interactive activity

Chapter 20

Uncertainty, Risk, and

Private Information

1. For each of the following situations, calculate the expected value.

a. Tanisha owns one share of IBM stock, which is currently trading at $80. There

is a 50% chance that the share price will rise to $100 and a 50% chance that it

will fall to $70. What is the expected value of the future share price?

b. Sharon buys a ticket in a small lottery. There is a probability of 0.7 that she

will win nothing, of 0.2 that she will win $10, and of 0.1 that she will win $50.

What is the expected value of Sharon’s winnings?

c. Aaron is a farmer whose rice crop depends on the weather. If the weather is

favorable, he will make a profit of $100. If the weather is unfavorable, he will

make a profit of −$20 (that is, he will lose money). The weather forecast reports

that the probability of weather being favorable is 0.9 and the probability of

weather being unfavorable is 0.1. What is the expected value of Aaron’s profit?

$88.

2. Vicky N. Vestor is considering investing some of her money in a startup

company. She currently has income of $4,000, and she is considering investing

$2,000 of that in the company. There is a 0.5 probability that the company will

succeed and will pay out $8,000 to Vicky (her original investment of $2,000 plus

$6,000 of the company’s profits). And there is a 0.5 probability that the company

will fail and Vicky will get nothing (and lose her investment). The accompanying

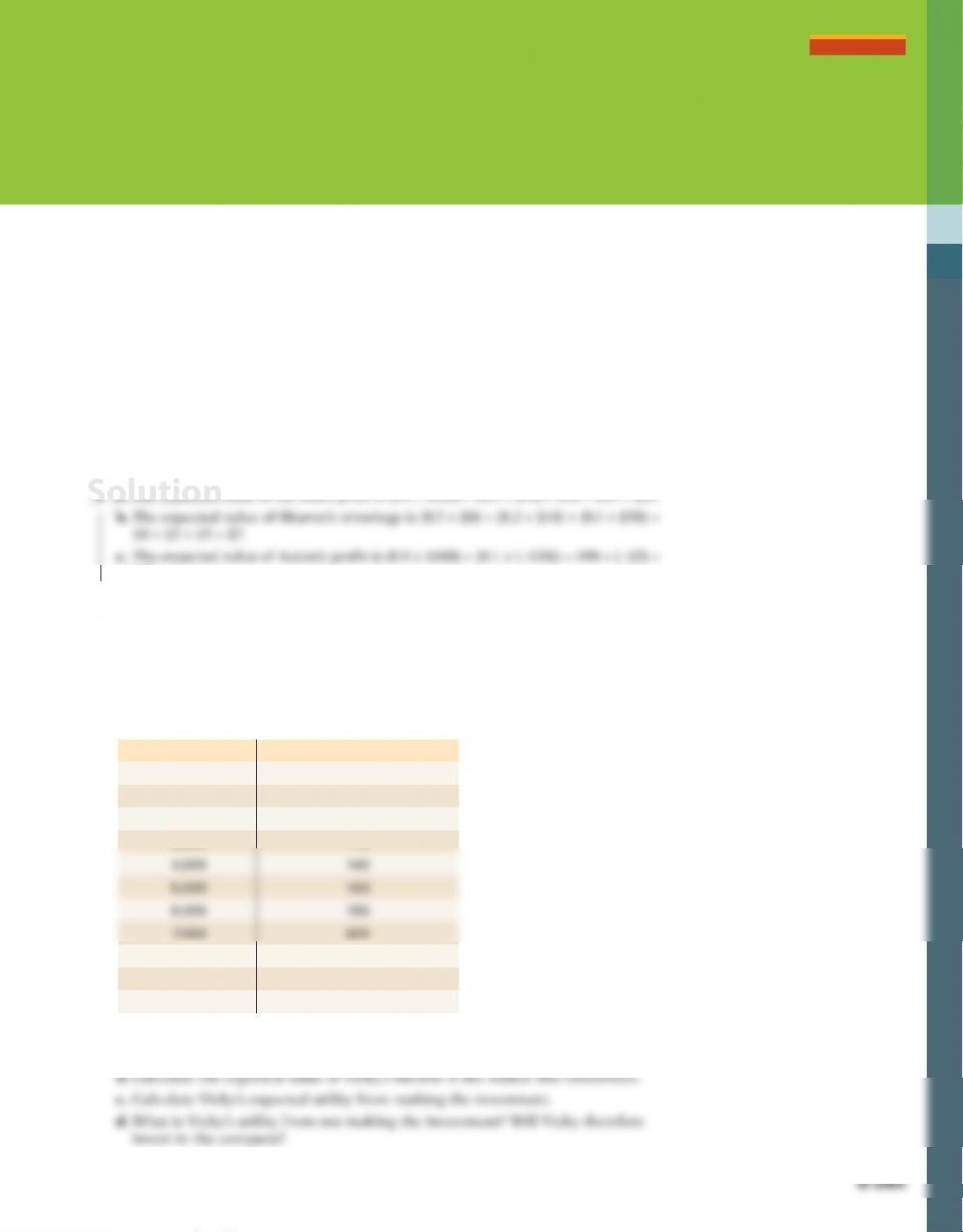

table illustrates Vicky’s utility function.

Income Total utility (utils)

$0 0

1,000 50

2,000 85

3,000 115

8,000 215

9,000 229

10,000 241

a. Calculate Vicky’s marginal utility of income for each income level. Is Vicky

risk-averse?

