

than exercise them. Therefore, warrants tend not to be exercised until just before they

expire.

Mini Case: 20 – 15

c. 3. Will the warrants bring in additional capital when exercised? If EduSoft issues

100,000 bond-with-warrant packages, how much cash will EduSoft receive when

the warrants are exercised? How many shares of stock will be outstanding after

the warrants are exercised? (EduSoft currently has 20 million shares

outstanding).

Answer: When exercised, each warrant will bring in an amount equal to the strike price, which

in this case means $25 of equity capital, and holders will receive one share of

common stock per warrant. Note that the strike price is typically set at 10% to 30%

Mini Case: 20 – 16

c. 4. Because the presence of warrants causes a lower coupon rate on the

accompanying debt issue, shouldn’t all debt be issued with warrants? To answer

this, estimate the expected stock price in 10 years when the warrants are

expected to be exercised, then estimate the return to the holders of the bond–

with- warrants packages. Use the corporate valuation model to estimate the

expected stock price in 10 years. Assume that EduSoft’s current value of

operations is $500 million and it is expected to grow at 8% per year.

Answer: Even though the 8.4 percent coupon rate on the bond is below the 10 percent coupon

on straight bonds, the overall cost of a bond-with-warrants issue is generally higher

than that of a straight-debt issue.

Mini Case: 20 – 17

Use these and previous data to find the intrinsic stock price:

Value of operations

$1,079.46

+ Value of cash received at exercise

$67.50

Total intrinsic value of firm

$1,146.96

− Debt

$90.17

Intrinsic value of equity

$1,056.79

÷ Number of shares

$22.70

Intrinsic price per share

$46.55

To find the expected return to the warrant-holder, consider the amount paid for the

initial value of warrants in bond and the amount received as the net payoff at

exercise:

N = 10; PV = −135; PMT = 0; FV = $581.85

Solve for I/YR = rw = 15.73%

rBwW = 10.77%

c. 5. How would you expect the cost of the bond with warrants to compare with the

cost of straight debt? With the cost of common stock (which is 13.4%)?

Answer: This cost is higher than the 10 percent cost of straight debt because, from the

Mini Case: 20 – 18

c. 6. If the corporate tax rate is 40%, what is the after-tax cost of the bond with

warrants?

Answer: Because the bond portion of the package was issued at a discount (its value was only

$865, not $1,000), its after-tax cost of debt is not equal to rd(1-T). You must find the

rate of return given the after-tax coupon.

d. As an alternative to the bond with warrants, Mr. Duncan is considering convertible

bonds. The firm’s investment bankers estimate that Edusoft could sell a 20-year, 8.5

percent annual coupon, callable convertible bond for its $1,000 par value, whereas a

straight-debt issue would require a 10 percent coupon. The convertibles would be

call protected for 5 years, the call price would be $1,100, and the company would

probably call the bonds as soon as possible after their conversion value exceeds

$1,200. Note, though, that the call must occur on an issue date anniversary.

Edusoft’s current stock price is $20, its last dividend was $1.00, and the dividend is

expected to grow at a constant 8 percent rate. The convertible could be converted

into 40 shares of Edusoft stock at the owner’s option.

1. What conversion price is built into the bond?

Answer: Conversion Price = PC =

received Shares #

Par value

=

40

000,1$

= $25.

Mini Case: 20 – 19

d. 2. What is the convertible’s straight-debt value? What is the implied value of the

convertibility feature?

Answer: Since the required rate of return on a 20-year straight bond is 10 percent, the value of

an 8.5 percent annual coupon bond is $872.30:

d. 3. What is the formula for the bond’s expected conversion value in any year?

What is its conversion value at year 0? At year 10?

Answer: The conversion value in any year is simply the value of the stock one would receive

upon converting. Since Edusoft is a constant growth stock, its price is expected to

d. 4. What is meant by the “floor value” of a convertible? What is the convertible’s

expected floor value at year 0? At year 10?

Answer: The floor value is simply the higher of the straight-debt value and the conversion

value. At year 0, the straight-debt value is $872.30 while the conversion value is

Mini Case: 20 – 20

d. 5. Assume that Edusoft intends to force conversion by calling the bond as soon as

possible after its conversion value exceeds 20 percent above its par value, or

1.2($1,000) = $1,200. When is the issue expected to be called? (Hint: recall that

the call must be made on an anniversary date of the issue.)

Answer: The easiest way to find the year conversion is expected is by recognizing that the

conversion value begins at $800, grows at the rate of 8% per year, and must rise to

one. However, the HP-17b gives the unrounded answer 5.27.)

d. 6. What is the expected cost of capital for the convertible to Edusoft? Does this cost

appear to be consistent with the riskiness of the issue?

Answer: The firm would receive $1,000 now, would make coupon payments of $85 for 6

years, and then would issue stock worth 40($20)(1.08)6 = $1,269.50. Thus, the cash

flow stream would look like this:

d. 7. What is the after-tax cost of the convertible bond?

Answer: Use the after-tax coupon payment, then find the rate of return.

Mini Case: 20 – 21

e. Mr. Duncan believes that the costs of both the bond with warrants and the

convertible bond are close enough to one another to call them even, and also

consistent with the risks involved. Thus, he will make his decision based on

other factors. What are some of the factors which he should consider?

Answer: One factor that should be considered is the firm’s future needs for capital. If Edusoft

anticipates a continuing need for capital, then warrants may be favored, because their

exercise will bring in additional equity capital without the need to retire the

f. How do convertible bonds help reduce agency costs?

Answer: Agency costs can arise due to conflicts between shareholders and bondholders, in the

form of asset substitution (or bait-and-switch.) This happens when the firm issues

low cost straight debt, then invests in risky projects. Bondholders suspect this, so