Answers and Solutions: 19 – 1

Chapter 19

Lease Financing

ANSWERS TO END-OF-CHAPTER QUESTIONS

19-1 a. The lessee is the party leasing the property. The party receiving the payments from

the lease (that is, the owner of the property) is the lessor.

b. An operating lease, sometimes called a service lease, provides for both financing and

maintenance. Generally, the operating lease contract is written for a period

considerably shorter than the expected life of the leased equipment, and contains a

amounts to actually borrowing money guaranteed by the lessee, it doesn’t appear on

the company’s books as an obligation. A special purpose entity (SPE) is a company

set up to facilitate the creation of a synthetic lease. It borrows money that is

guaranteed by the lessee, purchases equipment, and leases it to the lessee. Its purpose

is keep the lessee from having to capitalize the lease and carry its payments on its

books as a liability.

Answers and Solutions: 19 – 2

e. A guideline lease is a lease that meets all of the IRS requirements for a genuine lease.

A guideline lease is often called a tax-oriented lease. If a lease meets the IRS

guidelines, the IRS allows the lessor to deduct the asset’s depreciation and allows the

lessee to deduct the lease payments.

f. The residual value is the market value of the leased property at the expiration of the

lease. The estimate of the residual value is one of the key elements in lease analysis.

advantage to leasing.

The lessor’s analysis involves determining the rate of return on the proposed

lease. If the rate of return (or IRR) of the lease cash flows exceeds the lessor’s

opportunity cost of capital, the lease is a good investment. This is equivalent to

analyzing whether the NPV of the lease is positive.

h. The net advantage to leasing (NAL) gives the dollar value of the lease to the lessee.

It is, in a sense, the NPV of leasing versus owning.

19-2 An operating lease is usually cancelable and includes maintenance. Operating leases are,

frequently, for a period significantly shorter than the economic life of the asset, so the

lessor often does not recover his full investment during the period of the basic lease. A

financial lease, on the other hand, is fully amortized and generally does not include

maintenance provisions. An operating lease would probably be used for a fleet of trucks,

while a financial lease would be used for a manufacturing plant.

Answers and Solutions: 19 – 3

19-3 You would expect to find that lessees, in general, are in relatively low income-tax

brackets, while lessors tend to be in high tax brackets. The reason for this is that owning

19-4 The banks, when they initially went into leasing, were paying relatively high tax rates.

However, since municipal bonds are tax-exempt, their heavy investments in municipals

19-5 a. Pros:

• The use of the leased premises or equipment is actually an exclusive right, and the

payment for the premises is a liability that often must be met. Therefore, leases

operating results; that is, return on investment data.

b. Cons:

• Because the firm does not actually own the leased property, the legal aspect can

be cited as an argument against capitalization.

when assets are purchased.

19-6 Lease payments, like depreciation, are deductible for tax purposes. If a 20-year asset

were depreciated over a 20-year life, depreciation charges would be 1/20 per year (more

19-7 In fact, Congress did this in 1981. Depreciable lives were shorter than before; corporate

tax rates were essentially unchanged (they were lowered very slightly on income below

$50,000); and the investment tax credit had been improved a bit by the easing of

recapture if the asset was held for a short period. As a result, companies that were either

19-8 A cancellation clause would reduce the risk to the lessee since the firm would be allowed

to terminate the lease at any point. Since the lease is less risky than a standard financial

lease, and less risky than straight debt, which cannot usually be prepaid without a

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

19-1 a. (1) Reynolds’ current debt ratio is $400/$800 = 50%.

(2) If the company purchased the equipment its balance sheet would look like:

Current assets $300 Debt (including lease) $600

(3) If the company leases the asset and does not capitalize the lease, its debt ratio =

$400/$800 = 50%.

b. The company’s financial risk (assuming the implied interest rate on the lease is

equivalent to the loan) is no different whether the equipment is leased or purchased.

19-2 Cost of owning:

0 1 2

(200) 40 40

PV at 6% = -$127.

Cost of leasing:

Answers and Solutions: 19 – 6

19-3 a. Balance sheets before lease is capitalized:

Energen

Balance Sheet (Owns new assets)

(Thousands of Dollars)

Debt/assets ratio = $100/$200 = 50%.

Hastings Corporation

Balance Sheet (Leases as operating lease)

(Thousands of Dollars)

Debt/assets ratio = $50/$150 = 33%.