S-286 Chapter 20 Uncertainty, risk, and Private information

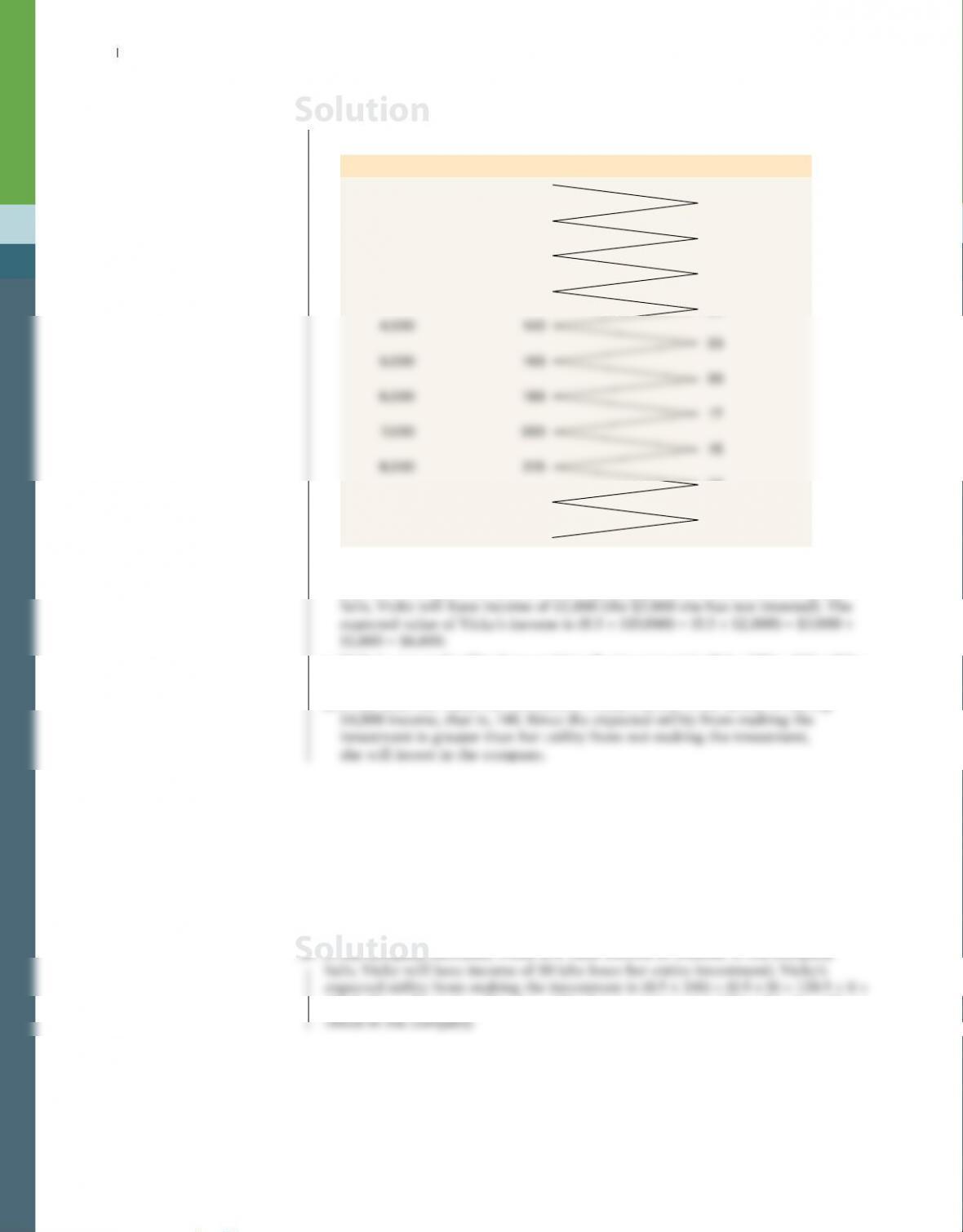

2. a. Vicky’s marginal utility of income is given in the accompanying table. Since

her marginal utility declines, she is risk–averse.

Income

$0

Total utility (utils)

0

Marginal utility (utils)

50

1,000 50

35

2,000 85

30

3,000 115

25

14

9,000 229

12

10,000 241

b. If the company succeeds, Vicky will have income of $10,000 (the $2,000 she

did not invest plus the $8,000 the company pays out to her). If the company

c. Vicky’s expected utility from making the investment is (0.5 × 241) + (0.5 × 85) =

120.5 + 42.5 = 163.

d. If she does not make the investment, Vicky’s utility is the utility of having

3. Vicky N. Vestor’s utility function was given in Problem 2. As in Problem 2, Vicky

currently has income of $4,000. She is considering investing in a startup com-

pany, but the investment now costs $4,000 to make. If the company fails, Vicky

will get nothing from the company. But if the company succeeds, she will get

$10,000 from the company (her original investment of $4,000 plus $6,000 of the

company’s profits). Each event has a 0.5 probability of occurring. Will Vicky

invest in the company?

3. If the company succeeds, Vicky will have income of $10,000. If the company

120.5. Since this is less than her utility from not investing (140 utils), she will not

Solution

Solution

4. You have $1,000 that you can invest. If you buy Ford stock, you face the follow-

ing returns and probabilities from holding the stock for one year: with a prob–

ability of 0.2 you will get $1,500; with a probability of 0.4 you will get $1,100; and

with a probability of 0.4 you will get $900. If you put the money into the bank, in

one year’s time you will get $1,100 for certain.

a. What is the expected value of your earnings from investing in Ford stock?

b. Suppose you are risk–averse. Can we say for sure whether you will invest in

Ford stock or put your money into the bank?

5. Wilbur is an airline pilot who currently has income of $60,000. If he gets sick

and loses his flight medical certificate, he loses his job and has only $10,000

income. His probability of staying healthy is 0.6, and his probability of getting

sick is 0.4. Wilbur’s utility function is given in the accompanying table.

Income Total utility (utils)

$0 0

10,000 60

a. What is the expected value of Wilbur’s income?

b. What is Wilbur’s expected utility?

Wilbur thinks about buying “loss-of-license” insurance that will compensate him

if he loses his flight medical certificate.

c. One insurance company offers Wilbur full compensation for his income loss

(that is, the insurance company pays Wilbur $50,000 if he loses his flight

medical certificate), and it charges a premium of $40,000. That is, regardless

of whether he loses his flight medical certificate, Wilbur’s income after insur-

ance will be $20,000. What is Wilbur’s utility? Will he buy the insurance?

d. What is the highest premium Wilbur would just be willing to pay for full

insurance (insurance that completely compensates him for the income loss)?