Answers and Solutions: 19 – 7

b. Balance sheet after lease is capitalized:

Hastings Corporation

Balance Sheet (Capitalizes lease)

(Thousands of Dollars)

19-4

I. Cost of Owning:

0

1

2

3

4

After-tax loan paymentsa

($135,000)

($135,000)

($135,000)

($1,635,000)

Depr. tax savingsb

$199,980

$266,700

$88,860

$44,460

Residual value

$250,000

Tax on residual

($100,000)

Net cash flow

$0

$4,980

$131,700

($46,140)

($1,440,540)

1

2

3

4

Lease payment (AT)

Net cash flow

Answers and Solutions: 19 – 8

III. Cost Comparison

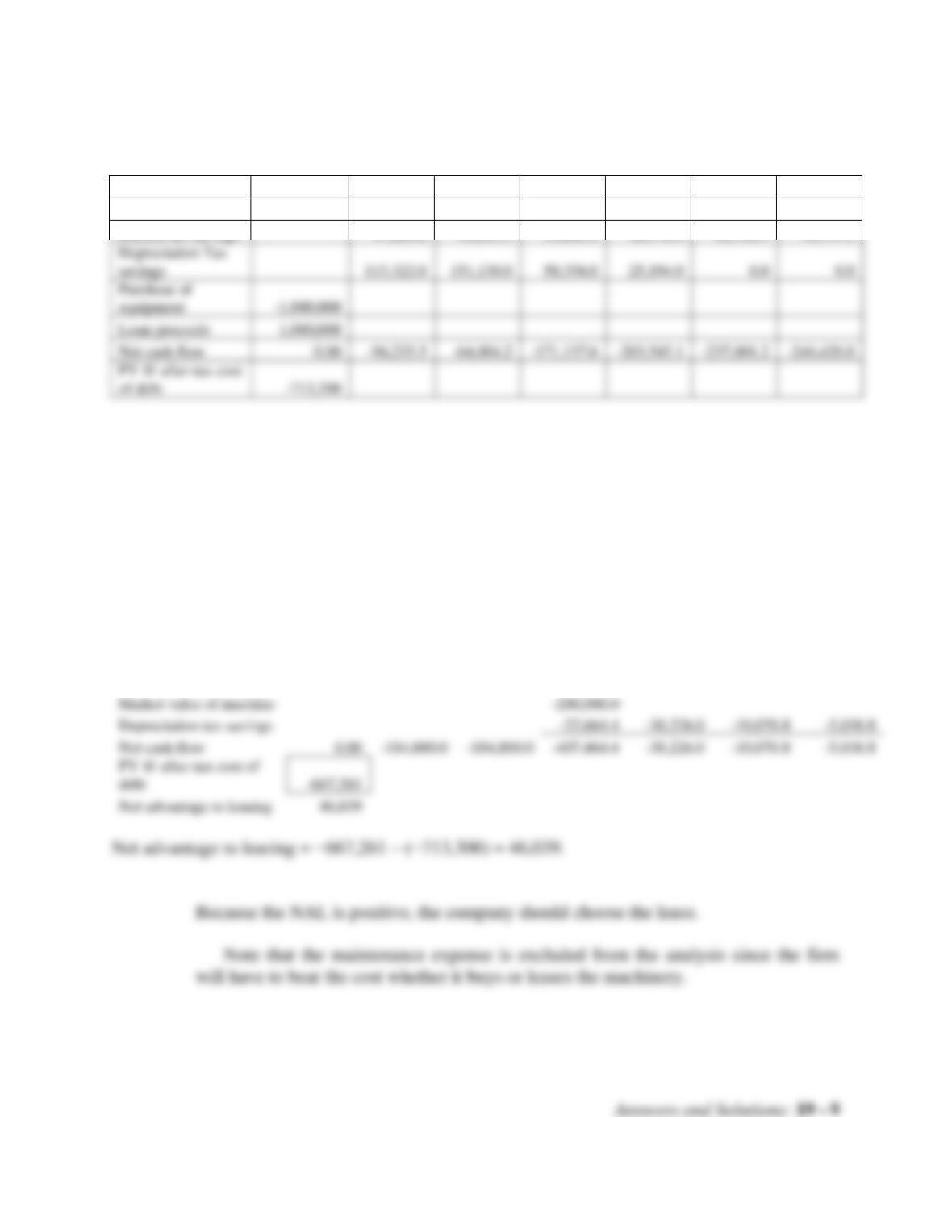

Net advantage to leasing (NAL)= PV of leasing – PV of owning

= −$777,532.77 – (−$885,679.47)

= $108,146.69.