6. According to the FBI’s Uniform Crime Reports, approximately 1 in 379 cars was

stolen in the United States in 2014. Beth owns a car worth $20,000 and is con-

sidering purchasing an insurance policy to protect herself from car theft. For

the following questions, assume that the chance of car theft is the same in all

regions and across all car models.

a. What should the premium for a fair insurance policy have been in 2014 for a

policy that replaces Beth’s car if it is stolen? (Hint: In your calculation, round

up to three decimal places.)

b. Suppose an insurance company charges 0.6% of the car’s value for a policy

that pays for replacing a stolen car. How much will the policy cost Beth?

c. Will Beth purchase the insurance in part b if she is risk-neutral?

6. a. The premium for a fair insurance policy is equal to the expected value of

Beth’s claim. Since the probability of having her car stolen is 1/379 = 0.003, the

expected value of Beth’s claim is 0.003 × $20,000 = $60.

b. The premium for this insurance policy is 0.006 × $20,000 = $120.

7. Hugh’s income is currently $5,000. His utility function is shown in the accompa-

nying table.

Income Total utility (utils)

$0 0

1,000 100

2,000 140

3,000 166

4,000 185

a. Calculate Hugh’s marginal utility of income. What is his attitude toward risk?

b. Hugh is thinking about gambling in a casino. With a probability of 0.5 he

will lose $3,000, and with a probability of 0.5 he will win $5,000. What is

the expected value of Hugh’s income? What is Hugh’s expected utility? Will

he decide to gamble? (Suppose that he gets no extra utility from going to the

casino.)

c. Suppose that the “spread” (how much he can win versus how much he can

lose) of the gamble narrows, so that with a probability of 0.5 Hugh will lose

$1,000, and with a probability of 0.5 he will win $3,000. What is the expected

value of Hugh’s income? What is his expected utility? Is this gamble better for

him than the gamble in part b? Will he decide to gamble?

Solution

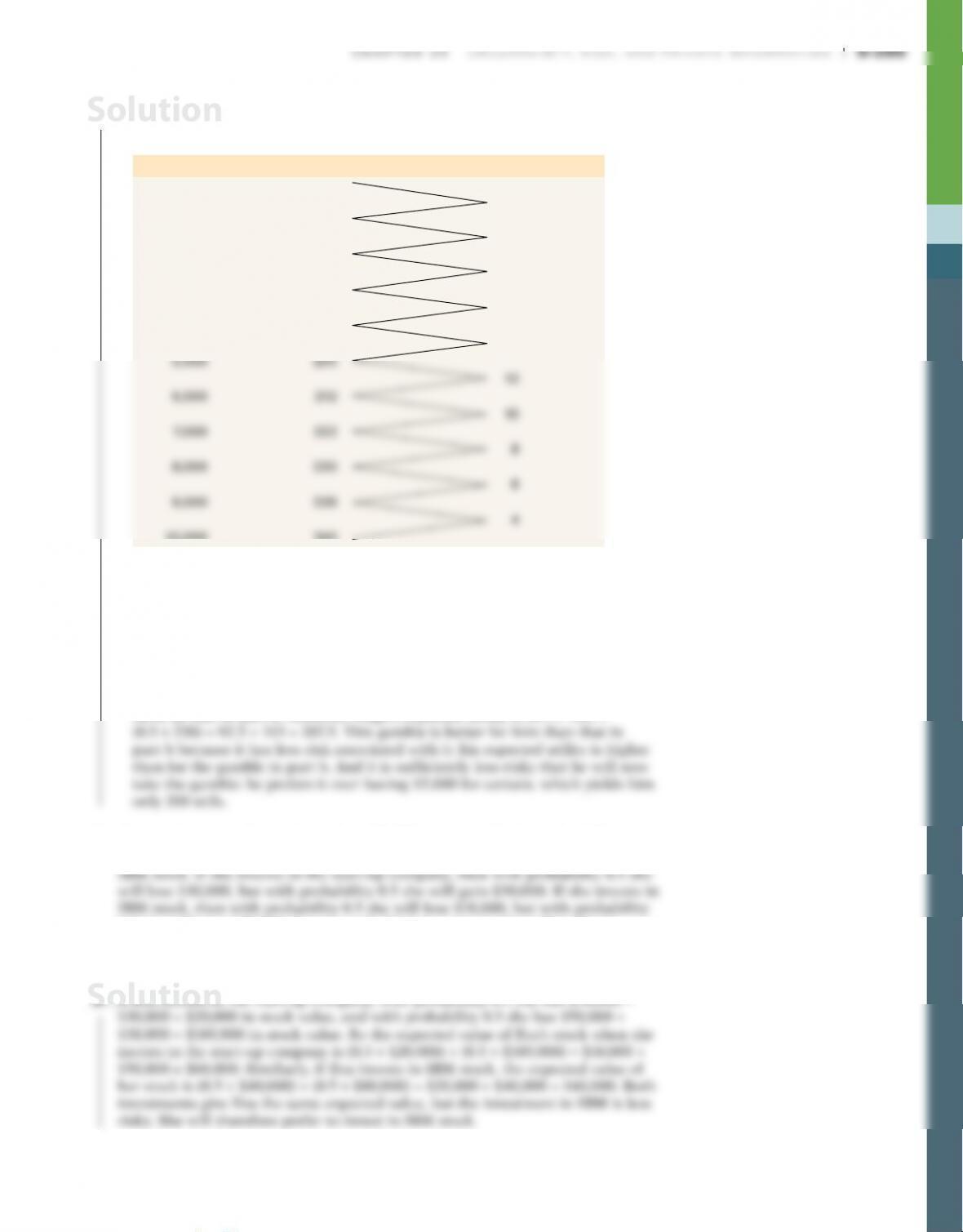

7. a. Hugh’s marginal utility is given in the accompanying table. Since his marginal

utility is diminishing, he is risk–averse.

Income

$0

Total utility (utils)

0

Marginal utility (utils)

100

1,000 100

40

2,000 140

26

3,000 166

19

4,000 185

15

10,000 240

b. Hugh will have $2,000 income with probability 0.5 and $10,000 income

with probability 0.5. The expected value of his income is (0.5 × $2,000) +

(0.5 × $10,000) = $1,000 + $5,000 = $6,000. His expected utility is (0.5 × 140) +

(0.5 × 240) = 70 + 120 = 190. His utility from not gambling is the utility of

having $5,000 for certain, which is 200. That is, he will not take the gamble.

c. Hugh will have $4,000 income with probability 0.5 and $8,000 income

with probability 0.5. The expected value of his income is (0.5 × $4,000) +

(0.5 × $8,000) = $2,000 + $4,000 = $6,000. This gamble has the same expected

value as that in part b. However, Hugh’s expected utility is (0.5 × 185) +

8. Eva is risk-averse. Currently she has $50,000 to invest. She faces the following

choice: she can invest in the stock of a start-up company, or she can invest in

0.5 she will gain $30,000. Can you tell which investment she will prefer to

make?

Solution

S-290 Chapter 20 Uncertainty, risk, and Private information

is $100. The fortunes of each company are closely linked to the weather. When it

is warm, the value of Ted and Larry’s stock rises to $150 but the value of Ethel’s

stock falls to $60. When it is cold, the value of Ethel’s stock rises to $150 but

the value of Ted and Larry’s stock falls to $60. There is an equal chance of the

weather being warm or cold.

a. If you invest all your money in Ted and Larry’s, what is your expected stock

value? What if you invest all your money in Ethel’s?

b. Suppose you diversify and invest half of your $1,000 in each company. How

much will your total stock be worth if the weather is warm? What if it is cold?

c. Suppose you are risk–averse. Would you prefer to put all your money in Ted

and Larry’s, as in part a? Or would you prefer to diversify, as in part b?

10. LifeStrategy Conservative Growth and Energy are two portfolios constructed

and managed by the Vanguard Group of mutual funds, comprised of stocks of

conservatively managed U.S. companies and stocks of U.S. energy companies.

The accompanying table shows historical annualized return from the period

2004 to 2014, which suggest the expected value of the annual percentage returns

associated with these portfolios.