19-5 a. Borrow and buy analysis:

Depreciation Schedule of New Equipment

Year

0

1

2

3

4

5

6

new purchase

Depreciation

74,100

Book Value

74,100

Depreciation rates for

Amortization Schedule of Loan

Year

0

1

2

3

4

5

6

Loan payment

Interest

140,000.0

123,598.0

104,899.6

Principal

117,157.5

133,559.5

152,257.9

173,574.0

197,874.3

225,576.8

Ending Loan Balance

882,842.5

749,283.0

597,025.1

423,451.1

225,576.8

257,157.5

257,157.5

257,157.5

257,157.5

257,157.5

257,157.5

Cost of Owning

Year

0

1

2

3

4

5

6

Loan payments

-257,157.5

-257,157.5

-257,157.5

-257,157.5

-257,157.5

-257,157.5

Interest tax savings

savings

Purchase of

equipment

Loan proceeds

1,000,000

Net cash flow

-171,137.6

-203,545.1

-237,001.2

-246,420.0

of debt

Depreciation Schedule of Used Equipment

Year

0

1

2

3

4

5

6

Depreciation Schedule

for used purchase

33.33%

44.45%

14.81%

7.41%

Depreciation

66,660

88,900

29,620

14,820

Book Value

200,000

133,340

44,440

14,820

0

Cost of Leasing

Year

0

1

2

3

4

5

6

After-tax lease payment

-184,800.0

-184,800.0

-184,800.0

Market value of machine

-200,000.0

Depreciation tax savings

Net cash flow

-184,800.0

-184,800.0

-407,464.4

debt

Net advantage to leasing

Notes:

aDiscount rate = 14% x (1 – T) = 14% x (1 – 0.34) = 9.24%.

bDepreciable basis = Cost = $1,000,000. MACRS allowances = 33.33%, 44.45%,

14.81%. Depreciation tax savings = T(Depreciation).

cCost of purchasing the machinery after the lease expires. Note that since the firm is

purchasing the machine at the end of the lease, there are no tax effects due to the

b. Using Goal Seek, we find that the purchase price can go up to $245,703 before the

NAL becomes negative.

c. We assume that the company will buy the equipment at the end of 3 years if the lease

plan is used; hence, the $200,000 is an added cost under leasing. We discounted it,

and the resulting depreciation tax shields, at 9.24 percent, but these cash flows are

risky, so should we use a higher rate? Since the purchase cost net of the present value

Answers and Solutions: 19 – 11

SOLUTION TO SPREADSHEET PROBLEM

MINI CASE

Lewis Securities Inc. has decided to acquire a new market data and quotation system for its

Richmond home office. The system receives current market prices and other information

from several on-line data services, then either displays the information on a screen or

stores it for later retrieval by the firm’s brokers. The system also permits customers to call

up current quotes on terminals in the lobby.

The equipment costs $1,000,000, and, if it were purchased, Lewis could obtain a term

loan for the full purchase price at a 10 percent interest rate. Although the equipment has a

six-year useful life, it is classified as a special-purpose computer, so it falls into the MACRS

3-year class. If the system were purchased, a 4-year maintenance contract could be

obtained at a cost of $20,000 per year, payable at the beginning of each year. The

equipment would be sold after 4 years, and the best estimate of its residual value at that

time is $200,000. However, since real-time display system technology is changing rapidly,

the actual residual value is uncertain.

As an alternative to the borrow-and-buy plan, the equipment manufacturer informed

Lewis that Consolidated Leasing would be willing to write a 4-year guideline lease on the

equipment, including maintenance, for payments of $260,000 at the beginning of each year.

Lewis’s marginal federal-plus-state tax rate is 40 percent. You have been asked to analyze

the lease-versus-purchase decision, and in the process to answer the following questions:

a. 1. Who are the two parties to a lease transaction?

a. 2. What are the five primary types of leases, and what are their characteristics?

Answer: The five primary types of leases are operating, financial, sale and leaseback,

combination, and synthetic. An operating lease, sometimes called a service lease,

provides for both financing and maintenance. Generally, the operating lease contract

a. 3. How are leases classified for tax purposes?

Answer: A guideline lease is a lease that meets all of the IRS requirements for a genuine lease.

a. 4. What effect does leasing have on a firm’s balance sheet?

Answer: If the lease is classified as a capital lease, it is shown directly on the balance sheet. If

a. 5. What effect does leasing have on a firm’s capital structure?