Portfolio Expected value of return (percent)

a. Which portfolio would a risk-neutral investor prefer?

b. Juan, a risk–averse investor, chooses to invest in the LifeStrategy Conservative

Growth portfolio. What can be inferred about the risk of the two portfolios

from Juan’s choice of investment? Based on historical performance, would a

risk-neutral investor ever choose LifeStrategy Conservative Growth?

c. Juan is aware that diversification can reduce risk. He considers a portfolio in

which half his investment is in conservatively managed companies and the other

(0.5 × 0.1266)) × 100 = 9.27%. If the two portfolios are not correlated (what

happens to one portfolio is an independent event from what happens to the

11. You are considering buying a second-hand Volkswagen. From reading car maga–

zines, you know that half of all Volkswagens have problems of some kind (they are

“lemons”) and the other half run just fine (they are “plums”). If you knew that you

were getting a plum, you would be willing to pay $10,000 for it: this is how much

a plum is worth to you. You would also be willing to buy a lemon, but only if its

price was no more than $4,000: this is how much a lemon is worth to you. And

someone who owns a plum would be willing to sell it at any price above $8,000.

Someone who owns a lemon would be willing to sell it for any price above $2,000.

a. For now, suppose that you can immediately tell whether the car that you are

being offered is a lemon or a plum. Suppose someone offers you a plum. Will

there be trade?

S-292 Chapter 20 Uncertainty, risk, and Private information

12. You own a company that produces chairs, and you are thinking about hiring

one more employee. Each chair produced gives you revenue of $10. There are

two potential employees, Fred Ast and Sylvia Low. Fred is a fast worker who

produces ten chairs per day, creating revenue for you of $100. Fred knows that

he is fast and so will work for you only if you pay him more than $80 per day.

Sylvia is a slow worker who produces only five chairs per day, creating revenue

for you of $50. Sylvia knows that she is slow and so will work for you if you pay

her more than $40 per day. Although Sylvia knows she is slow and Fred knows

he is fast, you do not know who is fast and who is slow. So this is a situation of

adverse selection.

a. Since you do not know which type of worker you will get, you think about

what the expected value of your revenue will be if you hire one of the two.

What is that expected value?

b. Suppose you offered to pay a daily wage equal to the expected revenue you cal-

culated in part a. Whom would you be able to hire: Fred, or Sylvia, or both, or

neither?

13. For each of the following situations, do the following: first describe whether it

is a situation of moral hazard or of adverse selection. Then explain what inef-

ficiency can arise from this situation and explain how the proposed solution

reduces the inefficiency.

a. When you buy a second-hand car, you do not know whether it is a lemon (low

14. Kory owns a house that is worth $300,000. If the house burns down, she loses all

$300,000. If the house does not burn down, she loses nothing. Her house burns

down with a probability of 0.02. Kory is risk–averse.

a. What would a fair insurance policy cost?

b. Suppose an insurance company offers to insure her fully against the loss

from the house burning down, at a premium of $1,500. Can you say for sure

whether Kory will or will not take the insurance?

c. Suppose an insurance company offers to insure her fully against the loss

from the house burning down, at a premium of $6,000. Can you say for sure

whether Kory will or will not take the insurance?

14. a. A fair insurance policy is one with a premium equal to the expected value of

the claim. The expected value of Kory’s claim is (0.02 × $300,000) + (0.98 × $0) =

$6,000.

b. Kory will take this insurance. It is better than fair: the expected value of her

claim is $6,000, but she only pays $1,500 for this insurance. Taking this insur-

ance will increase Kory’s expected income. Since we know that she is risk–

averse, we know for sure that she will take this insurance.

WORK IT OUT Interactive step-by-step help with solving this

problem can be found online.

15. You have $1,000 that you can invest. If you buy General Motors stock, then,

$800. If you put the money into the bank, in one year’s time you will get

$1,100 for certain.

a. What is the expected value of your earnings from investing in General

Motors stock?

15. a. The expected value of your earnings from investing in General Motors stock

is (0.4 × $1,600) + (0.4 × $1,100) + (0.2 × $800) − $1,000 = $640 + $440 + $160 −

Solution

Solution