Mini Case: 19 – 14

b. 1. What is the present value cost of owning the equipment? (Hint: set up a time

line which shows the net cash flows over the period t = 0 to t = 4, and then find

the PV of these net cash flows, or the PV cost of owning.)

Answer: To develop the cost of owning, we begin by constructing the depreciation schedule:

depreciable basis = $1,000,000.

MACRS Depreciation End-Of-Year

Year Rate Expense Book Value

1 0.3333 $ 333,300 $666,700

Mini Case: 19 – 15

b. 2. Explain the rationale for the discount rate you used to find the PV.

Answer: The proper discount rate depends on (1) the riskiness of the cash flow stream and (2)

the general level of interest rates. The loan payments and the maintenance costs are

fixed by contract, hence are not at all risky. The depreciation deductions are also

“locked in,” but the tax rate could change. Thus, depreciation cash flows (tax

c. What is Lewis’s present value cost of leasing the equipment? (Hint: again,

construct a time line.)

Answer: If Lewis leased the equipment, its only cash flows would be the after-tax lease

payments:

Mini Case: 19 – 16

d. What is the net advantage to leasing (NAL)? Does your analysis indicate that

Lewis should buy or lease the equipment? Explain.

Answer: The net advantage to leasing (NAL) is $18,751:

e. Now assume that the equipment’s residual value could be as low as $0 or as high

as $400,000, but that $200,000 is the expected value. Since the residual value is

riskier than the other cash flows in the analysis, this differential risk should be

incorporated into the analysis. Describe how this could be accomplished. (No

calculations are necessary, but explain how you would modify the analysis if

calculations were required.) What effect would increased uncertainty about the

residual value have on Lewis’s lease-versus-purchase decision?

Answer: First, note that the residual value in a lease analysis will be shown either in the “cost

of owning section” or in the “cost of leasing” section, depending on whether or not

the company plans to continue using the leased asset at the expiration of the basic

lease. If the lessee plans to continue using the equipment, then it will have to be

Mini Case: 19 – 17

In the case at hand, the lessor, not the lessee, will own the asset at the end of the

lease, so the lessor bears the residual value risk. In effect, the lease transaction passes

f. The lessee compares the cost of owning the equipment with the cost of leasing it.

Now put yourself in the lessor’s shoes. In a few sentences, how should you

analyze the decision to write or not write the lease?

Answer: The lessor should view “writing” the lease as an investment, so the lessor should

Mini Case: 19 – 18

g. 1. Assume that the lease payments were actually $280,000 per year, that

Consolidated Leasing is also in the 40 percent tax bracket, and that it also

forecasts a $200,000 residual value. Also, to furnish the maintenance support,

Consolidated would have to purchase a maintenance contract from the

manufacturer at the same $20,000 annual cost, again paid in advance.

Consolidated Leasing can obtain an expected 10 percent pre-tax return on

investments of similar risk. What would Consolidated’s NPV and IRR of leasing

be under these conditions?

Answer: The lessor must invest $1,000,000 to buy the equipment, but then it expects to receive

tax benefits and lease payments over the life of the lease. Note that the depreciation

expenses calculated earlier also apply to the lessor, so we have this cash flow stream:

g. 2. What do you think the lessor’s NPV would be if the lease payment were set at

$280,000 per year? (Hint: the lessor’s cash flows would be a “mirror image” of

the lessee’s cash flows.)

Answer: With lease payments of $260,000, the lessor’s cash flows would be the “mirror

image” of the lessee’s NAL—the same dollars, but with signs reversed. Therefore, the

Mini Case: 19 – 19

h. Lewis’s management has been considering moving to a new downtown location,

and they are concerned that these plans may come to fruition prior to the

expiration of the lease. If the move occurs, Lewis would buy or lease an entirely

new set of equipment, and hence management would like to include a

cancellation clause in the lease contract. What impact would such a clause have

on the riskiness of the lease from Lewis’s standpoint? From the lessor’s

standpoint? If you were the lessor, would you insist on changing any of the lease

terms if a cancellation clause were added? Should the cancellation clause

contain any restrictive covenants and/or penalties of the type contained in bond

indentures or provisions similar to call premiums?

Answer: A cancellation clause would lower the risk of the lease to Lewis, the lessee, because

then it would not be obligated to make the lease payments for the entire term of the

lease. If its situation changed, so that Lewis either no longer needed the equipment or